PLXS - Plexus: Hold Or Explore Alternatives

2023-12-07 16:31:42 ET

Summary

- Plexus achieved record annual revenue of $4.21 billion and 5.2% operating margin in FY2023, a remarkable milestone after 15 years.

- However, Plexus warns of revenue declines and softness in some segments for FY2024, facing challenges and uncertainties.

- Considering its risk-reward profile, we think that there are other EMS companies that offer better investment potential at the moment.

Investment Thesis

FY2023 was a great year for Plexus ( PLXS ). The company reported record annual revenue of $4.21 billion (10% YoY) and 5.2% non-GAAP operating margin. This achievement of double-digit revenue growth with greater than 5% operating margin was the first time in 15 years which is a remarkable milestone. This was also a significant progress toward its FY2025 goal of reaching $5 billion in revenue and 5.5% non-GAAP operating margin.

However, not everything is rosy for Plexus as the company is warning of revenue declines in FY2024, and softness in some of its segments. The company faces some challenges and uncertainties that could affect its future performance and valuation. In this report, we will examine the company's financial results, growth prospects, and valuation and compare them with some of its peers in the EMS industry. We will also provide our opinion on whether Plexus is a good investment opportunity or not.

Company Overview and Segment Performance

Plexus Corp. is a mid-cap company providing electronic engineering and manufacturing services to its customers in healthcare, industrial, aerospace and defense markets. The company operates in the EMS market, known for its high competition, low margins and cyclical nature. Plexus is aiming to stand out in this tough market by delivering highly complex products that have strict regulatory requirements. It operates through three segments: healthcare/ life sciences, industrial and, aerospace/defense.

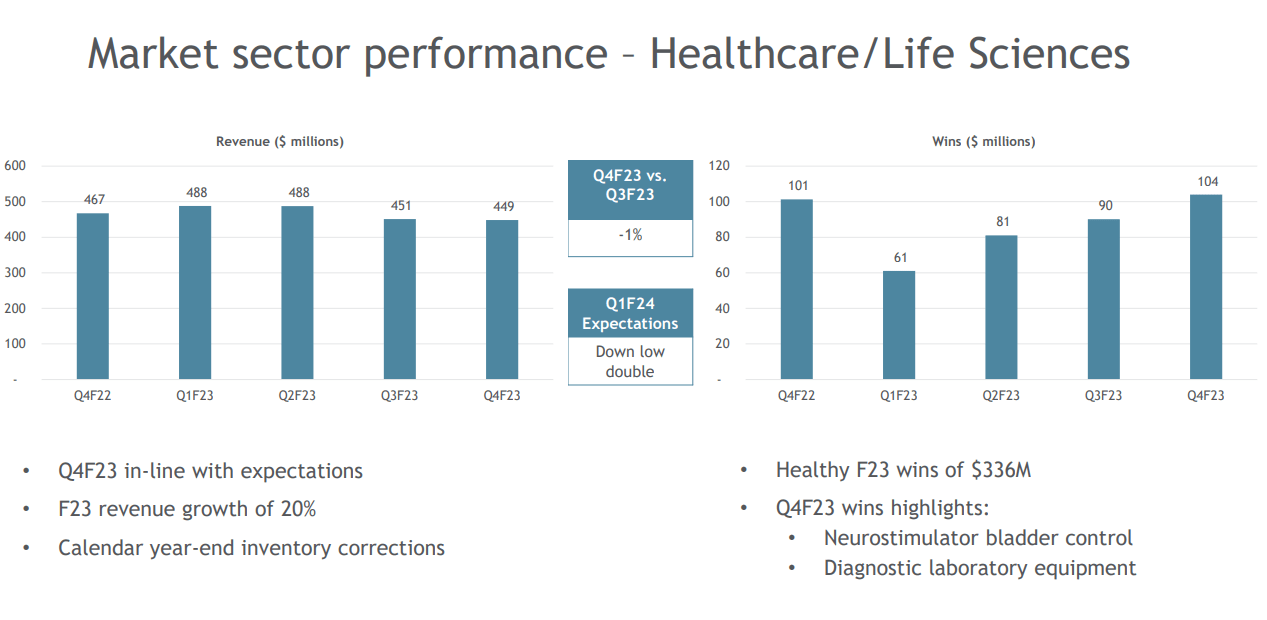

Plexus's healthcare and life sciences segment is its largest segment and offers solutions for medical devices, drug delivery systems, diagnostic equipment, and other healthcare products. The segment accounts for 46% of the company's revenue and had 20% YoY growth in FY2023. This segment is subject to some headwinds as management is guiding for double-digit revenue declines for FY2024 Q1 (see below).

Plexus Healthcare / Life Sciences Segment (Plexus FY2023 Q4 Earnings)

{kind=link}

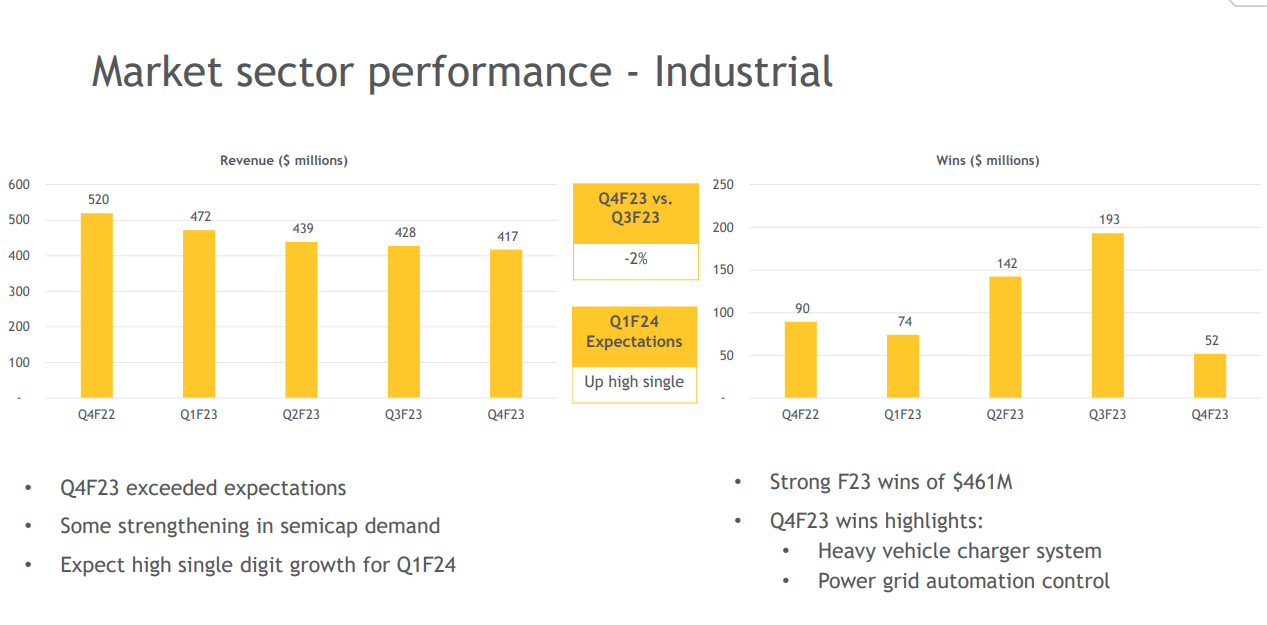

Plexus's industrial segment provides solutions for industrial automation, robotics, energy, transportation, and other industrial products. The segment accounts for 41% of the company's revenue and is expected to grow high single digit in FY2024 Q1 (see below)

Plexus Industrial Segment (Plexus FY2023 Q4 Earnings)

{kind=link}

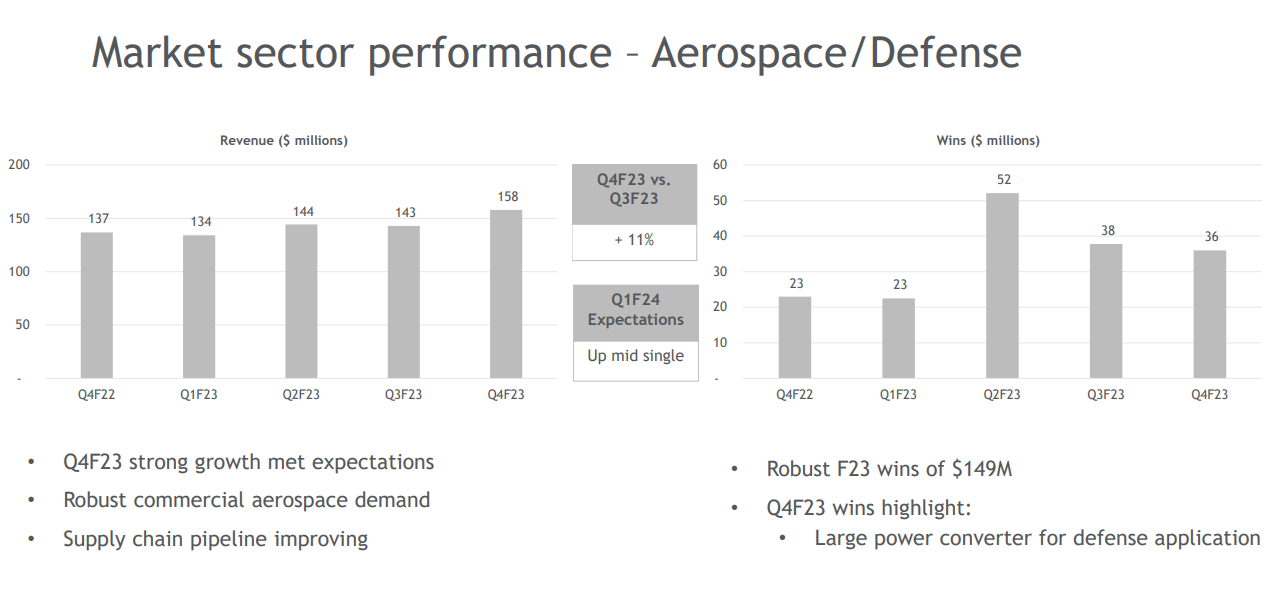

The aerospace and defense segment is the smallest segment of Plexus, contributing 13% of its revenue. It had 11% growth in FY2023 Q4. For FY2024 Q1, the segment is expected to grow at a moderate single-digit rate (see below).

Plexus Aerospace / Defence Segment (Plexus FY2023 Q4 Earnings)

{kind=link}

Plexus vs Other EMS Players

Now, we will compare the segment performance of Plexus with other major EMS players.

The EMS industry is seeing strong growth in Aerospace/Defense and Industrials, as shown by Plexus' segment results. These two segments are benefiting from secular trends, and most EMS companies are gaining from them. Plexus also has a strong position in these two segments and is expected to keep growing. However, we think that Plexus is facing competition in Healthcare, which is its biggest segment (45% of revenue)

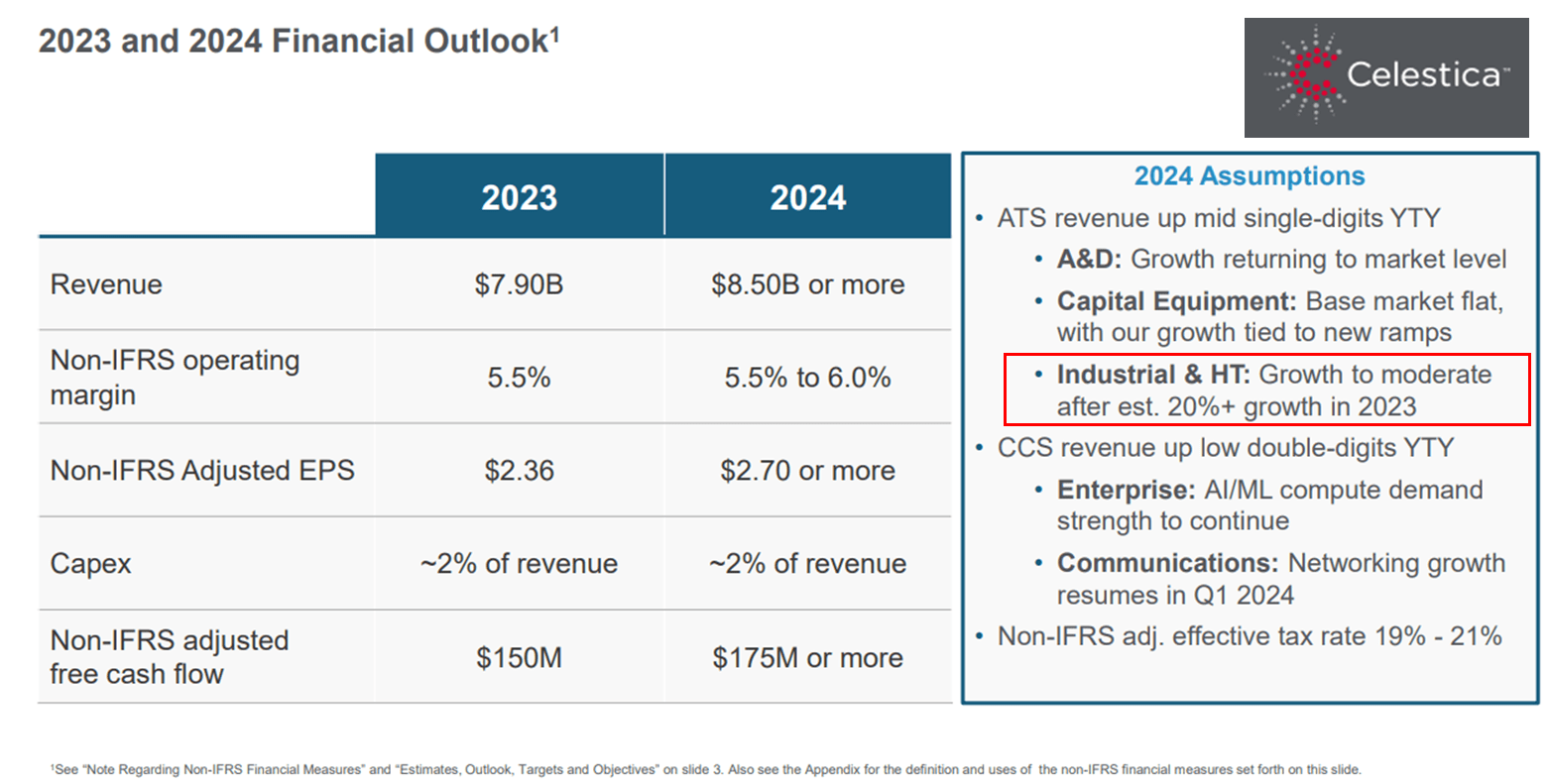

For example, when we look at Celestica's ( CLS ) Healthcare Tech segment, we can see 20%+ growth for FY2023 and positive growth guidance for FY2024 (see below) Unlike Plexus, Celestica also expects to improve its revenue and non-GAAP operating margin in 2024 (see below).

Celestica FY2024 Guidance (Celestica Virtual Investor Meeting)

{kind=link}

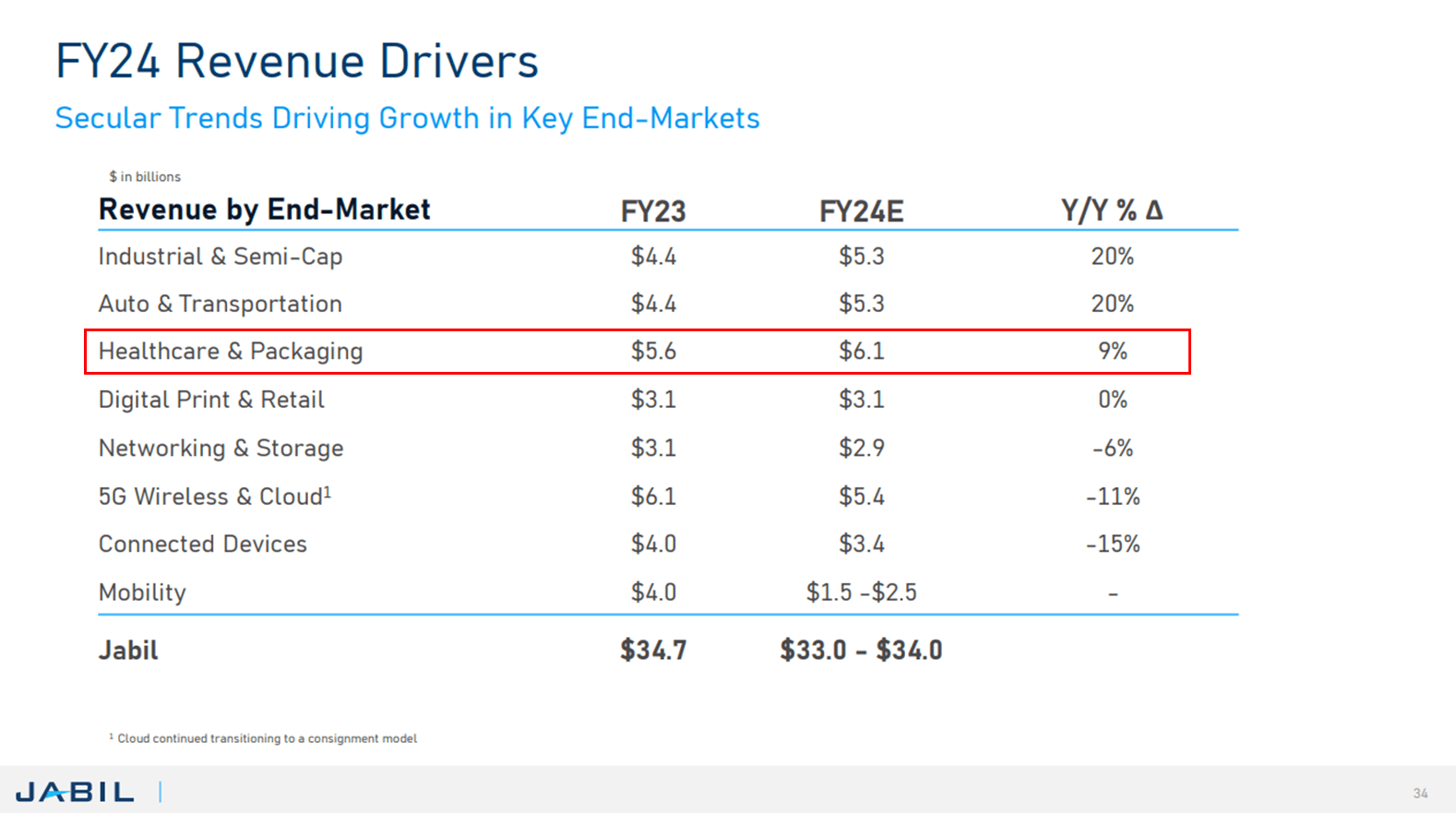

Also for Jabil ( JBL ) which is another key player, we can see it is guiding for higher YoY revenue for its Healthcare segment. Its segment is expected to grow by 9% YoY in FY2024. Although the company issued a guidance cut last week, we still think they will have positive Healthcare segment revenue growth in FY2024. Jabil also expects to grow its operating margin in FY2024 (see below).

Jabil FY2024 Guidance (Jabil FY2023 Q4 Earnings)

{kind=link}

We believe that Jabil and Celestica have more resilient portfolio of end-markets than Plexus and are better positioned to mitigate segment slowdowns. Plexus, on the other hand, may face more challenges in maintaining its growth and profitability due to its cyclical nature.

Financials - Revenue and Operating Margin Stalling

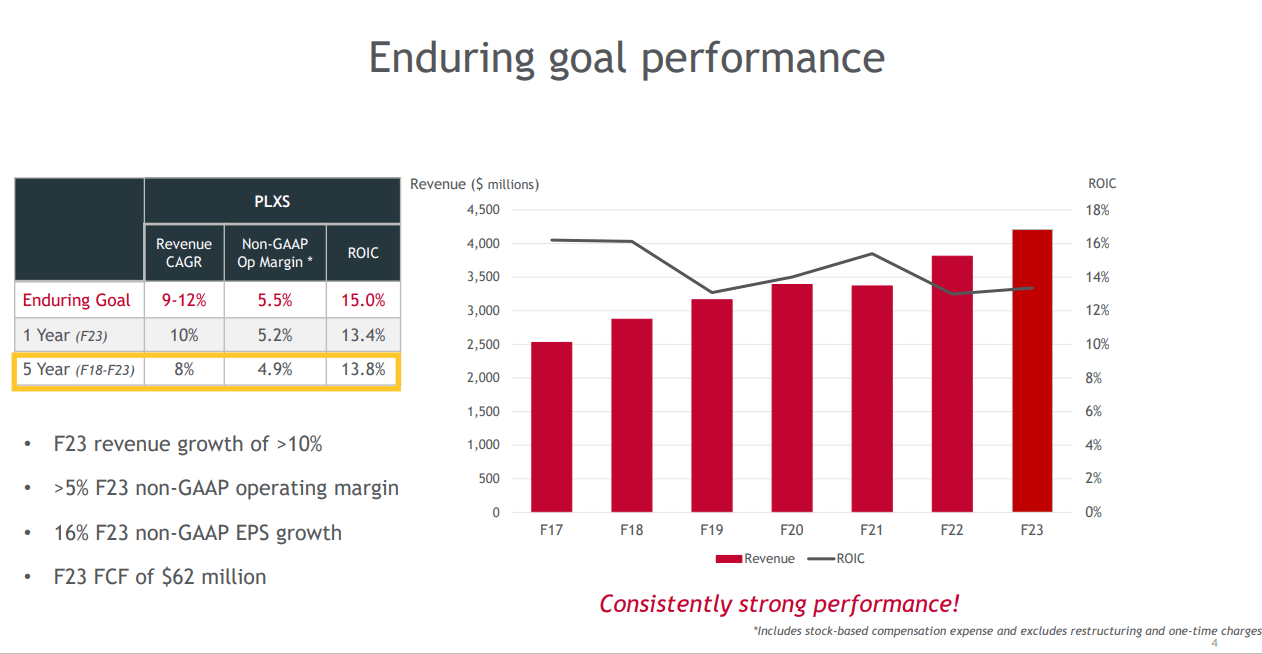

Plexus long-term goal is to achieve a 9-12% annual revenue growth rate while producing a ROIC of 15%. The company aims to achieve a positive economic return, which means to deliver a higher ROIC than its WACC (which is around 9% ). See the company's long term goals below.

Plexus FY2025 Goals (Plexus FY2023 Q4 Earnings)

{kind=link}

For the fiscal year 2023, the company produced a ROIC of 13.4%, which was below the target of 15%. The non-GAAP operating margin and revenue growth rate were 5.2% and 9.7%, respectively, which were within the company's long-term goals.

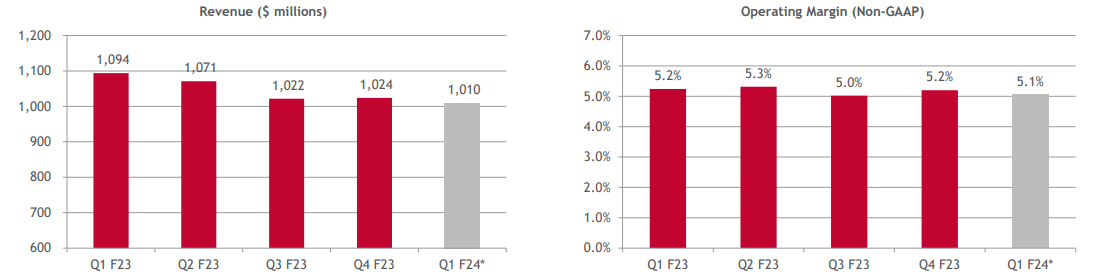

However, the quarterly revenue and operating margin trends raise some doubts about Plexus' ability to sustain its growth and profitability in the future quarters. Both the revenue and operating margin dropped from Q3 to Q4 in FY2023, and the outlook for Q1 in FY2024 suggests a further decrease (see below). We think that this shows that Plexus does not have the same diversification and resilience as some of its competitors, and may risk losing market share and customer loyalty over time. Also, we believe that the company is finding it hard to increase its operating margins, which is another indication of competitive pressure.

Plexus Revenue and Margin Guidance (Plexus FY2023 Q4 Earnings)

{kind=link}

Healthy Balance Sheet

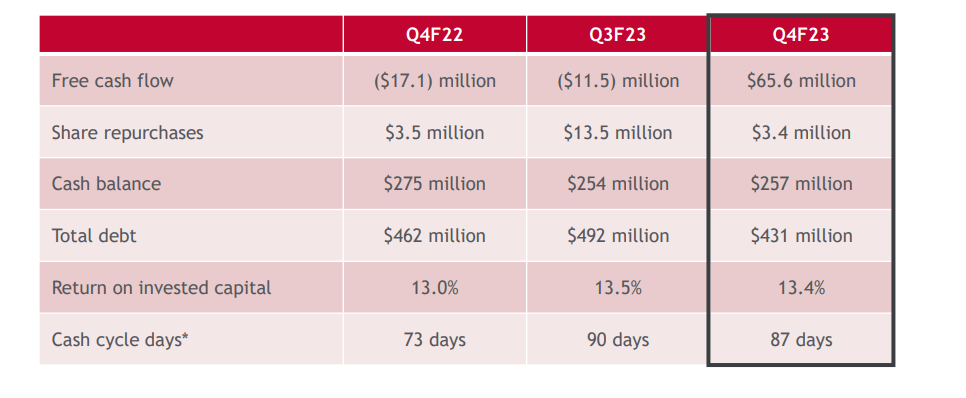

Plexus has a moderate leverage and a strong liquidity position, as shown by its balance sheet. The company holds $257 million in cash and owes $431 million in total debt (see below). Compared to its peers, Plexus has a lower total debt-to-equity ratio of 39%. The company can also meet its debt obligations, as its interest coverage ratio is 6.5. The company's current ratio of 1.47 is close to the industry averages, indicating that it has enough current assets to pay its current liabilities. We think that the company's debt level is manageable and that it has sufficient cash to support its operations and growth initiatives.

Plexus Balance Sheet (Plexus FY2023 Q4 Earnings)

{kind=link}

Relatively High Valuation

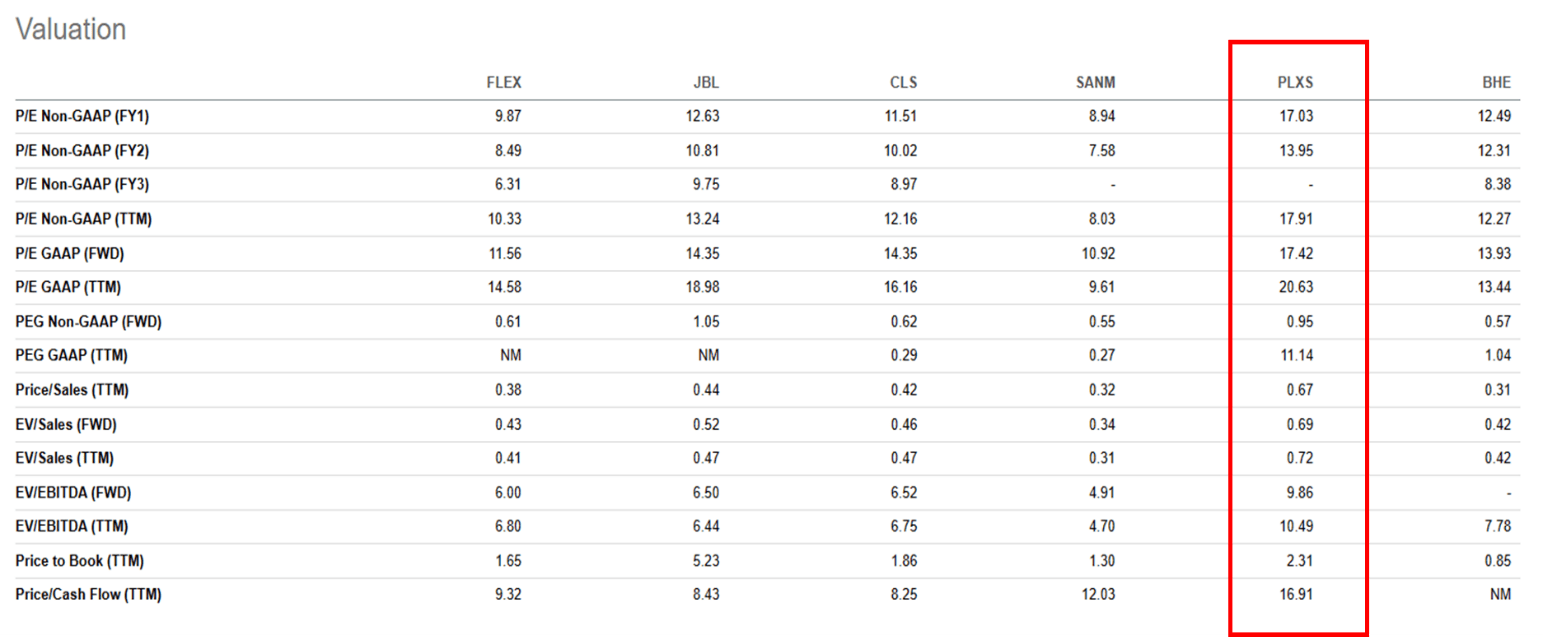

Plexus has a higher valuation than its EMS peers, as its Forward P/E ratio is 17 times earnings (see below). We do not see any justification for this multiple, given the company's weak outlook. The company's revenue growth is stalling, and its operating margins are falling behind its competitors. The company's guidance for the fiscal first quarter 2024 also reflects a lack of confidence in its near-term prospects.

EMS Peers Valuation Comparison (Seeking Alpha)

{kind=link}

Our analysis shows that Plexus is overvalued compared to its rivals.

Conclusion

Plexus delivered a solid performance in fiscal 2023, with record revenue and 5.2% operating margins. However, Plexus faces some headwinds in the near term and expects its revenue to decline sequentially in Q1 FY2024, reflecting lower demand from some of its segments. The company also anticipates its non-GAAP operating margin to decrease implying competitive pressures.

We believe Plexus can benefit from the long-term growth opportunities in its target markets, but we also acknowledge the near-term risks that could affect its financial performance and stock price. Considering its risk-reward profile, we think that there are other EMS companies that offer better investment potential at the moment.

We maintain a neutral stance on Plexus.

For further details see:

Plexus: Hold Or Explore Alternatives