PXLW - Pixelworks: There Are Better Companies In The Industry Avoid This One

2023-07-17 04:25:37 ET

Summary

- I advise against investing in Pixelworks due to its lack of profitability and worsening margins, despite its potential in the mobile segment.

- The company's gross margins have decreased by around 9% from the previous quarter, and there are no apparent cost-cutting measures to improve profitability.

- Although PXLW has clients such as OnePlus, Oppo, Realme, Honor, and Asus ROG, I believe the company's high operating expenses and lack of competitive advantage make it a risky investment.

Investment Thesis

I wanted to take a look at Pixelworks' ( PXLW ) financials in particular and its outlook in the mobile segment. The company has been around for a while and still is not profitable. I wanted to take a look at a potential calculation of where operating margins improve to where the company can make a profit. Unfortunately, as the scenario is hypothetical, coupled with worsening margins, I don't see the company as a viable long-term investment for now. I would like to see major improvements in margins in the upcoming years. I am giving the company a "sell" rating for now.

Briefly on the Company

Pixelworks manufactures integrated circuits (ICs) specifically for image processing in cinema projectors, home entertainment, and mobile sectors.

Outlook

Mobile Segment

The mobile market has been sitting on too much inventory which has led to very soft demand in the last year or so. This is projected to change in the next half year to a year when the demand for phones, tablets, and other similar products will start to pick up. To be honest, it is hard to see how the company will do even when the demand picks up because even in the last decade, the company's performance has been very bad, due to very high operating expenses.

The company's ICs in the mobile sector are being used by my favorite mobile company, OnePlus. I've been a fan since the first model and have been buying them ever since. The OnePlus brand has grown fast in popularity, and if it keeps growing this quickly in the future, this could potentially provide a good revenue boost for the foreseeable future. The units sold surpassed well over the 10m mark back in 2021 . Unfortunately, I can't find more up-to-date figures, which may mean that the phones got a bit too expensive, and people stopped buying them or Pete Lau forgot to tell us. The OnePlus Ace and OnePlus 12 will be using the new X7 visual processor. The phones usually get categorized within the Oppo brand, same with Realme, which is also a customer of Pixelworks.

Along with the above brands, the company also has clients with Honor and Asus ROG. Asus ROG in my opinion is a bit of a niche and I don't think there will be much growth there, however, Honor, which was formerly owned by Huawei may provide a good boost in the future as China continues to recover from COVID restrictions and spending picks back up.

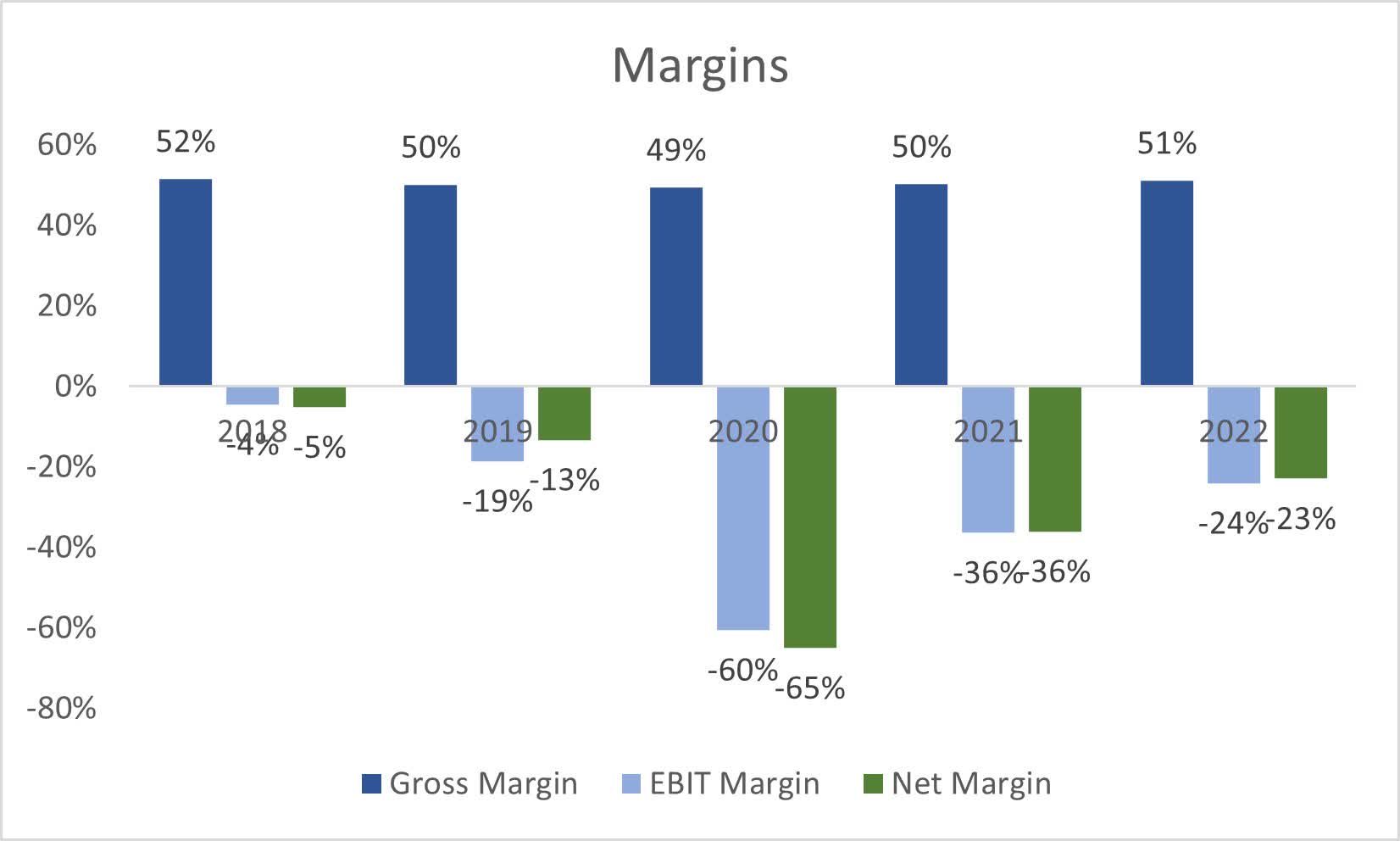

Margins

I am very concerned about the company's margins. In the most recent quarter , the company saw its gross margins decrease by around 9% from the previous quarter. The company did not have a good start to the year with such a negative sentiment around the mobile sector, coupled with macroeconomic headwinds. From reading the transcripts I did not find any cost-cutting measures that will help the company reach profitability in the near future and that is very concerning.

If we look at y-o-y margin figures we can see that these are improving, however, I expect these to be much lower in FY23 because these already got affected in Q1 '23. If the company doesn't find a way to improve efficiency, I don't see this as a viable long-term play, maybe just a gamble at these prices.

{kind=link}

Financials

As of Q1 '23 , the company had around $56m in cash against 0 debt, which is great. $56m in cash is very close to its total market cap already and having no debt while making losses every year means that the cash reserves may have to be used to keep operations alive.

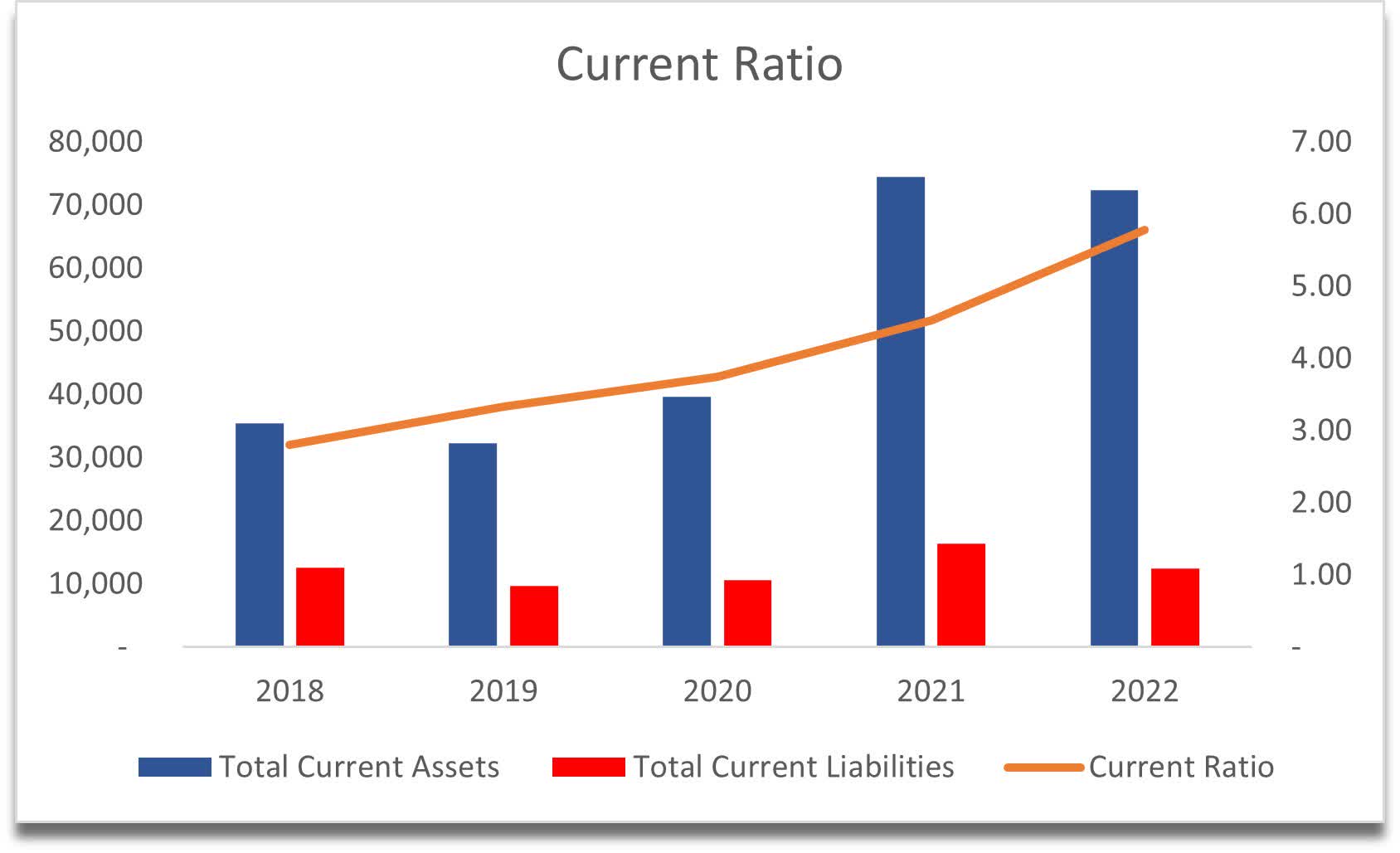

The company's current ratio, because of the high amount of cash on hand, stood at over 5 by the end of FY22. This is a bit too high in my opinion. A good range for me is 1.5- 2.0. Anything above that my belief is the company is not able to use its assets efficiently.

{kind=link}

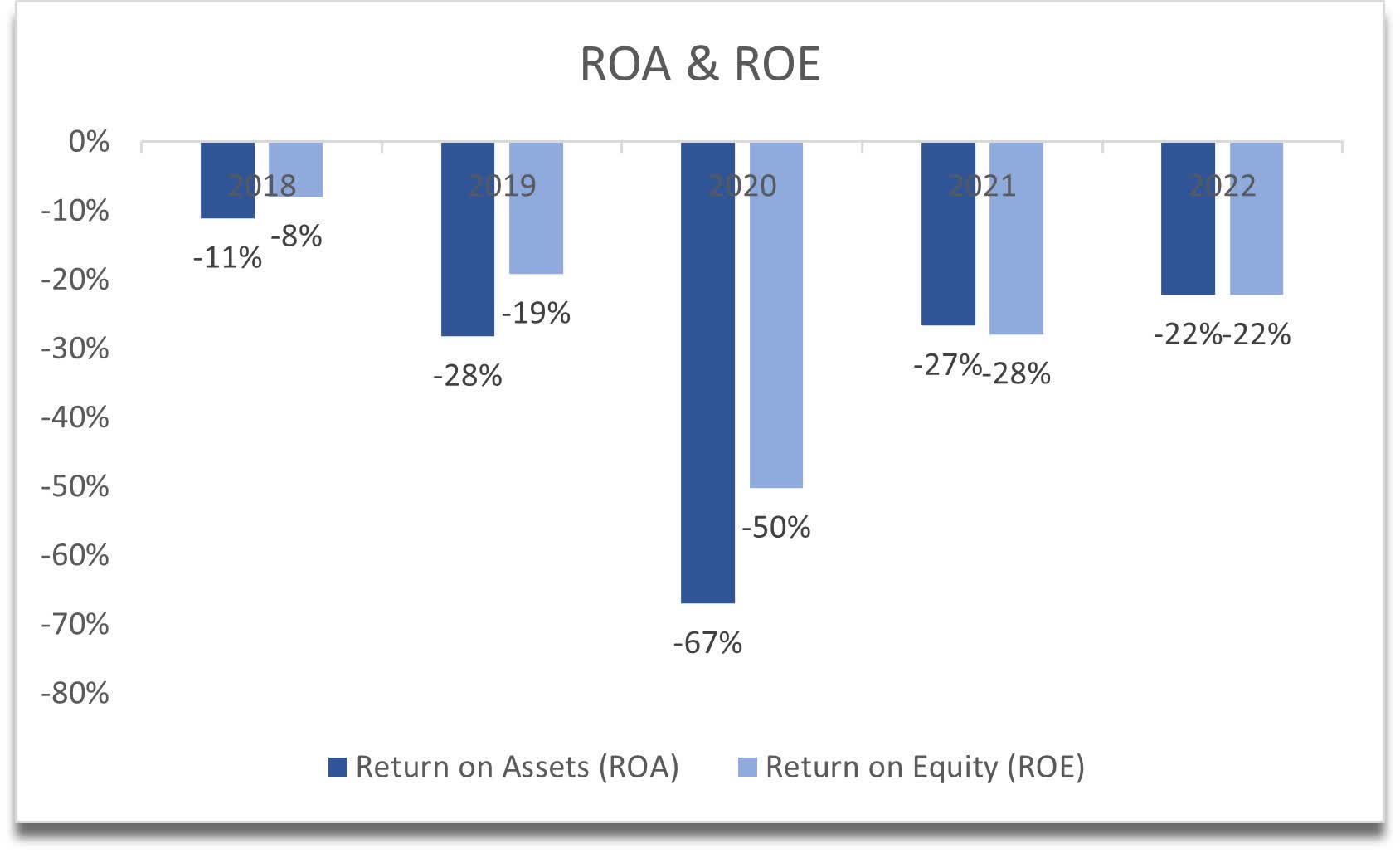

Speaking of efficiency and profitability, the company's ROA and ROE unsurprisingly are horrendous. This further solidifies my belief that the management is not able to utilize the company's assets and shareholder capital efficiently and is not creating value, which is reflected in the share price massive downtrend.

{kind=link}

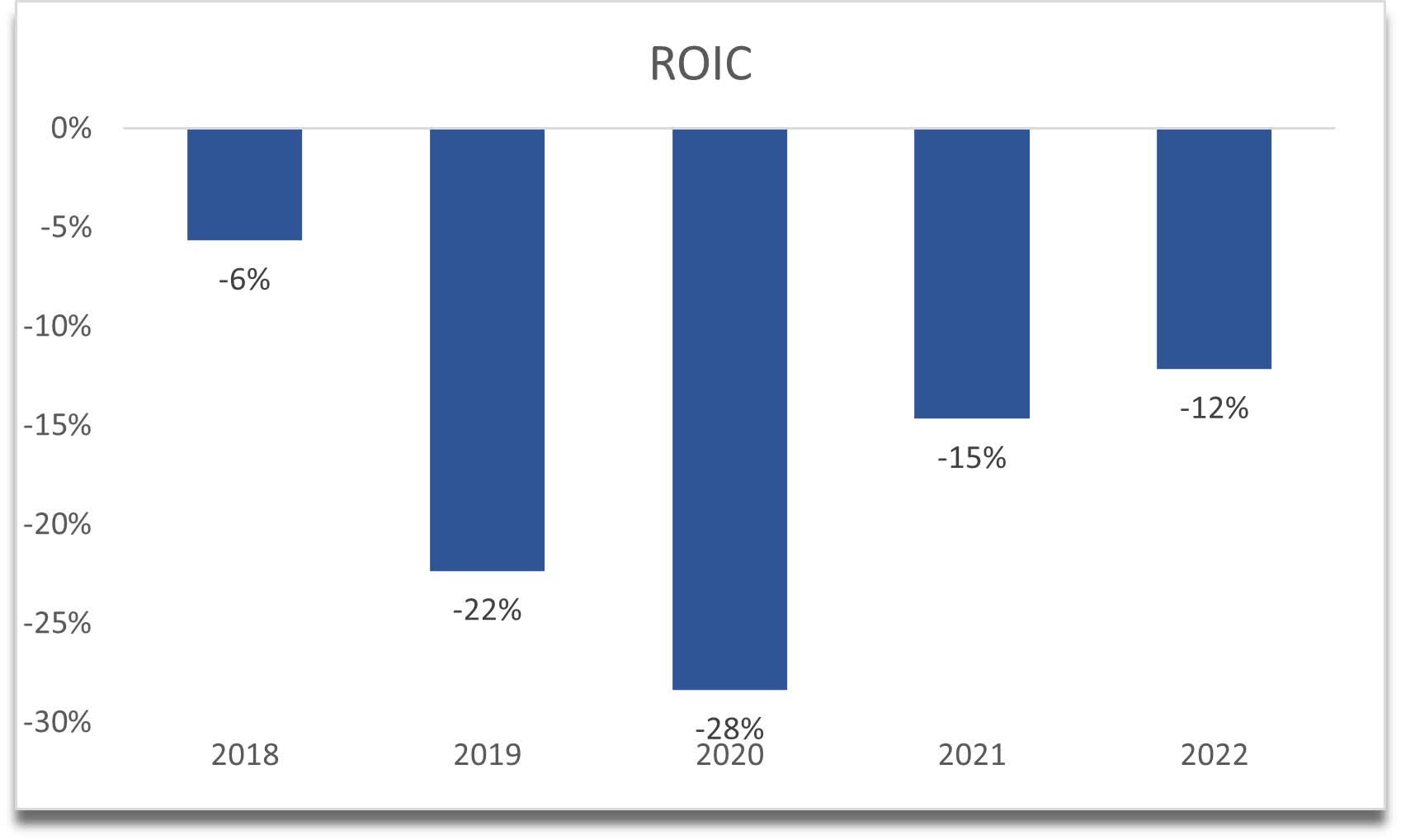

In terms of competitive advantage and a moat, also unsurprisingly it has none. I usually like to look for Return on invested capital to be over 10%, and clearly, the company has no moat or competitive advantage.

{kind=link}

If we look at these metrics from a glass-half-full perspective the good thing about them is that they seem to be trending upward, however, as I mentioned the first quarter of '23 already saw dips in margins, so I would expect these metrics may perform worse again.

Valuation

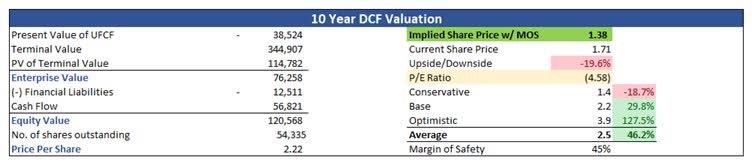

For the base case scenario in terms of revenue, I went with a 14.5% CAGR over the next decade. I think this is very reasonable in my opinion and maybe even on the conservative side. Over the last decade, the company grew at around 6% only but grew 35% in '21 and 27.3% in '22.

For the optimistic case, I went with 18.3%, while for the conservative case, I went with 12.5%.

I decided to approach the valuation with the assumption that operating expenses will come down significantly and leave a positive net margin by '28, and by '32, net margins will increase to around 14%, which is quite optimistic in my opinion.

Because of the financials above and my hypothetical positive net margin expansion, I have to put in a decent margin of safety. I chose 45% here because the model is a very "what-if" type of situation.

With that said the company's intrinsic value if it becomes profitable by '28 is $1.38 a share, implying the current valuation is too high.

Hypothetical Intrinsic Value (Author)

{kind=link}

Closing Comments

I cannot recommend this company at this moment. It is all too speculative. There are better stocks out there in the semiconductor industry that are well-established, profitable, and efficient. For instance, I recently covered Qualcomm ( QCOM ), which I think is a steal at these prices . I am honestly surprised that Pixelworks has been around since '97 and still is not making profits.

Something big needs to change internally, whether that is a management change or something else, but I don't see how this company could be a good investment, maybe a short-term gamble, but even then, the risks are too high. I'd say sell the positions and come back to the stock in a couple of years to see how it has developed margin-wise, but I think it will take many more years for it to become profitable.

For further details see:

Pixelworks: There Are Better Companies In The Industry, Avoid This One