PAA - Plains All American Yields Over 7% And Looks Undervalued

2023-08-30 08:45:00 ET

Summary

- Plains All American is an undervalued opportunity with a 7% yield and low valuation.

- PAA's infrastructure connects critical basins in the US and Canada to the Gulf Coast, positioning it well for future growth.

- PAA has shown financial growth, reduced debt, and increased its distribution, making it an attractive investment option.

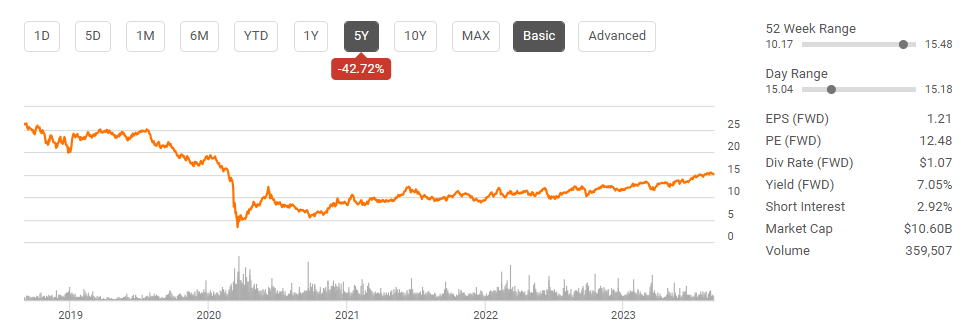

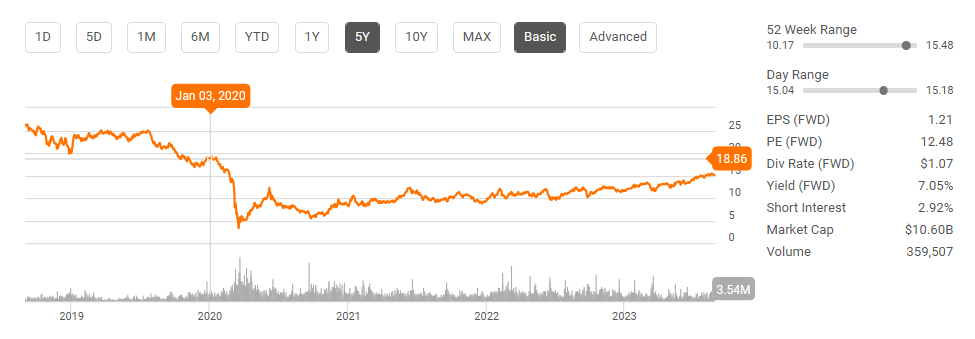

Whenever I write about Energy Transfer ( ET ) or Enterprise Products Partners (EPD), the one company that consistently turns up in my valuation models as an undervalued opportunity is Plains All American ( PAA ). I am not a unitholder of PAA just yet, but after reading through their publications , I am getting much more interested. PAA yields just over 7%, has a low valuation at a $10.6 billion market cap, and its pipeline allows crude to be transported from several critical basins in the U.S. and Canada to the Gulf Coast in Corpus Christi Texas. PAA has lowered its debt, increased its revenue, and grown its FCF since 2019, yet its unit price is still lower than its pre-pandemic levels. While PAA is having a strong year, with its units up over 30% YTD, there is still room to run as I am looking for it to go back into the $20s in 2024.

{kind=link}

Why I feel PAA is positioned well for the future

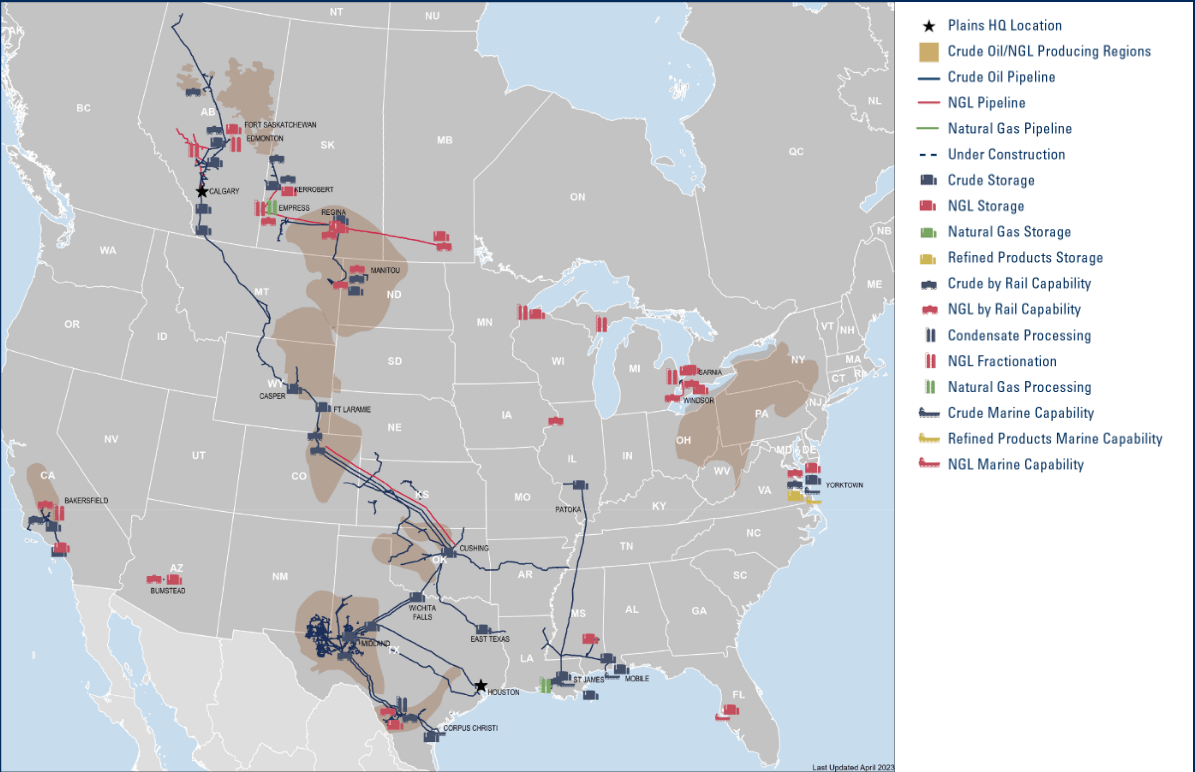

PAA is an interesting energy infrastructure company as its focus is predominantly throughout the centralized region of North America. While PAA provides critical infrastructure to our economy, it provides significant takeaway capacity and access to the U.S. and global energy markets for Canadian crude and NGLs. PAA operates 18,300 miles of Crude Oil | Plains All American Pipeline pipelines and has 74 million barrels of commercial crude storage capacity. PAA has 4 marine facilities and operates 7 crude rail terminals. On the NGL side of its business, PAA operates 1,620 miles of NGL pipelines, 9 fractionation plants, 4 processing facilities, and 16 NGL rail terminals. PAA is a full-service energy infrastructure company providing takeaway capacity through pipes, trucks, and rail, and storage for upstream exploitation and production companies to connect with refiners and exporters to international markets in the crude markets.

{kind=link}

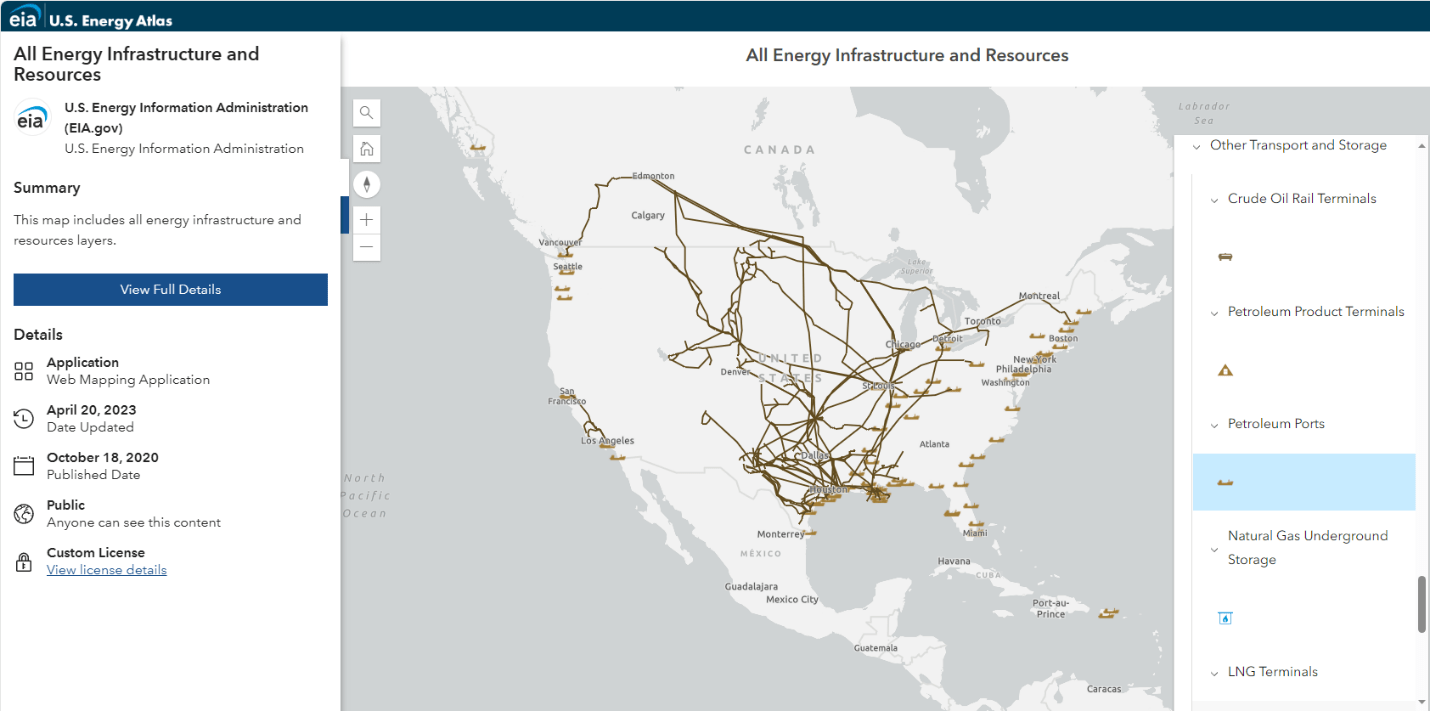

Above is a picture of PAA's energy infrastructure across its asset base. Below is a map of all the petroleum pipelines and export/import facilities in the lower 48 portion of the U.S. according to the Energy Information Agency ((EIA)) U.S. Energy Atlas . PAA's assets are at the heart of the American crude industry as they connect several basins to the most densely populated export/import location for American crude. Oil and gas aren't going away, and I feel investing in hard asset's is a theme that will become more popular as the years progress. PAA's infrastructure is next to impossible to be replicated by another company as the barriers to entry are immense for new companies to enter the space.

{kind=link}

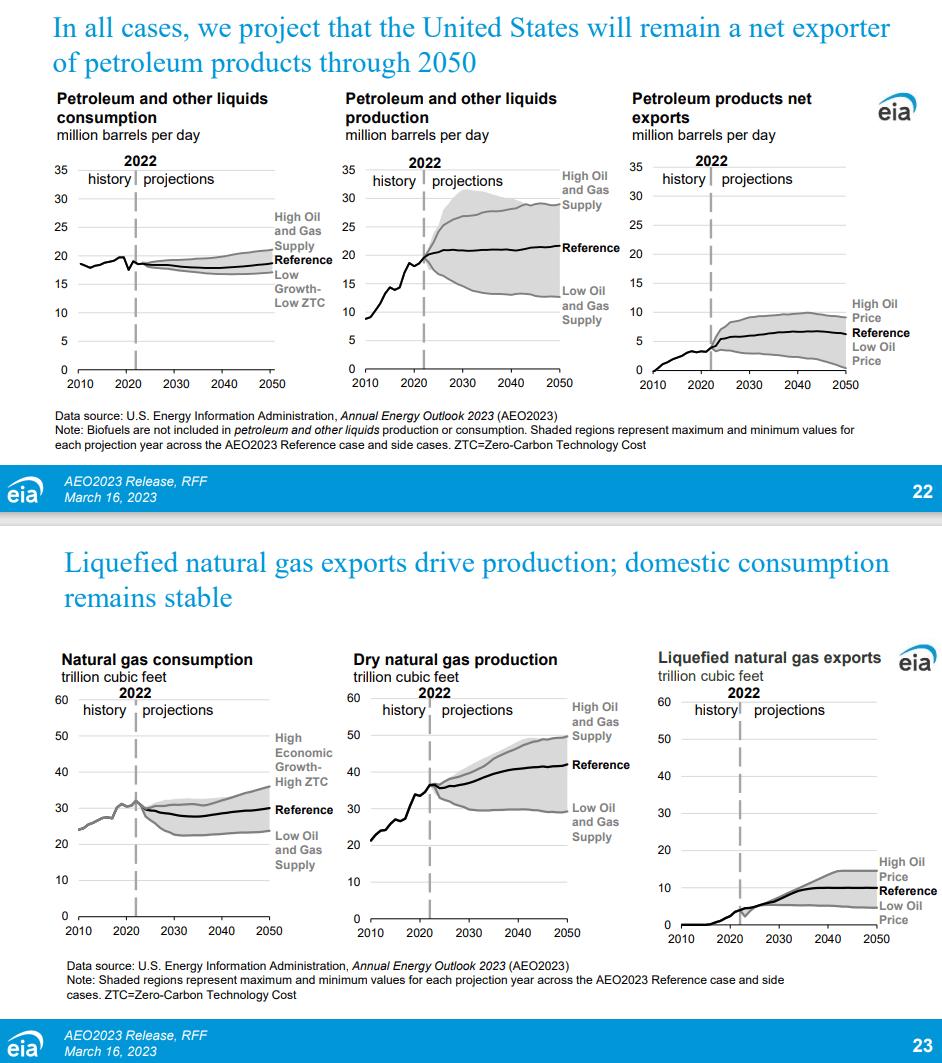

PAA could have significant growth running through their pipes as the 2023 Annual Energy Outlook from the EIA ( can be read here ) indicates that production levels in their reference cases for petroleum and other liquids, and natural gas will increase through 2050. The EIA also projects that the U.S. will remain a net exporter of oil and gas through 2050. My logic is simple as I follow what the government agencies responsible for energy are publishing. If the U.S. will grow its oil and gas production for the next 3 decades, then it will need excess transpiration capacity for these fuels. If the U.S. remains a net exporter, growing its oil and gas exports, then more fuel will have the Gulf Coast as a final destination. These are not my projections; they are the U.S. government projections, and I want to invest in companies that have infrastructure in these areas that can capitalize on the future growth in these areas. PAA is positioned to benefit from a growing domestic and international energy demand, and I feel unitholders can be rewarded with an appreciating unit price and growing distribution.

{kind=link}

PAA looks undervalued and it has a distribution that has been growing

PAA finished its 2019 fiscal year generating $33.67 billion in revenue, $2.5 billion in cash from operations, $1.32 billion in FCF, $10.22 billion in total debt, and having 728 million units outstanding. Based on the trailing twelve-month ((TTM)) numbers, PAA has grown its revenue by 52.16% ($17.56 billion) to $51.23 billion, its FCF by 76.64% ($1.01 billion) to $2.34 billion, reduced its total debt by -19.79% (-$1.92 billion) to $8.3 billion, and repurchased 29.6 million units, decreasing its shares outstanding by -4.07%. Today, you're able to purchase units below where they were prior to the improved balance sheet, financial growth, and lowered unit count.

{kind=link}

PAA has also strategically strengthened its company to capitalize on the future of American energy. PAA closed on its 43% acquisition of Diamondback Energy's ( FANG ) interest in OMOG JV LLC for approximately $225 million. This was funded through excess FCF, and further aligns PAA with FANG in the Midland Basin. PAA has updated its 2023 guidance and expects to come in the high end of its range for Adjusted EBITDA of $2.45 - $2.55 billion while decreasing its leverage to under 3.5x. PAA is expecting its FCF to come in around the $1.6 billion level in 2023, which will allow it to further reduce its debt load and should help provide future distribution increases.

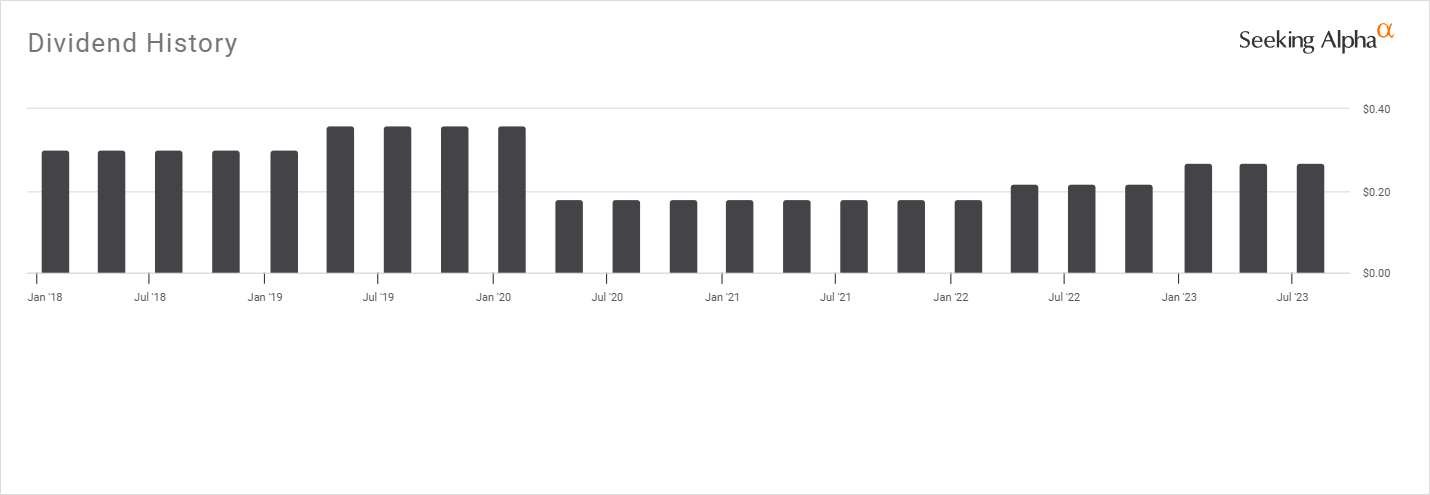

Like some other energy infrastructure companies, PAA reduced its distribution in 2020. Since then, PAA has improved its financial position, reduced debt, and provided 2 distribution increases. The quarterly distribution has grown from $0.18 to $0.27 in less than 2 years, and considering PAA is expected to retain $600 million of its $1.6 billion of FCF in 2023 after distributions, there is no reason for me to believe that increasing the distribution further isn't part of the gameplan. The current valuation looks discounted, provided the progress PAA has delivered.

{kind=link}

Now that earnings season has finished for Midstream Operators, PAA still looks undervalued compared to its peers based on the valuation metrics I look at

For Midstream Operators, I look at the enterprise value to Adjusted EBITDA, total debt to Adjusted EBITDA, the market cap to Adjusted EBITDA, market cap to distributable cash flow, and distribution yields. This helps me determine if there is an opportunity in one midstream units over another. PAA has always looked strong, and I am specifically looking at PAA based on these metrics.

I will compare PAA to the following companies:

- Energy Transfer ( ET )

- Enterprise Products Partners ( EPD )

- Magellan Midstream Partners ( MMP )

- MPLX LP ( MPLX )

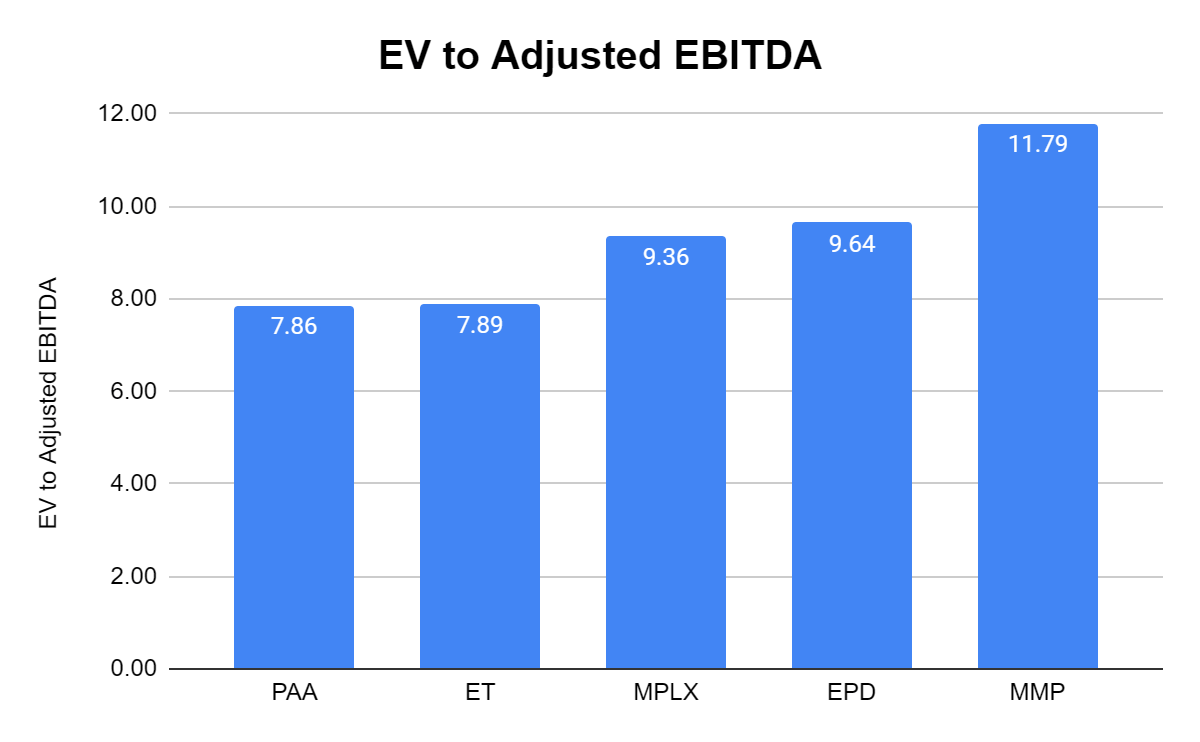

PAA trades at the lowest valuation on an enterprise value to Adjusted EBITDA methodology, slightly under ET. The peer group average for this metric is 9.31x, and PAA is trading well below this at 7.86x.

{kind=link}

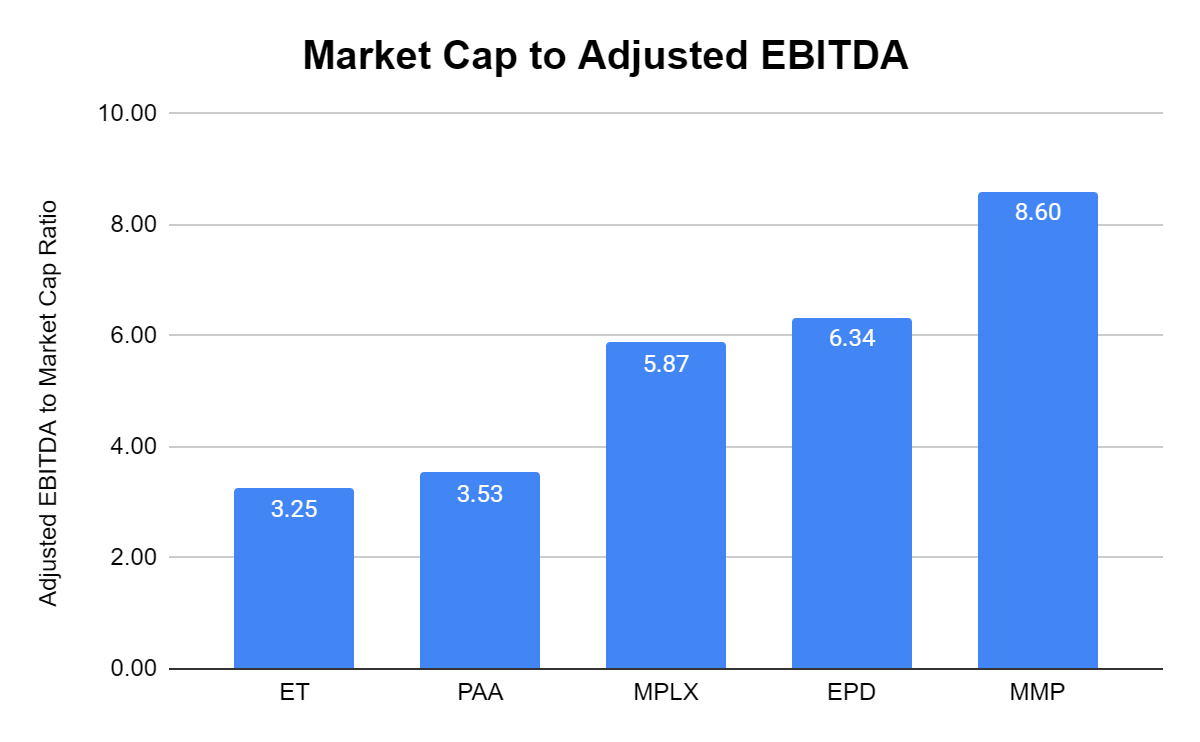

From a market cap to Adjusted EBITDA perspective, PAA also looks undervalued, trading at 3.53x compared to a 5.52x peer group average. PAA trades at a slightly higher multiple than ET but significantly below the rest of its peers.

{kind=link}

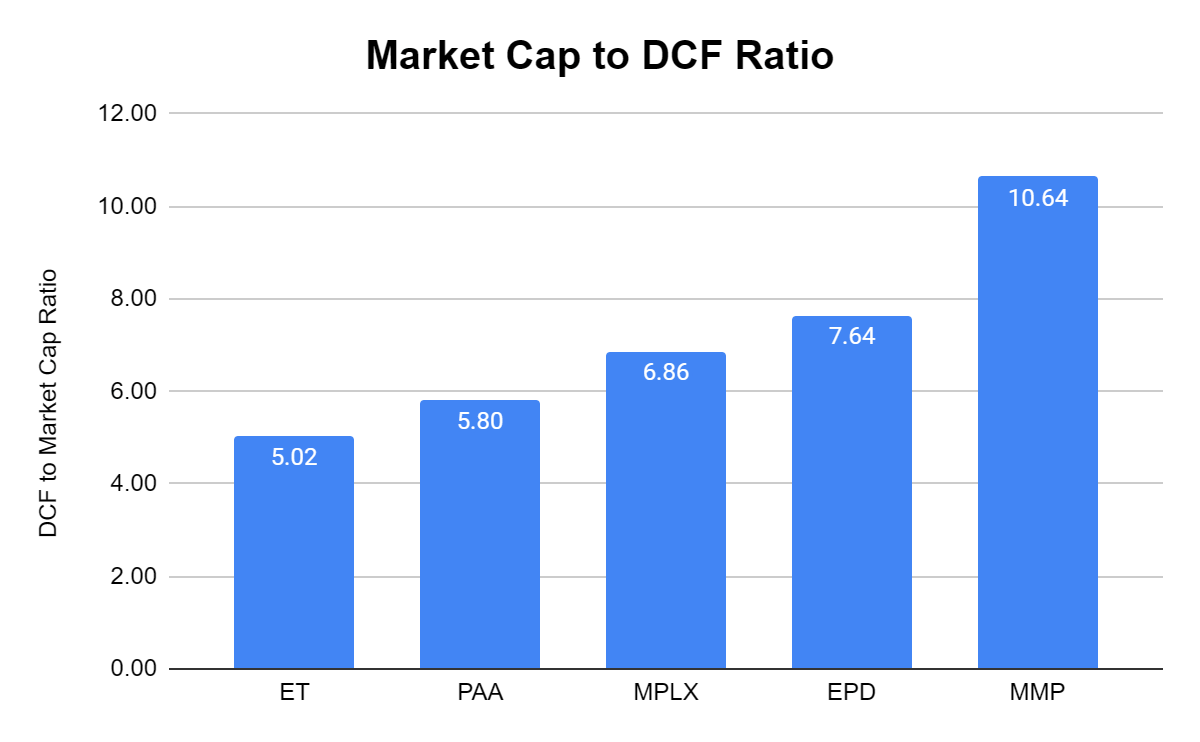

I want to pay the best multiple I can for DCF, and PAA is trading at 5.8x its DCF compared to the peer group average of 7.19x. ET is the only other company from the peer group that trades under a 6x multiple on its DCF.

{kind=link}

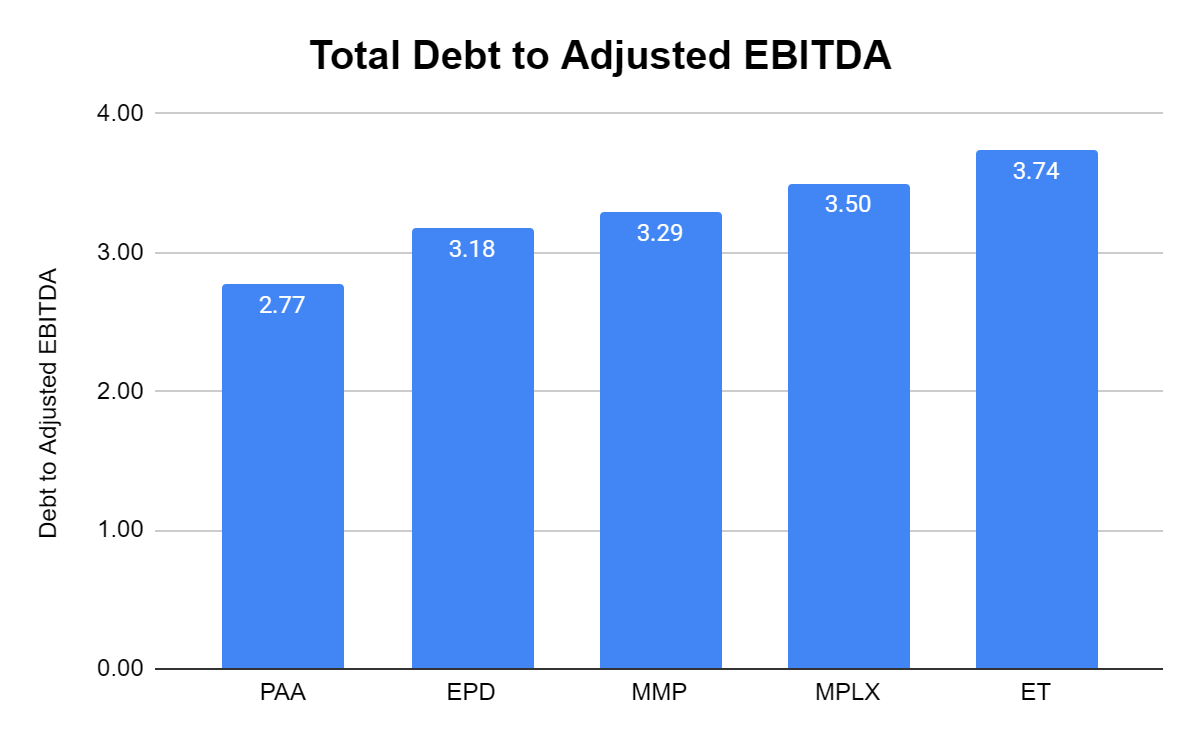

From a debt perspective, PAA trades at the lowest ratio as its total debt to Adjusted EBITDA is 2.77x. The peer group has an average of 3.3x, and PAA is the only peer that trades under 3x. From a leverage position, PAA looks attractive.

{kind=link}

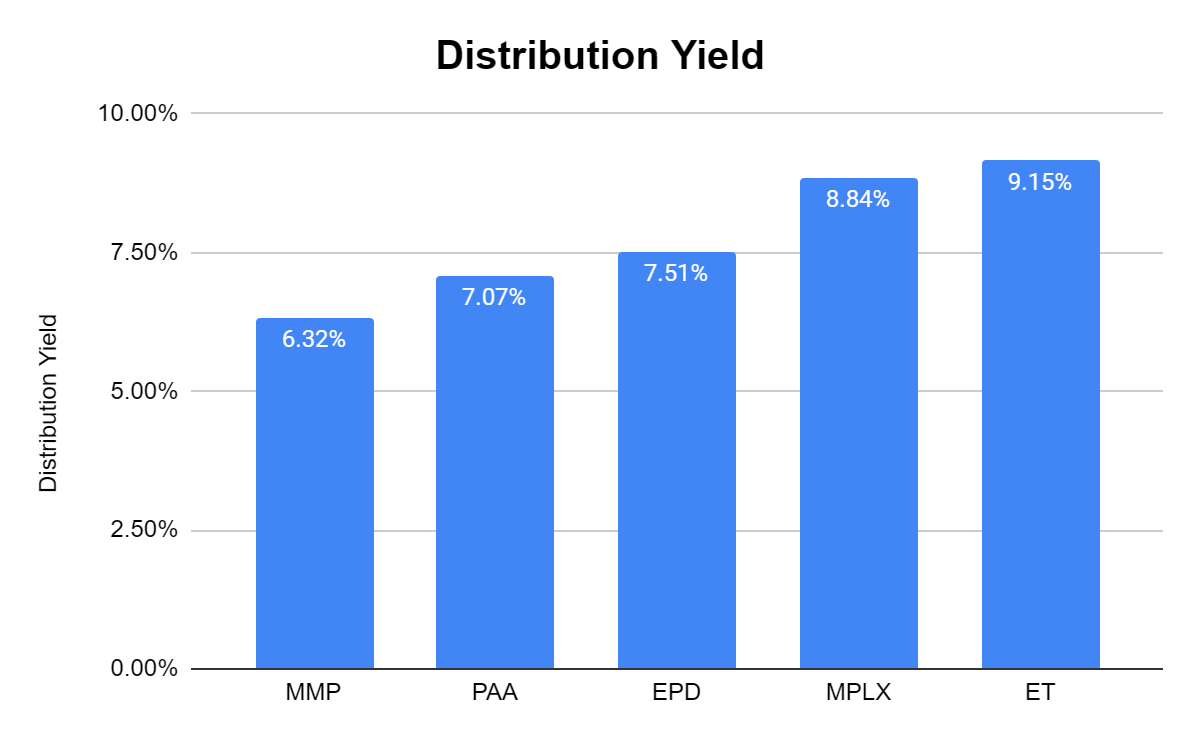

PAA has a distribution yield that exceeds 7%, but it's under the 7.78% peer group average. While I love a large yield, I am willing to invest in a smaller yield where the company has strong underlying fundamentals and ratios.

{kind=link}

Conclusion

PAA looks very interesting, and while I am not a unitholder, I am certainly considering adding PAA to my income-producing portfolio in the future. I think PAA is undervalued as its assets provide critical infrastructure to the oil and gas industry and are positioned to benefit from a growing demand for traditional energy. As the U.S. continues to increase production and exporting loads, I think PAA will see increased amounts of fuel running through its system and ultimately drive revenue and FCF higher. Based on the valuation, PAA could be an interesting acquisition target in an industry that has seen continuous consolidation through M&A activity. At a $23.5 billion enterprise value and $10.56 billion market cap, PAA looks interesting for an investment and as a target for an acquisition.

For further details see:

Plains All American Yields Over 7% And Looks Undervalued