VB - Pitney Bowes: The Tailwinds Trump The Headwinds

2023-12-04 13:32:28 ET

Summary

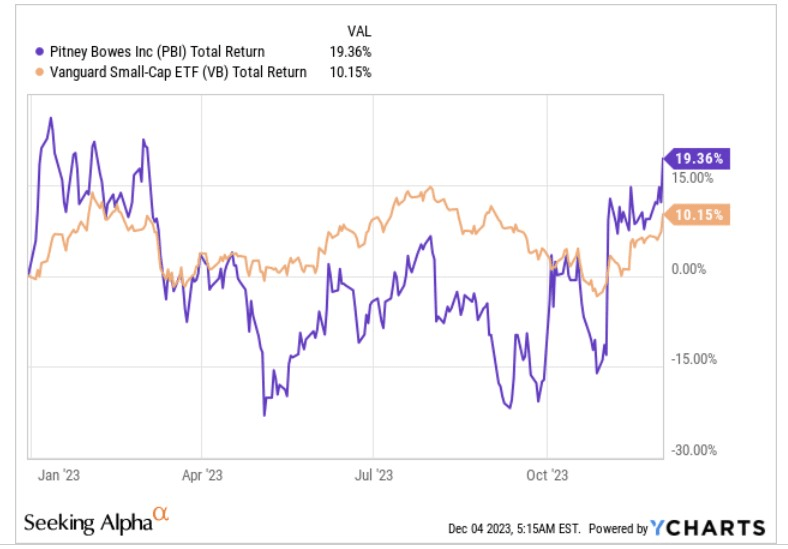

- Pitney Bowes stock has delivered almost 20% returns this year, outperforming a flagship small-cap portfolio.

- A change in leadership and positive operating developments in SendTech and Presort ought to be appreciated.

- Forward valuations are reasonable with enhanced cost savings targets, but the dividend sub-plot is not great due to restrictions and a sub-par yield.

- We like the risk-reward on the charts.

Introduction

This year, the stock of global shipping and mailing specialist Pitney Bowes Inc. ( PBI ) has been a decent source of returns, particularly in Q1 and the current quarter. All in all, it has ended up delivering almost 20% returns, which is twice as much as what a flagship small-cap portfolio has generated ( VB ).

{kind=link}

Could we see a continuation of this trend in the periods ahead? Well, here are a few important themes that could weigh on the future performance of the stock.

Positive Leadership and Operating Developments

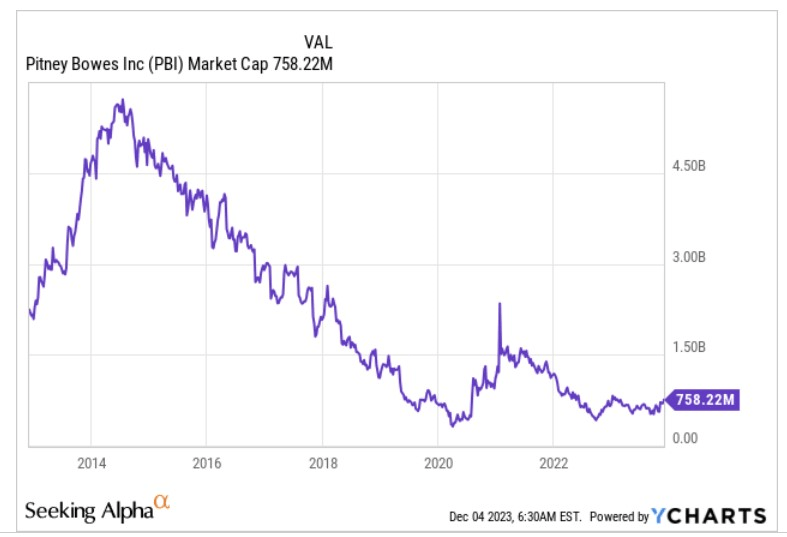

For much of this year, Pitney Bowes has been in the news on account of uncertainty linked to its management team. Hestia Capital Management, LLC, an important institutional shareholder, had long been pushing for the ouster of Marc Lautenbach, who took hold of the reins way back in December 2012 and has since seen the stock's market-cap shrivel by over -66% during his tenure.

{kind=link}

Earlier in Q4, we saw Lautenbach give way to an internal candidate - Jason Dies (been around since 2015), who has good experience of turning around sub-par divisions. He did so with the SendTech solutions segment and has also overseen positive developments in the Presort Services segment.

Note that, as things stand, both these segments are profitable at the operating level (the third division - Global Ecommerce is not), and crucially, both divisions have also seen an expansion in the EBIT margins on a YTD basis.

Annual and quarterly reports

Prima facie, SendTech is an attractive cog, given its recurring revenue tilt, but recently, the onus has also shifted away from equipment sales which had previously left an adverse mark on cash generation. Crucially, of late, this division has also been able to see a ramp-up in productivity which has abetted margin progression.

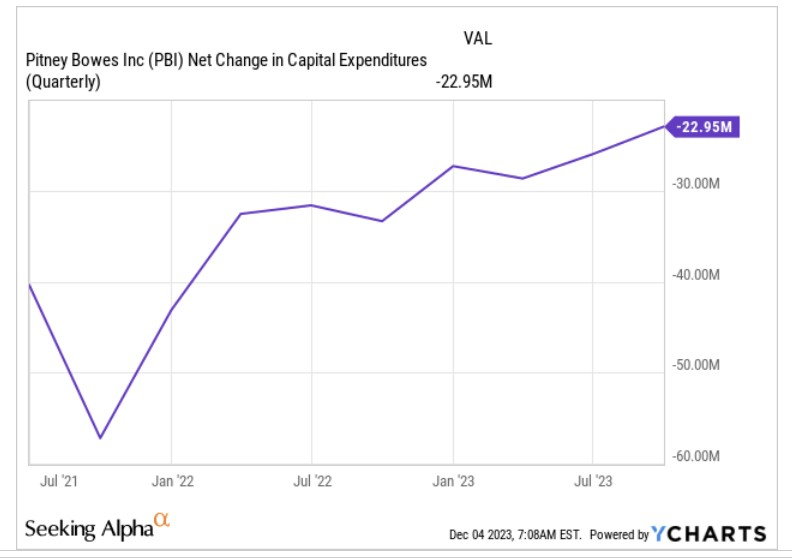

Besides lower equipment sales, it's also good to note that PBI isn't unnecessarily doubling down on its capacity in the underperforming global e-commerce unit, and you can see this playing out in the diminishing outlays towards CAPEX across time.

{kind=link}

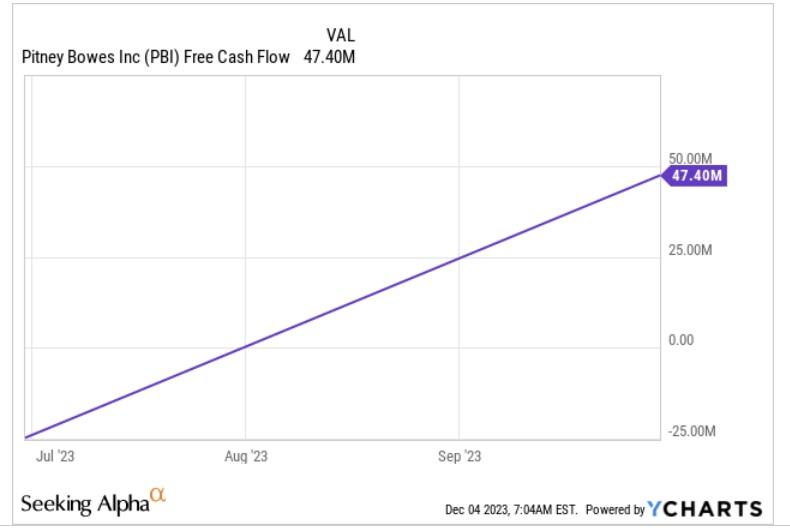

All in all, it's been encouraging to notice how FCF generation (on a TTM basis) has been trending up encouragingly over the last few quarters.

{kind=link}

Meanwhile, in Dies' other focus division - Presort services, don't attach too much of importance to volume declines; rather we think the focus should be on higher revenue per piece, as the shift toward higher-yielding mail classes pays off. In the presort segment as well, productivity (pieces fed by labor hour is trending up at 8% levels as of Q3) has been enhanced by increased automation and process improvements, and thus you're seeing this reflected in sizeable EBIT margin progression of 500bps (as of Q3).

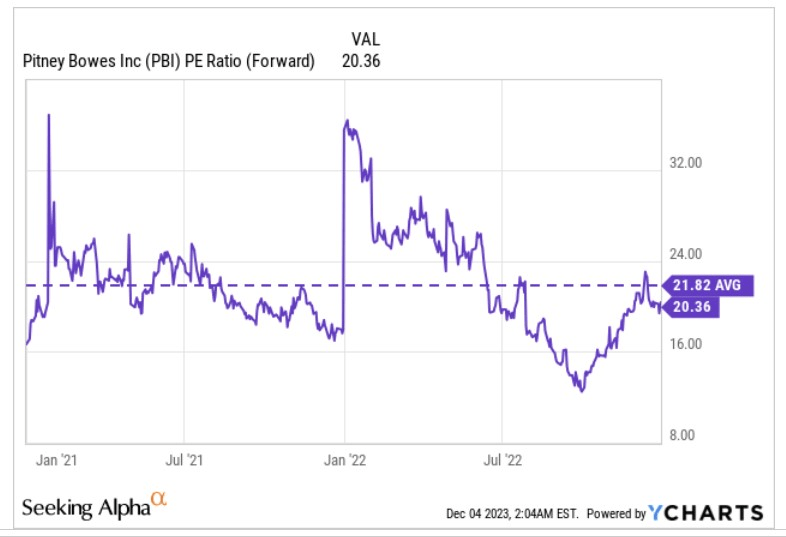

Valuations Look Reasonable Given the Enhanced Cost Savings Targets

On a forward P/E basis, the stock can currently be picked up at a little over 20x P/E, which represents a decent 7% discount to its long-term average.

{kind=link}

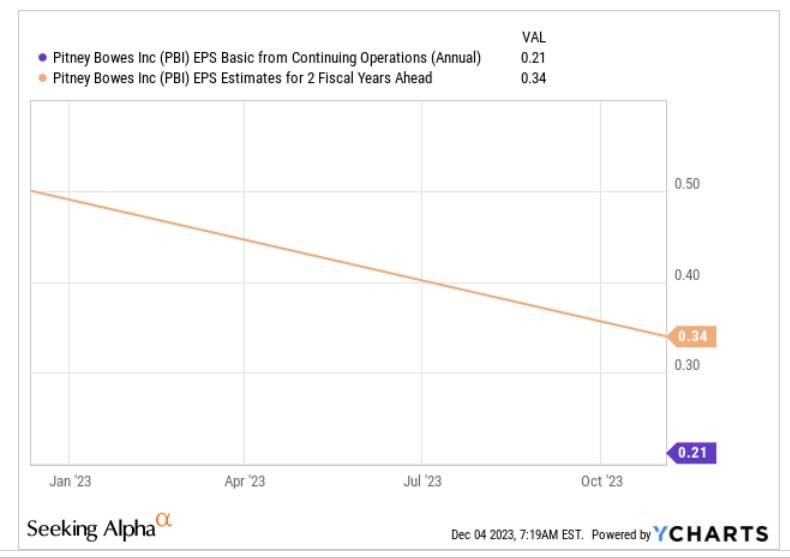

Now, consensus EPS estimates suggest that from FY22 through FY25, this business could potentially generate a healthy earnings CAGR of 17%. There's an argument to be made for the earnings potential turning out to be even better than that, considering how effectively Jason Dies and company have been executing on the restructuring front. Earlier their 2024 annualized cost savings target was only expected to be around $75m, but in Q3 they lifted this even further by over 50%, and now expect to bring through another $115m of cost savings,

{kind=link}

PBI's board is on the lookout for a permanent CEO, but if Dies keeps executing on the margin expansion and cost savings, don't be surprised to see him keep the top job for good.

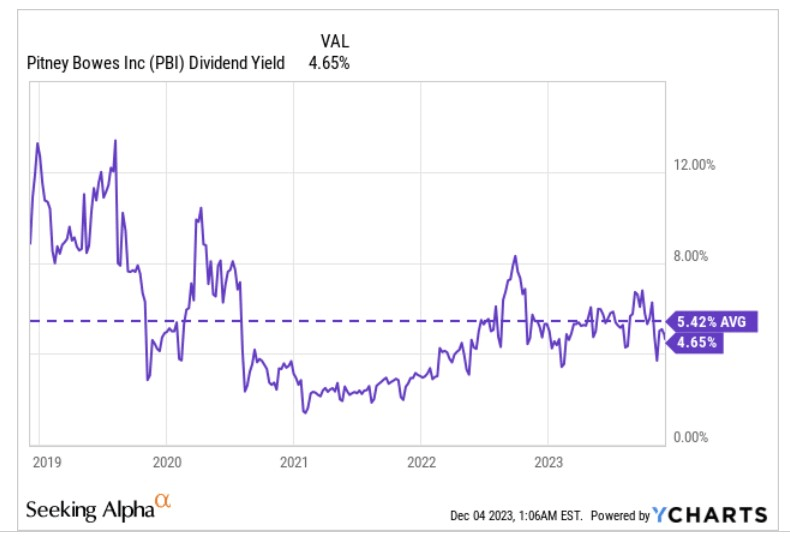

The Dividend Sub-Plot Is Not Great

Like a lot of value-style stocks, PBI is also tapped by plenty of investors for its useful income qualities. For context, you're looking at a business that has now been paying quarterly dividends for over 34 years, whilst most other industrial stocks have been doing so for only over a decade or so.

Whilst the longevity is impressive, one may question the timing of entering a dividend stock of this ilk, given that the dividends haven't really gone anywhere since FY19 and have been flat at $0.05. Do note that because of some restrictions linked to its March 2028 note purchase agreement, PBI will only be able to spend $36m p.a. on dividends every year, or alternatively, the yield on offer will be capped at 6.25%.

With a restrictive set-up of this sort, you ideally want to get in only when the yield is well above the historical average. That is hardly the case at the moment; with the stock having run up quite strongly in Q4 (up 46% so far), an entry at current levels will only yield a sub-par figure of 4.65%, over 75bps lower than its own 5-year average.

{kind=link}

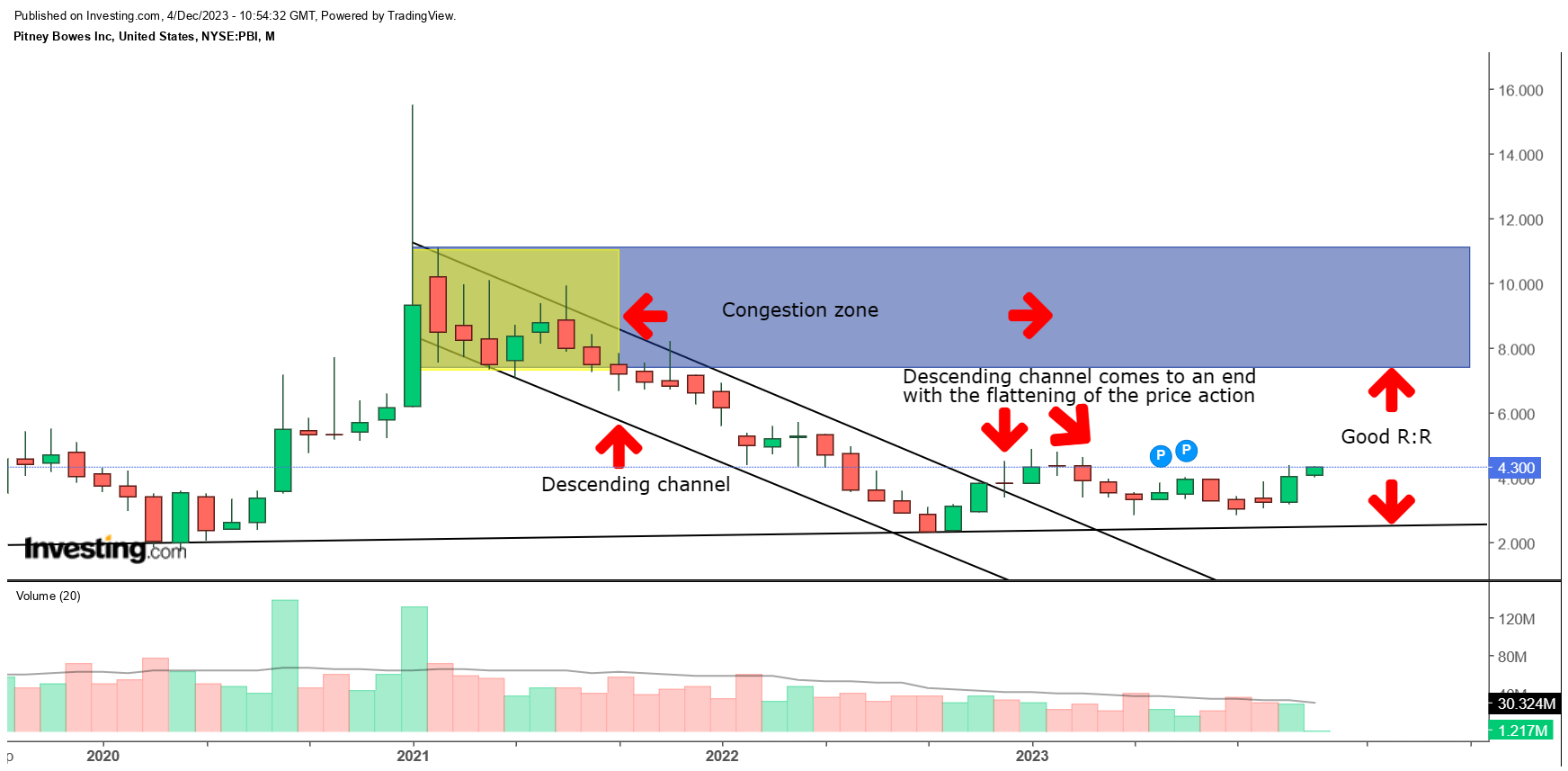

Closing Thoughts - Technical Considerations

If you're willing to overlook the current sub-par dividend theme, may we then conclude with some of the favorable developments on the charts.

From early 2021, over the next ~20 months, we saw the PBI chart lose clout quite quickly, with the selling taking place in the shape of a tight descending channel. However, encouragingly, since late last year/early 2023, we've seen the selling give way to a flattening out of the price action. What's also key is that in the brief selling bouts seen in March and August, the stock failed to retest its previous lows established in September 2022, reflecting the underlying support from bargain hunters.

Looking ahead, it also does not appear that PBI faces any major hindrance until around the $7 levels (the area highlighted in yellow shows that for the first eight months of 2021, we had seen a congestion zone above those levels), and given where the support lies (around $2.30 levels), we think you're getting pretty good reward to risk.

{kind=link}

Meanwhile, we also see PBI as one of those candidates that could appeal as a rotational play for those looking for beaten-down opportunities in the small-cap industrial space. The relative strength ratio of these two securities is a long way off the mid-point of its long-term range, and even if you think a return to those levels could remain a stretch for the foreseeable future, we'd still also point to how the upper boundary of the descending channel (of this ratio's imprints) is still over 4x higher than the current ratio.

{kind=link}

For further details see:

Pitney Bowes: The Tailwinds Trump The Headwinds