PLTM - Platinum And Palladium: Approaching The Bottom

2023-12-09 09:27:10 ET

Summary

- Platinum and palladium prices have dropped significantly in 2023 due to increased interest rates and reduced investment demand.

- Despite the belief that demand for platinum and palladium will decrease because of larger EV penetration, demand will actually continue to rise.

- Both platinum and palladium are facing supply challenges exacerbated by falling PGM prices and declining profit margins.

- Platinum has the most bullish fundamentals, because of the on-going palladium-to-platinum substitution in catalytic converters, deeper deficits, and a bigger role in the future hydrogen economy.

Platinum and palladium have experienced a significant drop in 2023, with platinum down by 16% and palladium nearly 45%. The increase in interest rates has curtailed investment demand for all precious metals (except for gold, thanks to its status as a reserve asset). The automotive sector (which accounts for 40% of platinum demand and almost 80% of palladium demand) has also seen its demand restrained due to higher interest rates. Moreover, the growing prevalence of battery electric vehicles (BEVs) has led to a widespread belief that the world will need less platinum and palladium in the future.

Prices of platinum, palladium and rhodium (last 12 months) (matthey.com)

{kind=link}

Demand picture

The reality is very different. Demand for both platinum and palladium is projected to continue to rise in the coming years. The World Platinum Investment Council (WPIC) estimates that palladium demand will remain fairly stable over the next four years, moving from 9,715 kOz in 2022 to 9,985 kOz in 2027. Platinum, on the other hand, is expected to see a more significant increase in demand, from 6,401 kOz in 2022 to 8,705 kOz in 2027.

{kind=link}

{kind=link}

Supply picture

When it comes to supply, both palladium and platinum are facing serious challenges. The two metals are inextricably linked, as platinum and palladium are co-products in polymetallic ores, typically found alongside other platinum-group metals (PGMs), including rhodium, as well as gold, nickel, and copper. As a result, PGMs producers are exposed to a wide range of commodities. Miners often report revenue and all-inclusive sustaining costs for an entire group of metals (such as the so-called 4E PGMs, which include platinum, palladium, rhodium, and gold, while 6E PGMs also include osmium and ruthenium). The prices of PGMs have decreased rapidly , with rhodium in particular dropping by 65%.

Even though platinum has not depreciated as much, the economics of mining it have drastically changed. Platinum production is primarily concentrated in South Africa, where the Bushveld Igneous Complex accounts for three-quarters of total production. Russia is the second-largest producer, contributing 15%, with the remainder made up by Zimbabwe, Canada, and the U.S. In South Africa, an energy crisis, labor strikes, political instability, and inflation have driven costs up. At the same time, prices have declined, thereby compressing profit margins. In fact, many operations are no longer commercially viable at current prices. This has compelled platinum-group miners to reduce capital expenditures and even suspend some operations. Consequently, platinum supply is expected to decline disproportionately in relation to its price drop.

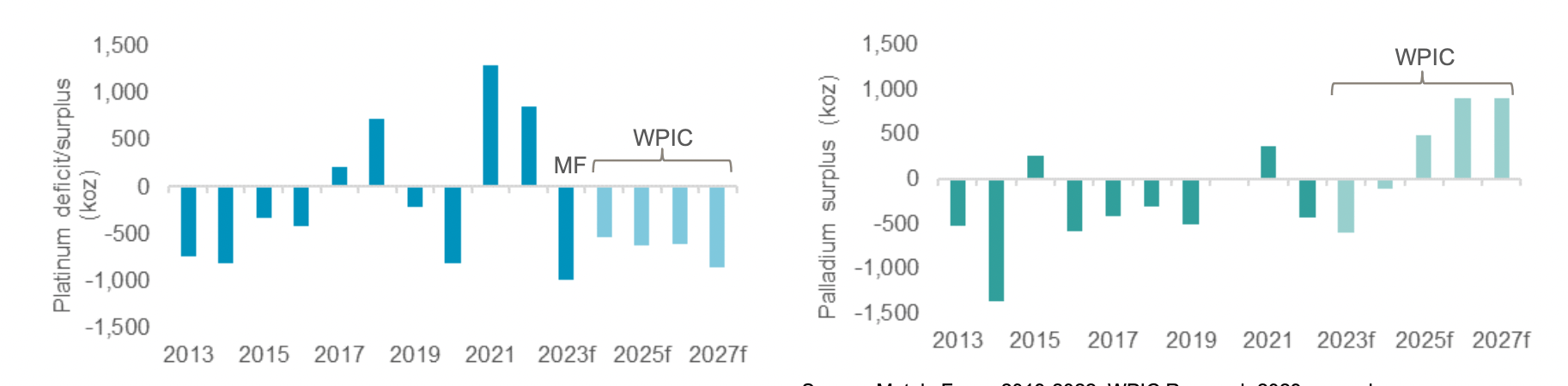

Record market deficits

In 2023, platinum is forecasted to face a deficit of about 1 million ounces. To silver and gold investors, this quantity may not seem significant, but it's worth noting that platinum is a much rarer metal. Total annual production is around 7 million ounces, with mining accounting for about 5.5 million ounces and the rest coming from recycling. This year's deficit is actually the largest on record since the 1970s. The deficit is projected to moderate next year, but it will then intensify again, reaching 851 kOz by 2027. In contrast, palladium is predicted to shift to a surplus starting from 2025, reaching 897 kOz by 2027, due to a 1.2 MOz increase in palladium recycling supply between 2022 and 2027.

Platinum forecast to move into market deficit from 2023 (Platinum Essentials (WPIC))

{kind=link}

Platinum and palladium substitution dynamics

Currently, platinum and palladium are mostly used in auto-catalysts for reducing vehicle emissions. The two metals are almost interchangeable in catalytic converters. The relative proportion of the two metals is determined during the development of a new vehicle model's emissions control system, based on their relative prices. This proportion is then locked in for the lifetime of that vehicle model (on average, seven years). This means that the substitution process between the two metals takes an extended period of time to manifest. Historically, platinum was the more expensive metal, which explains why palladium began to replace it. Now, the reverse process is happening. In fact, the price differential between platinum and palladium has already significantly narrowed. I expect this trend to continue until the prices reach parity, triggering the opposite dynamics.

{kind=link}

In addition to platinum-to-palladium substitution in automotive applications, there are other reasons to be more bullish on platinum. The platinum market is currently tighter and, importantly, platinum is anticipated to play a significantly larger role than palladium in the green energy transition, thanks to its use in fuel cells. Unlike platinum, palladium is not utilized in fuel-cell electric vehicles (FCEVs) due to its lower catalytic activity at the operating temperatures found inside proton-exchange membrane fuel cells. Unless there's a significant technological shift, platinum is the greener metal.

The platinum-to-palladium substitution will therefore continue until platinum prices rise above palladium. This is projected to happen around 2025, according to the World Platinum Investment Council (WPIC), based on current trends. At this point, the substitution of palladium for platinum in catalytic converters will commence and the price differential may begin to narrow again.

Palladium substitution for platinum will start from 2025 (Platinum Essentials (WPIC))

{kind=link}

How to invest

The Sprott Physical Platinum and Palladium Trust ( SPPP ) is a closed-end trust that invests in unencumbered and fully-allocated physical platinum and palladium. Its aim is to provide a liquid and convenient investment vehicle for investors wishing to hold physical platinum and palladium. The trust shares many characteristics with other Sprott trusts that are backed by physical gold and silver. Investing in an exchange-traded product is particularly sensible for platinum and palladium, considering the markup for buying platinum and palladium coins and bullion is higher than for gold and silver. The trust is also redeemable for metals, subject to certain conditions . The Management Expense Ratio is 1% per annum, which, though relatively high, can be attributed to the relative illiquidity compared to other precious metals.

Concluding remarks

Overall, both platinum and palladium have several secular tailwinds. I expect them to benefit from both their precious metal status and growing industrial applications. Long-term, I am bullish on both metals. However, I maintain a preference for platinum due to its higher correlation with gold prices and its unique role in the future hydrogen economy.

While the medium- and long-term fundamentals for platinum and palladium are bullish, the key question remains: have they already bottomed out? I believe the answer is no. Demand from the hydrogen sector is expected to be a significant source of marginal demand, but this is still several years away. In the meantime, higher interest rates and sluggish global growth are likely to continue to put pressure on prices. The significant deficits in the platinum and palladium markets might not have an immediate impact. For instance, platinum was also in a deficit from 2013 to 2016, and prices nearly halved during that period. Platinum and palladium may experience further declines from here, or consolidate at current levels for some time, before the fundamentals begin to take effect. However, investors with long-term horizons may not be concerned with timing the exact bottom of the cycle. They are likely to be well rewarded by investing at current prices.

For further details see:

Platinum And Palladium: Approaching The Bottom