PLNT - Planet Fitness: A Look At The Numbers Suggests Too Expensive

2023-03-29 04:17:58 ET

Summary

- Strong FY22 performance, however, with slight margin contractions.

- Guidance growth in the mid-teens for '23 from the management seems a bit low for a company that trades at 64x its earnings.

- Financials are a mixed bag.

- Even with more optimistic assumptions, the company is well overvalued.

Investment Thesis

Very impressive y-o-y revenue growth piqued my interest to look further into Planet Fitness ( PLNT ) to see how this growth company can sustain such rapid growth. With the management forward guidance of only around 13% for '23 and '24 I don't see how the company can sustain such a share price multiple in the long run. Even with my more generous estimates of revenue growth for the next 10 years, and an improvement in margins, the company is still very much overvalued and in the long run will come down if the company is not able to sustain such growth for the next decade.

In this article, I will discuss what worked for PLNT in '22, what they got in store for the future, and how that will affect their revenues. I will also look into how manageable their long-term debt is and the overall health of the balance sheet, and then I will present, in my opinion, a very optimistic DCF model.

FY2022 Results

As I mentioned the company saw good revenue increases from the year before. 60% increase y-o-y which can be attributed to people becoming more health-conscious after the pandemic lockdowns and in the last quarter of '22 the company was able to leverage local and national media on the marketing side of things. Net income more than doubled from the previous year, and gross margins have contracted slightly, around 300 bps but net margins managed to increase by about the same.

The management mentioned that they are expecting to grow 13%-14% in '23, which is much slower than what the company has seen in the last two years since the pandemic (44% in'21 and 60% in '22). The company currently trades at around 64x earnings, with that sort of an outlook for the next year, it seems that it is a little expensive. Let's have a look at what worked for them to get that 60% growth and would they can do in the future to improve returns.

Outlook

As I mentioned above what drove most of the revenue growth was people becoming healthier, which saw membership increases of 1.8m for the year, bringing the total memberships to around 17 million. That's a 10% y-o-y increase in memberships. Marketing also played a big role to promote the healthy way which brought in more customers and the opening of 158 new locations helped boost that as well.

In terms of future performance, the management expects to double their membership count but did not provide any solid timeline for that, so I will not focus on that growth prospect too much. They are going to continue to open more stores, however, they are still seeing some price pressures on that aspect of getting more stores opened especially in the first half of '23, as they believe they will be behind their target due to HVAC availability and other supply chain issues. The management is aiming to open 200 new stores per year, so 2,000 new stores in the next decade. That will certainly be a massive boost over time, however, that is a long time and so I need to discount the growth for the model.

I believe that increasing their membership prices could lead to higher revenues in the future, although not at the same levels as before. This could also improve margins overall. All new upcoming stores will start with the new pricing for the Black Card and increased annual fees, which will turn into around 300bps-400bps of margin increases. Eventually, all stores will see this new pricing level, but it will take time. The initial results of price increases showed that the customers are not price sensitive and did not see any cancelations due to the higher price. The company went ahead and increased prices for all their stores as the test was a success.

If the company continues on the same track as they have, I don't know why its guidance was so low. Maybe they are trying to under-promise and over-deliver when it comes to the year-end results.

Financials

The big item that stands out straight away is how the management is running the operations. Opening up so many new stores is very capital intensive for sure, so it's no surprise that the company amassed quite a substantial debt position, around $2B. I am not the biggest fan of debt especially when the company's market cap is around $7B while total debt is a bit less than a third. Let's dig into that in more detail to see if this is a red flag and if the company will have any problems with future obligations.

The company has a decent amount of cash on hand at the end of 2022, almost $410m. Interest expense on debt came out to be $88.6m for the year. Seems like the company is well able to pay off interest even with just the cash on hand which is a good sign. In addition to that, the company has a good operating cash flow throughout the year which also more than covers the interest. The interest coverage ratio sits at around 2.6x, which is not bad, however, there might not be too much wiggle room in the future if the company keeps re-financing its debt.

It looks like the company is managing the debt reasonably, however, with elevated interest rates in the economy, if the company continues to refinance its debt when another debt is due, interest payments could become harder to manage. Fortunately, that hasn't happened yet as the company brokered a deal for upsizing their debt which resulted in a lower weighted average interest rate for the total fixed debt. I'm not sure how easy it will be for them to keep lowering the interest rate in the future with such elevated interest rates to stay for a while and increase still.

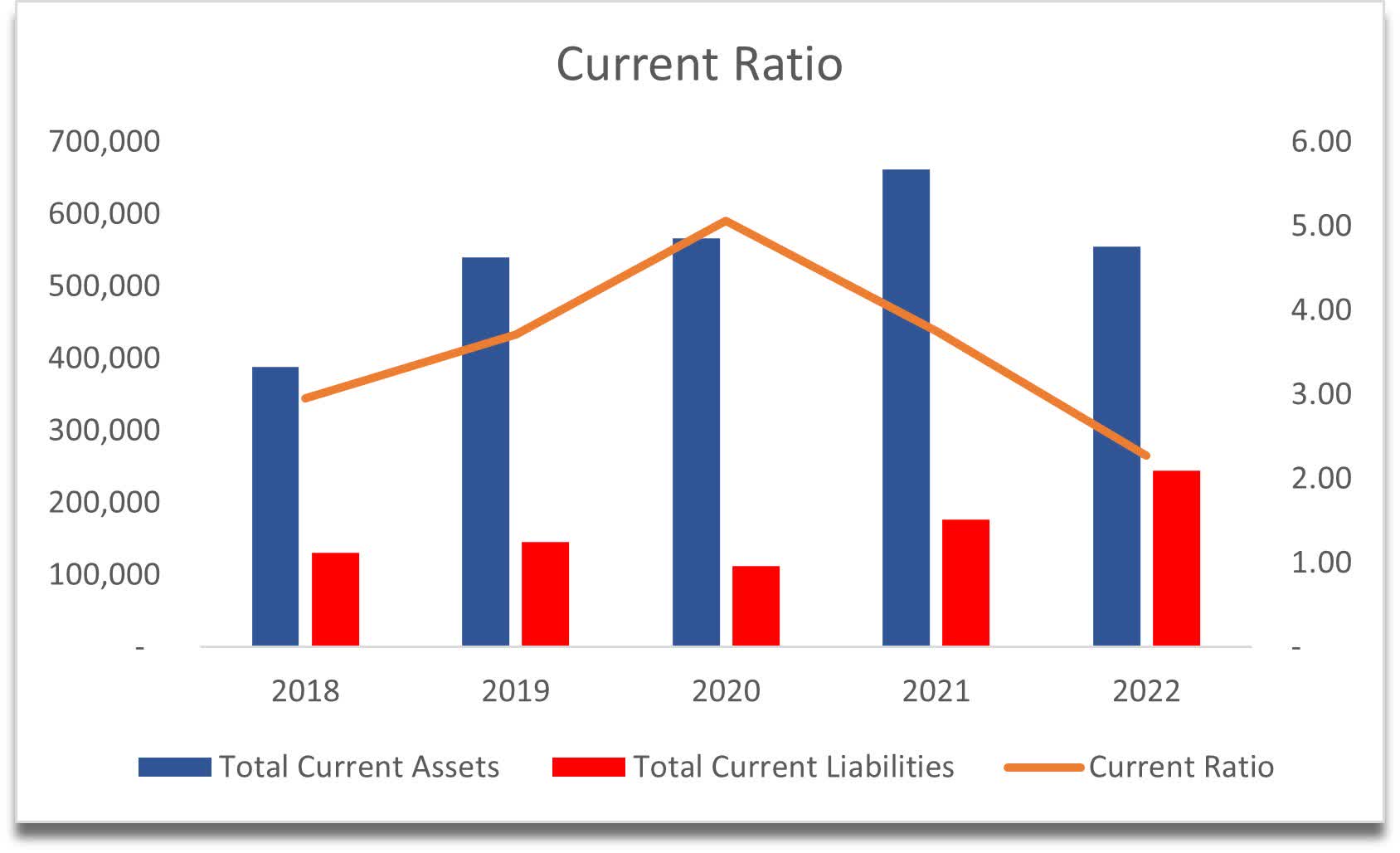

Further on liquidity, the current ratio is more than acceptable. It's been hovering well above the 2.0 threshold that I like to see, however, we can see a sharp drop-off in recent years. Let's hope it stabilizes there and does not drop below further.

{kind=link}

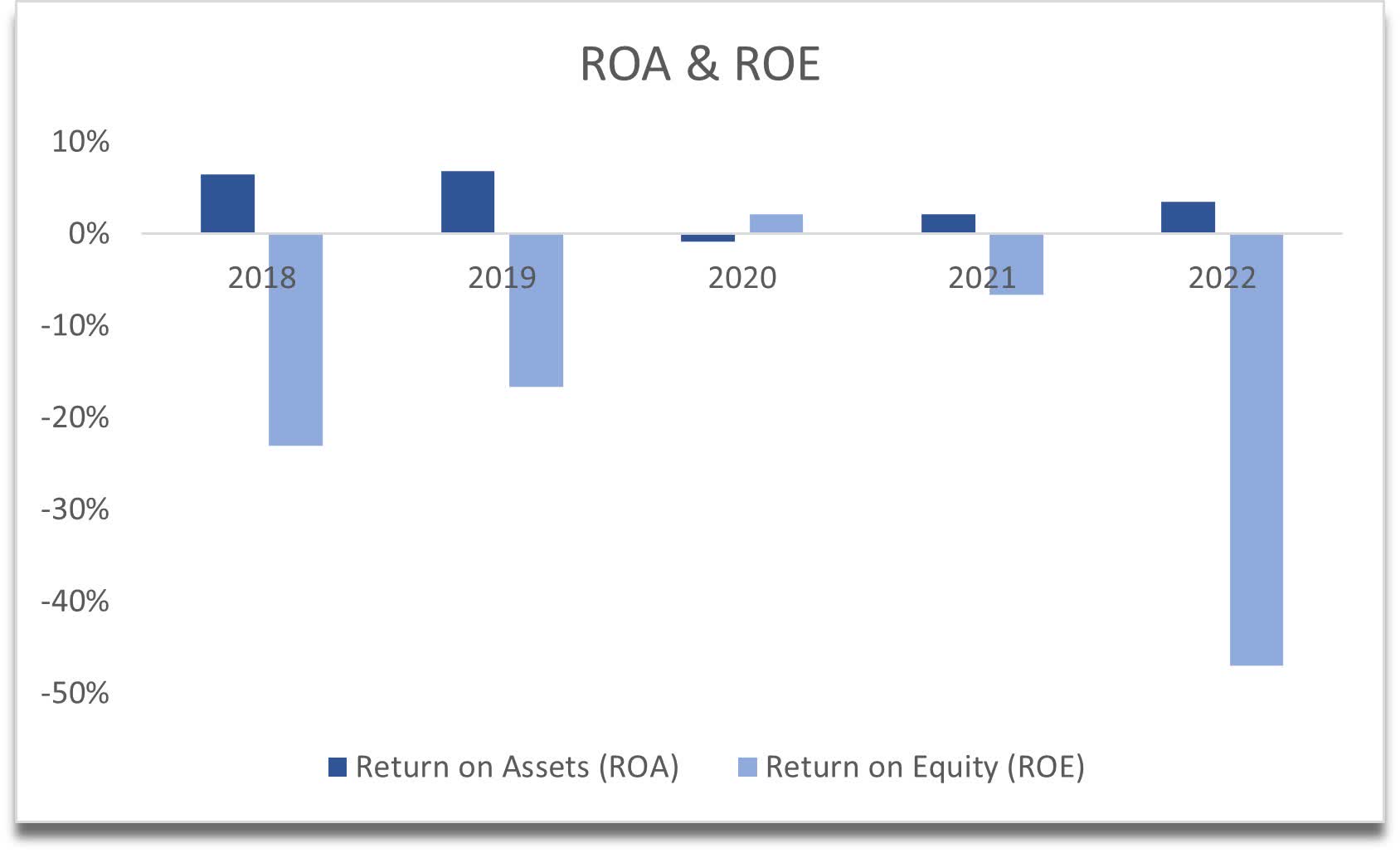

The next metrics show how the company is using the capital available to them, and how efficient and profitable the company is with it. I am not liking what I'm seeing in terms of ROA and ROE. As you can see below out of the 5 years shown, ROE has been negative while ROA has been slightly positive only.

{kind=link}

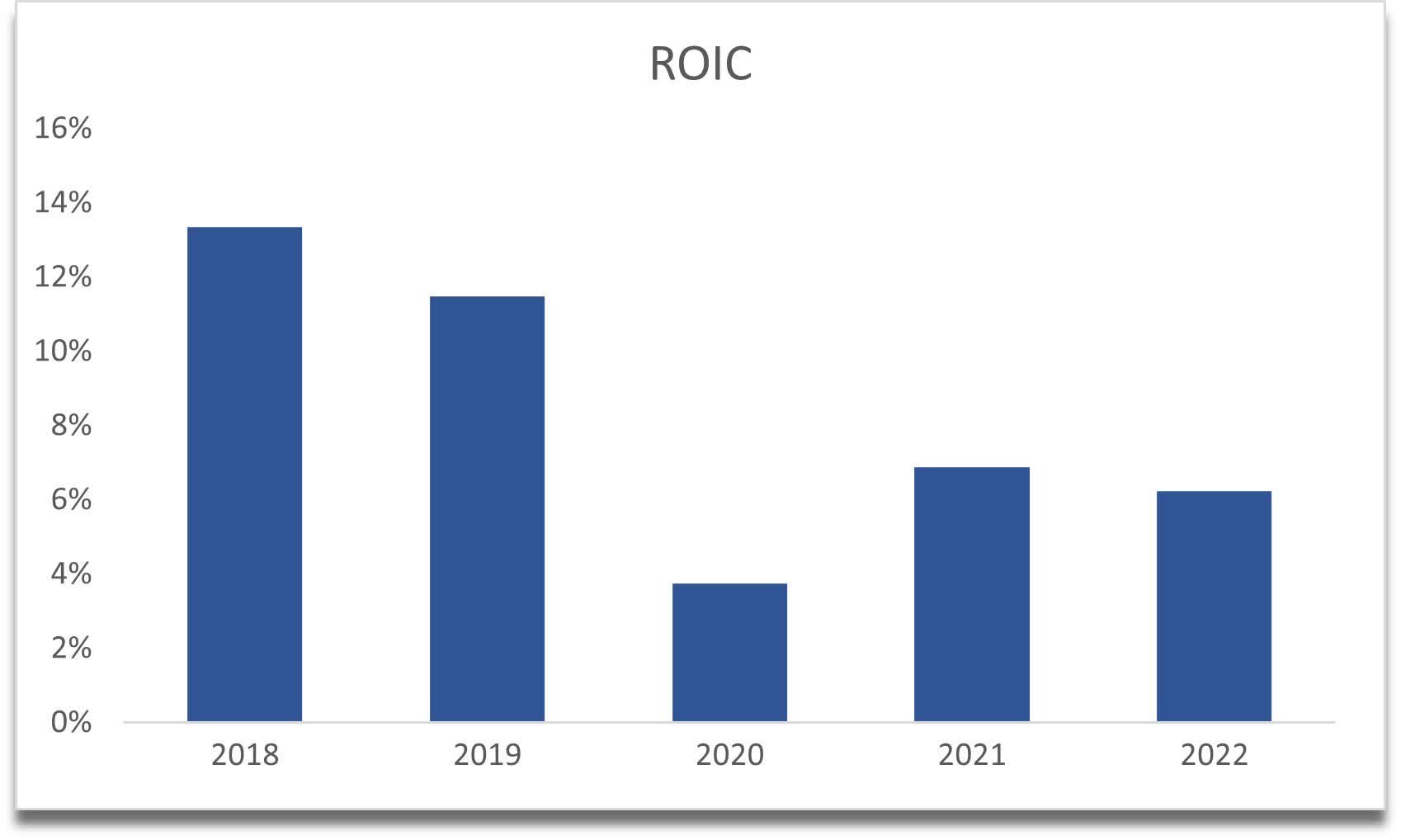

It is not looking much better in terms of invested capital as ROIC has been decreasing for the last 5 years.

{kind=link}

I usually don't mind paying a slight premium on a company that shows efficiency and high profitability metrics, however, it is not the case here and if this continues, the company does not seem to fit my criteria of what is a good investment.

Overall, some parts of the balance sheet are quite good, some could be improved on. I would like to see improvements in terms of steady reduction of the debt as I believe taking on more debt constantly in a high-interest rate environment is not a good idea, especially when debt makes up almost a third of the total market cap of the firm.

Valuation

I decided to be more optimistic than what the management is saying about the future revenue growth, granted they only provided one year's estimates, nevertheless I will approach my valuation with a much more upbeat tone just to show that even with much higher assumptions on revenue growth and improvements in margins, the company is still quite overvalued at this time.

Starting with the revenue assumptions for my base case, I decided to go with no recessionary environment built in at all and no more COVID measures coming back. I assume revenue will grow at double what the management is expecting for '23, at around 30%, and linearly grow it down to 10% by '32. This gives me around a 20% annual growth rate for the next decade. For the optimistic case, I added 2% extra in each period and for the conservative case, I took away 2% from the base case. For the base case scenario, the revenue will be at around $5.7B by '32.

In terms of margins, for the base case, I have gross margin improvements of around 340bps by '32 from current levels and around 300bps for operating margins. For optimistic cases, it is 100bps more and for conservative cases 100bps less on gross and operating margins. My reasoning for margin expansions is that the new higher pricing will become the new norm in all their stores which will improve margins because the new stores that will open with the new higher pricing will achieve higher margins from the get-go.

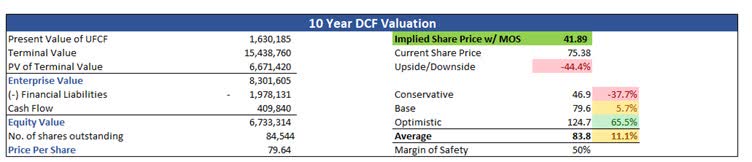

Seeing that this is a growth stock that has seen quite a bit of volatility, for that reason, I decided to give a much larger margin of safety to the intrinsic value. I usually go for 25%, however, this time I feel 50% is in order. With that said, if we assume 20% annual growth in revenues and margin expansion for the next decade, the company's intrinsic value is $41.89, which implies a 44% downside from current valuations.

10-Year DCF Valuation with more optimistic assumptions (Own Calculations)

{kind=link}

Closing Remarks

Even with much higher assumptions than what the management has guided for the company's growth, the lowest P/E ratio I would consider even looking at the company as a potential investment is around 35x. If the company can grow at the speed I modeled, the company is worth half of what it is trading at now, especially if the next year's revenue growth is hardly in the mid-teens.

I tried to model an outcome with the management's expectations and you can imagine it looked much worse than my optimistic model above. A company with a multiple of 64x should be seeing much higher growth potential than what they are guiding. Furthermore, if we do see a slowdown in the economy, gym memberships would be one of the first ones to go so that is a big warning there for anyone who would like to invest in the company for the long term.

I won't go as far as recommending a sale, as companies like Planet Fitness sometimes don't follow the fundamentals in the short run and might outperform the market. I'll keep the stock on my watchlist with a price alert below 50 so I can re-evaluate my analysis as we get more numbers in the upcoming quarters, and hopefully, by that time we will have a clearer picture of the economy and the demand for the company's services.

For further details see:

Planet Fitness: A Look At The Numbers Suggests Too Expensive