PAGP - Plains All American's Outperformance Is Not Reflected In Its Share Price

Summary

- Plains All American Pipeline, L.P.’s results have exceeded our expectations.

- We now see greater capital appreciation upside and distribution hikes for Plains All American Pipeline over the next few years.

- We explain the rationale for our increased price target for Plains All American Pipeline.

Plains All American Pipeline, L.P. ( PAA ) is a top contender for the Most Improved Player in midstream. Before the pandemic, the company suffered years of distribution cuts, overspending cash flow, a rising debt load, ill-advised acquisitions, and huge asset write-downs.

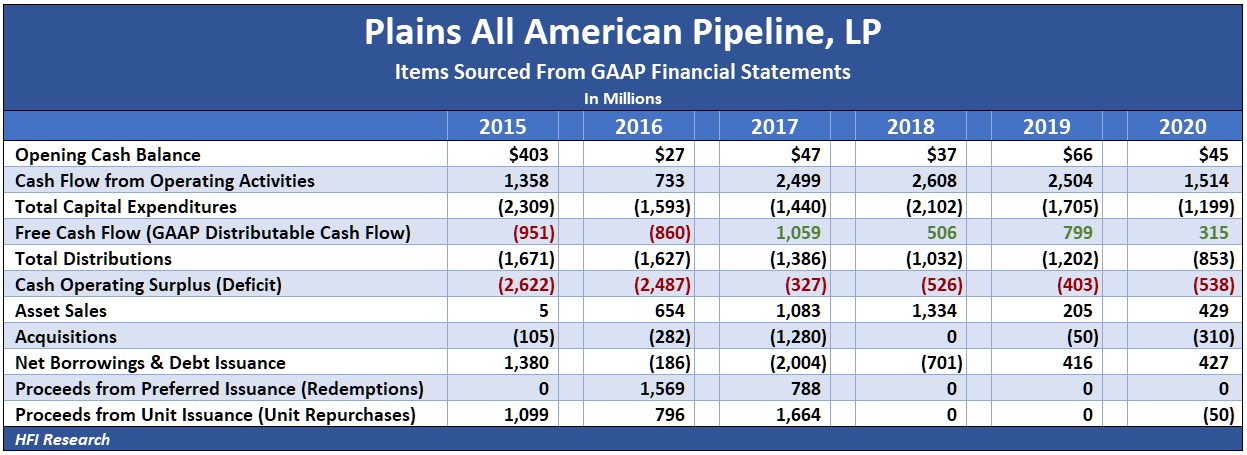

The table below shows how, prior to 2020, PAA operated at a cash flow deficit that it plugged by selling assets and by issuing debt, preferred equity, and common equity.

{kind=link}

Between 2015 and 2020, PAA ran a cash flow deficit of $6.9 billion, made acquisitions totaling $2.0 billion, and paid down $0.7 billion of debt. Those cash outflows were funded through $3.7 billion of asset sales, $2.4 billion of preferred unit issuance, and $3.5 billion of common unit issuance.

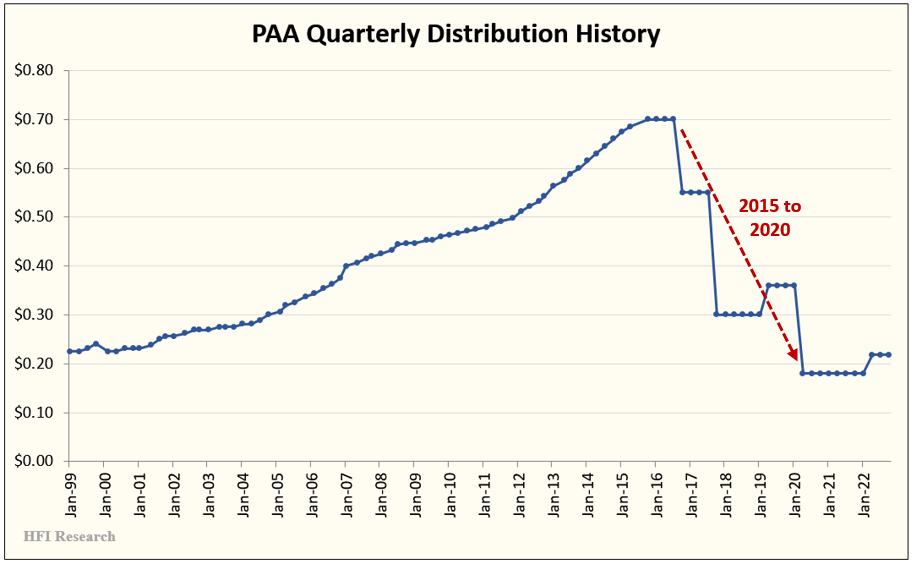

What were unitholders left with after that frenetic capital allocation activity? First, they saw their units decline by 82%, from $50 in early 2015 to $9 at the end of 2020. They also saw their quarterly distributions fall from $0.70 per unit in 2015 to $0.18 in 2022, a 74% decline.

{kind=link}

Clearly, management’s capital allocation program was a failure.

Righting the Ship

In 2020, PAA’s management vowed to change its stripes. Like its large midstream peers, it told equity owners it would manage for cash flow and reduce leverage.

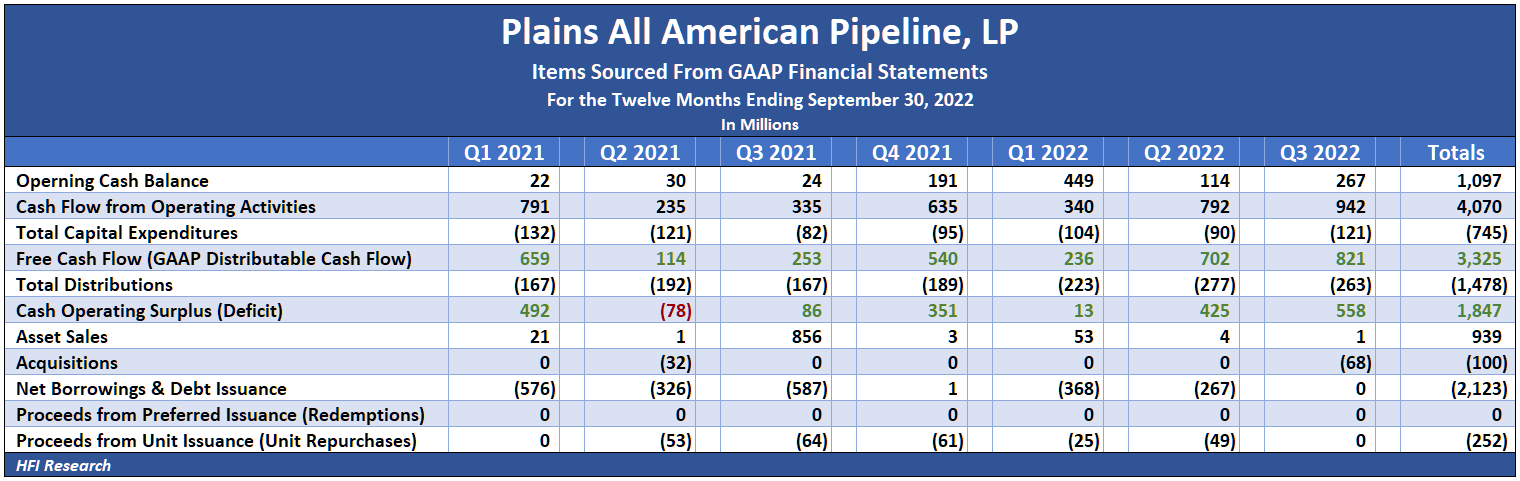

Fortunately for unitholders, that’s exactly what it did. The table below illustrates management’s success in generating a cash flow surplus in 2021 and year-to-date in 2022.

{kind=link}

From 2021 through the end of the third quarter of 2022, PAA generated $1.8 billion of surplus cash and completed $0.9 billion of asset sales. Of that cash, it used $2.1 billion to reduce debt, $0.3 billion to repurchase common units, and $0.1 billion for acquisitions. This level of discipline is like night and day when compared with PAA’s pre-pandemic behavior.

We would have found the 2015 to 2020 PAA uninvestable. The company was spending far beyond its resources to participate in a midstream infrastructure growth boom that was bound to end in overbuilding. These are the kinds of situations we seek to avoid.

But we became interested in PAA equity after we were confident that the industry’s capital cycle had turned. During 2020, the entire midstream industry swore off acquisitions and major growth projects in favor of generating surplus cash, reducing leverage, pursuing measured organic growth, and returning cash flow to equity owners. When we became confident that PAA would follow the midstream herd, we bought PAA units on March 2, 2021, at $8.91.

PAA also had an added kicker in the form of operating leverage in its Permian system, which had just finished an expansion phase as Permian throughput volumes fell. While overcapacity can often be a drag on a company’s results after an industry bust, PAA’s system was large enough to capture a significant proportion of future Permian oil production growth. As Permian production volumes picked up, PAA was well-positioned to benefit as its revenue grew without the need for much additional capital spending.

Sure enough, PAA's quarterly capex, which averaged $400 million from 2015 through 2020 has fallen to an average of $93 million since the first quarter of 2021. The lower spending freed up cash flow for management to allocate toward reducing debt, unit repurchases, and distribution increases.

This operating leverage tailwind, and to a lesser extent, the improved results in its other operating segments, caused PAA’s results to improve dramatically in short order. Its results continued their upswing in the third quarter of 2022. The year-over-year comparisons are as impressive as any of PAA’s midstream peers.

{kind=link}

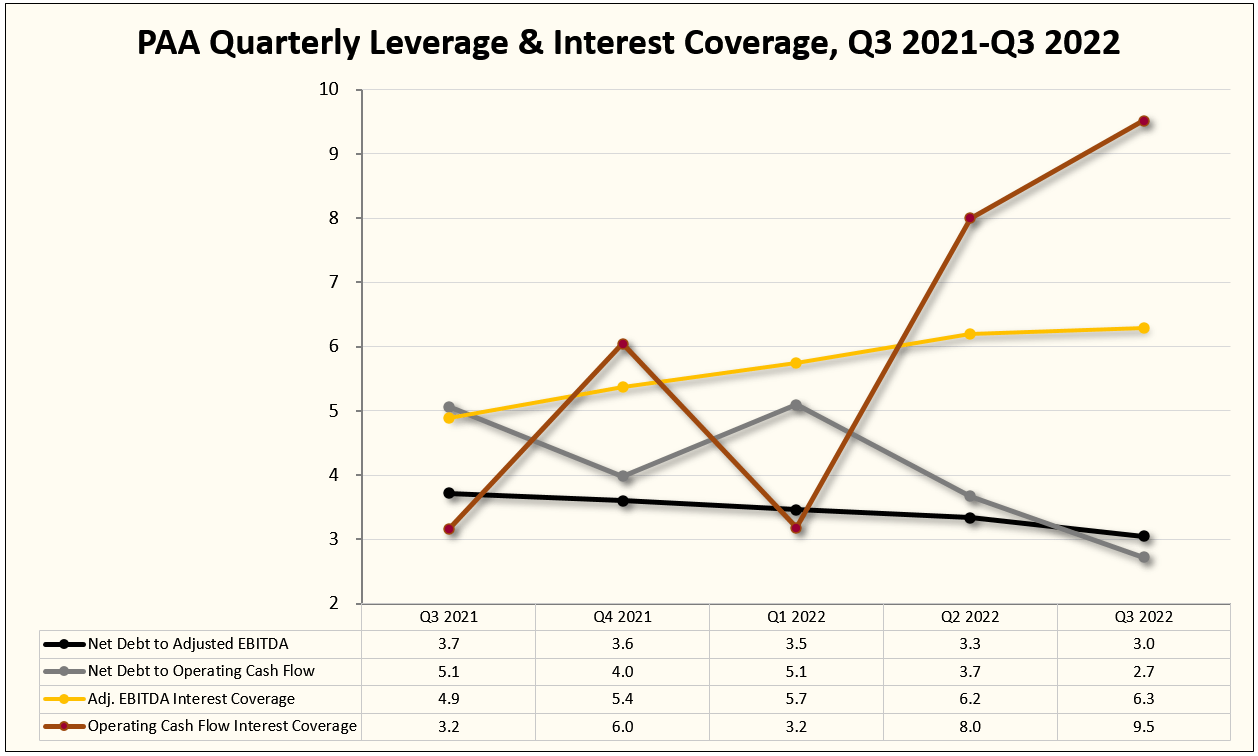

PAA’s impressive financial improvement is also evident in its credit metrics. Its leverage ratio and interest coverage ratios have all trended positively over the past year.

{kind=link}

Looking Ahead

We expect PAA’s management to continue with its conservative capital allocation policy. Its most recent move is along those lines. On December 14, PAA sold its stake in its Fort Saskatchewan joint venture for an attractive multiple of 11-times. Management intends to use a portion of the proceeds to reduce leverage.

While PAA’s high cash flow growth rate in recent quarters is set to slow, its large margin of cash flow after distributions—which currently amounts to $0.73 per unit—should provide a large enough cushion to provide for additional deleveraging and, eventually, distribution hikes. Management has pledged to increase distributions annually until the payout is covered 1.6-times by distributable cash flow.

So while PAA’s 7.5% current distribution yield is attractive on an absolute and relative basis even without future distribution increases, we expect future distributions to increase the yield over the next few years.

Valuing PAA Units

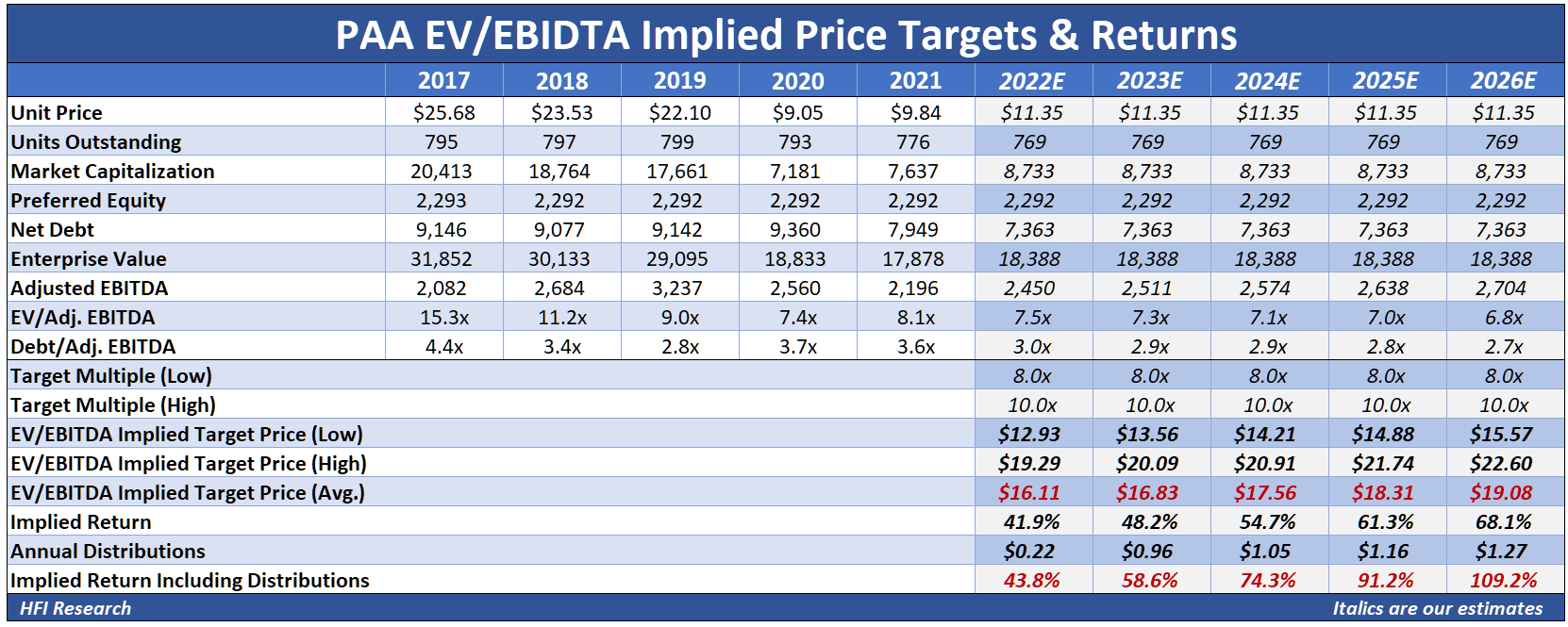

In valuing PAA based on EV/Adjusted EBITDA, we assume Adjusted EBITDA increases by only 2.5% per year and that PAA doesn’t pay down any more debt, doesn’t repurchase any more units, and hikes its distribution by 10% annually through 2026. Under these assumptions, the units are currently worth approximately $16 and have 109% total return upside over the next four years.

{kind=link}

With the units trading at $11.35, they have 43.8% upside based on 2022 Adjusted EBITDA, which offers unitholders both a substantial margin of safety and significant near-term upside.

In light of this valuation—which we view as conservative—and our confidence that management will continue to allocate capital conservatively, we are increasing our PAA valuation from our current range of $12.00 to $14.00 per unit to a higher range of $14.50 to $16.50. Our price target is the midpoint of our value range, or $15.50. PAA units currently offer 36.6% upside to our price target.

Investors could also buy shares in PAA’s corporate entity, Plains GP Holdings, L.P. ( PAGP ). PAGP shares possess virtually identical economic characteristics as the PAA MLP common units. Prospective PAGP buyers should be aware that the shares currently trade at a 6.2% premium to PAA units, which is higher than the average premium over the past few years.

Conclusion

PAA units and PAGR shares are a solid buy. They will benefit from the company’s position as a dominant Permian liquids-weighted midstream operator and from its other assets, which continue to recover from the post-pandemic downturn. We expect unitholder-friendly capital allocation to be the “icing on the cake” of our Plains All American Pipeline valuation, but the prospects are good that it will further increase the units’ value. Income investors seeking a conservative equity that offers significant capital appreciation and distribution growth prospects should consider PAA units or PAGP shares.

For further details see:

Plains All American's Outperformance Is Not Reflected In Its Share Price