PXD - Pioneer Natural Resources: Throttling Back Shareholder Returns Was Necessary

2023-05-01 16:59:28 ET

Summary

- Pioneer Natural Resources has an industry-leading shareholder return model, that at times has allowed it to return over 100% free cash flow to shareholders.

- During the 2023 Q1 conference call, the company rolled out plans to dial back their current distribution pace to 75% FCF.

- This move was necessary. The pace of 2022 could not be sustained for any significant amount of time without taking on debt. This allows for a reloading of its arsenal.

- In this article, we will explore the long-term implications and my views on the current valuation.

Thesis

Pioneer Natural Resources ( PXD ) released Q1 earnings that were down from Q4 due to lower crude and natural gas prices. As a result, the dividend was roughly 40% lower than the previous quarter.

More importantly, during the conference call, management outlined their intention to keep the base dividend, variable dividend, and buybacks within the constraints of the 75% FCF metric.

After several quarters of greater than 100% FCF distributions, this was a necessary move from a financial standpoint. That pace just could not be sustained. Management intends this change to allow it to focus on maintaining the balance sheet and allow the company to be opportunistic in the future. In this article, we will explore why this was necessary and what the long-term implications are for PXD.

Then and Now

2022 was a mega year for most oil producers, thanks to energy prices soaring to decade highs. This was set off by the Ukraine-Russian conflict as well as the worldwide economy restarting following the 'end' of the Covid Pandemic. Pioneer was a standout in the oil patch, returning $6.3 billion in dividends, $1.7 billion in buybacks and paying off $2.5 billion in debts. Returning $10.5 billion in one year for a company with a market cap of $50 billion is no small feat.

We are a third of the way done with 2023 and so far, it is nothing like 2022. Crude prices have generally hung between the $70 and $80 marks while natural gas prices have dropped into the low $2 range. It's obvious that investors should expect some things to change, but being human, that doesn't mean the change isn't disappointing.

Going at a Breakneck Pace

Pioneer had its foot smashed onto the accelerator when it came to returning cash to shareholders in 2022. So much so, it often was shelling out more than it was making during a record year. Total return to shareholders in 2022 ( Q1 through Q4 ) looked like this.

- Q1 - 88% of Free Cash Flow distributed.

- Q2 - 95% of Free Cash Flow distributed.

- Q3 - 108% of Free Cash Flow distributed.

- Q4 - 103% of Free Cash Flow distributed.

Most investors are delighted when that kind of dividend check comes in. The bad news is, it's hard on the money machine.

For the independent oil producers such as PXD, Devon Energy (DVN), Diamondback Energy (FANG), etc., I like to look at Net Income and take out the money spent on capex, dividend, and buybacks. I also add back depreciation. I do this because, let's be honest, depreciation is a non-cash accounting term when it comes to balancing a checkbook. This view makes it very similar to what all of us do every day, make sure what's coming in, is higher than what's going out.

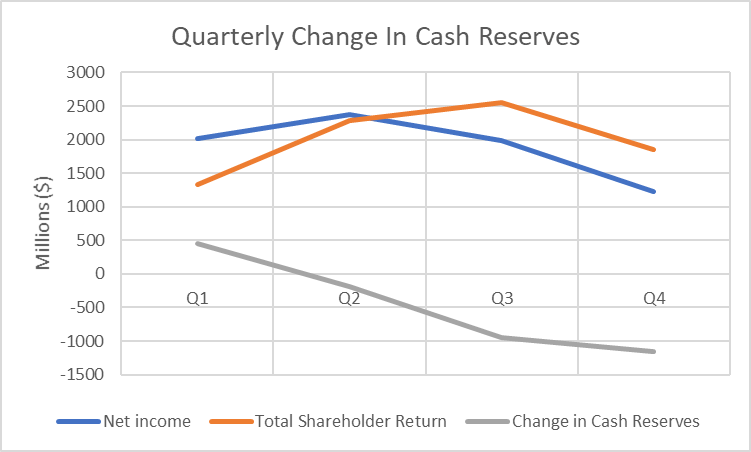

Here is how it looks on paper and on a graph. From the data supplied below, you can see how PXD's net cash balance is negative $1.8 billion from Q1 2022 to Q4 2022. With the exception of Q1 2022, PXD has been draining the bank account to fund the massive dividend and buyback shares at the same time.

Further, PXD reduced its total debt by $1 billion during 2022. This has resulted in cash reserves being depleted from $3.8 billion at the end of 2021 to $1.0 billion at the end of 2022. Ultimately, this cannot be sustained forever, and as such, PXD has to throttle back some.

| ($ Millions) |

| Q1 |

| Q2 |

| Q3 |

| Q4 |

| Net income |

| $2009 |

| $2371 |

| $1984 |

| $1222 |

| Depreciation |

| $614 |

| $620 |

| $641 |

| $664 |

| Cap Ex |

| ($852) |

| ($895) |

| ($1014) |

| ($1193) |

| Dividend |

| ($1073) |

| ($1788) |

| ($2052) |

| ($1356) |

| Share Repurchase |

| ($250) |

| ($500) |

| ($500) |

| ($500) |

| Net Cash Balance |

| $448 |

| ($192) |

| ($941) |

| ($1163) |

{kind=link}

Doing What Must be Done

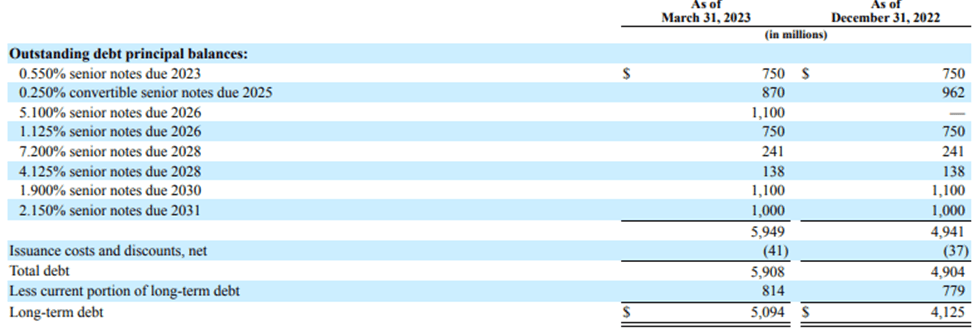

With minimal dry powder left, PXD was forced to refinance the $750 million worth of 2023 Senior Notes . The real shame here is that these notes had an interest rate of 0.55% and were refinanced at 5.1%. Unfortunately, given the circumstances, not much else could be done, and the company certainly has the cash flow to cover the added expense, but a shame, nonetheless.

It appears management is not oblivious to this fact and announced action during the conference call on April 27th.

In total, 75% of our quarterly cash flow will be directed towards capital returns, while the remaining 25% will be used to increase financial flexibility and further strengthen our balance sheet.

The company stressed how it will focus on whittling down its higher interest debt to continue to strive for a net debt position of zero or even negative. This is how a good management team keeps the business healthy and prosperous in good times and bad.

Looking at near-term maturities shows that with this disciplined approach, the company will be prepared to eliminate these debts. Once the 2023 notes are formally extinguished, there will be no debt due until 2025, providing ample time to prepare for and execute a plan to retire this debt.

PXD's Long Term Debt Obligations (10-Q, Q1 2023)

{kind=link}

It is also worth noting that the company still left the door open to capitalize when the market offers up the occasional gift.

...it also provides the flexibility to continue to allocate capital between variable dividends and opportunistic share repurchases. So that was a big feature of what we wanted to accomplish, too. And then the third piece is really with the greater liquidity, it really supports our intention of reducing gross debt through time and provides the ability repurchase incremental shares at times of major market dislocations like we saw in March. So we think it's a good refinement to the plan.

Long-Term Implications

The management team capitalized when 2022 gave them lightning in a bottle. They gave shareholders everything they could and more. Now they have the fortitude to dial it back to ensure the business is not overly stressed. I view this as a reload to its arsenal, not a sign of weakness.

The shareholder return model will still remain best in class, returning 75% of profits back to shareholders. The only complaint I can muster is that the framework is a little gray for my taste. There is no established framework for how the variable component will be structured from a quarter-to-quarter basis. Below is the guidance given by management.

...to your second question on what will be the distinguishment between variable versus buybacks. It's really a conversation from those conversations that was clear that in the last few months that our investors do like the variable dividend, and it remains an important part of our method to which we return capital, but we want to also be able to continue to repurchase shares on an opportunistic basis when we see attractive value.

And so as you can imagine, that's really based on many factors that we evaluate when identifying that opportunity. It's not formulaic in nature...

This certainly does not give any pillars for estimating your potential income. I can see if you were a retiree who was using this as a bill-paying mechanism, it could be somewhat frustrating. Other than that, I don't view it as much of a problem. It does, however, provide some level of mystery going quarter to quarter.

Venturing an Estimate

So, what should an investor expect? I think a fair expectation going forward would be for dividends to make up 50% of the variable component and the remaining 25% to be allocated for buybacks. I will also assume that energy prices remain relatively flat at current levels for 2023 to give investors some idea of what they should expect for a return at current prices.

Using a consistent production of $1 billion in FCF per quarter would translate into almost $300 million to fund the $1.25 per share for the base dividend. This would leave $525 million left over for the variable component. Using a 2/3 dividend and 1/3 buyback split, this works out to be an additional payout of $1.50 per share in dividends and $175 million spent on buybacks.

Annualizing this works out to be $11/share in dividends and $700 million spent on buybacks. This equates to an annualized yield in the ballpark of 5% and repurchasing roughly 1.4% of the shares outstanding at a price of $217.50.

Risks

Since Pioneer operates in the commodities space, their earnings can fluctuate wildly. Unfortunately, this is largely out of their control. Crude has gotten some support thanks to Saudi Arabia's desire to maintain a price floor and the eventual need to refill the Strategic Petroleum Reserve.

Pioneer's breakeven is roughly $40/barrel, WTI. This level is sufficient to fund operations and CAPEX for 2023, which we have been well above so far this year. I believe that, given the mechanisms in place to support prices, there is more upside than downside for crude prices. However, natural gas prices have bottomed out around $2.00. While not a major component of PXD's production, it does drag total profits down due to it accounting for roughly 25% of total volumes.

Per the EIA , over the last 10 years, oil prices have averaged about $65/barrel. The downside risk is real, however, as prices have flirted with breakeven in 3 out of the 10 years. That is why I stress the need to be patient, waiting for an entry point that protects against capital losses. At this time, I believe there is adequate support to oil prices to preclude any near-term fallout.

As far as natural gas is concerned, I believe in the long term, natural gas prices will rise when export capacity is slated to dramatically increase. Unfortunately, this is not planned to occur until mid-2024 at the earliest. In the near term, I do not see any significant drivers for a price rebound, aside from seasonal demand. The earliest I would expect significant moves would be the 2023-2024 winter season, so depressed prices should be anticipated for the next few quarters.

Summary

It has been shown how, while disappointing, the throttling of returns to shareholders needed to happen to preserve the long-term health of PXD. This move will allow the company to shore up cash reserves. This is a reload period to capitalize on the next opportunity. In addition to that, it still has a top-tier return program for its shareholders.

I discussed in a previous article how PXD is one of the best-positioned independent oil producers in the Permian. The recent alteration in return philosophy takes some of the edge off my previous thesis but as a whole, remains largely intact. Thus, Pioneer should be considered a valuable asset in any dividend portfolio.

I view the energy markets as being 'stable' for the near term and expect crude to continue its bounce between $70-$80 per barrel. Natural gas may recover in the gear up for winter, but with inventories already at high levels, it may not be significant. In my view, we can expect somewhat stable cash flows from PXD over the near term.

If you buy into that narrative, the projections point to a 5% dividend, plus a moderate buyback program for 2023. Given the volatility that energy stocks display, I believe PXD is fairly valued at around $220/share. I would hold here, waiting for a lower entry point to either add to or start a position. Over the last year, share prices have dipped below $200/share five times, and I have confidence that will happen again. As always, be prepared for the next opportunity the market gives you.

For further details see:

Pioneer Natural Resources: Throttling Back Shareholder Returns Was Necessary