PZA:CC - Pizza Pizza: Execution To Perfection

2023-04-03 10:31:59 ET

Summary

- Same-store sales increased 15% YoY rivaling 2019 system sales with less system stores.

- The dividend is compelling at 6.3% and is well covered.

- The stock trades at 17x my 2023 earnings estimate which is not compelling enough.

Please note all figures in CAD unless otherwise noted as that is the company's reporting currency.

Introduction

For those who follow my work you may recall that I have written on the Boston Pizza Royalties Income Fund ( BPF.UN:CA ) multiple times. One of the more recent articles I wrote was in July 2022 when I was most bullish on the stock and made the following conclusion.

One of the most enticing aspects of BPF from an inflation standpoint is that royalty and distribution income are not directly impacted by the underlying profitability of BPI, as the income is entirely based on the licensing fees paid by the franchisees and incurs very low administrative expenses. As inflation reaches its highest levels in decades, we should expect franchises to charge higher prices, which will mean more off the top for the fund.

Source: Boston Pizza: The Time Is Now

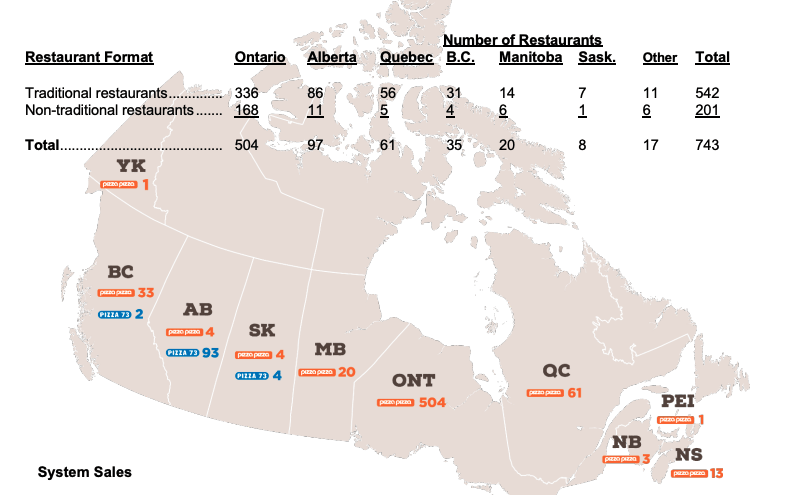

I have since wrote an updated thesis titled Boston Pizza: The Story Has Played Out As Previously Told in December 2022. I present an analysis on another restaurant royalty play that has benefited greatly from inflation which is Pizza Pizza Royalty Corp. ( PZA:CA ). Much like BPF, PZA receives royalty on top line sales from two well known Canadian franchises which are Pizza Pizza and Pizza 73. The restaurants in the royalty pool of Pizza Pizza pay 6% into the royalty fund and Pizza 73 pays 9%. The pool is adjusted on the first day of each year based on the net new openings each year. For 2023, the pool consists of 644 Pizza Pizza and 99 Pizza 73 restaurants. Pizza Pizza locations are primarily in Ontario, whereas Pizza 73 locations are primarily in Alberta.

{kind=link}

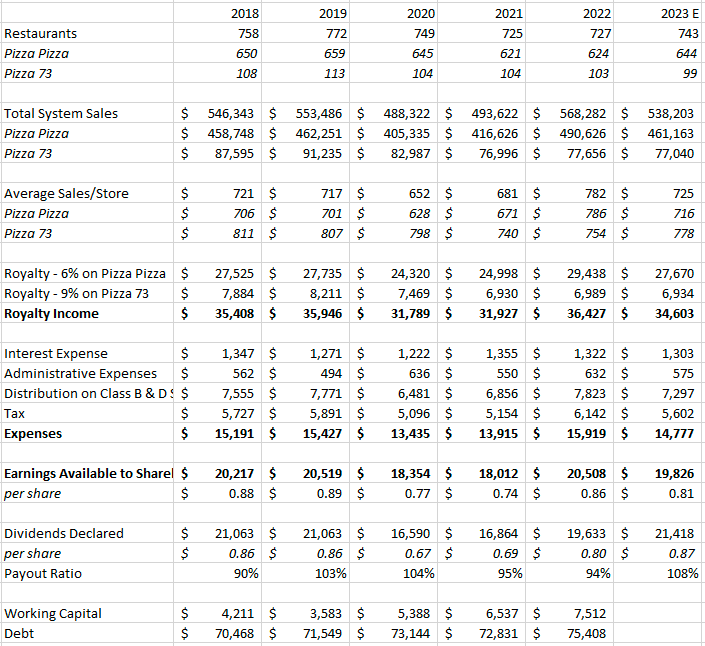

Like all of its peers, system-wide sales fell sharply during COVID, however PZA was less impacted as it relies more on take-out and delivery services which didn't have the same restrictions surrounding "sit in dining." The decline in system-wide sales did lead to a dividend cut of 30% as a means to conserve working capital. The number of system wide restaurants fell from 773 at the end of 2019 to 726 at the end of 2021, a decline of 6% over that time.

2023 Annual Information Form (Pizza Pizza Royalty Corp.)

Despite having less restaurants in the system, total system-wide sales actually beat 2019 sales by 2.3% as same-store sales increased ~15% YoY from 2021 to 2022 largely due to rising inflation. The Pizza Pizza brand is obviously the much stronger of the two brands. The main expenses are financing expenses on the revolving facility and dividend payments on the Class B and D shares which are owned by the Partnership which owns 24% of the fund. Therefore, almost all sales go direct to the bottom line which makes it the ultimate inflationary hedge. There is no CAPEX which allows the fund to have a generous dividend policy, where it has distributed all available cash to shareholders, after allowing for reasonable working capital. As a result of increased system-wide sales and an improved working capital balance in Q4 2022 the monthly dividend was raised to $0.0725/share which means a juicy 6.3% dividend yield going forward.

The working capital reserves have increased in recent years due to the sub 100% payout ratio, which helps service increasing interest obligations and potentially lower royalty income due to downturns in the economy. The credit facility includes positive and negative covenants, and as of December 31, 2022 all covenants were met. The Partnership is required to maintain a funded debt-to-EBITDA ratio not greater than 2.5:1.0 on a four quarter rolling average. The debt-to-EBITDA ratio for the last four-quarter rolling average was 1.31:1. The interest rate on the company's $47 Million credit facility is based on the Canadian Banker's Acceptance rate plus a 0.875% to 1.375% credit spread based on its rolling average debt to EBITDA. The Partnership has managed to stay in the lowest tier of BA + 0.875% since 2021 FYE as a result of higher profitability.

2023 Annual Information Form (Pizza Pizza Royalty Fund)

Outlook

The Bank of Canada has been aggressively raising interest rates since March 2022, as the policy interest rate was 0.25% and is now at 4.5% which has been effective at lowering the inflation rate from over 8% in July 2022 to 5.25% currently.

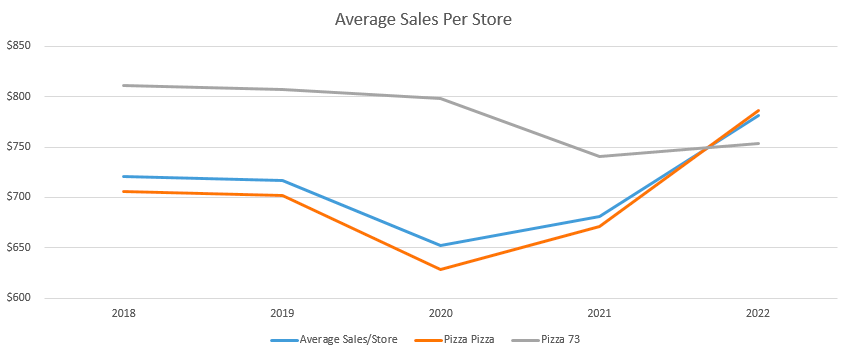

Inflation was the primary driver for the increased system-wide sales in fiscal 2022 as the Pizza Pizza brand increased same-store sales over 17% YoY from 2021 to 2022. Although average sales per store for Pizza 73 was fairly flat average sales-per-store for Pizza Pizza reached all time highs at $786,000 annually per store up ~12% from 2019. As inflation calms down in 2023 the fund will unlikely be able to rely on higher than usual pricing and will need to add franchisees to the pool to grow distributable income.

{kind=link}

Toronto, February 1, 2023 – Pizza Pizza Royalty Corp. (the “Company”) (TSX: PZA) and Pizza Pizza Limited (“PPL”) today announced that effective January 1, 2023, the number of restaurants on which royalties are paid to the Company by PPL (the “Royalty Pool”) has been adjusted to include 45 new restaurants opened during the prior year vend-in period, offset by 29 restaurants which were closed during the period.

Source: Pizza Pizza Royalty Corp. Adds 45 Restaurants to the Royalty Pool

The fund will now have 743 stores in the pool for 2023 which is up 2.2% from what it had at 2021 YE but still 4% less than what it had at entering the 2020 fiscal year.

I have chosen to model below expectations for system-wide sales, royalty income, and cash available to shareholders for fiscal 2023. I use an average annual sales per store from fiscal 2018-2022 (I exclude fiscal 2020) to forecast system-wide sales which reflects more normalized same-store sales. I also assume no new stores get added to the pool or get closed. As financing expenses stay relatively constant YoY, I use an average of expenses paid from 2018-2022.

{kind=link}

***Figures in thousands except per share or per store data.

Key takeaways:

- Based on a normalized annual sales-per-store of $725,000 in the system rather than $782,000 which was realized in fiscal 2022, system sales would fall ~5%.

- The payout ratio would certainly test 100%, as it was already 94% at 2022 FYE. The sub 100% payout ratio since 2020 YE has helped build working capital which would easily bridge the gap for at least four years at current profitability.

- The stock trades at ~17x my normalized price earnings estimate.

Valuation/Verdict

It can't be denied PZA has executed to near perfection in a difficult environment, yet its total return over the past year when it has been most successful hasn't even equaled its dividend yield.

That being said, 16x trailing earnings is not enough to get me excited when the forward multiple is likely to be even higher and its peers such as the aforementioned BPF, The Keg Royalties Income Fund ( KEG.UN:CA ), and SIR Royalty Income Fund ( SRV.UN:CA ) trade at much cheaper valuations and have higher dividend yields (BPF trades at less than 10x forward earnings). You could make the argument PZA stores are more recession and pandemic proof than its peers other than A&W ( AW.UN:CA ) as they are considered more of a quick service establishment rather than a "fine dining" establishment like the rest of the peer group and therefore deserves a higher valuation.

The dividend should be sustainable even if we witness a minor recession due to the working capital reserves but the set up isn't compelling enough for double digit returns which I target. I would consider $12/share a bargain price as that is 15x my 2023 earnings estimate.

For further details see:

Pizza Pizza: Execution To Perfection