PAA - Plains All American: Dividend Increase In The Cards

Summary

- Plains announced its plan to prioritize increased distributions.

- The amount of increase might reach $2 a share per year in a few years.

- The business should generate sufficient levels of cash to pay all of its bills, with enough left over for growth.

- The presence in the Permian Basin is the key to Plains' future.

Plains All American Pipeline's ( PAA ) business is returning in strong fashion. With this strength, management notified investors at the last conference its intention to lift distributions. The company announced a formula for calculating future distributions, one we plan to explore at all possible depths. The Plains is flat; the sunny weather makes it all ready to rumble; so let's go rumble.

Latest Quarter Results

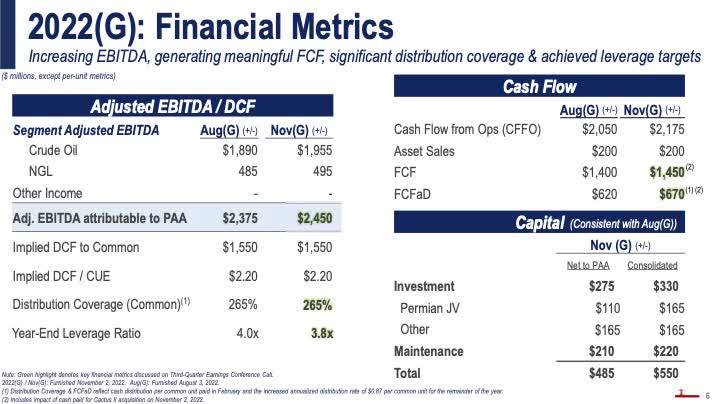

Beginning with updates from the last quarterly report , management increase its 2022 EBITDA guidance by $75 million to $2.45 billion. The increases came through both businesses, crude oil and the NGL business with higher volumes in the former and higher margins in the later. This increase represents $250 higher than the first 2022 guidance offered in February. For the quarter, EBITDA equaled $623 million.

The quarter closed with a leverage of 3.7 and a guided leverage of 3.8 year-end slightly below the mid-range target of 4.

The company also purchased an additional 5% of the Cactus II pipeline increasing its ownership to 70%.

Finally, management stated, " Slide 6 shows our key 2022 financial metrics and reflect strong distribution coverage of 265% with free cash flow [after] distributions at $670 million."

{kind=link}

The Future

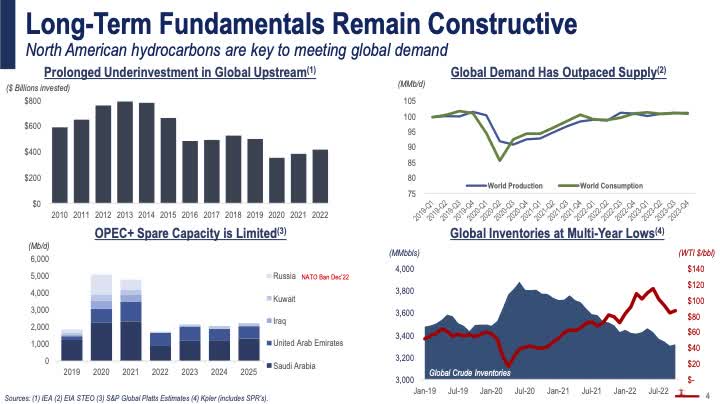

With the present viewed, management commented on the future displaying its vision in the following slide:

{kind=link}

The lower right of the slide shows the extremely low circumstance for world-wide crude inventories. In the top right-hand corner, global demand now exceeds supply. Finally, global spare capacity is almost non-existent. Insufficient investment is the primary cause for this shortage. Global markets remain tight and the world needs short-cycle North American production growth, which leads into the next discussion, Plains infrastructure position.

The Plains' Position

The company's assets rely deeply upon the Permian Basis. The next slide shows the upside leverage available without significant capital investment within that basin.

Plains All American Pipeline

For gathering, the upside equals 35%; intra-basin equals 35%; long-haul equals 35%. Without significant capital, Plains could grow its volumes by 55% plus.

NuStar Energy ( NS ) continues to include a slide on the Permian Basin projected production. With Plains so heavily involved in this region, it is an essential piece for this discussion.

NuStar Energy Wells Fargo Presentation

The upper right-hand corner of the slide predicts flows from the Permian to almost double between now and 2025-26 with 2023 and 2024 increasing from 6 million a day to 8 million a day at crude oil prices around $80. That is a 50% increase. With Plains spare incremental capacity at approximately 55%, EBITDA growth without massive capital becomes a natural result. An example illustrating the magnitude can be derived from the 3rd quarter report. (Note: Plains doesn't break out EBITDA by region.) We created a table to show the effect.

| EBITDA Estimate |

| Total Flow ((MM)) * |

| Permian Flow |

| Total EBITDA |

| Permian EBITDA (Estimate) ** |

| Crude 2021 |

| 6.2 |

| 4.4 |

| $459 |

| Approximately 60% of the volume change drops to EBITDA. |

| Crude 2022 |

| 7.6 |

| 5.7 |

| $536 |

* Basically all the growth in volumes came from the Permian. (1.8 difference verses 1.9)

** Calculation: The difference in EBITDA almost solely resides with change in Permian flows. Permian Flow 2022 divided by Permian Flow 2021, a fractional change of 1.3, compared with EBITDA 2022 divided by EBITDA 2021, a fractional change of 1.17.

From the table listed above, Plains could expect a 30% increase in EBITDA from the Permian over the next two years or approximately $450 million. (The estimating calculation involves starting with the latest crude EBITDA generated, the business percentage from the Permian Basin, the percentage of EBITDA created from the volume difference and an estimate for future Permian production. We stress that this is an estimate and a little complex in thought.)

Continuing, management noted two negative events occurring in 2023 vs. 2022. The first, NGL (natural gas liquids) is expected to be lower for 2023. "Furthermore, current forward markets indicate lower year-over-year frac spreads. The combination of these could lower 2023 NGL segment adjusted EBITDA by roughly $100 million versus 2022 guidance." Second, with its preferred shares going floating into a higher interest rate, management mentioned another negative hit. "If both were to reprice at current market conditions, total annual preferred dividends would increase by approximately $55 million a year . . . " During the Q&A, management made it clear that no plans were in place to repurchase those shares anytime soon. The preferred share value , both A and B are significant being slightly greater than $2 billion. Adding some detail to the preferred issue, Al Swanson, Executive Vice President & Chief Financial Officer commented,

"At some point, we may have the capacity to deal with that. But today, we don't believe that would be prudent to use the leveraging traction to try to reduce that cost. It's actually pretty manageable relative to what the current capital markets are providing and we surely don't want to use equity -- common equity to try to take it out at this point. But all of that could be on the table a year or 2 . . . And the important thing is we do see call options coming our way with this. So we do control our destiny . . . when we get into a position to be able to deal with it."

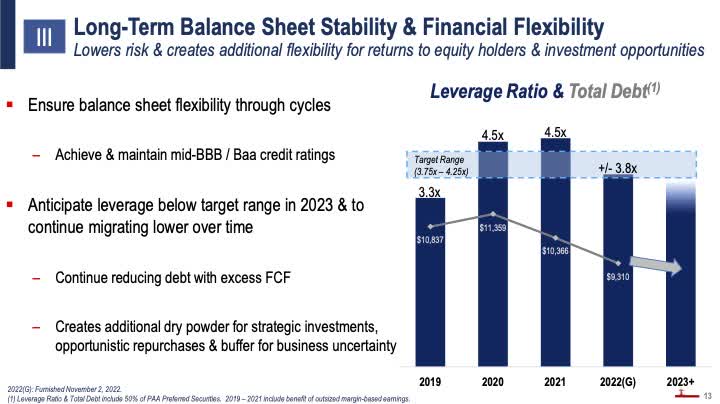

Lastly, the company's financial leverage shown next is within its target.

{kind=link}

Leverage dropped into the targeted range after a precipitous increase in 2020. Interpretation, paying down debt isn't a major issue.

Management also included a general principle vision for its capital allocation.

{kind=link}

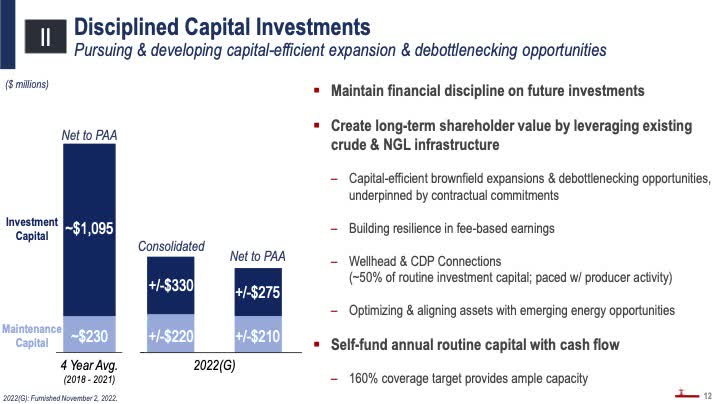

The idea for disciplined capital investments continues, which was communicated in more detail in the next slide.

{kind=link}

Notice that growth capital now falls in the $300 million per year range while maintenance capital remains near $200 million.

An example of recent capital expenditures or enhancing capital assets include a non-cash transaction to gain full ownership of our existing Canadian Empress. In general terms, capital will be targeted at brownfield expansions and debottlenecking, complete purchase of Cactus II, Saskatchewan expansion, or optimization of existing assets. Going forward, capital expenditure are expected to be not focused on massively expansive new ventures.

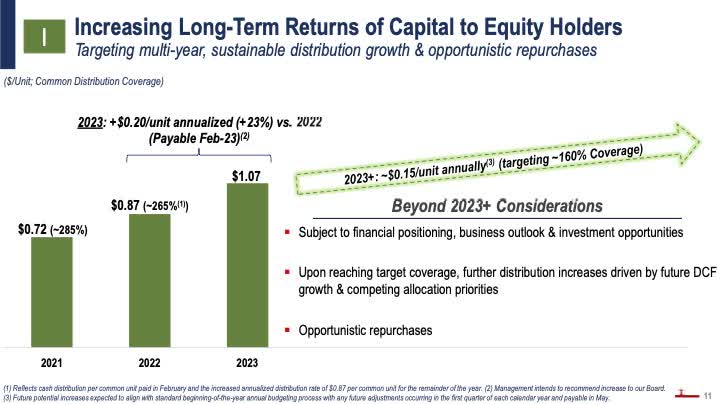

Now, The Plan, The Plan, The Plan

The company plan places dividend increases high on its list shown in the next slide.

https://static.seekingalpha.com/uploads/sa_presentations/831/89831/original.pdf (Plains All American)

{kind=link}

After management stated that it will be recommending to the board an increase of $0.20 for 2023, they added:

"Beyond '23, as part of our annual budget review process with the Board, we anticipate targeting annualized distribution increases of approximately $0.15 per unit each year until reaching a targeted common unit distribution coverage ratio of approximately 160%."

As noted in the slide, "opportunistic unit repurchases will remain a component of our capital allocation framework" which will be a dynamic assessment of business outlook, market environment and capital allocation options.

With respect to debt maturities, Swanson again answered a question from Brian Reynolds of UBS concerning priorities. He noted that Plains' had a liquidity of $3.3 billion with $600 million in cash. Because the cash was earning a higher interest rate than the note due early next year, the company was holding off paying for it. He summed up next year's debt reduction intention to take out the entire $1.1 billion due and not access the market.

Balancing the Cash

With growth anticipated from the key basin, a simple calculation shown above estimates future EBITDA growth giving investors a qualitative picture. The company has approximately 700 million shares outstanding. Each 15 cents added cost approximately $100 million. The anticipated hike in February adds $150 million. We estimated the 4th quarter by adding a meager amount of $15 million to the September actual results.

Management noted that for next year, two negative factors equaling $150 million will drag on cash flow results, but they also reassured analysts that they still expected growth in spite. Jeremy Goebel, Executive Vice President & Chief Commercial Officer for Plains answered a question on this subject, ". . .I think his comment in the script, I think it was from Al actually was that we would expect year-over-year growth." Formally, management stated that the crude business would grow and the NGL business would decrease. During the 2022, the crude EBITDA grew much more than the $100 decrease expected in the NGL business.

The next slide adds depth into the past cash flow calculation.

{kind=link}

From the above slide, the following table approximates cash flow for the next few years. Management strongly claimed growth going forward including next year in spite of the $150 million headwind. The company also expects growth in years afterward. With adjusted EBITDA of $2.45 billion guided for 2022, it isn't much of a stretch for $2.6 billion in 2023. And the same is true for some modest level of growth estimated in 2024.

| Cash Balance (Millions) |

| EBITDA |

| Capital |

| Distribution |

| Debt Maturities |

| Total Expenses |

| Net Difference |

| 2023 |

| $2600 |

| $300 |

| $850 * |

| $300 ** |

| $1500 |

| $1100 |

| 2024 |

| $2800 |

| $300 |

| $925 |

| $750 |

| $2000 |

| $800 |

* Plains paid $700 million in 2021 in distribution. The preferred costs will increase by roughly $50 million plus at 700 shares the expected basic distribution will increase by $100 million.

** Plains has a total debt of $1.1 billion to retire in 2023 and will have approximately $800 in cash by 2022 year's end. The net difference is $300 million.

Note: The increase from the Permian noted above might be $450 million by 2024. In the table, we used a much more modest approach only adding $300 from 2022 guided result near $2500 million.

It is clear that the coverage ratio isn't going to be a restriction for distribution increases going forward even if the business only slightly grows. It is also very evident that the business is generating plenty of cash for capital investment increases and for share repurchase or retiring the $2 billion plus worth of preferred stock.

The numbers calculated offer some level of insight into the coming financial future for Plains. For example: the company likely has enough cash after all investing and distributions to cover the coming debt due in 23 and 24 dropping obligations from $8.3 billion to approximately $6.5 million. In 2025, the company has another $1 billion due, which could also be paid off. With the debt lowered to $5.5, Plains could then convert the preferred, now $2 billion plus to debt returning the total debt to $7.5 plus billion. After EBITDAs in the $2600-$2700 million range, leverage remains lower than 3. Going forward over the next few years, Plains All American Pipeline might find itself in a transformative position. It might pay much higher than $2 distributions. It could invest in a totally different business such as hydrogen transportation in significant fashion without needing to head to the bank. Rumbling through the plains offered investors a very pleasant experience.

Risk

For Plains and other companies focused in on fossil fuels, risk from government interference or major world health issues, either perceived or real. Plains hit under $5 during the last economic health shutdown, yes, under $5. But, the key portion for Plains is it's already in place, spare capacity within the Permian Basin and an ability to grow almost immediately. We added shares recently, because we strongly believe that going forward, the distribution will reach at least $2 per year. At that rate, the stock price will more than double from today's value at $12. Investors can skate along collecting nice rewards while capital appreciation marches along in the Plains. On any weakness, our view changes to strong buy.

For further details see:

Plains All American: Dividend Increase In The Cards