PAGP - Plains All American Benefiting From Permian Growth

2023-12-08 22:58:07 ET

Summary

- Plains All American Pipeline is a liquids-focused midstream company that has experienced distribution cuts in the past but is now showing signs of stability.

- The company's earnings are derived primarily from crude oil gathering, storage, and transportation, with a smaller portion coming from natural gas liquids.

- The increasing gas-to-oil ratio in oil wells and the volatility of crude volumes versus natural gas volumes present challenges for Plains, but the company has spare capacity for growth.

Plains All American Pipeline, LP ( PAA ) is a liquids focused midstream master-limited partnership partially owned and fully operated by their general partner, Plains GP Holdings, LP ( PAGP ). Like many similarly structured partnerships, the changes to their corporate structure over the past several years resulted in a roller-coaster ride as their distribution was cut 3 times. First, the consolidated company eliminated their incentive distribution rights back in mid-2016, which had been draining $620 million per year to the general partner. That sounds like a favorable change, but the move caused a 21% reduction in the distribution to limited partners ($2.80 down to $2.20/unit).

Then in 2017 plunging profits from its Supply & Logistics segment triggered another 45% reduction in the annual distribution from $2.20/unit to $1.20/unit. After a brief rise to $1.44 in 2019, they received a COVID 50% cut to $0.72. Fortunately, it has steadily risen back to $1.07 since then. During the 3 rd quarter earnings release, Plains announced a probable distribution increase of $0.2 to $1.27 per common unit (payable in February 2024). At $14.95, that would yield 8.5%, a relatively healthy amount. Despite the rocky past, PAA earnings have been consistent recently, and their medium-term outlook appears likewise stable with modest growth expectations in the next 3 years as spare capacity in their Permian portfolio of gathering lines, intra-basin and long-haul pipelines make a substantial recovery. If you’re an income seeking investor, Plains could be a stable addition to your portfolio.

Liquids Focused Midstream

It’s important to note that Plains is a liquids focused midstream company. Unlike similar midstream companies that primarily focus on natural gas and natural gas liquids, Plains straddles the other side of the business – crude oil and natural gas liquids. Approximately 83% of their EBITDA is derived from crude oil gathering, storage and transportation. The other 17% is focused on natural gas liquids (NGLs). The NGL side of their business is derived from their Canadian assets, not the Permian where the near-term growth resides.

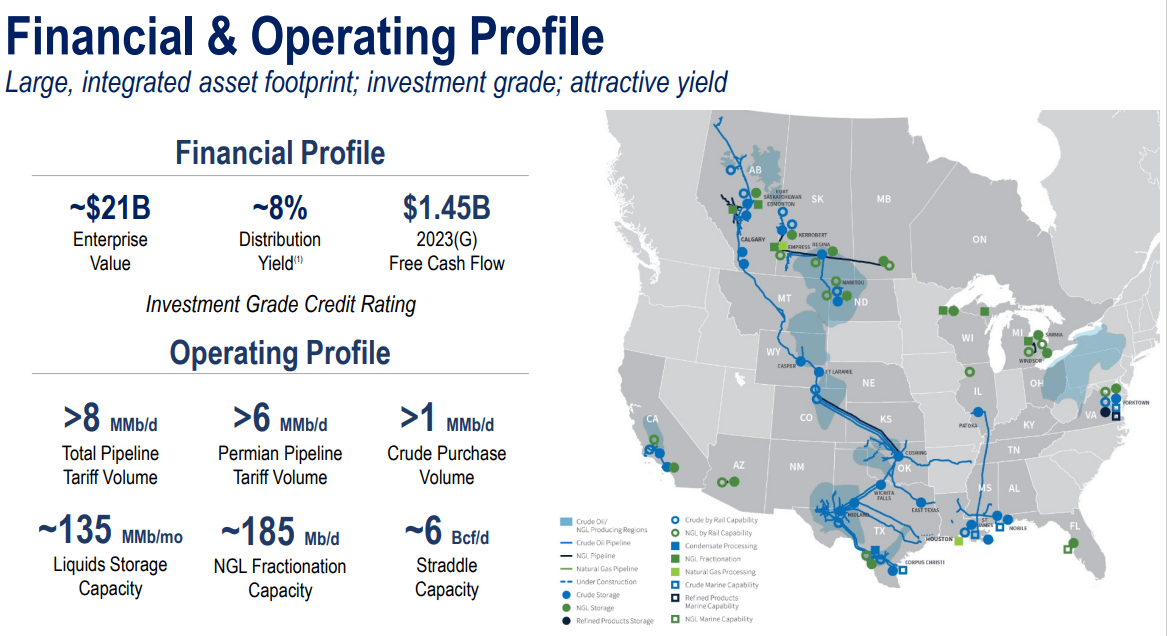

Plains All American Midstream Assets (Plains Investor Presentations)

{kind=link}

The liquids focused business brings on some disadvantages. In general, the earnings of the oil side of the business is more volatile (and historically less profitable), although recently, it has moved into more stable ground. The adjusted EBITDA estimate for 2023 was upgraded at the 3 rd quarter earnings call from an estimated $2.55B (high-end of previous guide) to $2.625B (at the midpoint of the current guidance).

Plains' adjusted EBITDA millions of dollars 2015-2023 (Plains' SEC filings)

{kind=link}

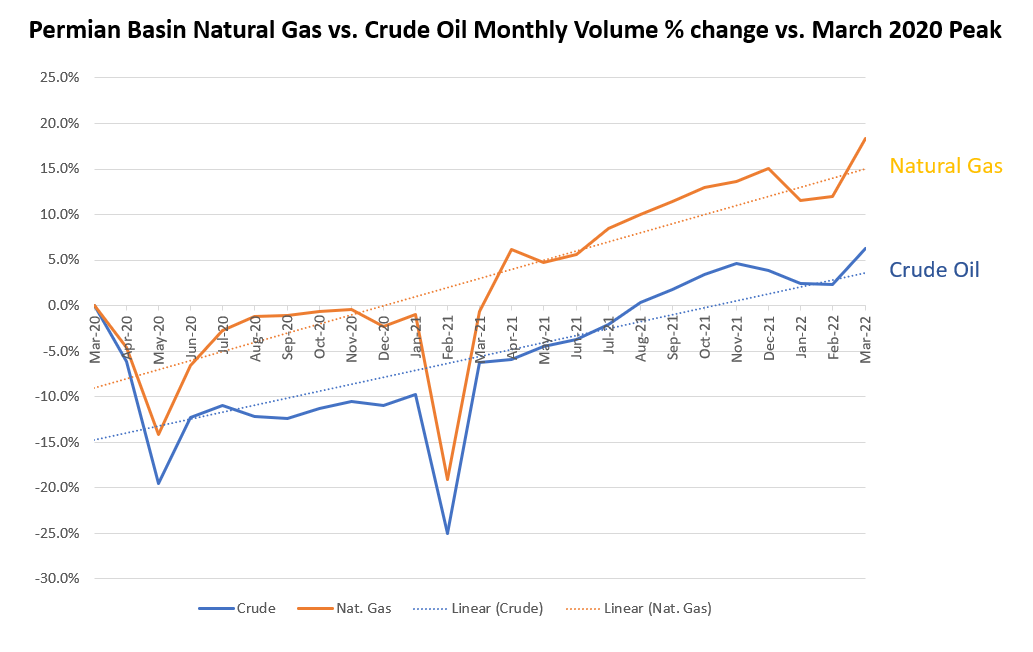

The volatility in Plains’ dividend and earnings outlook is due in part to the volatility in crude volumes. For example, during COVID, the Permian crude volumes dropped by as much as 19.5% from the March 2022 volumetric high versus natural gas which only dropped 14.1% from high to low. Natural gas volume recovered to the former peak within one year versus crude which required an additional 5 months to recover. (Note, the 2 nd drop in the chart was due to storm Uri which roiled the commodity markets in February of 2021 as gathering lines froze in the Permian, but quickly recovered the following month).

Permian Natural Gas vs. Crude Oil since March 2020 (Author, data from EIA)

{kind=link}

Rising Gas-to-Oil Ratios!

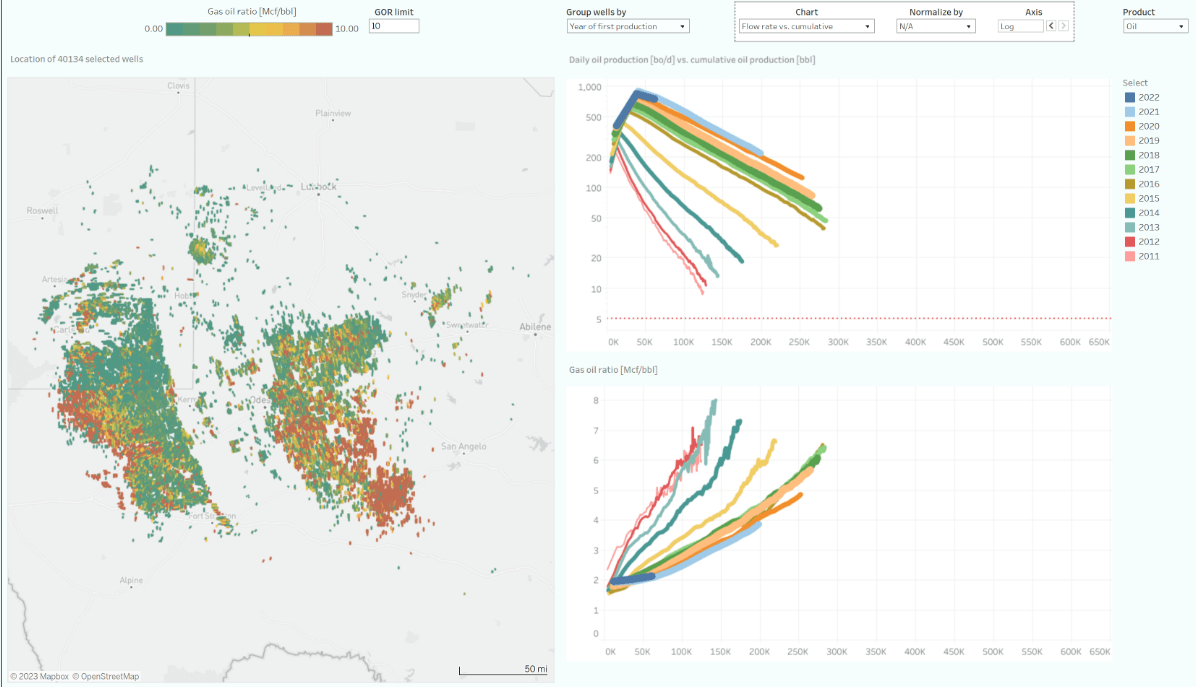

The production of Permian associated natural gas also declines slower relative to crude, so there is an ever-increasing gas-to-oil ratio (GOR) in oil wells that produce associated gas. You can see this in the above chart as a divergence in the linear lines between natural gas and oil in the Permian Basin. Producers are drilling for oil, but those wells become proportionally gassier over time. Also, as drilling moves from the prime tier 1 acreage to weaker drilling areas in the coming decades, the chosen wells will produce less oil and more gas. The gassier locations are part of the reason these future drilling sites are classified with higher tiers. In the following image from Novi , you can see the gassier regions of the Permian represented by the orange to red shading in the left-hand chart, while the oilier sections are in green.

{kind=link}

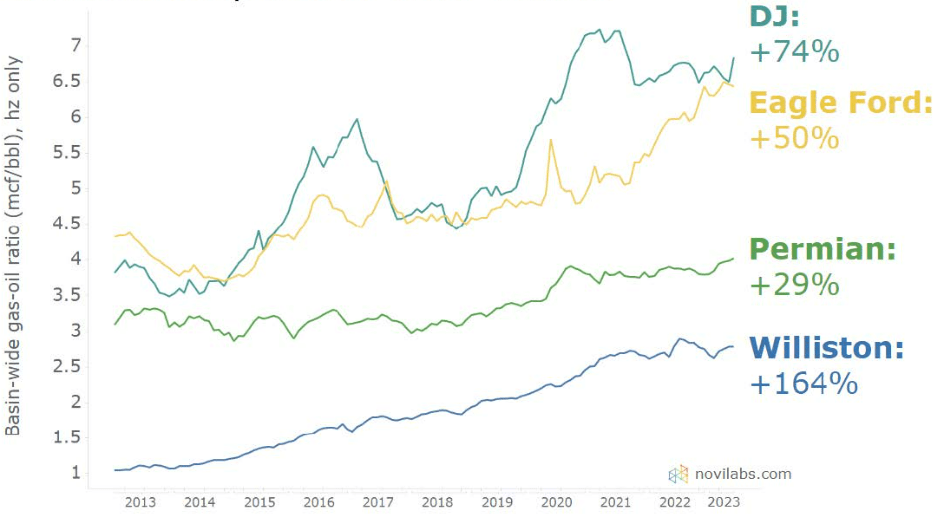

The rising GOR favors the NGL/Natural gas midstream companies versus the oil midstream companies like Plains. This divergence will become more pronounced in the coming years as drillers shift to Tier 2-4 locations in the Permian. The GOR problem is not just a problem for the Permian basin but all oil focused shale basins. Here we can see the Permian is doing better than other oil basins for various reasons.

Oil focused basins GOR ratio 2013-2023 (Novi)

{kind=link}

The trend in the Permian shows that drillers have become increasingly focused on better oil production areas at the expense of natural gas, and they are getting more oil per well relative to previous generations as shown by the two charts on the right. Drillers have combated the higher GOR problem by focusing on better drilling sites and employing better techniques. We know that greater proppant loads and frac intensity increase both oil and gas production, but proportionally speaking, it produces a greater volume of oil relative to gas in the Permian. As proppant and frac intensity has increased, and as drillers favored better drilling sites, they have reduced but haven’t eliminated the problem of higher GORs over time.

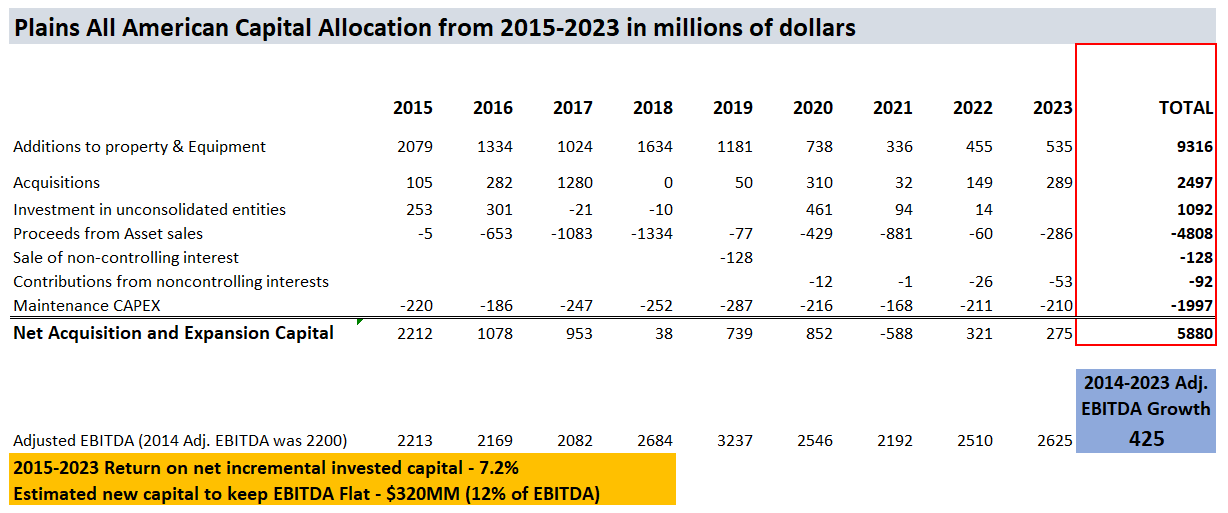

Capital Allocations

Another way to visualize the challenges of investing in the oilier side of midstream is to look at capital allocation. Capital allocations for Plains show a business that invested heavily in 2015-2020 period – close to $6B (net of asset sales) while their adjusted EBITDA grew just $425MM ($2200MM in 2014 to an estimated $2625 in 2023). Their return on net invested capital of 7.2% is near their cost of capital, which is not a good sign. It means that from the common unit holder’s perspective, investing large sums of additional capital into the crude side of the shale boom from 2015 to 2020 hasn’t been productive – the financial term for this is “value neutral.”

Plains' return on net acquisition and expansion capital (Author, data from Plains' Annual reports 2014-2023)

{kind=link}

On a more positive note, it also suggests that there is a fair amount of spare capacity into which Plains can grow. Although drillers generally face higher drilling costs over time, G&P midstream companies tend to spend less to connect a well because they have already invested in the high-pressure lines, long haul pipelines, storage facilities and other expensive infrastructure in the earlier days of the shale boom. Over time, their pipes cover more acres and so it becomes ever easier and less expensive to connect an additional well.

With a much lower capital intensity, better days for the common unit holder are ahead. The net acquisition and expansion capital is leveling out in that $300MM range and we are even seeing growth in the EBITDA numbers from $2510MM in 2022 to $2625MM in 2023 at the midpoint of the guide (4.6% growth). Again, what this is telling us is that they have a lot of capacity into which they can grow and rationalize all that previous investment, and given the lower capital intensity, shareholders should see a rise in returns (in the form of increased buybacks and rising dividends).

Gauging the future for PAA

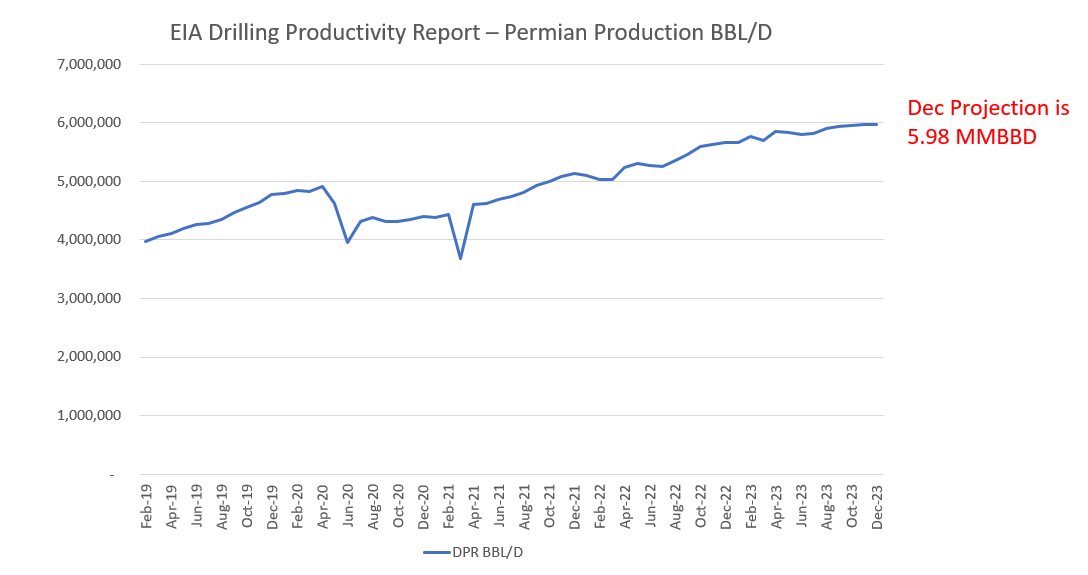

Looking specifically at the Permian, where Plains earns 60% of their 2023 adjusted EBITDA, we can see that this amazing asset is expected to continue to grow over time. If we want to understand where Plains is headed from an earnings perspective, this is a good place to start. Here’s a chart I derived from the EIA’s current productivity report data which shows Permian oil production currently in the 6 MMBBLD area:

Permian Oil Production 2019-23 (Author with data from EIA Productivity Report)

{kind=link}

Given that oil rigs in the Permian have declined to 310 in November from 350 in December 2022 and well completions have fallen from 480 wells per month down to 450 wells per month, it’s clear that the number of rigs and completions will need to increase to drive production levels to higher levels. I suspect that many of the larger public E&P companies are waiting for more natural gas take-away capacity to resume the steady march upward. Matterhorn (a Permian natural gas pipeline) is slated for completion in Q4 2024 and will add 2.5 Bcf/d of additional takeaway capacity.

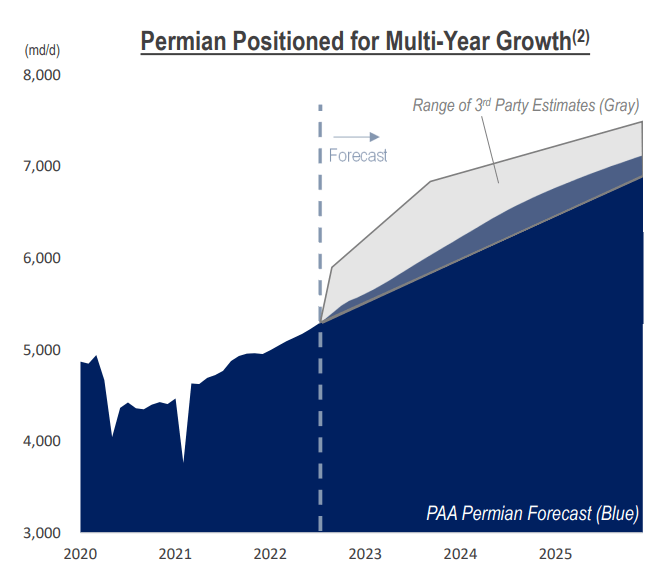

If we look at long-term forecasts for Permian oil, we see moderating, though increasing levels of oil production. Here was Plain's Permian crude volume forecast (dark blue & light blue shaded areas in the following chart) relative to a range of other predictions by various third-party estimators (gray shading which overlaps with the blue). Most third-party forecasts were too high. Plain’s prediction for Permian crude volumes as we head into 2024 is nearly spot on - in the vicinity of 6 MMBD. Their future prediction shows a 1MMBD rise from here to 2026 or a 17% rise in production. This bodes well for their earnings in the next 3 years.

PAA Permian Oil Forecast (Plains Investor Presentations)

{kind=link}

If we extend this projection out to 2030, most charts show the Permian tabling out in the 7 to 7.7 MMBL/D range. Enterprise Product Partners (NYSE: EPD ) has the crude production for the Permian leveling out at 7.7 MMBL/D by 2030.

Permian Oil Production Forecast to 2030 (EPD Investor Presentation)

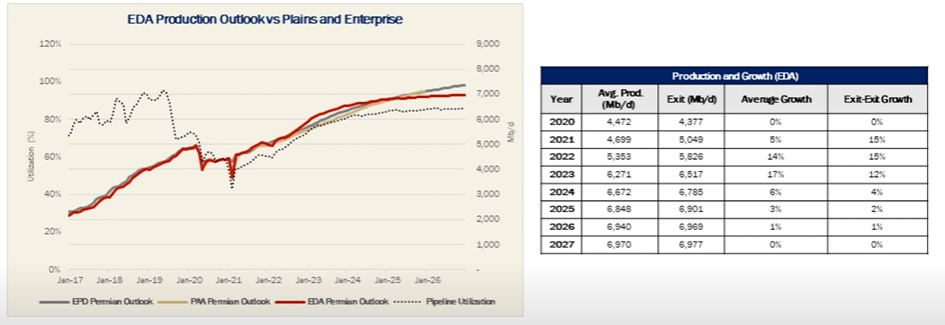

While others take a more modest view and see it tabling out at 7 MMBL/D per day (East Daley Analytics). That’s a roughly 2.5% to 4% annual growth rate.

Permian Oil Production Forecast to 2026 (East Daley Analytics)

{kind=link}

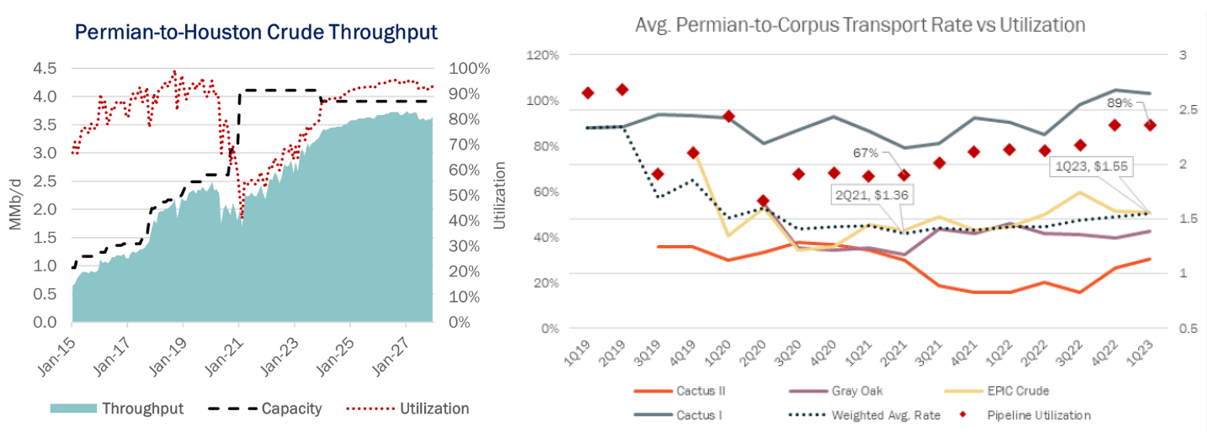

Note, this projection from 2022 shows that East Daley’s 2023 exit rate projections were high, and as stated, we appear to be temporarily tabling out in the sub 6 MMBLD range. Plain's projections were the closest to the mark (yellow line). There is another important factor in the East Daley chart above – Permian pipeline utilization (shown by the dotted line). During the 2019-2021 period, a series of new Permian crude pipelines entered service in anticipation of higher crude volumes which never materialized. Instead, the pandemic curtailed crude volumes leading to a glut of takeaway capacity . As utilizations on some pipelines dropped to the sub-50% mark, Plain’s volumes and margins were hit across the board.

As those pipelines fill up again, healthy margins are returning. For example, the Permian-to-Houston utilizations are expected to leap to 88% by January of 2024 now that a competing crude pipe, Midland to Echo (owned by Enterprise Product Partners), is converting back to NGL service . According to East Daley, current basin fundamentals indicate that tariff rates on pipelines owned by Plains are likely to continue to climb higher for several reasons, including higher pipeline utilization from rising Permian production, higher annual tariff rates (due to indexing linked to rising inflation), a greater portion of uncommitted shipments for shippers who must pay higher spot rates, and the phasing out of cheap incentive rates.

Crude Oil - Permian Pipeline Utilization (East Daley Analytics)

{kind=link}

Note, Cactus I and II are partially owned by Plains and Gray Oak and Epic are competing pipelines. As utilization rises, Catus II tariff rates have the most to gain over time and with it, Plains stands to recapture margin.

Risks

There are several risks for Plains. We've discussed the GOR problem at length. GOR ratios favor midstream companies who process natural gas and natural gas liquids. Plains is at the mercy of ever worsening GOR ratios.

The second risk is the health of the Permian basin and shale in general. Predicting the future supply from a basin with hundreds of E&P companies is always challenging and theories abound about when the Permian will peak and if production will plateau or take a nose dive. Which viewpoint you take largely depends on which data sources you trust and whether drillers hoard their inventory, consume it or sell their wells to companies who don't drill.

All the data and research that I follow suggests that the Permian has decades of running room - up to 30 years - and midstream companies are investing billions in anticipation of its future growth (this is topic we'll cover in a future article). Of course basins can peak for reasons that have nothing to do with how much inventory is buried in the earth's crust.

There is a strong trend towards consolidation in the E&P industry and more potential tie-ups are forecasted. Companies like Exxon are buying companies like Pioneer Natural Resources in multibillion dollar deals. In many instances, we've seen rig attrition as companies buy competing companies and then lay down rigs to preserve drilling inventory. We are currently down 41 Permian oil rigs according to Baker Hughes rig count. In part this is because oil prices have deflated to the $70 per barrel mark, and in part it is a move to preserve the longevity of their assets.

We are also seeing some well degradation in the Permian that is subtle, but measurable over several years of production. The degradation that we've seen isn't catastrophic and has been easily overcome with longer laterals and more efficient drilling. (We'll also take up this topic in detail in that future article).

If you own Plains or other midstream assets, you can take comfort by studying the geology. The Permian is a vast area (75,000 sq. miles) and has up to 3000 feet of thickness per formation. With multiple layered formations (Sprayberry, Wolfcamp, Bonesprings, etc.) to target, Plains and other sources like Enverus estimate that the Permian has 30 years of drilling inventory at current rates, assuming oil prices stay elevated.

Other locations scattered throughout Plains’ footprint don’t have the depth of drilling locations to sustain current production levels passed 2030. These tier 2 oil plays, including the Eagle Ford, Bakken and Niobrara, risk inventory exhaustion by the end of the decade. As inventory becomes exhausted, E&P companies with longer horizons tend to hoard their remaining locations. All of this could depress some of Plains’ crude volumes on their non-Permian pipes beyond 2030.

My preference as an investor is to do what you can to high grade your portfolio. Drillers optimize their production and you should optimize your investments. In my opinion, the stronger opportunities are on the midcap NGL/natural gas midstream side of the equation, but if you already have positions in that space and want to add some incremental exposure to the oil side of the business, Plains could be a nice addition.

Conclusion

Like a teenager whose parents bought them clothes two sizes too big, Plains is growing into their oversized midstream assets. They invested heavily into a Permian build from 2015-2020 in anticipation of continued growth out of the Permian which was put on pause following the pandemic outbreak. Now, the Permian has returned to growth mode. As utilization rates rise on their long-haul pipelines and the Permian resumes its relentless growth, their EBITDA will rise modestly over time – about 3-5% per year. With capital intensity dropping to $300MM per year, more free cash flow will be generated for the shareholders. You will see this in rising dividends and buybacks over time.

When we dive into the specifics of their assets, we see a company focused primarily on the crude side of the shale boom which has been a more challenging midstream investment strategy due to rising GORs and the severity of decline rates on the oil side of the business. Many midstream companies have shed their crude assets to focus on the natural gas and natural gas liquids side of the business, while Plains has leaned into it. If you are looking to diversify into additional midstream names, Plains is a good bet in the short to medium term as rising shareholder returns and modestly increasing earnings keep their share price well supported.

In part 2 of the Plains discussion, we will look at the massive Permian natural gas plant buildout and take a deep dive into well economics to see how the Permian is fairing. Suffice it to say, this basin is still in growth mode and midstream names like Plains stand to benefit.

For further details see:

Plains All American Benefiting From Permian Growth