PBI - Pitney Bowes: FY 2022 And Activist Update; Risk-Reward Favorable

Summary

- There has been recent activist activity involving Pitney Bowes. I agree whole heartedly with this outside push to get the board and management team to unlock shareholder value.

- I opened a position in the stock after this news came out because with the additional pressure of outside shareholders, I think the risk/reward for owning the stock is favorable.

- Unfortunately for the current management team, the fourth quarter and 2022 fiscal year results did not do much to help their cause.

I wrote last about Pitney Bowes Inc. ( PBI ) in September 2022. The main idea of my article was that the global ecommerce segment was dragging the value of the company down and that management would do best for shareholders by selling the assets of that segment. Interestingly in November 2022 the hedge fund Hestia Capital, at the time a 7% owner of Pitney Bowes, revealed plans to have a dialogue with current Pitney Bowes management about plans to unlock shareholder value. One of these plans was to consider selling the assets of the global ecommerce segment.

Then in December 2022, a Reuters article shared that BWM AG, a Swiss asset manager and 1.5% percent owner of Pitney Bowes at the time, wanted the board to “consider strategic options, preferably a sale, for the global ecommerce segment”.

I like to think that my article may have had a hand in spurring these discussions, but these plans were likely in the works for some time as the solution to maximize shareholder value is clear. Either way, I agree whole heartedly with the outside push to get the board and management team to do something to unlock shareholder value.

In fact I opened a long position in PBI after hearing about the activist movement. I was hesitant before this; a competent management team and aligned board of directors is a large consideration in my investment decisions. But because so much value is hidden in the business, I think it’s worth a position if large shareholders will be pushing for change. Based on what I wrote in September I’m obviously a fan of selling the global ecommerce assets, but I also like the idea of installing a new CEO and/or new members of the board to help right the ship.

Unfortunately for the current management team, the fourth quarter and 2022 fiscal year results did not do much to help their cause. This makes Hestia’s case much more compelling and will make for a bit of drama at the next annual meeting as Hestia nominates CEO and board seats candidates. In this article I will go into some more detail about the activist situation, the 4Q and FY 2022 financial results, and why I think all of this makes Pitney Bowes an investment with a good risk/return profile.

4Q and FY2022 Results and Analysis

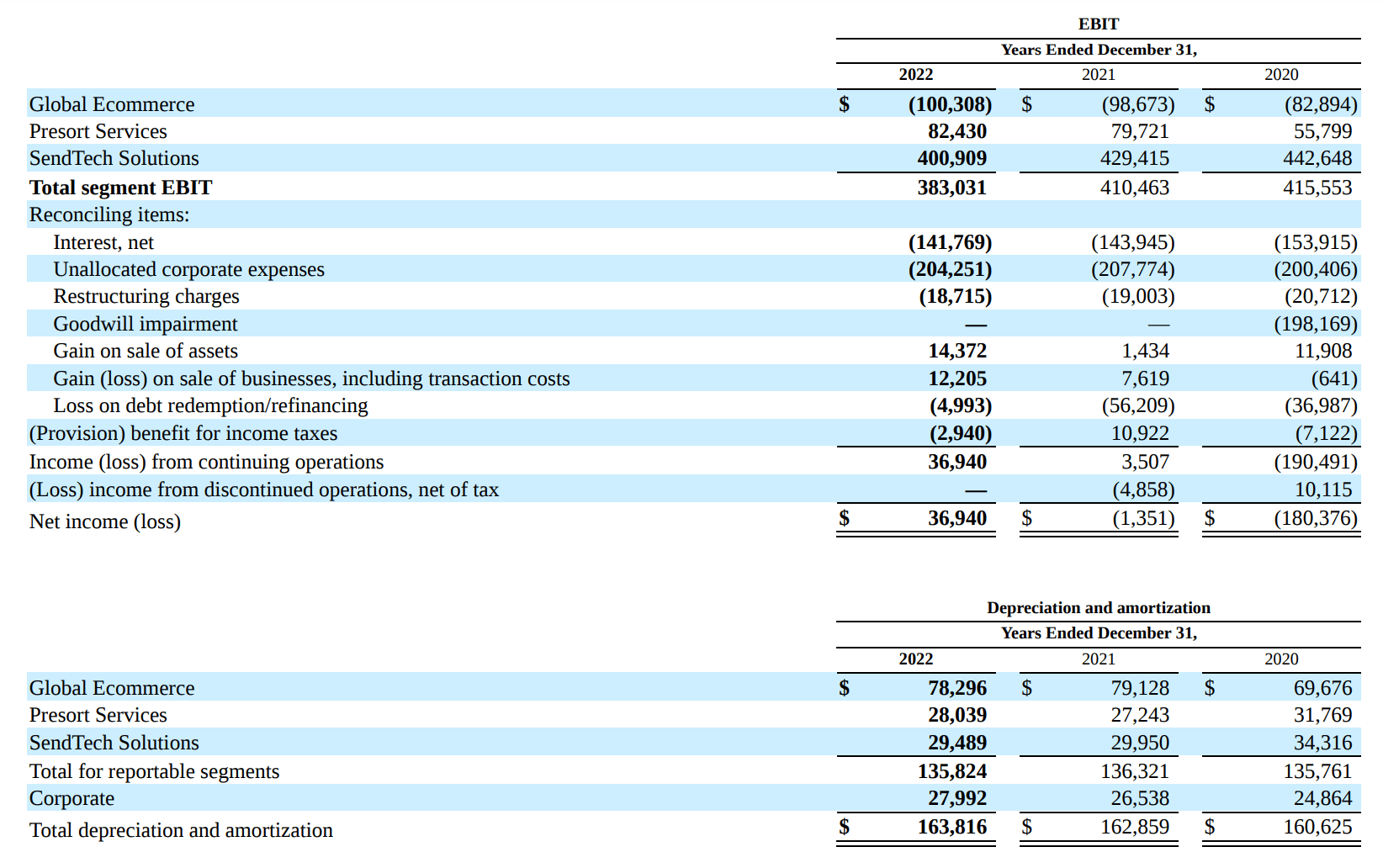

For the full year 2022, revenue decreased 4%. GAAP earnings before taxes were about $40 million. I usually prefer to look at EBIT but interest expense is a big expense for Pitney Bowes so it’s more prudent to consider EBT.

At a more granular level, segment EBIT, which doesn’t include net interest expenses, unallocated corporate expenses, restructuring charges etc., decreased by 7%. Most importantly, the global ecommerce segment fell short of expectations for the quarter and year. I say this is most important because global ecommerce is the segment that has management on the hot seat. EBIT for the segment declined 2% and amounted to a loss of $100 million.

What’s interesting about these results is that using last year’s expense methodology, global ecommerce 2022 EBIT would have been about $10 million less than what is reported! I’m not sure if this methodology makes more sense than the previous one and it may, but it also seems convenient that this change occurred when management is feeling the most pressure to show improvements in the segment.

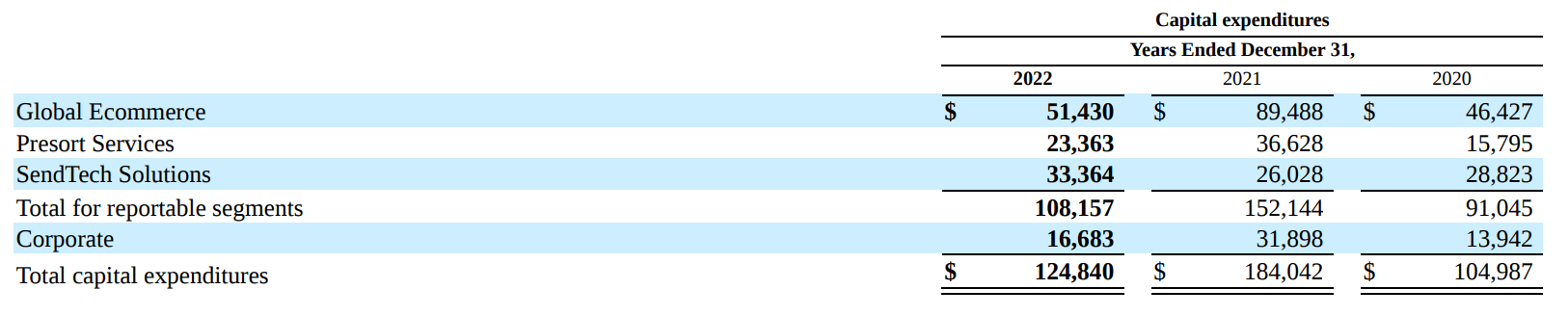

The SendTech and Presort segments continue to chug along very profitably. SendTech EBIT was $400 million and Presort EBIT was $82 million. I still think the value of these two businesses combined is worth far in excess of the current market cap for Pitney Bowes. I have further analysis of this in my previous article but for 2021 I calculated about $215 million in EBT less capex for the two segments. Using the methodology from that article, I get to about $250 million in EBT less capex for 2022. The gain from 2021 is from a much smaller debt refinancing expense. Using a 10x-15x multiple for that metric, the market cap would fall in a range of $2.5 billion to $3.75 billion, or more than triple above today's market cap.

That $250 million EBT less capex number also assumes that debt was not paid off from the proceeds of the hypothetical global ecommerce sale. For example, if they simply paid a special dividend with that money. However interest expenses would be even lower, thus EBT less capex even higher, if they would pay down debt with the cash from the sale of the segment.

Segment EBIT and D&A 2022 (PBI 2022 10-K) Segment CapEx 2022 (PBI 2022 10-K)

{kind=link}

{kind=link}

| Presort EBIT |

| $82,430 |

| SendTech EBIT |

| $400,909 |

| Interest Expense |

| -$141,769 |

| Restructuring Expense |

| -$18,715 |

| Debt Refinancing Expense |

| -$4,993 |

| 1/3 Unallocated Corporate Expense |

| -$68,083 |

| = earnings before tax |

| $249,779 |

| Presort and SendTech D&A |

| $57,528 |

| Presort and SendTech CapEx |

| -$56,727 |

| = 2022 EBTDA minus CapEx |

| $250,580 |

Activist News

With activist investors pushing the board in the right direction I hope that this value will be unlocked. Hestia nominated a slate of potential new board members, one of which is Ken McBride, the previous CEO of Stamps.com Inc. (STMP). I covered stamps before it got bought out in a private equity deal, but I really admired how McBride ran stamps.com. Notably, he made the very bold move to cancel an exclusive relationship with the USPS which caused the stock to drop 50% as investors were spooked by the loss of assured income. This ended up being the smart move to make as McBride accurately saw that companies such as Amazon were changing the shipping business and that stamps.com needed to work with these companies.

I will be sure to cast my votes accordingly at the upcoming annual meeting.

More recently, the Hestia Capital CIO Kurt Wolf spoke about the opportunity with Pitney Bowes. The main point he makes is that the global ecommerce segment has drastically underperformed expectations. He notes that in 2019, management guided that global ecommerce EBIT margins would be around 8-12% by the end of 2023. This has obviously not been the case. In the defense of the current team, even Amazon has botched their ecommerce plans due to the uncertainty created by the pandemic. Ecommerce is a tough business with low margins and high capital intensity. At this point it makes more sense to cut losses and sell the segment.

Interest Expense

The most pressing issue is the rising upcoming interest expenses and higher interest debt that will come with any refinancing. They reduced debt by $124 million in 2022 and so far in 2023 they have repurchased $12 million of their debt on the open market, compared to $9 million in all of 2022. For 2023, the issues come with the variable rate debt which represent about 35% of total debt. Management notes in the 10-K that they expect the interest expense to be about $30 million higher in 2023.

Snippet from PBI 2022 10-K (Pitney Bowes Investor Relations)

{kind=link}

Total earnings before tax were about $40 million in 2022 so all else equal, this rise in interest expense could cut almost all GAAP earnings before tax. 2023 guidance calls for flat to a mid-single digits rise in revenue with percentage growth of EBIT expected to slightly outpace that. This means GAAP earnings before tax will likely not drop to zero, but even if this guidance holds true, earnings will suffer greatly due to the higher interest payments. This is another reason why I advocate selling the global ecommerce assets as it can help reduce debt and those interest expenses. This will mean that all cash produced by the two cash flowing segments can go directly to the balance sheet and subsequently to the shareholders.

Final Thoughts

Not much has changed with my thoughts on Pitney Bowes’ best course of action. I think selling the global ecommerce segment, paying down debt with the proceeds from the sale, and running the two cash flowing segments would unlock the most value. Coincidentally, some large shareholders of the company have also called for that to be considered. I opened a position in the stock after this news came out because with the additional pressure of outside shareholders, I think the risk/reward for owning the stock is favorable. If the activist pressure works, the value could be unlocked and the stock could double to triple based on my 2022 estimate of $250 million in EBT less capex for the SendTech and Presort segments.

On the other hand, if nothing comes of this activist pressure the stock price will likely flounder or drop as there is minimal cash flow. For 2022, EBT less capex of all segments was $45 million. Using the same 10x-15x multiple range, the range of potential market caps is $450 million to $674 million which is less than the current market cap. Yet at the same time, there is still a dividend so the capital loss would be partially offset. So in my range of outcomes the bear case has 15-40% downside plus some dividend income to offset, with a bull case of 100-200% upside also with additional dividend income.

For further details see:

Pitney Bowes: FY 2022 And Activist Update; Risk-Reward Favorable