LAZ - Piper Sandler: Not Snapping Back In Advisory

2023-11-14 05:43:16 ET

Summary

- Piper Sandler's cyclical advisory business is still suffering, as can be expected from a still-depressed sector of the market.

- Corporate finance activities, such as ECM and DCM, are stabilizing, but the clear lack of market confidence and certainty affects the activity levels.

- Don't expect financial sponsor activity to come back to markets yet.

- The brokerage business remains resilient, but PIPR's valuation is high compared to Lazard, which we think is ultimately a safer model.

Piper Sandler ( PIPR ) had a relatively decent performance, but struggles in advisory are still showing and pockets of demand are not snapping back despite a stabilising rate situation. Some corporate finance activities are beginning to bottom out at least following a depression this last year, and brokerage continues to be quite resilient. The issue remains valuation. PIPR is relatively expensive, and the stubbornly high price in the face of cyclical forces demonstrates it.

Q3 Breakdown

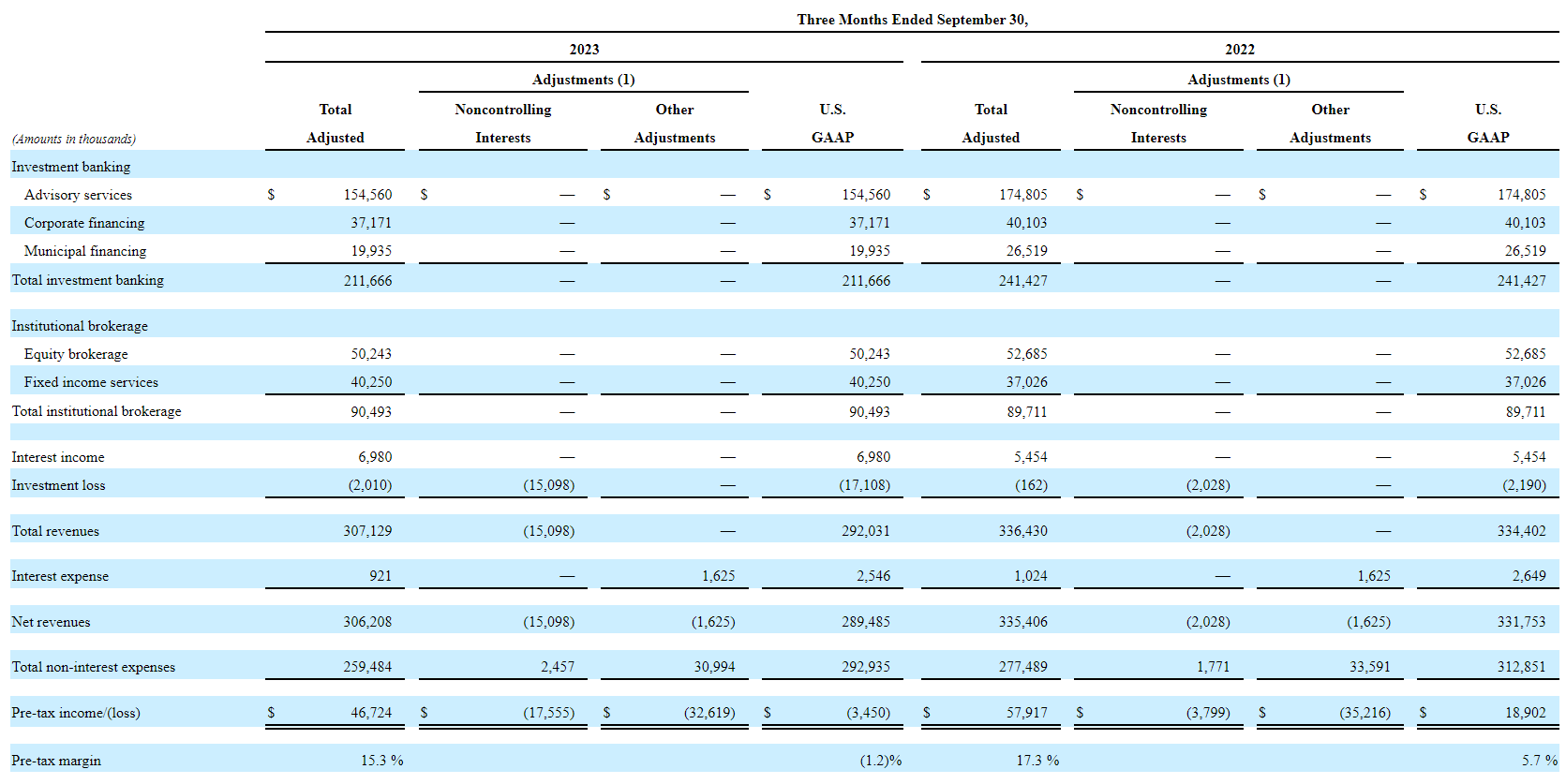

As always, following the comments of advisors is illuminating and is a litmus test for the whole financial system and lead for the economy. All the relevant data is below.

{kind=link}

Advisory is still declining, but it's slowing, and this quarter is the best we've seen so far this year. Q4 tends to be seasonally better, and management is already indicating that it's shaping up that way. M&A deals are down a lot, and while PIPR has seen deal declines, their declines are about half of the mid-market benchmarks.

Corporate financing activity, including ECM and DCM, is finally stabilising. We are seeing some DCM action picking up as rates stabilise and corporates are forced to refinance at these higher rates, no pivot in sight - sequential increases happening. We are also seeing some share wins in ECM, mostly in healthcare, which together with financials are PIPR's key markets. ECM is still weak, however.

Muni financing is still in decline, but up sequentially. There are headwinds due to the higher rates, despite growing certainty - there is less refinancing action, and some players are still on the sidelines. On the flip side, material costs are up and that means bigger tickets to finance. Most of the business is new projects, not refinancing. Also, there's a lot of higher yield exposure here which is still difficult to digest, hence being more challenged than the rest.

There are some interesting comments on private equity and sponsor activities in general.

Yes. Maybe I'll start with the sponsor side and private equity. We've definitely seen more transactions as sell-side processes start. There's definitely interest. We can definitely get bids. You get to the end of a process, instead of multiple parties, you're down to a couple of parties still closing the sort of the ask -- the bid-ask gap. But financing is definitely there and better. So, I would say on the sponsor side, it's improved, but slowly. It's not like it's snapping back

Apparently, antitrust questions are kicking in more frequently now too, with regulators more up in arms. It is extending timelines a bit, in addition to general deal delays due to uncertainties around the market.

The brokerage business remains strong. Equity is down a bit as volatility subsides, but now there is less of a one-way train in rates and more speculation, driving up the fixed income brokerage business. On balance: resilient.

Bottom Line

Same as Lazard ( LAZ ), things aren't popping back . It's a slow scaling. Sponsors have to be careful and score winners after the post-2022 writedowns and massive fund raising the year before. It's harder in a higher cost of capital environment. Mid-market isn't doing too bad, fees from companies sub $5 billion have gone up 88% over last year for PIPR, and 26% in the broader fee pool for the market. Strategic activity is pretty strong still. But other market facing corporate finance activities are not coming online yet. Also, while PIPR had added restructuring headcount some years ago, that business remains small overall and is growing but mainly idiosyncratically, although generally larger volumes of restructuring mandates can be expected.

The issue is PIPR is still expensive. It's lying at pretty high levels. While brokerage activities are resilient, advisory is still their bread and butter and that's down. Lazard has a more resilient and relatively larger asset management business to its advisory activities, and the multiples are lower, dividends higher and prices much more retracted.

We prefer them over PIPR, especially since European franchises are more stable in advisory shown by more limited advisory declines.

For further details see:

Piper Sandler: Not Snapping Back In Advisory