PAA - Plains All American: Raising Price Target On Continued Strong Performance

2023-11-08 17:00:20 ET

Summary

- PAA posted a solid Q3 despite some lower than expected volumes out of the Permian.

- The company will look to increase its distribution by 19% next year.

- Trading at one of the lower valuations in the midstream space, PAA remains a "Buy."

Back in May, I started Plains All American ( PAA ) with a “Buy” rating, saying it was once of the cheapest stocks in the midstream space and that it should benefit from increased Permian oil production growth. The stock has returned over 18% since then, versus an over 5% return for the S&P over the same period. In August , I reiterated my "Buy" rating, saying the company had a lot of room to increase its distribution. With the company recently reporting earnings, let’s catch up on the name.

Company Profile

As a reminder, PAA is a liquids focused midstream operator that operates in two segments: Crude and NGLs. It Crude segment is the larger of the two, accounting for over 80% of its EBITDA and includes gathering, intra-basin, and long-haul pipelines, as well as storage assets. The Permian is its largest basin, making up about 60% of the segment’s EBITDA.

PAA's NGL segment consists of assets primarily located in western Canada and includes 4 natural gas processing plants and 8 fractionation plants, as well NGL storage, pipelines, rail terminals, and rail cars. About 60% of the segment's EBITDA comes from fracs spreads and marketing, with the rest from fees.

Q3 Results

For the most-recent quarter, PAA recorded adjusted EBITDA attributable to PAA of $662 million, which was an increase of 6% from a year ago.

Crude Oil segment adjusted EBITDA came in at $553 million, a 3% increase from $536 million a year ago. Throughput volumes in its Crude Oil segment rose 9% to 8,259 Mb/d. The Permian saw volumes jump 7% to 6,114 Mb/d. The company credited it improved Crude Oil Segment results to higher tariff volumes, tariff escalations, the timing of MVC deficiency payments, and bolt-on acquisitions.

NGL segment adjusted EBITDA, meanwhile, climbed 15% from $86 million to $99 million. The company credited the gains to higher margin and NGL sales volumes, noting that last year the company was impacted by turnarounds.

Implied distributable cash flow ((DCF)) available to common unitholders came in at $431 million, up 12%. On a per unit basis, it was 62 cents, up 13% from 55 cents a year ago.

PAA paid a distribution of 26.75 cents in the quarter. It had a coverage ratio of 2.30x and excess DCF of $244 million.

Free cash flow was -$386 million versus $726 million a year ago.

The company ended the quarter to $7.75 billion in net debt. Its leverage stood at 3.4x.

Overall, PAA posted solid results despite seeing some lower-than-expected volumes in the Permian, as other basins had strong volumes while it also benefit from annual tariff escalators. Permian volumes were impacted by some weather-related issues that impacted gas processing capacity as well as some field compression issues. These ultimately should be temporary and not impact the longer term PAA story, but it will impact it for the rest of the year.

The NGL segment is more variable and the company benefited from stronger regional basis differentials and higher realized frac spreads. This is more a spread business, and there has been a lot of volatility in spreads.

2023 Outlook

Looking ahead, PAA said it now expects 2023 adjusted EBITDA to be between $2.60-2.65 billion. That’s up from a prior outlook of $2.45-2.55 billion.

PAA now expects free cash flow for the year of $1.45 billion. It expects to end the year with leverage under 3.5x.

The company will recommend the board increase its distribution by 19% to $1.27 from $1.07.

PAA also announced that its Permian JV acquired Rattler Midstream's Southern Delaware Basin crude gathering system and LM Energy’s Touchdown crude gathering system for $205 million in aggregate, or $135 million net to PAA. Management said the deals are expected to generate unlevered returns in line with its return thresholds of approximately 300 to 500 basis points above its weighted average cost of capital ((WACC)).

Discussing its outlook for Permian volumes moving forward on its Q3 earnings call , CEO Willie Chiang said:”

"This has been a little bit of a strange year in that we had some weather issues in the summer that really impacted both second and third quarter. Our original guidance for the year was 500,000 barrels a day growth exit to exit. We updated on our last call that we thought it was going to be a little bit below that. Our views now is it's probably in that 350,0000 to 400,000 range for the year. But the thing I wanted to share with you is if you look at our October volumes and gathering, this may address your question, we're actually 175,000 barrels a day higher in October than we were for the third quarter. So it really gives us confidence in the fourth quarter. You never can perfectly predict the future, but we are seeing increased volumes as we start the fourth quarter off and then certainly, a lot of the recent announcements, particularly with 1 of the large transactions in 1 of the very large super majors really lends support and aligns our view of the Permian going to be around for a long, long time as we go forward.”

Lower than expected Permian volumes will continue to impact PAA the rest of the year, but higher tariffs and the two bolt-on acquisitions (which should continue $10-15 million in EBITDA) will more than make up for this, leading the company to raise its EBITDA guidance by $50-100 million. In addition, Permian volumes were running much higher in October versus Q3, showing the temporary nature of the volume impact. NGL frac spreads, meanwhile, remain volatile, but the company is well hedged for Q4 and has also hedged out two-thirds of its 2024 expected volumes.

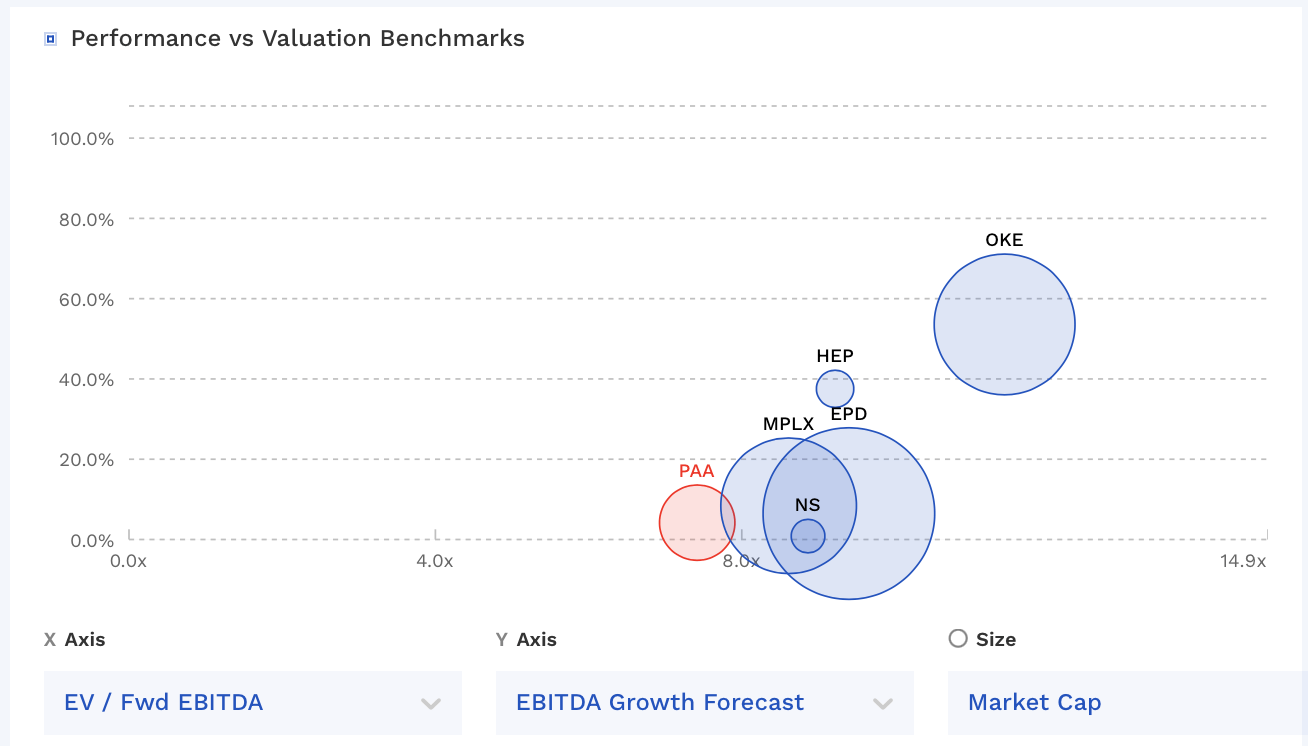

Valuation

PAA currently trades at 8x the 2023 EBITDA consensus of $2.63 billion, and 7.8x the 2024 EBITDA consensus of $2.64 billion.

It trades around 9.1x its core Crude segment '23 EBITDA of approximately $2.125 billion.

On an FCF basis, the stock has an FCF yield of 10.4% based on a 2023 FCF forecast of $1.15 billion. For some reason the company includes assets sales when it discusses free cash flow, but I leave that out of the calculation. The stock yields about 6.8% on its current distribution and 8.2% on its proposed distribution.

PAA trades at one of the cheaper valuations among its midstream peers. A 9x multiple, which many of its peers command would equate to a $22 priced stock, while and 8.5x multiple would be a $20 stock. Given its strong balance sheet and its ties to growth in the Permian, I think the stock needs to trade more in line with its peers.

PAA Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

Despite its solid results, it actually hasn’t been an easy year for PAA. Industrywide Permian volume growth did not materialize as much as it was projected to at the start of the year, which was supposed to be one of its main drivers. However, the company was still able to put up some solid results and increase its outlook, helped by tariff increases and solid results from other basins.

I think that should bode well for next year, as at the end of the day, the Permian is still the best growth basin in the U.S. and PAA is uniquely set up to benefit from volume growth in the basin given its underutilized pipelines in the region. Meanwhile, the company just nicely raised its distribution for next year, and should have room to continue to do so in years beyond that as well. With the stock still trading at a discount to peers, I’m going to raise my price target from $17 to $20.

The biggest risks to the downside would be a steep decline in oil prices, which could lead to decreased oil production and the volumes that go through PAA's pipelines. Continued natural gas takeaway constraints in the Permian is another risk, which could impede oil production in the region. Pipelines are being built and coming online, but natural gas production keeps rising and it remains an issue in the basin.

For further details see:

Plains All American: Raising Price Target On Continued Strong Performance