PLNHF - Planet 13: Rescheduling Isn't Enough

2023-05-19 13:08:23 ET

Summary

- Planet 13 has a unique and attractive business model.

- Overall, revenue has been declining since the highs of $32.8M and $33M in late 2021.

- ROIC is currently at -2.94%, ROCE is -2.11%, and ROE is -3.38%.

- While considering their declining revenue and negative returns, their forward Price/Sales of 1.32x, a forward EV/Sales of 1.10x, and forward EV/EBITDA of 11.13x appear to show the company as overvalued.

- I currently rate Planet 13 as a Hold.

Thesis

The cannabis industry is prone to periodic euphoria-driven rallies. With most Canadian cannabis companies experiencing negative gross margins, and most of their United States based counterparts currently suffering from negative operating margins, most of the industry is currently trading in gutter. I believe now, while valuations are low, is a good time to find good companies to buy into them for the long term.

After looking at the financials of Planet 13 ( PLNHF ), the removal of the brutal 280e tax obligation the sector has been suffering from wouldn't be enough to allow the company to reach profitability. Until they improve their operating margins, I am forced to avoid buying. I currently rate Planet 13 as a Hold.

Company Background

Planet 13 opened the world's largest cannabis dispensary in Las Vegas on Nov 1, 2018. Their store offers a truly unique experience, they also sell beer and pizza; customers are encouraged to stay for a while and treat the store as an entertainment experience. In July 2021, the company opened Planet 13 Orange County in Santa Ana, California.

The most recent earnings call indicated the company is looking forward to completing the construction of a third dispensary; this one in Illinois. They are also looking to expand their cultivation capabilities in Florida and are searching for an accretive M&A target.

PLNHF Forward Guidance (Q1 2023 Earnings Call Transcript)

{kind=link}

Financials

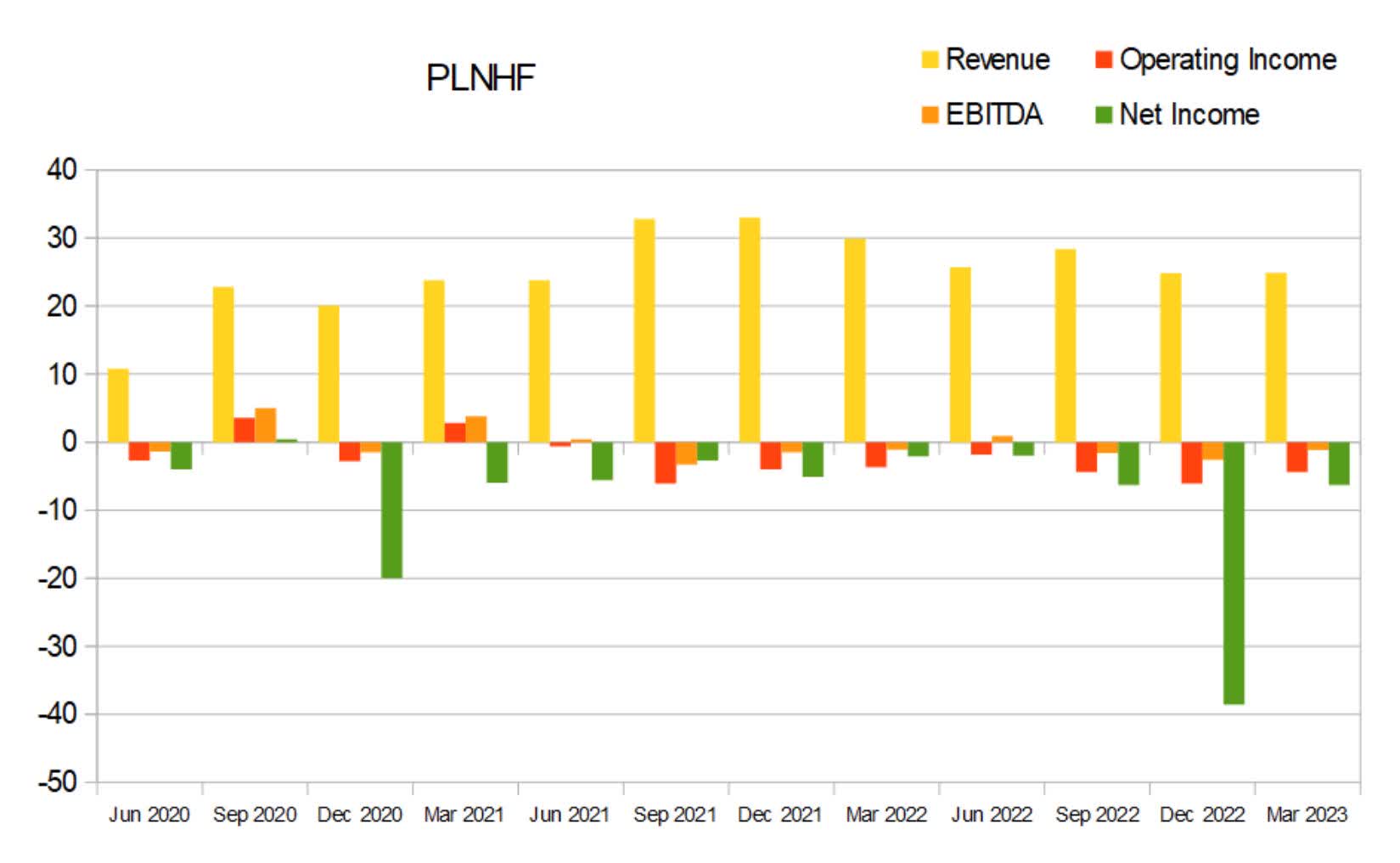

Since mid-2020, Revenue has remained at or above $20.1M. This most recent quarter, it was at $24.9M. Overall, revenue has been declining since the highs of $32.8M and $33M in late 2021.

PLNHF Quarterly Revenue (By Author)

{kind=link}

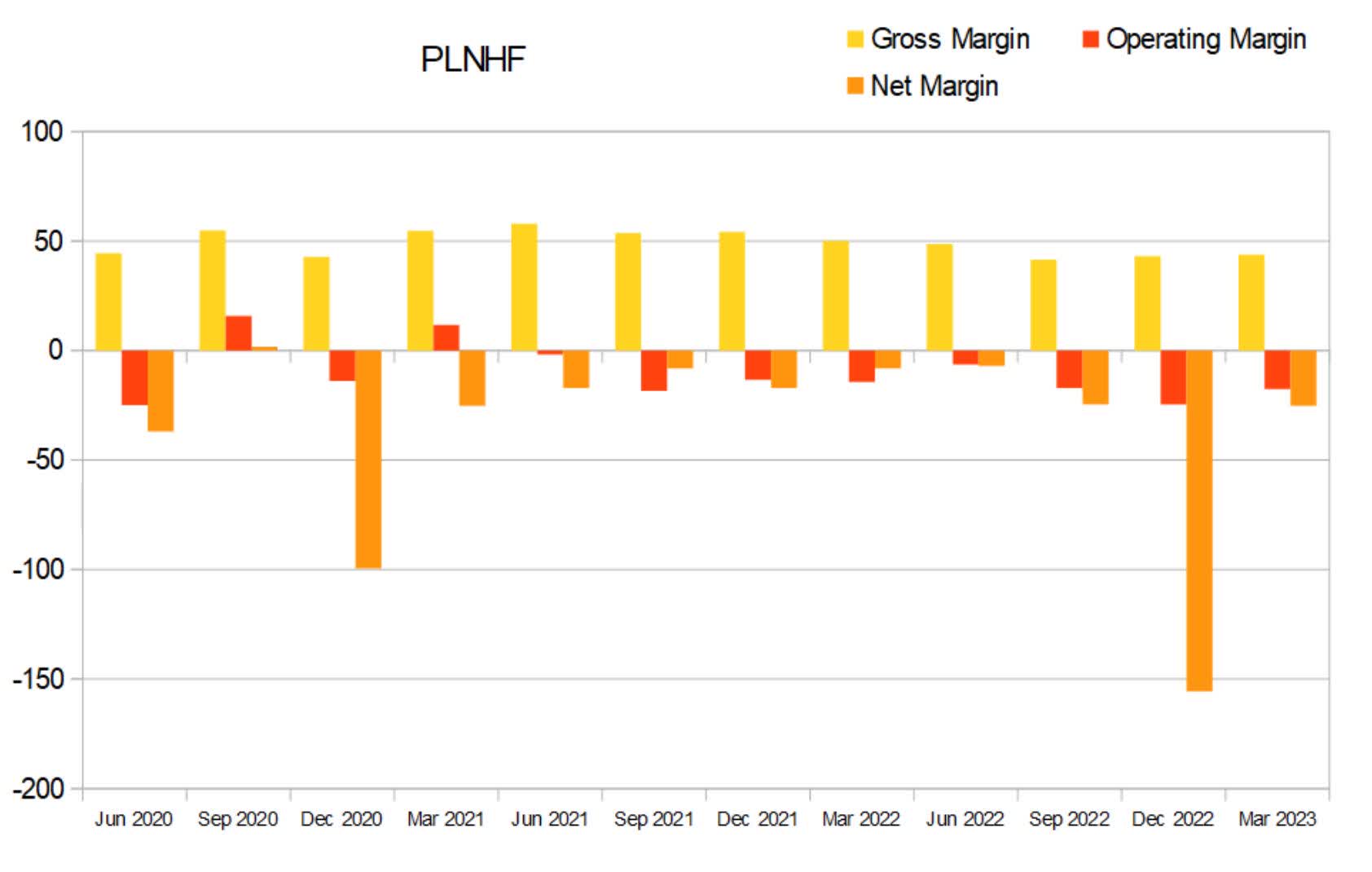

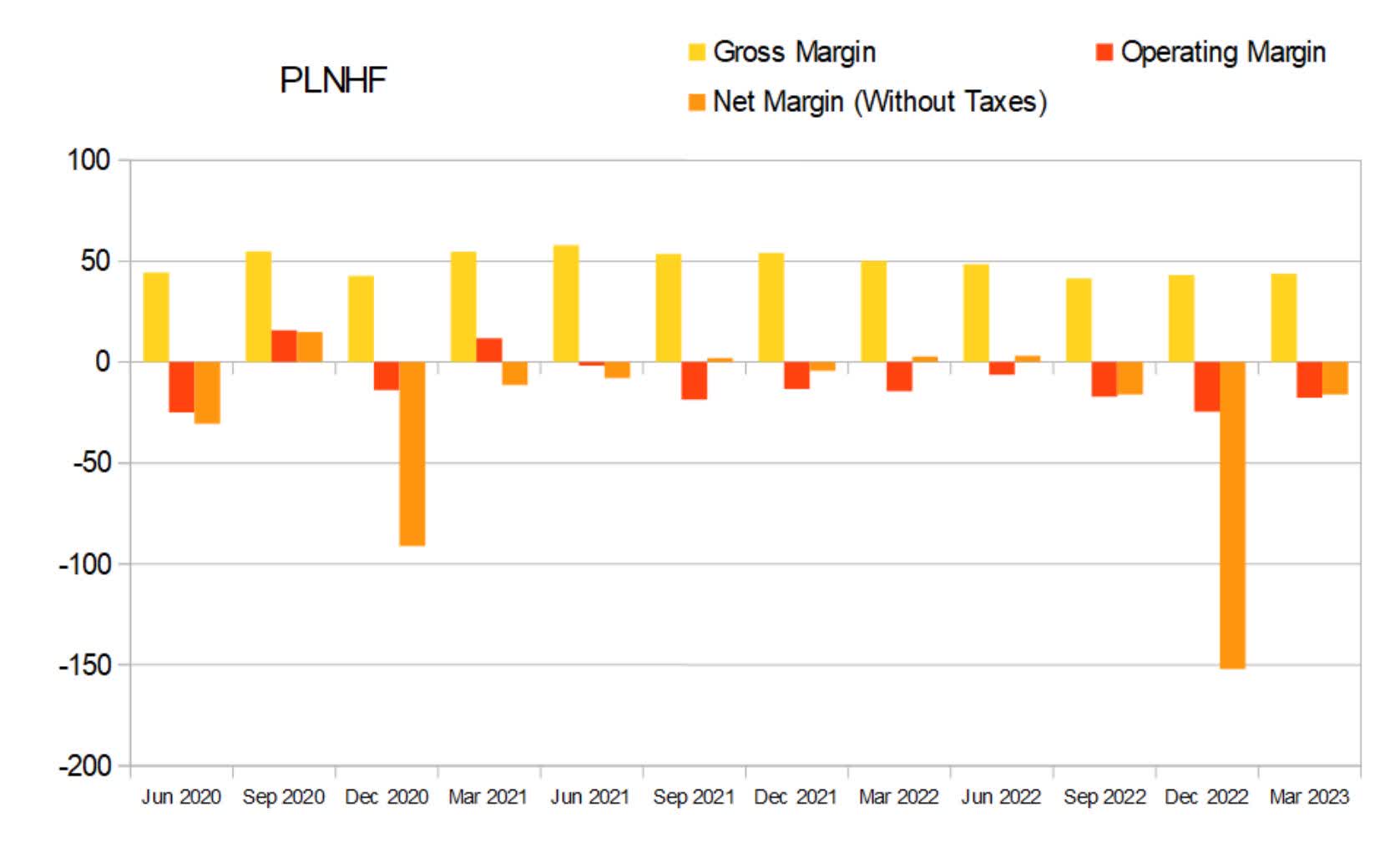

Gross margins are consistently high, the ranges shown vary between 43.1% and 57.9%. This most recent quarter, gross margins were at 43.77%. Operating and net margins are both consistently negative. Currently, operating margins are at -17.67% and net margins are at -25.3%.

PLNHF Quarterly Margins (By Author)

{kind=link}

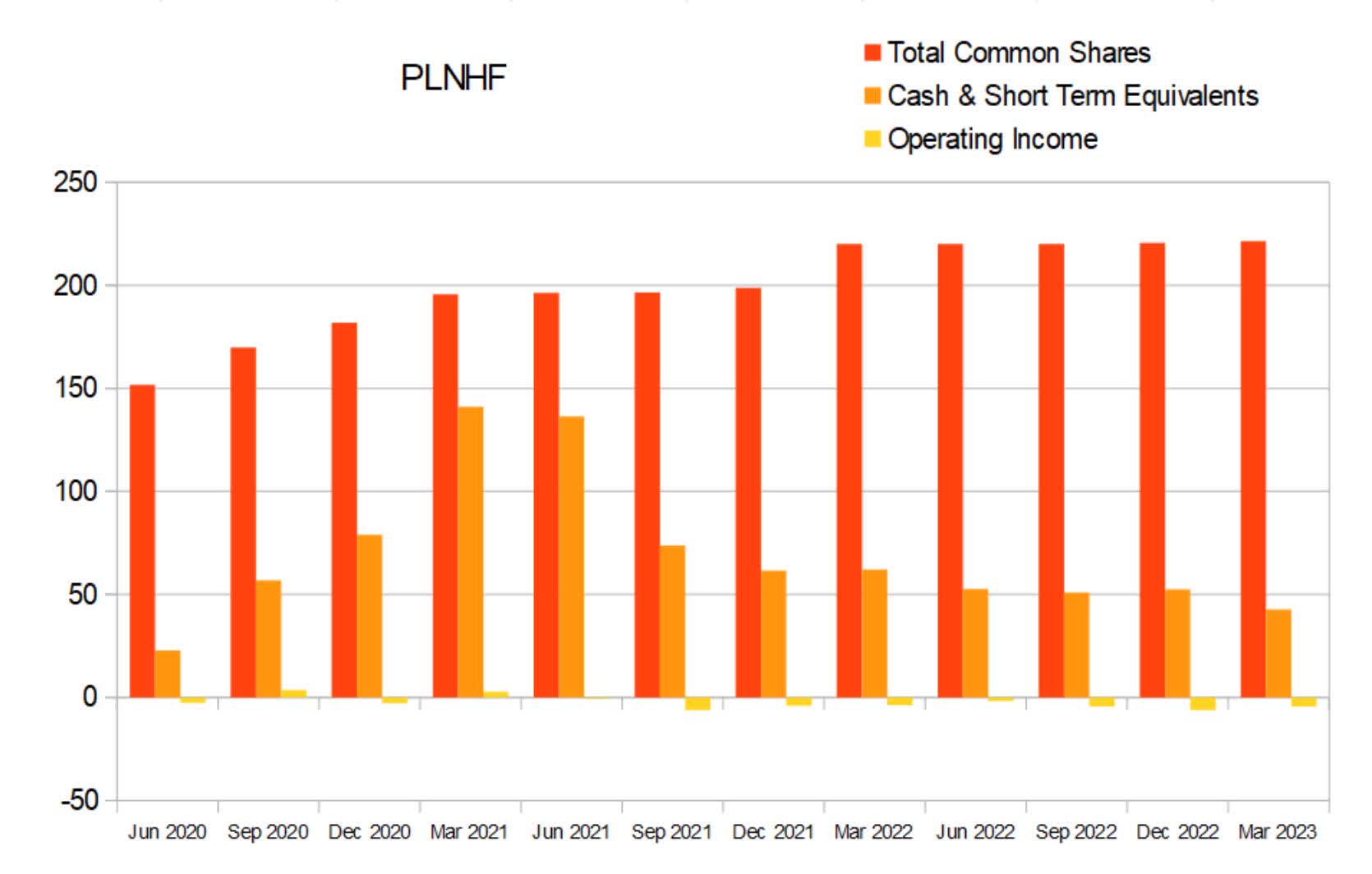

The share count rose by an additional million this quarter. The share count has been relatively flat since the beginning of 2022. Investors can expect additional dilution as the company is already looking for an appealing acquisition target in Florida. This alone should not be a deterrent.

When looking over companies that are still this early in their business life cycle, we want to see them translate their dilution into income. So far, Planet 13 has been unable to consistently achieve positive operating income. With $42.7M in Cash and Equivalents, its most recent quarterly operating income of -$4.4M leaves them with a little over two years of cash left to support operations. Their rate of cash burn will likely change significantly after they open their Illinois store and find their desired M&A target in Florida. Other than the planned Florida acquisition, the risk of near-term dilution seems low.

PLNHF Quarterly Share Count vs. Cash vs. Operating Income (By Author)

{kind=link}

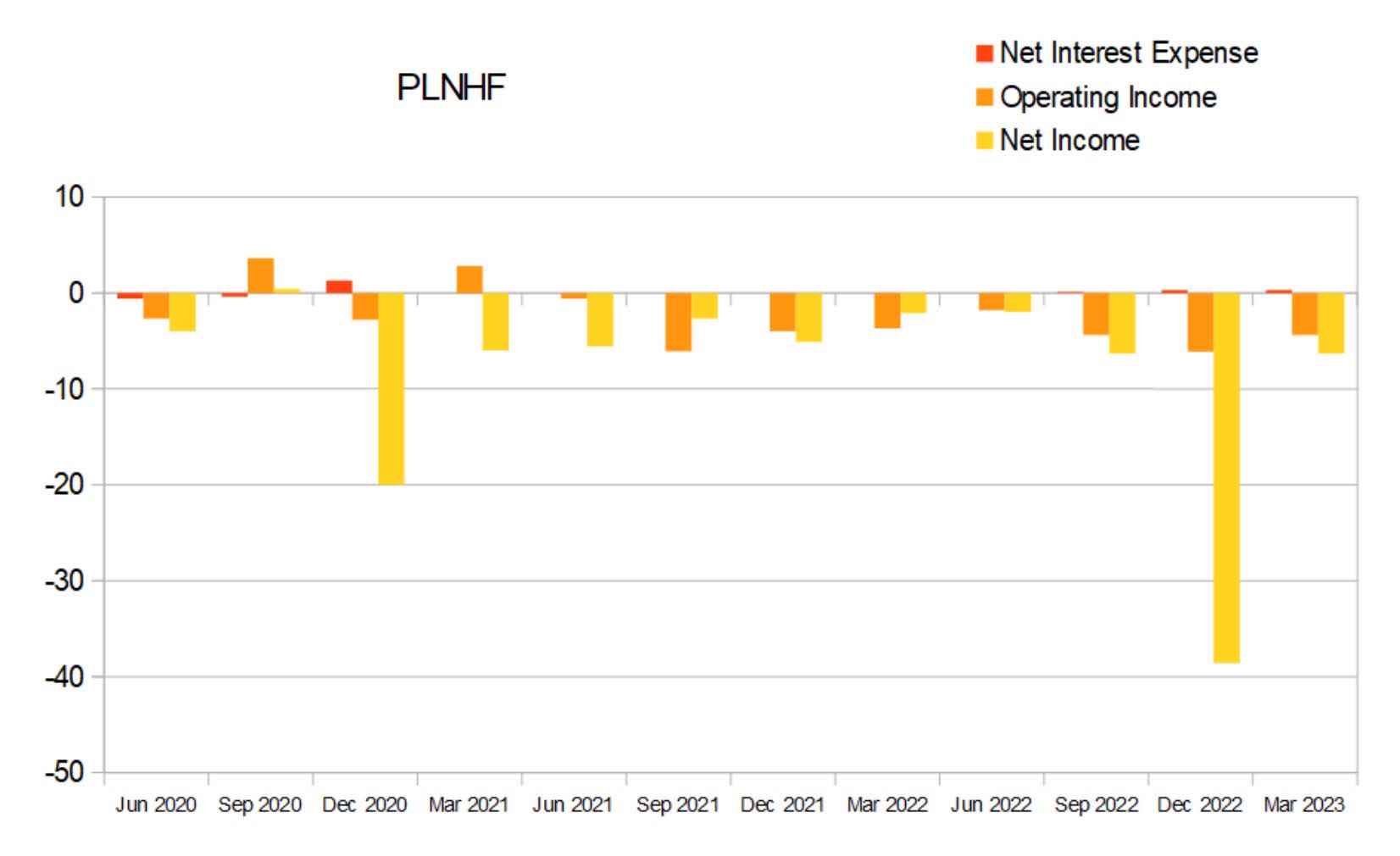

Fortunately, Planet 13 carries very low debt.

PLNHF Quarterly Net Interest Expense (By Author)

{kind=link}

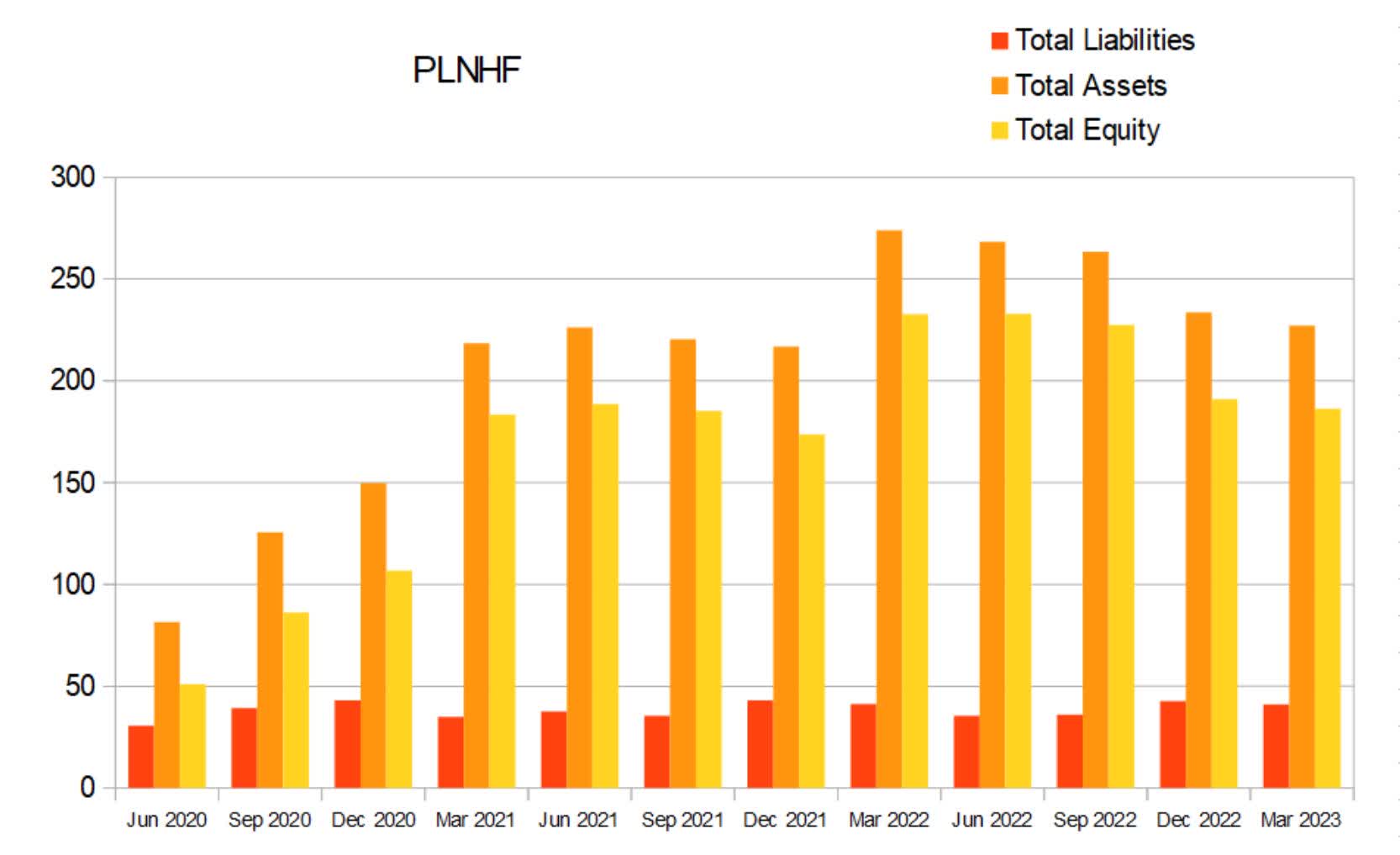

Total Equity was rising until 2022. The good news here is that assets have been rising while liabilities have remained fairly stable. As this trend plays out, equity should continue to rise.

PLNHF Quarterly Total Equity (By Author)

{kind=link}

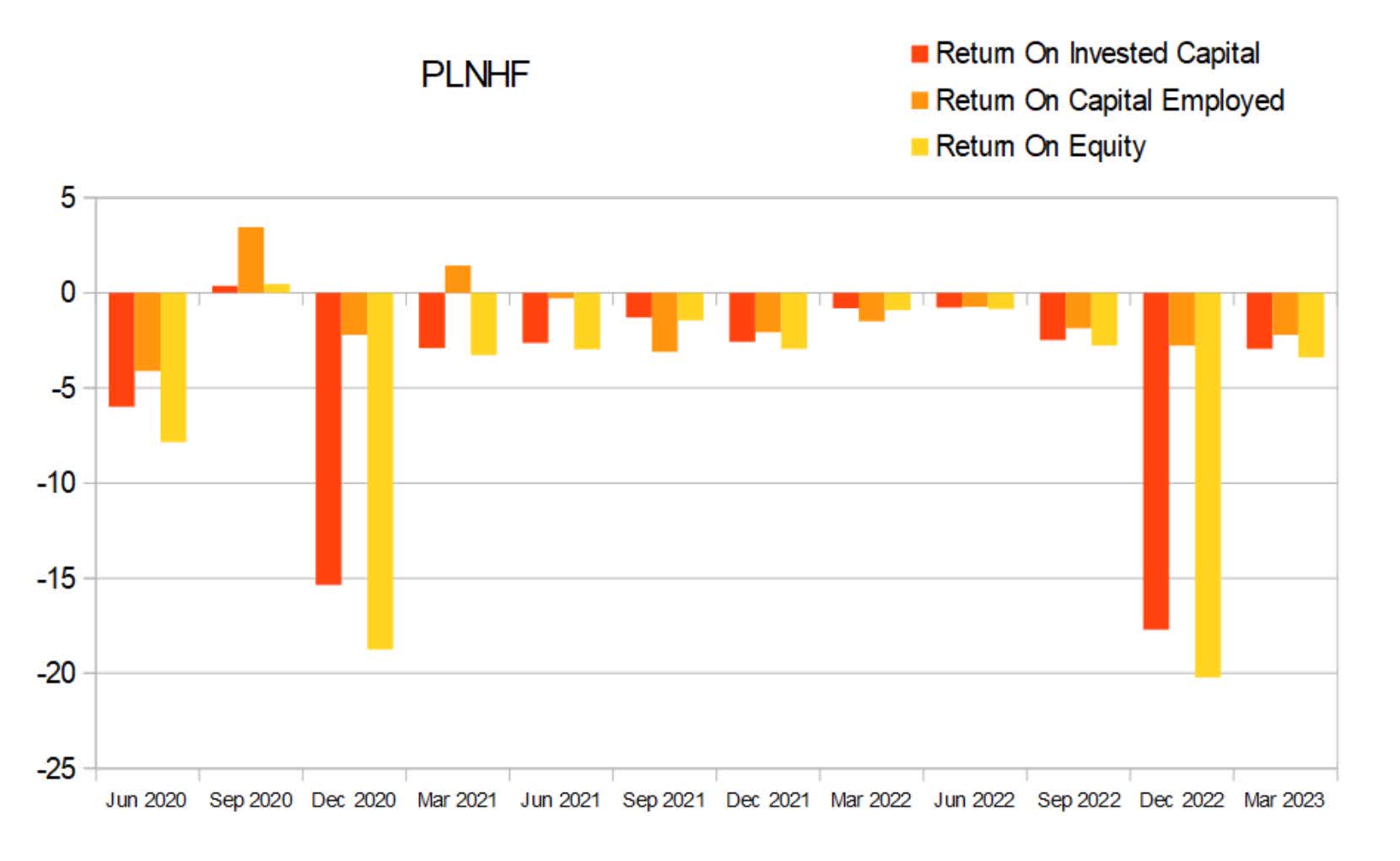

With the exception of a couple of outliers, returns are negative. When looking at companies on a quarterly basis, I want to see the average of these three numbers at or above 2.4% before I will consider buying. ROIC is currently at -2.94%, ROCE is -2.11%, and ROE is -3.38%.

PLNHF Quarterly Returns (By Author)

{kind=link}

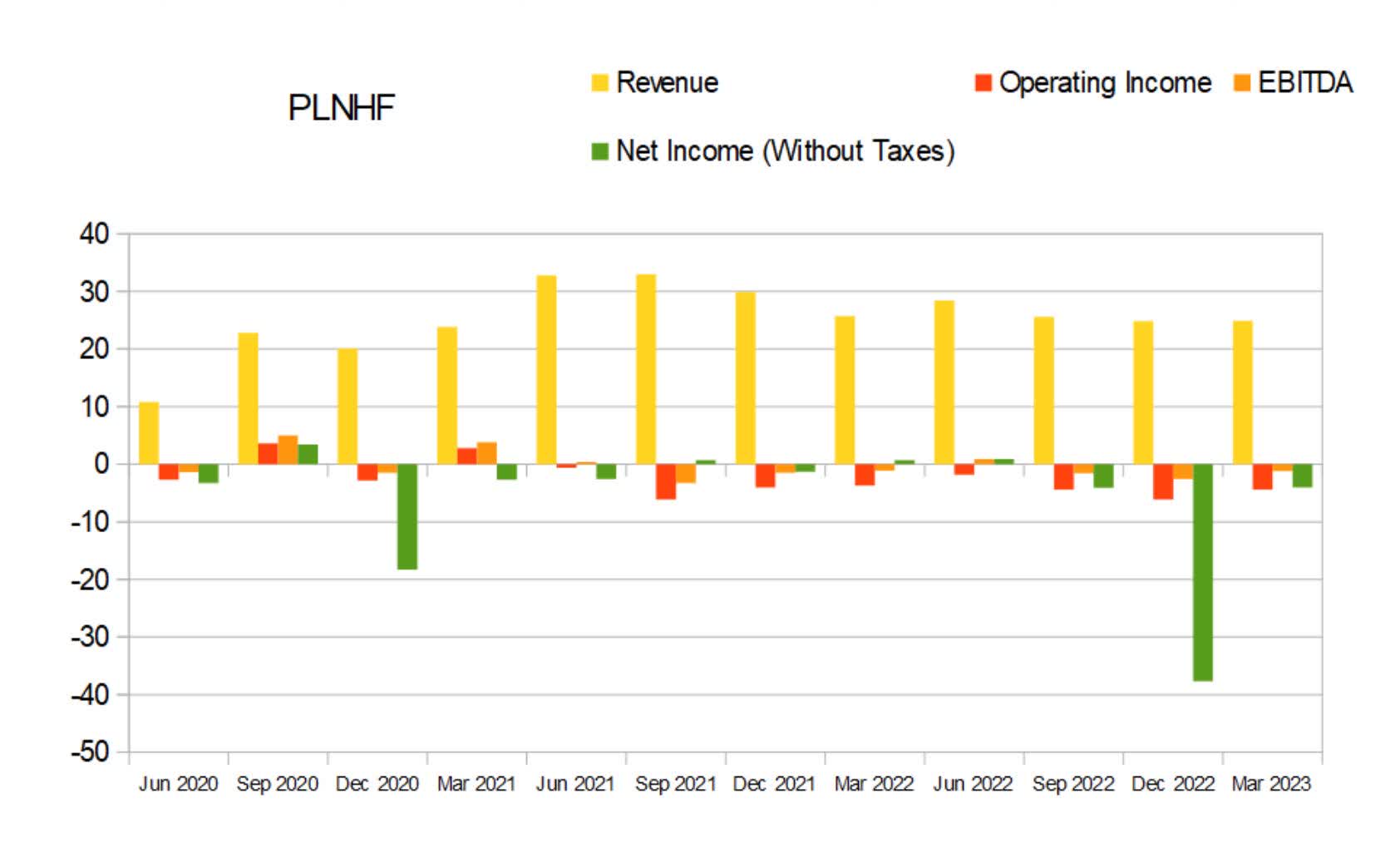

The narrative with cannabis companies in the United States is that they are not profitable because of the 280e tax obligation. It forces cannabis companies to pay taxes based on their gross income before deductions instead of after deductions.

The two charts below show what the company would look like if they didn't have to pay income taxes. We can see that even without taxes, Planet 13 wouldn't be profitable. Without taxes, net revenue for this most recent quarter would have been -$4M.

PLNHF Quarterly Revenue Without Taxes (By Author)

{kind=link}

Their net margins without taxes would be -16.06%.

PLNHF Quarterly Margins Without Taxes (By Author)

{kind=link}

Valuation

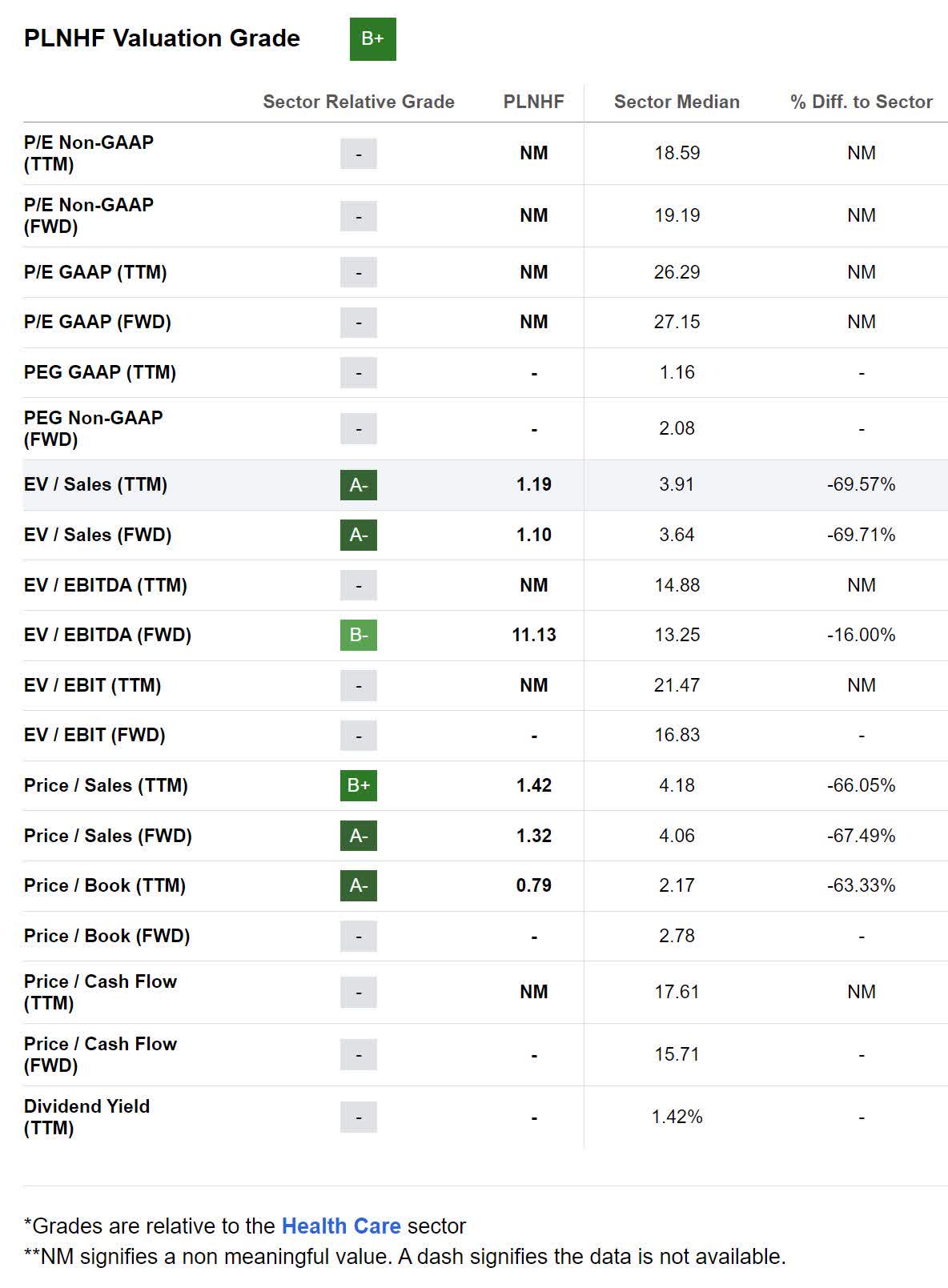

As of May 17th, 2023, Planet 13 had a market capitalization of $138.05M and traded for $0.61 per share. With a forward Price/Sales of 1.32x, a forward EV/Sales of 1.10x, and a forward EV/EBITDA of 11.13x, I view the company as overvalued. If the company was net income positive, it would appear close to fair value. Note, the sector comparisons below are with the Health Care sector, and not an accurate comparison of its metrics vs. its peers.

PLNHF Valuation (Seeking Alpha)

{kind=link}

Risks

By concentrating their operations into fewer, larger stores, the company takes on additional risk from random low-frequency events (plane crashes, structure fires, earthquakes, et cetera).

Although unlikely, if the inquiry into rescheduling results in cannabis being removed from the list of controlled substances, and it is given the same treatment we do alcohol and tobacco, then ultra-cheap Canadian cannabis is going to flood the market and most of the U.S. based producers will be driven into bankruptcy . As far as I know, the only state that already has protections in place to prevent this, is preparing to remove them .

Even more unlikely, the DHHS may decide to keep cannabis as a schedule-1 substance. If this happens, the brutal tax burden the cannabis industry is suffering under will continue. Sentiment in an already sour sector will continue dropping; valuations will likely follow.

Catalysts

The cannabis industry in the United States is expected to have a CAGR of 14.2% until 2030. This will provide sustained tailwinds for the entire industry, including Planet 13.

When rescheduling arrives , the entire sector should experience a euphoria-driven rally. It will provide Planet 13 with an opportunity to raise cash with offerings while the shares are overvalued. Depending on how efficiently the company deploys this capital, it could provide a significant boon for their long-term competitiveness.

Conclusions

Although I like their unique business model, I do not like their present financial situation. While rescheduling will relieve some of their tax burden, it won't be enough to make them net profitable. Most importantly, it won't do anything to help their negative operating income and operating margins. It's hard to believe they will fare well against their competition over the long term without first finding positive operating income. As neat as the business model is, it's not currently profitable enough for me to be willing to invest into it.

For further details see:

Planet 13: Rescheduling Isn't Enough