PLNT - Planet Fitness: The King Of An Asset-Light Business

2023-07-24 23:38:45 ET

Summary

- The recent acquisition has significantly changed Planet Fitness's business structure, leading to a market revaluation.

- The company's structural changes are temporary, but the outlook for the company's competitiveness and growth opportunities remains positive.

- I believe that the current share price of PLNT is an appropriate level to invest in considering the risks and opportunities.

Investment thesis

Planet Fitness Inc. ( PLNT ) is one of the largest franchisors and operators of fitness centers in the United States. The company's business model is characterized by an asset-light model. By granting licenses to a third-party to use the company's brand and business model in exchange for fees or royalties, the company has enabled rapid growth without heavy capital expenditures.

But recently, the company made a big acquisition of Sunshine Fitness Growth Holdings, which was one of its franchisees. The acquired company owned and operated 114 franchise stores. As a result, its corporate-owned stores increased to 234 stores in 2022 from 112 stores, approximately doubled from the previous year. Now, the corporate-owned stores account for about 10% of the total compared to 5% prior to the acquisition. Corporate-owned stores are more capital-intensive than franchising. The increase in corporate-owned stores made investors concerned because it may worsen the company's cash flows and balance sheets.

However, I believe that the company's change in its business structure are just a temporary response to macro-economic changes such as a rapid increase in interest rates. Its competitiveness remains strong, and in fact, its market position has been further strengthened in comparison to its direct fitness center competitors. I expect that the company will return to a business structure focused on franchising within a short period of time, and if this materializes, the market will reevaluated the company. Therefore, I believe that the current stock price is attractive to invest.

Company overview

Planet Fitness is a franchisor and operator of fitness centers. It recorded revenues of $936.8 million and system-wide sales of $3.9 billion in 2022. It has about 17.0 million members and 2,410 stores in all 50 states as well as Canada, Panama, Mexico, and Australia. It operates three main business segments: Company-owned stores, franchising, and equipment division. The following table displays the revenue and EBITDA for each business segment.

| Revenue |

| Weight |

| EBITDA |

| Weight |

| Unit: |

| % |

| % |

| Franchise |

| 330 |

| 35 |

| 217 |

| 59 |

| Corporate-owned |

| 379 |

| 41 |

| 142 |

| 39 |

| Equipment |

| 228 |

| 24 |

| 59 |

| 16 |

Source: 2022 Annual report

Each business segment is associated with operating fitness centers, but they exhibit significant differences in terms of revenue and expense patterns, profitability and cash flow quality. First, franchise segment revenue includes royalties and fee from franchisees. This segment demonstrates the highest profitability among the three segments as franchise revenue has little cost of goods sold and minimal operating expenses. Furthermore, franchise-owned stores are funded by a third party, resulting in lower investment burdens for the company, and enabling high cash flow generation.

Second, the company-owned stores recognize revenue directly from operating the fitness centers itself, which results in a significant revenue scale. However, the profitability is not necessarily high. In addition, higher operating expenses and capital expenditures for operating stores can negatively impact the ability to generate free cash flows.

Lastly, the equipment segment generates revenue through the replacement of exercise equipment in franchise stores. This segment accounts for a significant portion of the company's cost of goods sold. While profitability may be relatively lower, it helps create repetitive cash flows through periodic equipment replacements specified in the franchise agreement with a certain cycle (typically 5 to 7 years).

Considering that the value of a company is determined by the present value of future cash flows, it can be said that the growth of the franchise segment (the highest profitability and the lowest reinvestment needs, resulting in high-quality cash flows) will have the greatest impact on the company's value.

Quality analysis

Growth

The company's revenue in 2022 has increased by about 1.7 times compared to the 2018 level , with an average annual growth rate of 15%. The company has abundant opportunities for growth through various sources, including increasing the number of stores through franchisee recruitment, expanding the member base through advertising and marketing, and venturing into international markets to explore new market opportunities. In the short term, the company can materialize the growth just with existing franchisees. They have an obligation under contracts to open additional 1,000 franchise stores, with over 500 of them required to be open within three years. Furthermore, according to the company's internal analysis, it has the potential to grow its store base over 4,000 stores in the United States alone.

{kind=link}

Next, the company can achieve growth through an effective combination of pricing strategies. It offers two types of memberships: Classic Membership which has an annual fee of $39 and a monthly fee of $10, and Black Card Membership which provides more perks and has the same annual fee and a monthly fee of $24.99. As of the end of 2022, 62.5% of the total membership were Black Card Memberships, showing an increase compared to 60% at the end of 2018. During the same period, the monthly membership fee per member increased from $16.52 to $18.01. This increase is expected to continue gradually as members perceive that despite the higher price, the membership provides them with greater value and benefits.

Lastly, an additional growth opportunity will come from international markets. The company has expanded into markets beyond the United States, including Canada, Australia, Mexico, and Panama. As of the end of the third quarter of 2022, the company operated 60 stores in Canada, 10 stores in Australia, 12 stores in Mexico, and 6 stores in Panama. Given the company's simple business model and unique value proposition, it is anticipated that significant growth opportunities can be enjoyed in these new markets as well.

{kind=link}

Competitive advantages

The company has not only abundant growth opportunities ahead but also strong economic moats. First, the company offers high quality fitness centers at incredibly affordable prices (about $18, significantly below the industry average of $58 per month). Not only is the price competitive, but the company also tries hard to sustain its unique value proposition by strictly making its welcoming, non-intimidating environment called Judgement Free Zone durable. As a result, the company effectively lowers the barrier to entry for newcomers, making it possible to target a broader member base, approximately 80% of the U.S. and Canadian populations over age 14 who do not belong to a gym.

Second, as a leading player in the fitness industry, the company enjoys a strong market position and scale advantage. As of the end of the third quarter of 2022, the company operates 2,353 centers, while the second-largest operator has only 400 centers.

{kind=link}

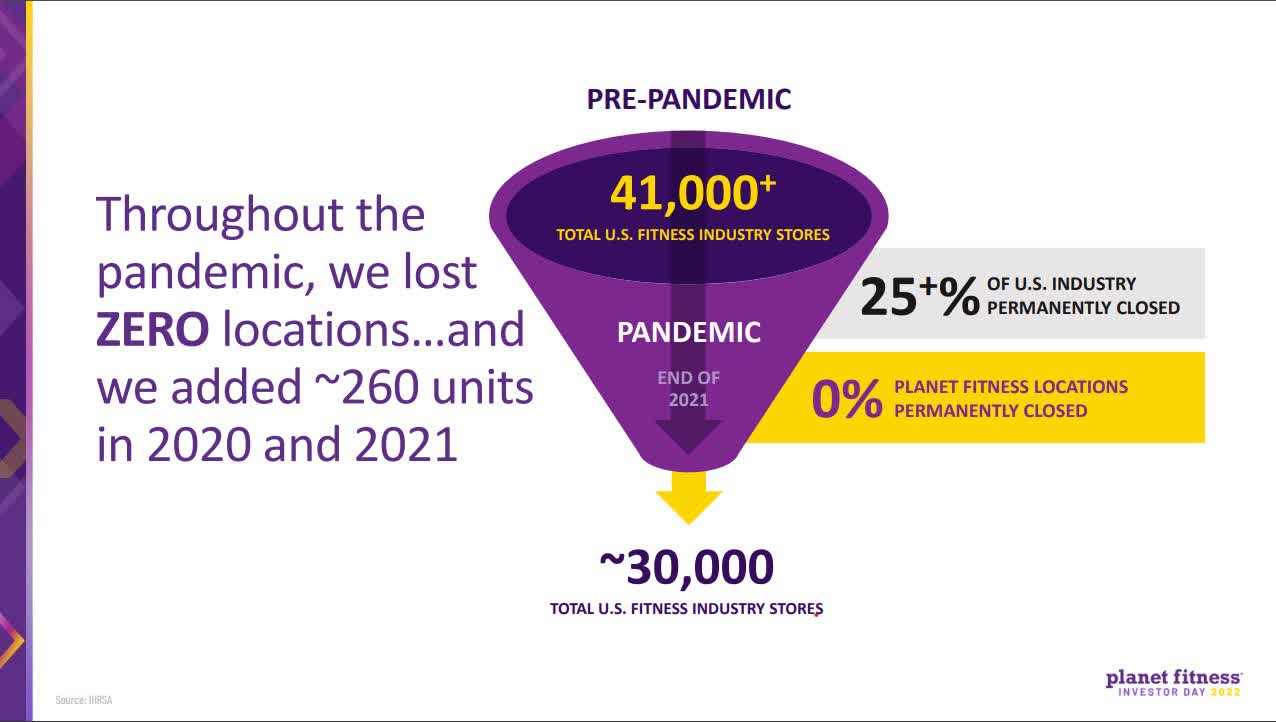

Even when combining the number of stores of the following top 10 companies, it amounts to only half of the company's total. The gap between the company and its competitors has widened even further during the pandemic. The pandemic disrupted industries associated with physical human contact, including fitness centers. Consequently, many fitness centers had to close their doors. However, during the same period, the company not only kept all its centers open but also expanded. This was possible due to its flexible business structure, which allowed it to adapt during the crisis. Thanks to its overwhelming scale, the company can maintain strong purchasing power for exercise equipment and other related items. Additionally, it helps to facilitate to recruit new franchisees and enhance its brand power through nationwide advertising campaigns, far more scalable and effective than its competitors.

{kind=link}

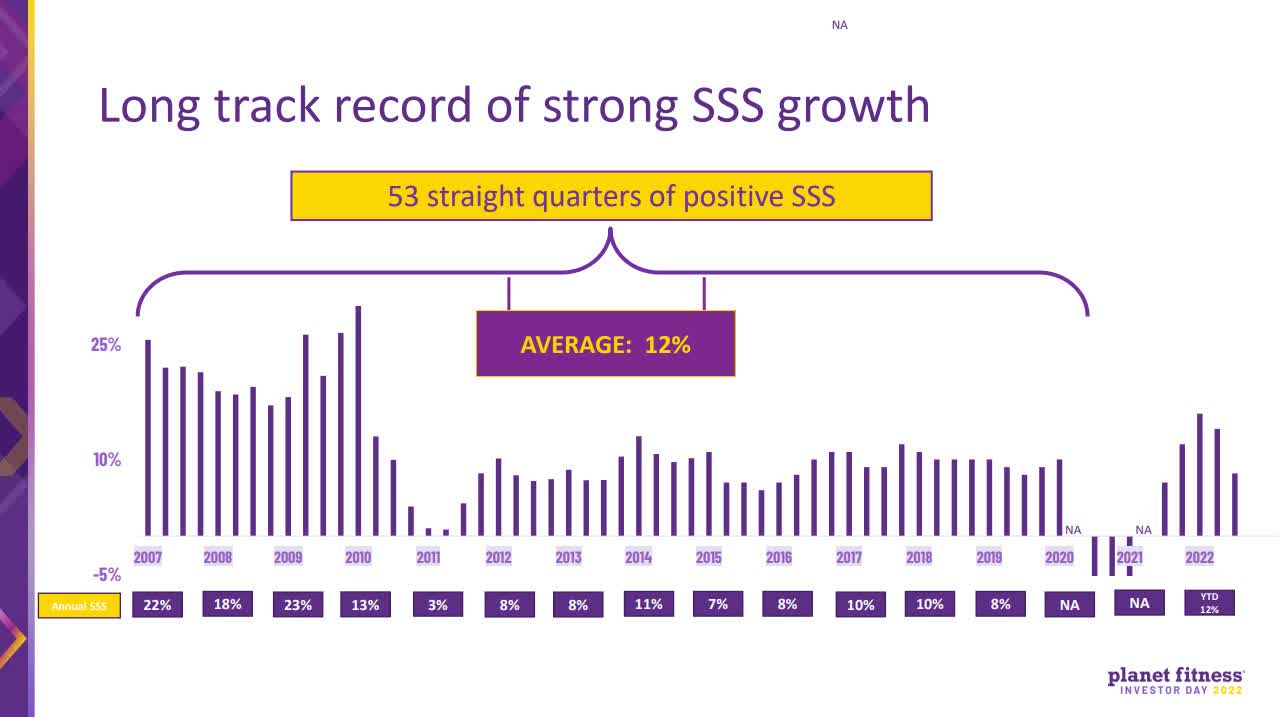

Lastly, the company has demonstrated high ROICs by presenting a highly attractive business model to franchisees over the past years. Its fitness centers operate on a simple and easy-to-run model with mainly fixed cost structures, allowing them to generate strong cash flows in line with revenue growth. Unlike other quick-service restaurant franchise stores, there is no inventory risk involved. The expansion of franchise stores provides predictable, repetitive cash flows through royalty fees, equipment replacements, and other sources to the company.

Historical ROIC without goodwill (Expensed investment adjusted)

| FY13 |

| FY14 |

| FY15 |

| FY16 |

| FY17 |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| 17.3% |

| 25.0% |

| 29.3% |

| 34.7% |

| 41.2% |

| 46.4% |

| 43.6% |

| 9.1% |

| 22.7% |

| 25.4% |

Valuation

During the past period, the company demonstrated the rapid growth rates while maintaining stable cash flow generation. As the company has entered its mature stage, I used the free cash flow yield as a valuation method. I made several assumptions to estimate future free cash flows. Firstly, the number of total stores is projected to increase from 2,446 in the first quarter of 2023 to 3,655 over the next five years. As mentioned earlier, 500 of these stores are contractually required to be opened by existing franchisees within the next three years. The rest can be developed from domestic and international markets. As a result of my assumption the number of total stores is anticipated to increase at an average annual growth rate of approximately 8.4%. It's worth noting that from 2020 to 2022, the number of the stores increased at a growth rate in the 6.0% range due to pandemic effects, whereas before the pandemic, the growth rate was around 15%.

Next, as of the end of 2022, the company's system-wide sales were approximately $3.9 billion, and when divided by the total number of stores, the revenue per store is about $1.7 million. For the next five years, I have assumed that the sales per store will grow at a rate of 4%. The company's average same-store sales growth rate was 12% but considering factors such as store openings and closures over the next five years, I have taken a conservative approach with a 4.0% assumption. Taking these assumptions into account, the system-wide sales is expected to reach approximately $7.0 billion after five years.

{kind=link}

My investment thesis is based on the expectation that although the company's corporate-owned store proportion has temporarily increased, it will eventually return to a higher franchise proportion, as it was in the past. Considering this, I have assumed that the current store proportion will remain the same for the next two years. From the third year onwards, I assumed the proportion of corporate-owned stores to change from 10% to 5%. Lastly, the equipment segment sales are closely linked to that of franchise stores. Historically, the equipment segment revenue was approximately 7% of the system-wide franchise store revenue. I have assumed that this proportion will remain consistent over the next five years. The table below represents estimated revenue figures by business segment:

| FY24 |

| FY25 |

| FY26 |

| FY27 |

| FY28 |

| System-wide sales |

| $ Millions |

| 4,381 |

| 4,829 |

| 5,425 |

| 6,206 |

| 7,099 |

| System-wide sales per store |

| $ Millions |

| 1.7 |

| 1.8 |

| 1.9 |

| 2.0 |

| 2.0 |

| Franchisee-owned stores |

| # |

| 2,332 |

| 2,472 |

| 2,869 |

| 3,156 |

| 3,472 |

| Corporate-owned stores |

| # |

| 260 |

| 275 |

| 152 |

| 167 |

| 183 |

| Total stores |

| # |

| 2,592 |

| 2,747 |

| 3,021 |

| 3,323 |

| 3,655 |

| Franchise |

| $ Millions |

| 354 |

| 390 |

| 463 |

| 529 |

| 605 |

| Corporate-owned stores |

| $ Millions |

| 452 |

| 497 |

| 286 |

| 327 |

| 372 |

| Equipment |

| $ Millions |

| 275 |

| 303 |

| 360 |

| 412 |

| 471 |

| Total Revenue |

| $ Millions |

| 1,081 |

| 1,190 |

| 1,108 |

| 1,267 |

| 1,449 |

Next, to calculate operating profit, I used the average EBITDA margins for each business segment over the past 5 years. I also calculated other remaining operating expenses using the average of the past 5 years. Marketing-related expenses were capitalized, and then the operating profit was adjusted accordingly. Historical EBITDA margins are as follows.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Franchise |

| 68.1% |

| 69.3% |

| 55.8% |

| 66.8% |

| 65.8% |

| Corporate-owned stores |

| 40.9% |

| 41.1% |

| 20.2% |

| 29.4% |

| 37.5% |

| Equipment |

| 22.7% |

| 23.7% |

| 15.7% |

| 23.0% |

| 25.9% |

| Corporate and other |

| (7.6%) |

| (6.7%) |

| (8.2%) |

| (13.3%) |

| (5.3%) |

| Total EBITDA margin |

| 37.2% |

| 39.4% |

| 29.1% |

| 33.2% |

| 39.3% |

Lastly, to calculate the free cash flow, I took into account depreciation and capital expenditures. To maintain consistency with the revenue assumptions, for the first 2 years, I assumed higher depreciation and capital expenditures due to the higher proportion of company-owned stores. From the third year onwards, as the proportion of company-owned stores decreases, the scale of depreciation and capital expenditures also decreases accordingly.

| LTM |

| FY24 |

| FY25 |

| FY26 |

| FY27 |

| FY28 |

| Total Revenue |

| $ Millions |

| 972 |

| 1,081 |

| 1,190 |

| 1,108 |

| 1,267 |

| 1,449 |

| EBIT, adjusted |

| $ Millions |

| 258 |

| 334 |

| 365 |

| 367 |

| 434 |

| 508 |

| D&A |

| $ Millions |

| 134 |

| 130 |

| 138 |

| 76 |

| 84 |

| 92 |

| EBITDA, adjusted |

| $ Millions |

| 392 |

| 464 |

| 503 |

| 443 |

| 518 |

| 599 |

| Reinvestment |

| $ Millions |

| (142) |

| (170) |

| (113) |

| (58) |

| (72) |

| (79) |

| FCF |

| $ Millions |

| 250 |

| 294 |

| 389 |

| 385 |

| 446 |

| 521 |

I calculated the earnings yield using EBIT and Enterprise Value and FCF and Equity Value. After 2 years, significant growth is anticipated as the company's business portfolio shifts to an asset-light structure. Compared to the 5-year government bond with a 4% interest rate, I believe the company has a relatively higher investment attractiveness.

| FY24 |

| FY25 |

| FY26 |

| FY27 |

| FY28 |

| Earnings yield (EBIT) |

| 4.4% |

| 4.9% |

| 4.9% |

| 5.8% |

| 6.8% |

| Earnings yield ((FCF)) |

| 5.2% |

| 6.9% |

| 6.9% |

| 8.0% |

| 9.3% |

| Treasury yield (5y) |

| 4.0% |

| 4.0% |

| 4.0% |

| 4.0% |

| 4.0% |

Risks

The company's key risk appears to be credit risks, as it has taken on higher leverage levels through acquisitions that exceed historical levels. While the historical total debt to EBITDA ratio was around 5 times, it currently stands at around 6 times. However, I believe there is not a significant cause for concern. Firstly, examining the maturity structure of the borrowings, they seem to be well distributed across different years. There is no concentration of debt maturing in a single year, reducing the risk associated with refinancing.

| Debt schedule |

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| Thereafter |

| total |

| Lease |

| 50 |

| 61 |

| 61 |

| 59 |

| 55 |

| 171 |

| 457 |

| Long-term debt |

| 21 |

| 21 |

| 600 |

| 419 |

| 10 |

| 954 |

| 2,025 |

| Total |

| 71 |

| 81 |

| 661 |

| 479 |

| 65 |

| 1,125 |

| 2,482 |

| Weight |

| 2.8% |

| 3.3% |

| 26.6% |

| 19.3% |

| 2.6% |

| 45.3% |

| 100.0% |

Another significant risk is related to the acquisition of Sunshine Fitness on February 10th, 2022. The company acquired a 100% stake in Sunshine Fitness, which operated 114 stores in Alabama, Florida, Georgia, North Carolina, and South Carolina. The purchase price of the acquisition was $824.6 million consisting of $430.9 million in cash consideration, and $393.7 million of equity consideration. The deal structure allowed the company to save its cash reserves and provides financial flexibility, reducing the need for excessive borrowing. The company appropriately diversified the risks arising from the acquisition with the shareholders of the target company.

Sunshine Fitness Acquisition

| Number of stores |

| # |

| 114 |

| Purchase price |

|

|

| 824.6 |

| Cash |

|

|

| 430.9 |

| Equity |

|

|

| 393.7 |

Furthermore, the acquired stores have excellent profitability. In 2022, the company's annual revenue for the company-owned store segment was $379.4 million, with an incremental effect of $180.8 million attributable to the acquisition. The EBITDA for the company-owned store segment was $142.1 million, and the incremental effect from the acquisition was $78.1 million. Consequently, the EBITDA margin for the acquired segment is calculated to be 43.2%(=$78.1 / $180.8). In comparison, the EBITDA margins for the company-owned store segment in 2022 and 2021 were 37.5% and 29.4%, respectively. The pre-pandemic (before 2020) five-year average EBITDA margin was 39.9%. It is evident that the stores acquired from Sunshine Fitness have higher profitability than the historical and current average, indicating they will contribute positively to cash flows while under the company's ownership and are expected to facilitate a smooth sale in the future.

Lastly, I expect the company's second-quarter financial results, due to be released next week, to be not significantly different from the previous quarter, as the sales and profits have showed a predictable pattern. The company has set a target for 13% to 14% growth in revenue and 17% to 18% growth in EBITDA for 2023. Looking further ahead, their three-year financial targets indicate a low to mid-teens growth rate for revenue and a high teens growth rate for AEBITDA.

In contrast, my revenue and EBITDA estimations, considering my assumption of the business structure change three years from now, suggest a growth rate in the range of 4% to 5%. However, from the perspective of free cash flow, there is much room for improvement and I see an investment opportunity at this point.

In conclusion, I believe that the risks are being overestimated, and the current stock valuation presents a favorable buying opportunity.

For further details see:

Planet Fitness: The King Of An Asset-Light Business