PAGP - Plains GP Holdings: Strong Industry Positioning Isn't Enough Reason To Buy

2023-05-30 22:56:51 ET

Summary

- Plains GP Holdings and Plains All American have a strong position in the midstream market, particularly in the Permian Basin, but have a history of cutting dividends.

- The companies have made a key assumption that WTI crude will average $82.50/bbl in 2023, which may be too high if a recession occurs.

- Despite their problems, they are a critical player in the oil and gas industry, so it's unlikely that they'll have a cash flow issue.

Thesis

Plains GP Holdings (PAGP) and Plains All American (PAA) are situated strongly in the midstream market. I believe they have a great market share in one of the most desirable locations in the US - the Permian Basin. But they've also got some issues.

Most notably is that they're what I like to call a "serial dividend cutter."

You'll see that, although they have strong industry positioning, this dividend cutting combined with too high of a key assumption on WTI pricing leave me wanting more to issue a buy recommendation.

You see when I buy a stock for my dividend portfolio, I want companies that not only will pay a great dividend but will also potentially provide capital appreciation. I personally don't believe PAGP/PAA fit this criteria; I don't entirely believe that they will continue paying the distribution despite the ability to do so - based on their history.

Company Overview

Plains GP Holdings is a publicly traded entity that owns a non-economic controlling general partner interest in Plains All American and an indirect limited partner interest in PAA, one of the largest energy infrastructure and logistics companies in North America. The company owns and operates midstream energy infrastructure in the United States and Canada.

Plains is one of the largest midstream service providers in North America. Plains All American handles over 7 million barrels per day of crude oil and natural gas liquids through the company’s extensive network of assets.

The company owns pipeline transportation, terminaling, storage, and gathering assets in key crude and NGL producing basins (including the Permian Basin) and at major market hubs in the U.S. and Canada.

As of December 21,2021, Plains owns approximately 18,300 miles of active crude oil and NGL pipelines and gathering systems. The company also has around 140 million barrels of storage capacity.

Operations

The company operates in two segments – crude oil and natural gas liquids (NGLs). Plains All American operates in one of the most prolific shale plays in all of North America in the Permian Basin. The company engages in the transportation of crude oil and NGLs on pipelines, gathering systems, and trucks. The company features around 2100 trucks and trailers and over 6,000 crude oil and NGL railcars.

Permian Basin

{kind=link}

The Permian Basin is the most prolific shale play in North America and is where Plains All American has a large infrastructure position, allowing the company to share in capturing the Permian volume growth. Company leadership expects the Permian Basin to drive growth in the United States crude oil markets and forecasts for continued production growth, even in the face of a looming recession.

The company has key infrastructure that connects the Cushing, Oklahoma hub to the Permian Basin, and also connects the Permian to major hubs in Corpus Christi and Houston as well. This is a big deal because producers always want to get their products from the well site to the best market possible for their products for as cheap as possible.

And as it turns out, the best markets that every producer wants to be in are Cushing, Oklahoma, Houston, and Corpus Christi. So, producers are going to be naturally dependent on Plains All American to transport their products to market, making the company almost mission-critical in the Permian Basin.

Crude Oil

Plains All American transportation assets primarily generate revenue through a combination of tariffs, pipeline capacity agreements and other transportation fees. The company’s facilities assets generate revenue through a combination of month-to-month and multi-year agreements and arrangements which include storage, throughput and loading/unloading fees at Plains’ crude oil facilities.

The company boasts 74 million barrels of commercial crude oil storage capacity with 38 million barrels of active, above-ground tank capacity used to facilitate pipeline throughput and help maintain product quality segregation. Plains has 4 marine facilities, 7 crude oil rail terminals, 640 trucks, and 1275 trailers for crude oil transport.

NGL (Natural Gas Liquids)

The NGL segment for Plains includes operations involving natural gas processing and NGL fractionation, storage, transport, and terminaling utilizing the company’s highly integrated network of assets. The company’s NGL revenues are primarily derived from a combination of providing gathering, fractionation, storage, and/or terminaling services to third-party customers for a fee.

Plains All American owns 4 natural gas processing facilities and 9 fractionation plants. In addition to their plants and facilities, the company boasts 28 million barrels of NGL storage capacity and 1620 miles of active NGL transportation pipelines. When it comes to NGL transportation, Plains is one of the largest with 16 NGL rail terminals, 3900 NGL rail cars, and 220 trailers.

Revenue

PAGP, and by extension PAA, have done a good job here with their FCF. Take a look at their revenue, and notice that FCF increased in the period from 2016 to 2021 even though revenue remained stagnant. Well done by the company there. But what's unfortunate is what happened to the company's distribution amount during that timeframe, despite the fact the company now has the highest FCF/Share it's ever had.

Plains has been cutting their distributions for years now. Again, and again, and again. It's understandable to cut them in 2015 when the Great Oil Collapse hit, but when FCF once again exceeded pre-2015 levels then they should have focused on returning value to shareholders - but instead cut more.

Over the last few quarters they've risen, but I'm not ready to trust them just yet.

Potential Risks

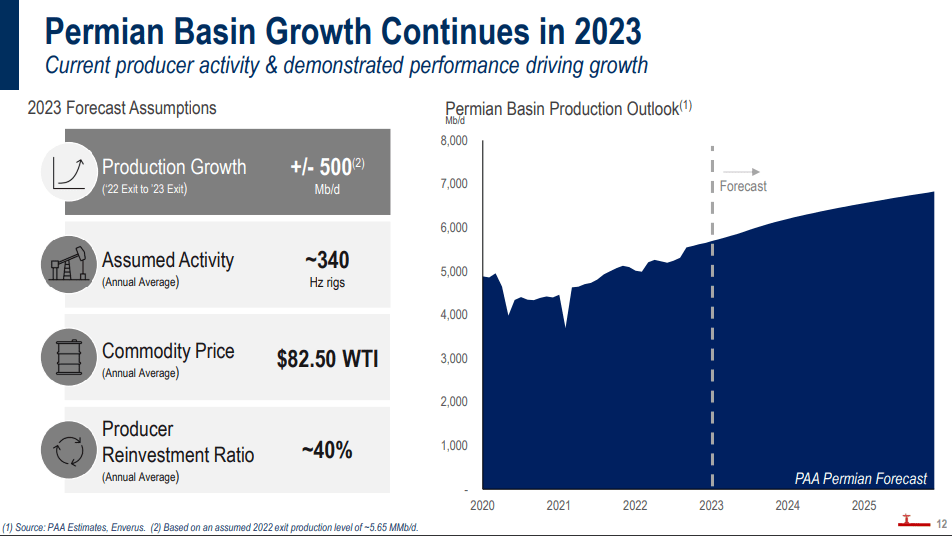

One of the key assumptions that PAGP and PAA have made for 2023 is that WTI crude will average $82.50/bbl. I certainly have my doubts about that, as well as many other analysts - IF we see a recession. In a recession the pricing floor will likely be closer to the mid-$60s (only kept that high due to the US government's refilling of the SPR), and will throw a lot of their projections into potential chaos.

Now if we don't see a recession then it's certainly possible, if not probable, to be around $85/bbl by the end of the year. But again, the average seems high since we're already half way through and pricing has barely been over $80 so far this year on CL futures. I have my doubts about this key assumption of theirs. See my article here for more discussion on oil pricing in a recession.

Now, all of that being said, PAGP is a midstream company and will be buffered somewhat from pricing concerns. They also have significant storage capacity which would be heavily sought after in a potential recessionary environment.

Overall though the key assumption being high just seems a bit like an excuse in the making for yet another dividend cut.

Conclusion

Plains All American is a staple of the oil and gas industry and the company is well known in the industry to be a critical cog in the oil & gas wheel. They are one of the biggest midstream companies in North America. The company’s infrastructure is key to getting crude oil & NGL’s from the largest and most prolific basins in North America to the major market hubs for refining and marketing.

Company leadership appears dedicated to efficient operations as can be seen with the Capline Pipeline reversal, bringing new capacities, and allowing producers across Canada, with access to infrastructure, to bring Canadian crude oil and NGLs to new and major markets.

It’s no secret that there is a looming recession hovering over the United States and investors are weary of what this will do to markets and stocks. Investors in Plains All American can breathe a sigh of relief for now, as the company is as well-protected as can be as a midstream services provider with assets and infrastructure that are critical to both the upstream and downstream market.

The demand for the company’s services isn’t going anywhere, and one could even argue that the company could see a spike in storage revenues in the event of commodity price drops. The critical infrastructure that the company owns and operates makes the company almost “too big to fail”.

Investors should certainly feel safe about the future of the company. In the event that commodity prices drop, and drilling activity goes down, the company shouldn’t see a significant change to its operations as both upstream and downstream companies will still need to transport and/or store their products - and the company’s revenue is fee-based, not dependent on commodity pricing.

Plus, the Permian Basin producers should continue pumping existing wells regardless of a recession as this region has some of the lowest breakeven pricing in the country for both new and existing wells.

So for the existing investor who has received numerous distributions already and is well in the green on PAGP (thus you bought it after COVID) I'd say PAGP could be a hold. I think it can continue to pay the distribution, but the question is "will it?" It's a serial distribution cutter, so that's up in the air.

For anyone else looking to get into energy for the income, I'd just say steer clear because there are better alternatives out there - I just wrote a strong buy article for EPD so check that out.

Important

Distributions

Please note that PAA is an MLP and issues a K-1. Ticker PAGP, however, issues a 1099 form instead of a K-1.

The tax situation for LP K-1 distributions can be complex and will require your research and possibly consulting a tax professional. They are generally not taxable when received, instead, they reduce the partner's tax basis in the partnership. Once the partner's basis hits zero, additional distributions are considered a gain and subject to capital gains tax. Also, partners must pay taxes on their share of the partnership's income, even if they don't receive an actual distribution.

The individual partner's share of the partnership's income could include ordinary income, capital gains, and other types of income, each with its own tax rate. LP partners also receive a Schedule K-1 form, which details their share of the partnership's taxable income and deductions. The unique tax situation can create a confusing scenario upon sale of the security as well.

Do your due diligence and research carefully to decide which ticker, PAA or PAGP, is right for you.

For further details see:

Plains GP Holdings: Strong Industry Positioning Isn't Enough Reason To Buy