PAA - Plains All American Pipeline: A 7% Yield Protected By The Permian Basin

2023-10-04 15:20:42 ET

Summary

- Plains All American Pipeline holds strong midstream positions inside the Permian Basin that connect to Houston, Corpus Christi, and Cushing.

- The company's current 7 percent dividend is projected to grow at growth rates that significantly outpace its peers, however, rising interest rates pose a risk.

- The company has a manageable balance sheet that is backed up by strong free cash flow, giving the company capital flexibility for the foreseeable future.

- The company operates in two of the counties in New Mexico with the strongest oil production growth in the Permian Basin.

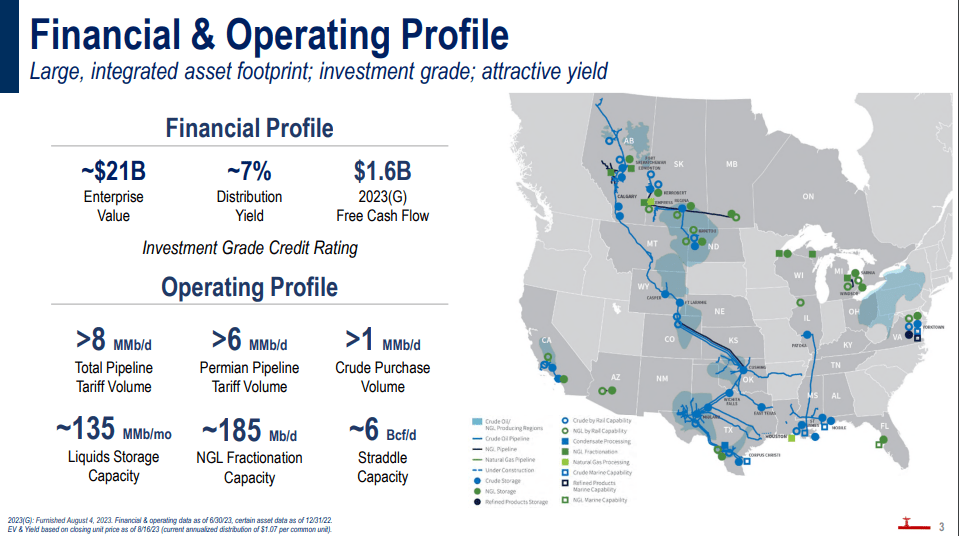

Plains All American Pipeline (PAA) is a midstream master limited partnership company with operations that span from Canada to Texas and currently trades with a market cap of $10.7 billion and offers a rich 7 percent distribution yield.

The company has strong leverage to the Permian Basin with a well-established footprint in the play.

The company has a total pipeline tariff volume of greater than 8 million barrels per day. Six million of those 8 million barrels per day is focused in the Permian Basin.

Plains All American Financial Profile (PAA Q3 Presentation)

{kind=link}

Distributions

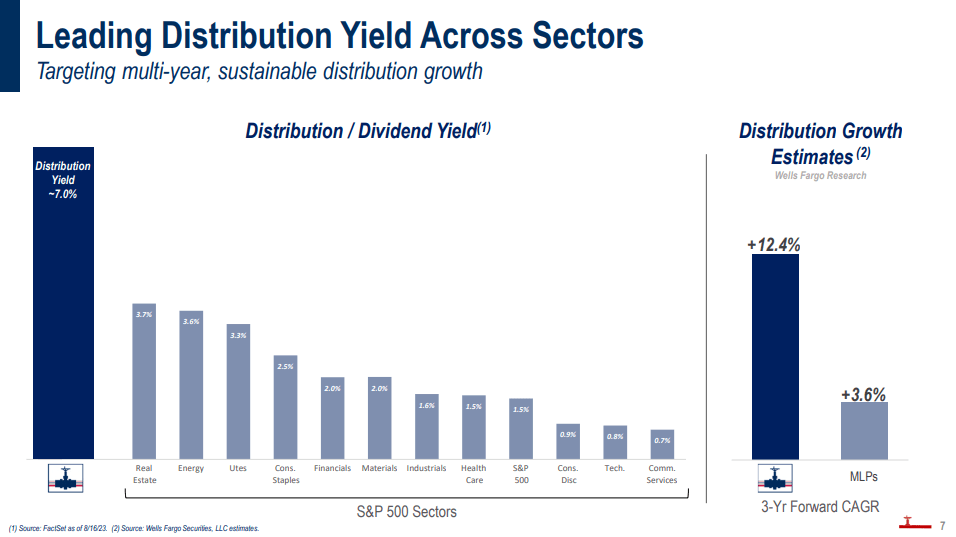

When someone purchases an MLP pipeline company, the majority of the yield usually comes from the company's distribution. MLP's have tax-advantages in that when money is used to purchase units in an MLP, the units purchased is considered a capital contribution and the distributions are considered a return of capital, which are tax-free until the total capital contribution amount is recouped.

PAA currently offers a distribution yield of 7 percent currently. This far outpaces the average distribution/dividend yield in other sectors of the economy as demonstrated below. Also, they expect to have a CAGR (Compound Annual Growth Rate) in their distribution of 12.4 percent which is an estimate/expectation provided by Wells Fargo. Compared to average expectations among MLPs, this distribution growth is around 9 percent greater than the average.

This is due to its exposure to the Permian Basin as we will discover below. I wrote an article last month describing how energy exploration companies are tomorrow's steady dividend payers, but traditional MLPs can also provide strong yields from their distributions. Especially when leveraged to the Permian.

Plains All American Distribution Comparison (PAA Q3 Presentation)

{kind=link}

A Permian Basin Focused MLP

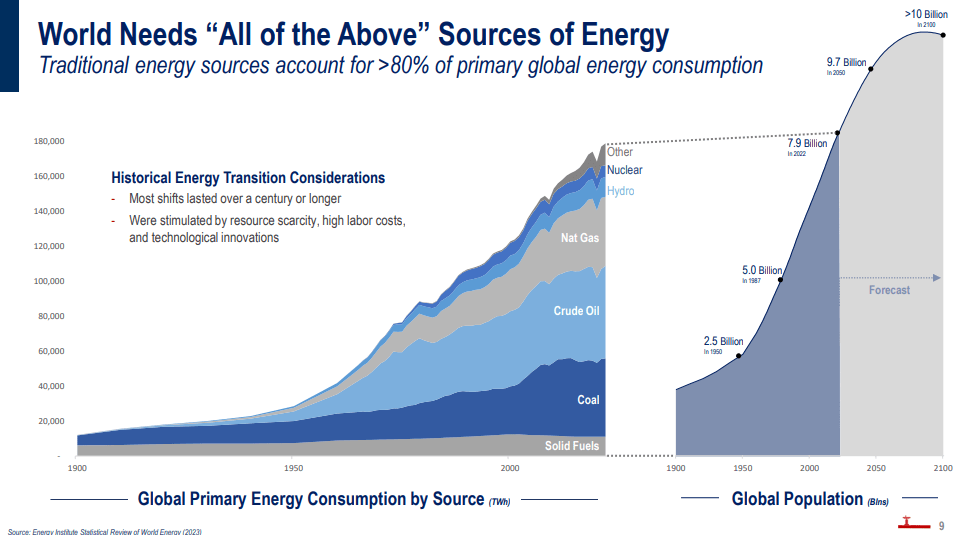

In the following slides, PAA puts the narrative that the world is quickly transitioning off of fossil fuels to rest.

In this slide, the company demonstrates how the narrative is a narrative based on fear and not logic. Fossil Fuels currently make up a strong majority of energy production and to transition away from that "overnight" would have catastrophic consequences for the world, and simply isn't feasible. As I've stated in other articles, the fossil fuel narrative is a false one which when you look at the world on a global scale, its common sense that third world countries are not going to quit using fossil fuels. Why? Because they are the most reliable and economical sources of energy.

The global population is forecast to continue growing aggressively into 2050 and beyond. I would even suggest that the global population is not going to see a rounded top as shown here. Historically, the world population is forming an exponential curve and even the Malthusian's greatest warnings and efforts aren't going to stop it from continuing on an exponential curve...and to be clear, this is a great thing. Not something to be feared as the aforementioned Malthusians would like you to believe. Nonetheless, the narrative that suggests fossil fuels are quickly being phased out, is to be strongly ignored.

Sources of Energy For the World (Plains All American Q3 Presentation)

{kind=link}

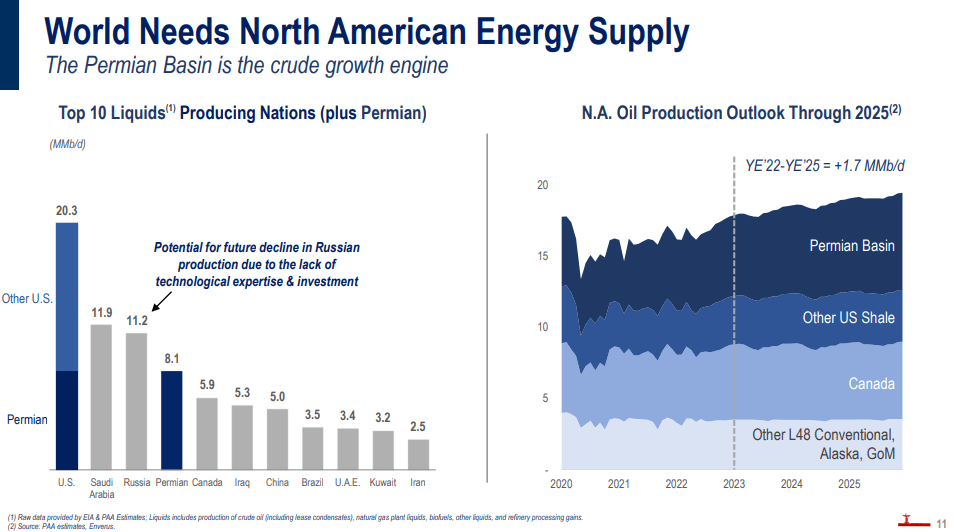

Here, the slide demonstrates that America IS the premier liquids producing nation in the world. Keep in mind that this slide is compiled by factoring in natural gas liquids and not just oil production. On the right hand side, it highlights where North America's future oil production is expected to come from...and the most growth is going to be the prolific Permian Basin. To sit on the sidelines in fear that the world is moving away from fossil fuels is a fear that is not based in facts.

North American Energy (Plains All American Q3 Presentation)

{kind=link}

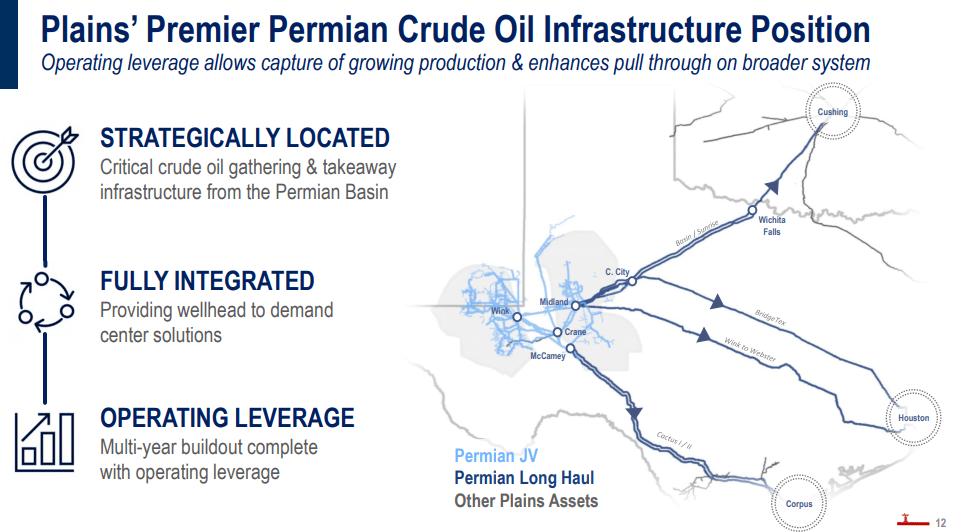

This slide "drills" in on the Plains All American's pipeline position inside the Permian Basin. As was mentioned before, the majority of their pipeline capacity comes out of the Permian Basin. They have long haul pipelines going to three of the major United States oil hubs in Cushing, Houston, and Corpus Christi.

Plains All American Texas Pipelines Long-Haul (PAA Q3 Presentation)

{kind=link}

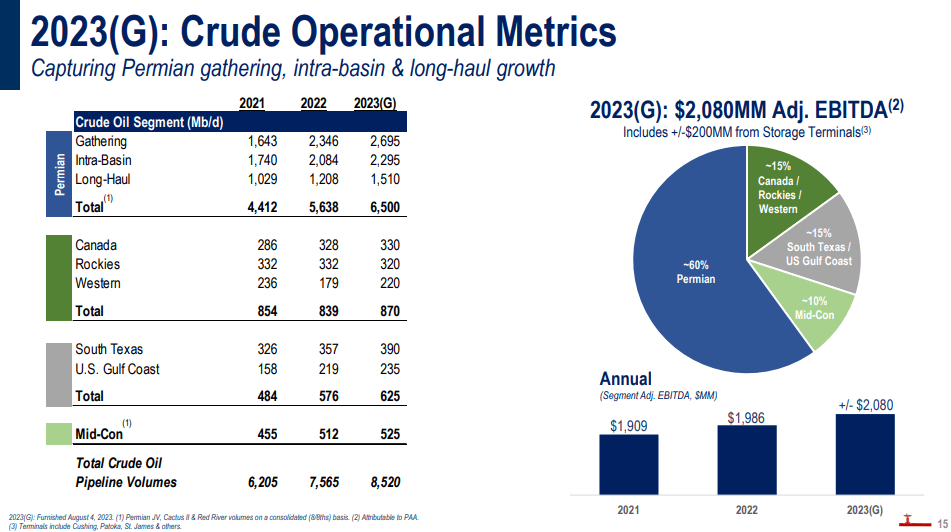

Here, we can see that their 2023 estimated EBITDA will be roughly 60 percent due to the Permian Basin operations. And as far as volumes are concerned, they have experienced impressive volume growth since 2021, primarily in the Permian Basin (blue) and other regions in Texas (grey).

2023 Crude Pipeline Volume Growth (Plains All American Q3 Presentation)

{kind=link}

Cash Flow Analysis

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| TTM 2023 |

| Operating Cash Flow |

| 2,608.0 |

| 2,504.0 |

| 1,514.0 |

| 1,996.0 |

| 2,408.0 |

| 2,907.0 |

| Cap-Ex |

| (1,679) |

| (1,181) |

| (752) |

| (373) |

| (539) |

| (570) |

| Free Cash Flow |

| 929 |

| 1,323 |

| 762 |

| 1,623 |

| 1,869 |

| 2,337 |

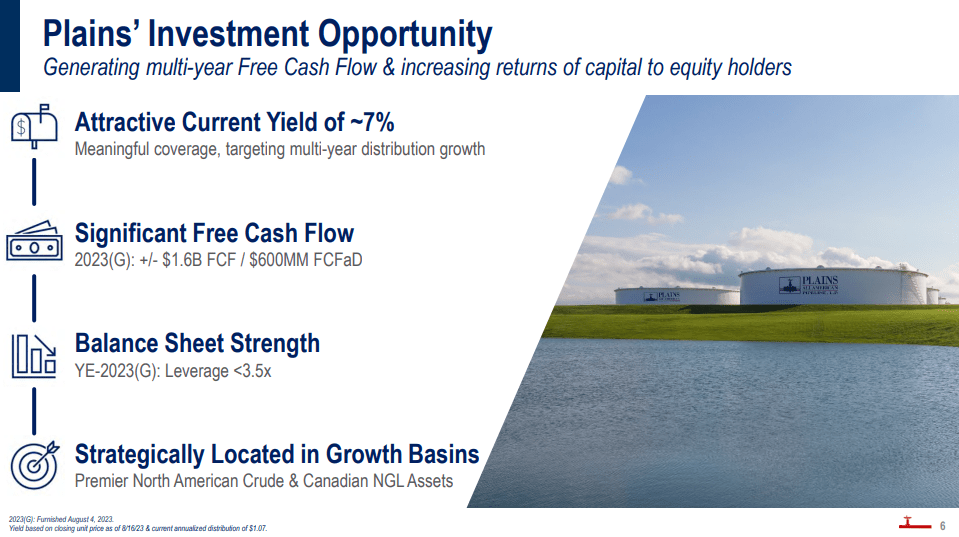

The company has experienced strong growth rates of free cash flow over the years while managing capital expenditures well. Much of the capital expenditure for their Permian Basin pipelines has been spent and so only incremental capex will likely be needed as demonstrated by the CapEx trend in the table above. This bodes well for the company's free cash flow flexibility as they determine the best use of capital...whether that be distributions, accretive acquisitions, or retiring debt.

The company's operating cash flow has not grown as quickly as free cash flow but since 2021, it has seen strong growth rates of over 20 percent per year. It will be interesting to see if this trend can continue into 2024 and beyond. As we shared earlier, Wells Fargo projects that the company's distribution is going to grow over 12 percent per year. For the company's distribution to grow at this rate, it only makes sense that Wells Fargo expects it to grow its operating cash flow as well.

Plains All American Investment Opportunity (PAA Q3 Presentation)

{kind=link}

Balance Sheet

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Q3 2023 |

| Assets |

| 25,511 |

| 28,677 |

| 24,497 |

| 28,609 |

| 27,892 |

| 26,900 |

| Debt |

| 13,473 |

| 15,448 |

| 14,745 |

| 15,799 |

| 14,378 |

| 13,298 |

| Debt-to-Assets |

| .53 |

| .54 |

| .60 |

| .55 |

| .52 |

| .49 |

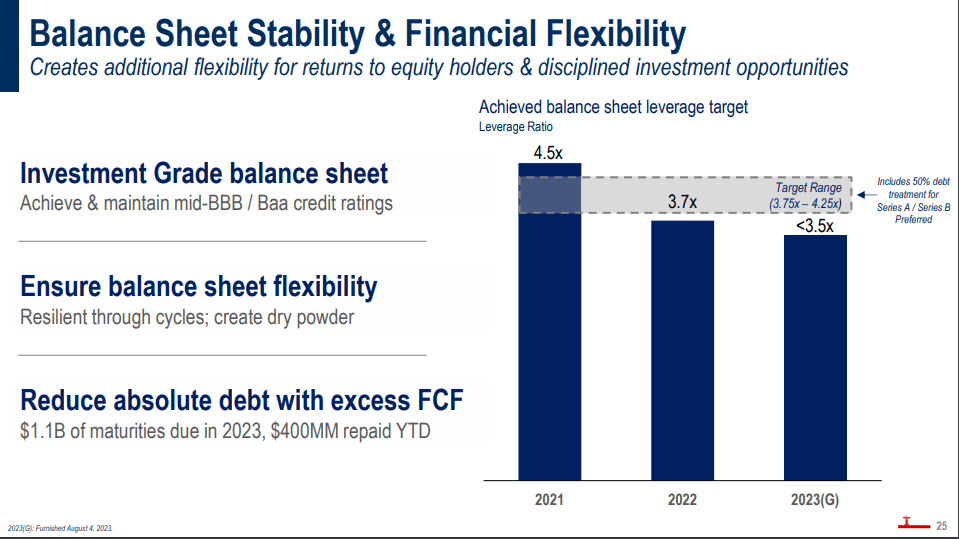

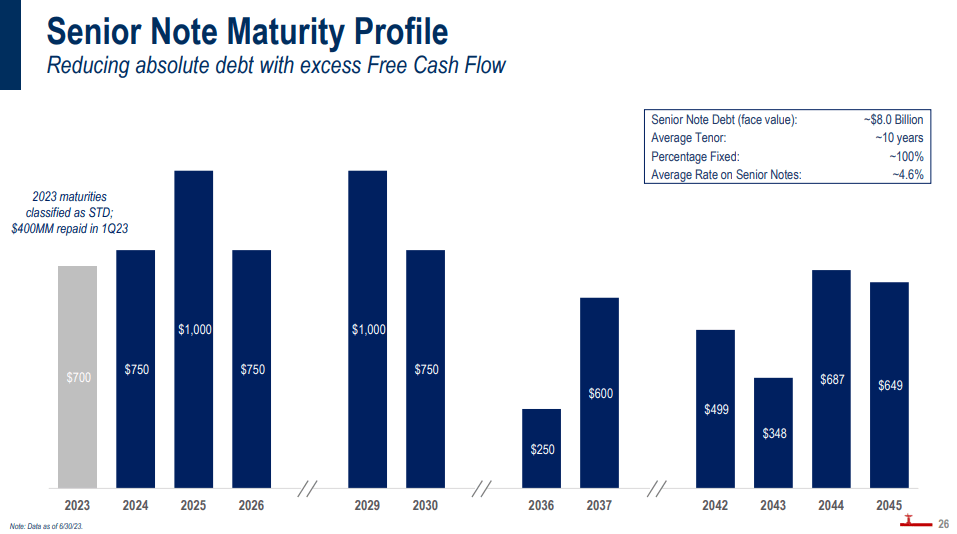

Across the stock market, and in the energy sector, companies are beginning to become more fiscally responsible. Plains All American is no different and they plan to retire some of the 1.1 Billion of debt maturing in 2023. As of this slide, they had retired $400 million in 2023 and will continue to manage the balance sheet in order to maintain their investment grade rating.

Plains All American Balance Sheet (PAA Q3 Presentation)

{kind=link}

Here is a snapshot of their debt maturity profile. Right now, they have attractive rates on their Senior Notes, but it will be imperative that they remain flexible and open to what interest rates continue to do in the near future. If interest rates continue to rise, it will become more appealing to retire debt rather than reinvest capital. The company has significant debt maturities in 2024 through 2026 so it will be interesting to see what percentage they roll over into new debt and what percentage they retire.

Plains All American Senior Note Maturities (PAA Q3 Presentation)

{kind=link}

Recent Acquisition

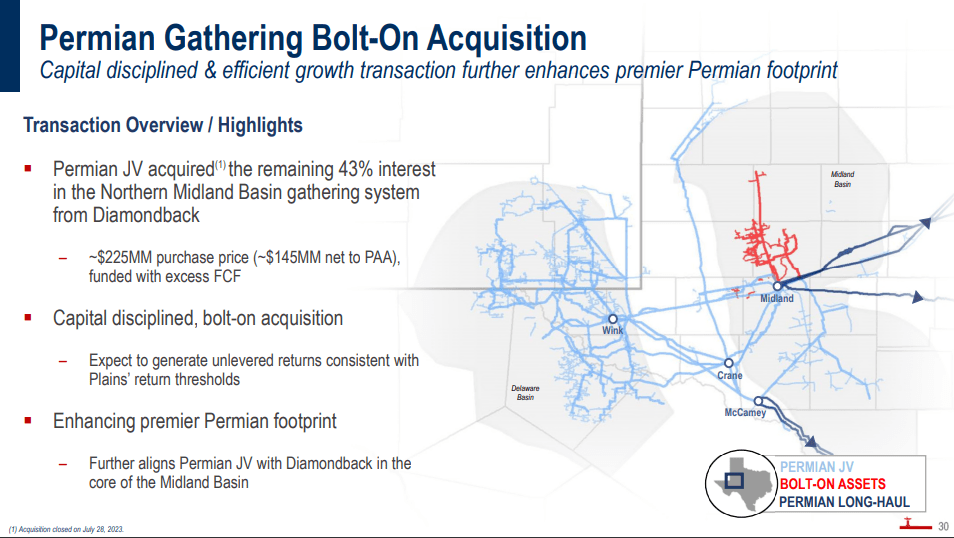

In July of this year, the company acquired the "bolt-on" assets of Diamondback Energy in the Midland Basin. Those assets are highlighted in red below and represent a 43 percent interest in OMOG JV LLC. This slide shows how the company already has extensive reach into the Delaware Basin and now through this acquisition, the company furthers its reach into the Midland Basin. This acquisition leverages the company to one of the larger producers in the basin, Diamondback Energy ( FANG ).

Also, as the next section will discuss, it is important to understand the company's exposure to the two New Mexico counties shown on this graphic.

Plains All American Permian Basin Acquisition (PAA Q3 Presentation)

{kind=link}

Permian Basin Oil Growth

We've already seen from Plains All American how they expect the Permian Basin oil production to grow. But is there a third party resource to verify this with? Confirmation from another source may confirm that Plains All American Pipeline is set up for years of growth from the Permian Basin.

Here's a chart from the Energy Information Administration that further confirms the investment thesis for Plains All American Pipeline. The chart shows how oil production has grown in the Permian Basin since 2010. Notice how the EIA highlights the production that is coming from Lea and Eddy Counties in New Mexico. They are highlighting this production because prior to horizontal drilling, these counties were not producing very much crude oil. Now, thanks to horizontal drilling, these two counties are prolific producers.

Returning to the graphic above that highlights Plains' area of operations and you will notice that Plains All American's web of pipelines extends deep into Lea and Eddy counties. This is confirmation that Plains All American Pipeline will be positioned to profit from the Permian Basin's growth for many years to come.

EIA Monthly Permian Basin Oil Production (Energy Information Administration)

Here is a quote from that same article provided by the EIA.

Output from horizontal wells in the two counties accounted for 29% of all crude oil production in the Permian Basin in the first quarter of 2023, averaging 1.7 million barrels per day (b/d), according to data from Enverus.... Permian crude oil output increased to 5.7 million b/d in March, the most recent month for which data are available. That amount of output compares to an average of 5.3 million b/d in 2022 and 4.7 million b/d in 2021. Horizontal wells in Lea and Eddy counties accounted for 60% of total growth in the region in the first quarter of 2023, compared with 44% in first-quarter 2022. Source: EIA

Keep in mind that natural gas production is also increasing dramatically in the region and natural gas production has doubled since 2021 in Lea and Eddy counties thanks to efforts to unlock oil via horizontal drilling.

Risks

The biggest risk I see for a company like Plains All American Pipeline, which isn't specific to PAA, is a rising interest rate environment. We've been in a ~50 year bull market for bond prices and given this was somewhat manufactured by an overly reactive Federal Reserve, we could be in for a much more dramatic rise in interest rates than we have already seen. Currently, a 30-year home mortgage interest rate sits above 8 percent and a fixed CD rate has jumped to over 5 percent. This may change where capital flows as fixed interest becomes more attractive.

Although a fixed rate of interest is great if interest rates are high and inflation is contained, but if interest rates are 5 percent and inflation is still a concerning factor, then fixed interest products are at a disadvantage as they don't give you any hope to outpace inflation. I believe that is where we find ourselves...in a stagflationary environment.

Nonetheless, the risk of rising interest rates could cause the market to reprice company share prices lower relative to their dividend/distribution rate so that their risk/reward is more in line with fixed interest rates. This could even happen in light of higher oil prices which if that occurs, then you can suspect that stagflation is the trend and companies leveraged to hydrocarbons would become even more attractive.

The second risk I see is if the Permian Basin suddenly depletes its reserves and there isn't as much oil in place as previously thought. I view this as a very minor risk. If the Permian suddenly depletes faster than expected, you and I will have bigger concerns than stock prices.

And lastly, a risk that should be considered is the regulatory risk. Every company is becoming "ESG friendly" to avoid any legalities from governments, whether they be federal or state. Although the constitution would forbid it via what would be a long legal battle, there is always the risk that a company gets penalized for its ESG practices or lack thereof.

Conclusion

Plains All American Pipeline is a buy. The company is leveraged strongly to the Permian Basin which will continue to be a source of growth for the company. There is very little danger posed to the strength of the company's cash flow and thus its distribution. It already has a strong distribution relative to its peers and this distribution is projected to grow at a rate that is multiples more than the average distribution growth rate of its peers, according to analysts from Wells Fargo.

If you are an energy investor, or a dividend investor, then gaining leverage to the cash flows that will come out of the Permian Basin over the next several decades is one of the best investment decisions available right now, in my opinion.

For further details see:

Plains All American Pipeline: A 7% Yield Protected By The Permian Basin