PLNT - Planet Fitness: $10 Membership Pricing Is A Moat

2023-07-27 11:13:39 ET

Summary

- At scale, Planet Fitness has several competitive moats: low pricing, recognizable brand awareness, and size advantages.

- Virtuous cycle is held together by attracting the best investors and operators and successfully converting younger generation, Gen Z members.

- Store unit growth and gym utilization trends suggest accelerating growth.

Editor's note: Seeking Alpha is proud to welcome Alan G Li as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

This is my first article on Seeking Alpha, and I'm excited to be here. By way of introduction, I spent the first few years out of college working in tech investment banking at Goldman and tech private equity at Siris Capital before attending business school at Harvard. My path after business school has been less structured. I joined a nicotine alternative startup, sold a wellness mobile app, and opened a self-portrait photo studio.

Both sets of experiences have led me to realize that I am an operator first, investor second. As an operator, I have a profound admiration for management teams that can execute consistently day to day, while threading the needle between profitability and growth. As an investor, I take a wider view, trying to identify companies that have built effective moats. In terms of sectors, I prefer technology and consumer, but operate as a generalist. And to support my investment theses, I often rely on public and proprietary data, which I believe can be hugely valuable.

Today, I'm focusing on a company that has revolutionized the fitness industry, a highly competitive and commoditized space. And it's done this not through technology but rather focus and operational efficiency. I am talking about Planet Fitness (PLNT) , which I am bullish on over the next 3-5 years. My investment thesis is based on public filings, earnings transcripts, and data collected at Blink Data. Let's dive in.

How It All Started…

Like many founding stories, Planet Fitness' beginnings aren't exactly clear. Brothers Michael and Marc Grondahl are listed as founders, but it was actually Rick Berks who opened the first Planet Fitness in 1993 down in Sunshine, FL.

What is clear though is that gyms at the time were in fierce competition for members, even back then. In the early '90s, gyms mostly catered to bodybuilders, powerlifters, and serious athletes, and there weren't enough of these guys to go around.

Planet Fitness decided that instead of targeting the small minority of " lunks " (gym meatheads), they would target "everyday people" (the remaining 85 percent of the population that didn't have a gym membership).

Their first thought was to slash prices to $10 a month - which helped, up to a point. It may be surprising today, but back then, gyms were intimidating. Imagine a room full of stringer tank tops, not Lululemons. It was tough for ordinary people to find themselves, much less workout, at a gym. With this knowledge, Planet Fitness set out to attract the mass market and pioneered the "judgment free" zone.

Planet Fitness Website

This philosophy was a way to ease first-time gym goers into their fitness journeys. To create the judgment free zone, Planet Fitness introduced "lunk alarms," a blaring blue siren that would shriek any time a "lunk" dropped their weights, grunted, or judged someone else. Planet Fitness also removed weights above 75 pounds, and began providing free pizzas on Mondays, bagels on Tuesdays, and Tootsie rolls at the counter. These kooky offerings delighted many first-time gym goers, who comprised a sizable and largely untapped market.

At the same time, Planet Fitness cut all group classes, juice bars, and childcare facilities. The strategy was to laser in on one overarching goal - to make fitness accessible to all. Over time, Planet Fitness' bare bones facilities became its biggest sell, allowing it to offer a consistent experience at an unbeatable price.

"One thing we wanted to have with Planet Fitness is what I call the Big Mac, so it tastes the same wherever you go," Rondeau added.

With this formula, memberships started flying.

Rick Berks grew Planet Fitness to three locations before selling the franchise rights to Michael and Marc Grondahl in 2002. Chris Rondeau (the Grondahl's front desk associate) became COO in 2003 and CEO in 2013. He spent the next 30 years helping PLNT reach their 100th club in 2006, 1,000th club in 2015, and 2,000th club in 2019. As of the most recent quarterly earnings (Q1 2023), PLNT has 2,446 stores, and Chris is still at the helm as CEO.

A large part of Planet Fitness' success today is owed to the San Francisco-based private equity firm TSG Consumer Partners. TSG first acquired a majority stake in PLNT in 2013. They subsequently IPO'ed the company in 2015 and fully exited their stake in 2017. Throughout this period, TSG helped PLNT compound top-line growth ~19% each year, improved gross profit margins from 42% to 56%, and increased EBITDA margins from 31% to 42%. In other words, they turned Planet Fitness into a growing cash machine.

Created by author using public filings 10-K and S-1

Now, let's take a look at how Planet Fitness has performed over the last few years.

Moving Beyond COVID...

Planet Fitness emerged from the pandemic, the undisputed leader in High-Value Low-price ('HVLP') gyms. While competitors like 24-Hour Fitness and Gold's Gym declared bankruptcy in 2020, PLNT didn't close a single location.

This is a testament to the strength of Planet Fitness' business model and franchisees (more on the latter, below).

At a high level, Planet Fitness earns revenue in three ways: (1) franchises; (2) corporate owned stores; and (3) equipment.

Created by author using public filings 10-k

-

Franchises (~35% of total revenue and ~66% EBITDA margins): Planet Fitness' franchise revenue comes from Royalty Revenue, National Advertising Fund (NAF) fees, and other franchise fees.

-

Corporate-Owned Stores (~40% of total revenue and 37% EBITDA margins): Planet Fitness currently owns 235 (~10%) of existing Planet Fitness stores. It got a boost in 2022, after acquiring its largest franchisee Sunshine Fitness, which operated 114 locations and was previously owned by TSG.

-

Equipment (~25% of total revenue and 26% EBITDA margins): Planet Fitness sells equipment to their franchisees. Cardio equipment is replaced every five years, and non-cardio equipment is replaced every seven years. Equipment sales account for ~20% of total revenue.

So how does PLNT stack up with public comparables today? Below, I compare Planet Fitness with fitness (LTH, PTON, and LULU) and franchise (DPZ, LOCO, QSR, FRG, MCD, and WING) comps.

{kind=link}

PLNT continues to have best-in-class profitability metrics, second only to McDonald's in my chosen list of peers. PLNT's gross profit margin of 55% is 16 points higher than comparable averages of 39%. PLNT's EBITDA Margin of 41% is 23 points higher than comparable averages of 18%.

This is good, but I think PLNT can do even better.

Pulling Levers

I believe Planet Fitness has some key levers to increase overall revenue and margins, which the market has undervalued.

New Stores - When it released its S-1 in 2015, PLNT defined its point of saturation in the U.S. to be ~4,000 gyms. Now, with 25% of gyms having shut their doors during the pandemic, this forecast is likely a floor. I would not be surprised to see management project higher saturation going forward. In the short-term, I believe PLNT is also opening new stores faster than their guidance:

App.blinkdata.io as of July 26, 2023

{kind=link}

In Q1 2023, management reduced its guidance for 2023 franchise openings from 200 to 175 locations. As of July 26, 2023, Planet Fitness is now at 2,534 stores - up by 124 from 2,410 locations on Dec 31, 2022 ( BlinkData dashboard ). Thus, PLNT is ahead of their guidance, and is on track to deliver over 200 new locations by the end of the year. This could be an under-promise and over-deliver tactic which management teams have been known to do.

PLNT is also poised to accelerate international growth. It's HVLP model will resonate well with lower GDP countries (see its successful expansion into Canada, Mexico, and Australia). A dedicated international team is being hired to catalyze continued growth as PLNT reaches maturity in the U.S.

Franchise Royalty Rates - In 2017, PLNT increased its royalty rates from five to seven percent (royalty rates typically range from 4-12% for franchises overall). As of December 31, 2022, only 47% of stores were paying the seven percent royalty rate. With most franchisees on 10-year cycles, there's room for blended royalty rates to grow.

Equipment Replacement Cycles - Historically, PLNT has been lax with five-year cardio and seven-year non-cardio equipment cycles. Stricter enforcement of replacement cycles will boost revenue and increase customer satisfaction.

Larger Negotiating Power - PLNT's made its last public equipment manufacturer announcement with Precor in 2018; at the time, PLNT had about 1,700 clubs. Now with over 2,400 clubs, PLNT can negotiate better prices and improve its equipment margins.

However, as a franchisor, you're often faced with a delicate balance between doing what's best for corporate vs. the franchisee. Let's take a look at the franchisee and how their numbers look.

Franchisee Health

Future growth will rely on attracting new franchises. The key to attracting continued interest from world-class operators and investors is consistent and sustainable cash flows. PLNT's 2023 Franchise Disclosure Document shows that in 2022, the median revenue was $1.7mm and median EBITDA was $522k, a 30% margin. Given that margins in 2018 and 2019 (pre-covid) were around 38%, I feel confident that a reversion from 2022 numbers is still at play.

To get into the mindset of a potential franchisee, let's take these numbers and do a simple back-of-the-envelope analysis:

Created by Author using 2023 PLNT FDD

The median cost to open a Planet Fitness is $3.3mm and typical franchisees may borrow 70% with 30% down. Assuming interest rates of 8.5% ( Conventional Loan Rates ) with a 10-year term and 34% EBITDA margins (midpoint between 2019 and 2022), a franchisee can expect to see mid-teen returns. This assumes a conservative 8x EBITDA multiple where Project Sunshine was sold at a likely higher EBITDA multiples ( $800mm for 114 gyms representing ~$7mm per gym ). As EBITDA margins return to the high thirties, you can expect 20%+ IRRs in Planet Fitness Franchises.

Despite increases in interest rates, I believe PLNT is still an attractive and proven franchise model offering best-in-class margin profiles. Furthermore, PLNT requires $25mm in liquid assets to open a 10-club Area Development Agreement and $10mm in liquid assets for a 3-club consideration. Given these stringent requirements, PLNT mostly attracts larger and more sophisticated investor operators to open new gyms.

Planet Fitness has healthy margins and growth at the corporate and franchisee level, but the question remains: can the McDonald's of gyms sustain its competitive advantage?

How We Choose Gyms…

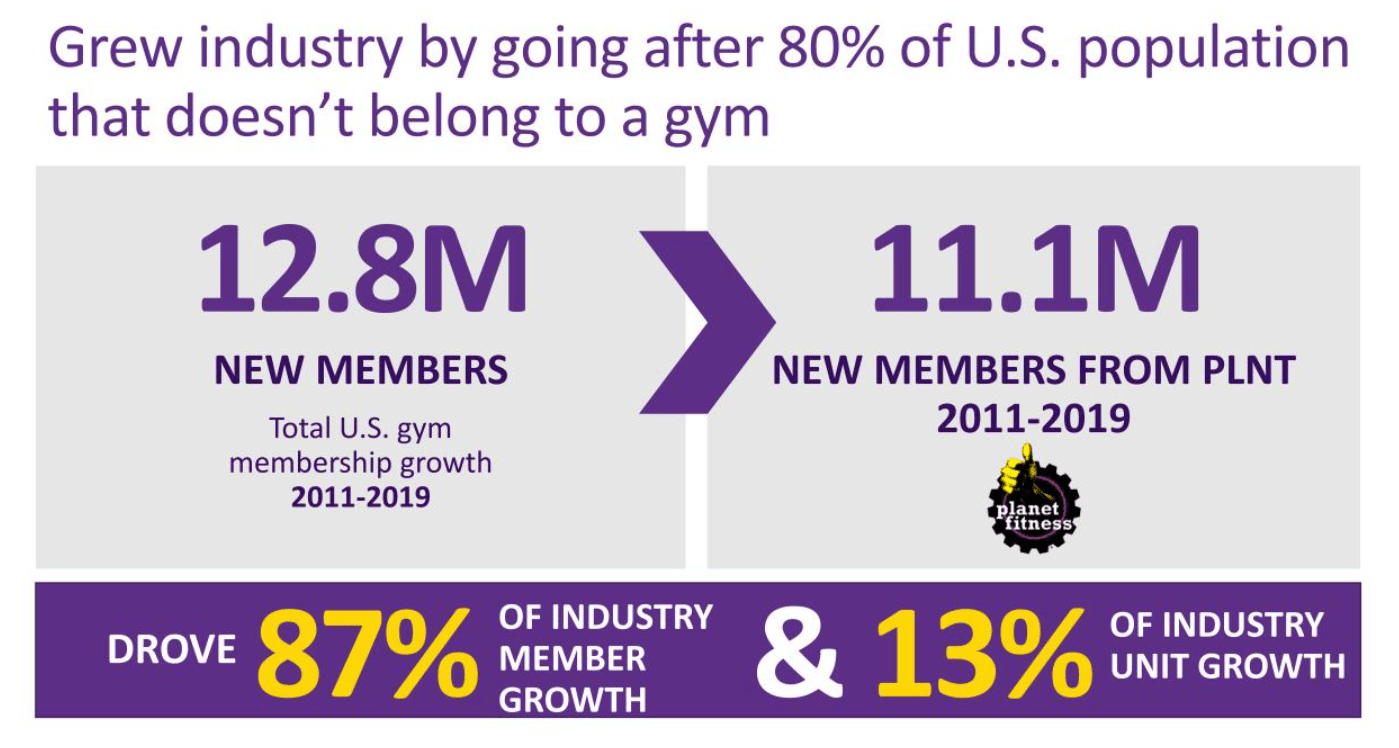

Price and proximity. These are the two most important criteria for Americans signing up for a gym, and Planet Fitness dominates both. This is especially true for first-time gym goers.

From 2011 to 2019, Planet Fitness accounted for 87% of all new gym membership growth while accounting for 13% new unit growth.

Planet Fitness Investor Presentation 2022

{kind=link}

At a $10 membership price, there is no other gym at scale that competes with PLNT. The $10 membership hasn't changed in 30 years. The only other consumer product that hasn't changed price from 30 years ago is the Costco Hot Dog and Drink combo for $1.50. That's another great business.

Like Costco, PLNT has many levers to pull to increase overall membership dues.

Proven Track Record Of Successful Upsell

PLNT offers a black card membership for $24.99 (previously $22.99, previously $19.99) that includes additional access to any PF location, tanning beds, massage chairs, exclusive discounts, and more. Management has not only increased the black card membership's price and value over time, but also increased PF Black Cards as a percentage of total memberships. In 2018, 60% of members held black cards. In 2022, 62.5% of members held black card members despite price increases.

Planet Fitness Investor Day 2022

Despite the headline $10 price point, there are levers PLNT can pull to increase annual membership costs: raising annual fees and increasing mix to PF Black card. These price increases contribute to the 53 straight quarters of same-store-sales (SSS) growth from 2007 - 2020 and 6 quarters of SSS growth since Q3 2021.

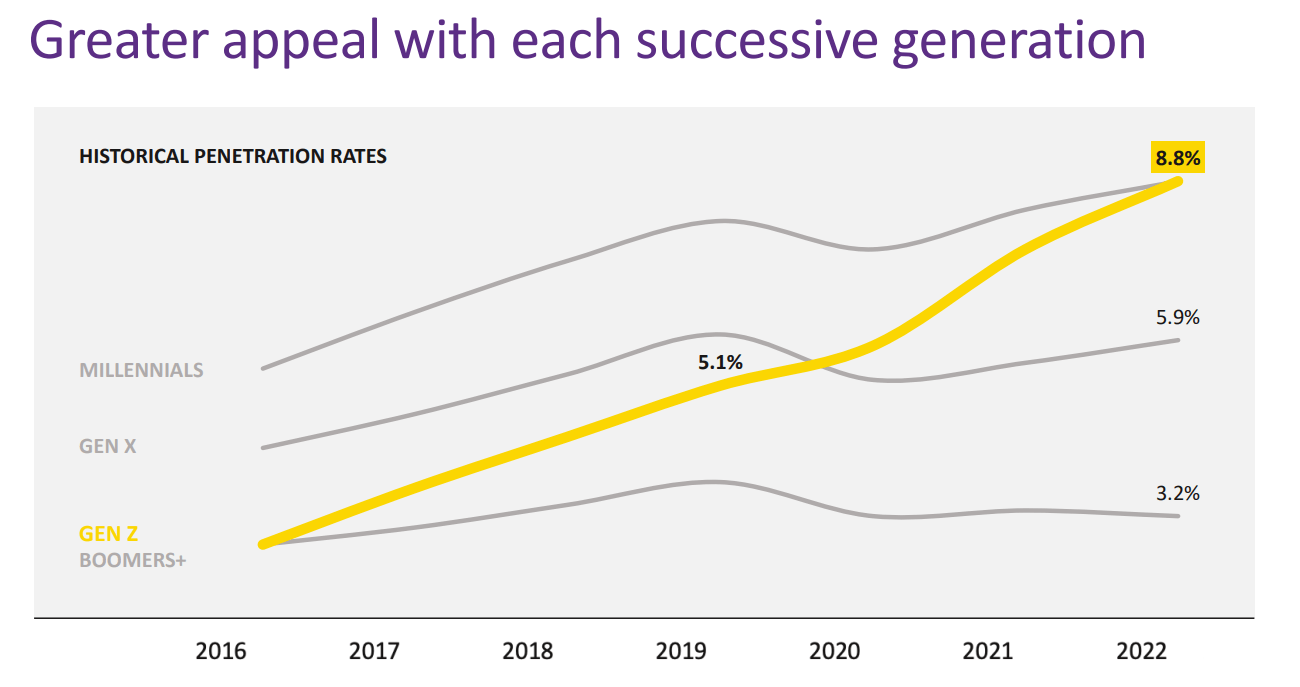

Marketing To New Generations

PLNT outspends all of its peers on marketing, over $1 billion since IPO in 2015 and over $240 million in 2022 alone. #Planetfitness has over 1.7 billion impressions on TikTok, more than any other gym on TikTok by a wide margin. Many of these videos have questionable substance, but they are viral, and that's what matters in today's day and age.

TikTok - First Day at Planet Fitness

As the adage goes, any press is good press. This is especially important for long-term growth as gym membership declines with age; it's an all-out race to capture the younger generation, Gen Z.

Planet Fitness Investor Day 2022

{kind=link}

With the launch of the PF Summer Pass in 2019, high schoolers between the ages of 14-19 received a FREE membership to Planet Fitness for the entire summer. Management noted that 25% of those members in summer 2019 converted to a paid membership and 11% are still members as of Q3 2022, three years later.

More recently, in the summer of 2022, PLNT saw 3.5 million teenagers join through the summer pass and conversions for the summer 2022 cohort are trending higher than the equivalent cohort in 2019. With ~90% of members downloading their mobile app, PLNT has proprietary methods of retargeting and gathering data on this new cohort of Gen Z (and future Gen Alpha) members and converting them to paying members.

With its retail footprint, price point, and digital presence, Planet Fitness is uniquely positioned to grow their customer base and capture the upcoming generations.

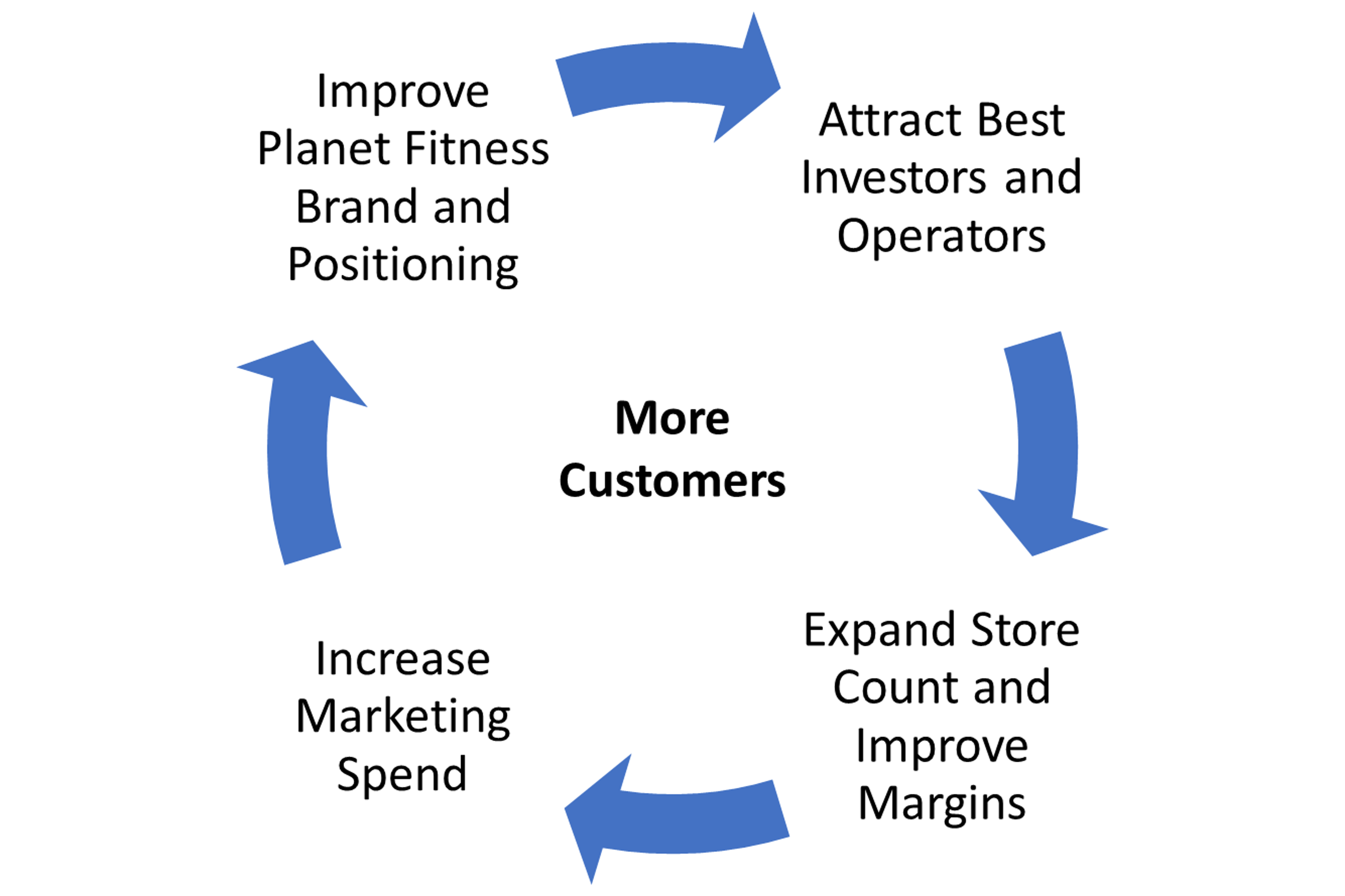

The Virtuous Cycle

To put it all together, PLNT has created a virtuous cycle that isn't easy to replicate. As PLNT continues to offer world-class profitability margins, this attracts the best private equity investors and operators. With better investors and operators, PLNT can expand quickly and spend more on marketing, further strengthening its position and brand. With a better product and brand, this attracts more paying customers. This flywheel relies on over 30 years of fine-tuned operating efficiency and world-class management.

{kind=link}

With this flywheel in motion, PLNT can offer a $10 price at scale because of its size, operations, and brand. Gyms that have the locations don't have the margin to spend (e.g., Anytime Fitness has ~5,000 locations but ~16% EBITDA margins). And gyms that have the margin don't have the locations (e.g., LA Fitness has ~550 locations).

This flywheel is Planet Fitness' moat. It's a way of doing business that has built the brand into what it is today.

Recent Management Guidance And Outlook

Management released guidance in their latest investor deck on June 7, 2023 reiterating placements of 160 franchise stores and SSS of high single-digit percentage range for 2023. As mentioned before, we think PLNT is ahead of new store openings and will likely end the year closer to the 200-store mark (inclusive of company-owned store opens).

Management also guided to low-to-mid teens % growth for Revenue, high teens % growth for AEBITDA, and low-to-mid 20% growth for AEPS (inclusive of planned share repurchases). As long as PLNT can continue to open new franchises, this growth trajectory seems reasonable given historical trends (ex-COVID).

What Can Go Wrong?

Despite PLNT's historical execution and growth prospects, there are risks to the business.

Non-Usage - Gyms often rely on a subset of members to not show up, thereby subsidizing frequent gym-goers. This is common and allows gyms to sell more memberships than it would be able to handle if all members showed up at the same time. Some sources say that as many as 60% of PLNT members won't visit in a 30-day period. But non-usage is also a leading indicator of churn. I believe interest in fitness and health will continue to accelerate in importance, but just in case, I'm referencing Blink Data to track daily utilization rate changes across all PLNT locations to notice any drastic changes.

app.blinkdata.io as of July 20, 2023

"Click to Cancel" Legislation - A proposal by the FTC proposes a click to cancel provision requiring sellers to make it as easy for consumers to cancel their enrollments as it was for them to sign up. Planet Fitness currently requires most members to cancel in person or physically mail a cancellation request. Some argue that the passing of a "Click to Cancel" proposal would decimate Planet Fitness' business.

Click to cancel has already been in place for a few states at PLNT, including California . There, management has noticed an initial boost in cancellations, but found these rates tend to normalize after the first few months. Management noted Tennessee is likely to be next; it will be interesting to monitor whether the same trends are obtained.

While there have been numerous reports of difficulties canceling Planet Fitness memberships, I believe they are overblown. You don't get to 18 million recurring members without upsetting a few. Plus, the 30% rejoin rate by canceled members is likely one of the highest in the industry and a testament to the value Planet Fitness provides.

Planet Fitness has also been working hard to provide value for those who don't go to the gym. They recently added discounts and promotions for partner retailers like Reebok, Swell, and Crocs, making it harder for members to cancel. Depending on usage, the discounts earned can be greater than the cost of membership.

Valuation is Expensive - Most analysts on Seeking Alpha have valued PLNT on a historical or forward P/E ratio. I have chosen a comp set including fitness peers (LTH, PTON, and LULU) in addition to franchise peers (DPZ, LOCO, QSR, FRG, MCD, and WING). Indeed, PLNT currently trades at 40x forward P/E and 54x LTM P/E which is a premium to industry peers at 38x forward P/E and 45x LTM P/E.

Seeking Alpha as of July 20, 2023

{kind=link}

However, PLNT is still in a growth phase and should be valued on growth-adjusted multiples. If we take PEG ratios (growth adjusted P/E multiples), PLNT trades at 0.55 LTM PEG and 1x FWD PEG while comps trade at 1.4 LTM PEG and 2.6 FWD PEG, representing a 60% discount to comps. If you take into account the growth of PLNT, the current valuation is quite conservative to its chosen set of peers.

That being said, if PLNT starts trading at a premium on a PEG ratio, I would reevaluate.

Slower Build Out due to Rising Interest Rates - High interest rates are a headwind for new store build outs that will need to be continually monitored. However, this is an issue for ALL gyms. Planet Fitness gyms are more expensive to build, but they have higher EBITDA margins. PLNT franchisees are run by professional investor operators who are also likely to have better borrow rates than individual mom and pops.

Gyms are Cut in a Recession - The basket of goods cut first during a recession includes luxury goods, travel, home improvement, new cars, and gym memberships. However, PLNT is a HVLP gym and more recession-proof. If anything, PLNT should outperform in a downturn where individuals trade higher priced mid-tier gyms for PLNT memberships.

Here's how PLNT performed during the last recession.

Planet Fitness Investor Day 2022

Final Thoughts

I am bullish on Planet Fitness because they have built a moat around their brand and operations to attack a massively underserved market. PLNT offers a low-price that is not replicable at scale for other gyms. At the same time, it has proven its ability to increase membership dues without increasing the headline $10 entry price. Despite macro headwinds, the core business should perform well over a 3-5 year time horizon. Additional growth levers such as digital products and health insurance coverage could contribute as well.

I'm excited to see PLNT's journey and would love to hear your thoughts on my analysis.

For further details see:

Planet Fitness: $10 Membership Pricing Is A Moat