XLV - Pliant Therapeutics: Trading In Oversold Territory Buying The Dip

2023-05-23 08:35:26 ET

Summary

- Undervalued: the stock is currently in the oversold territory after some investors over-reacted and sold after the Phase 2 BEXO trial, we like the FVC slow down and clean safety data.

- Promising Upcoming Trials: The mid-2023 Phase 2b BEACON-IPF trial could act as a significant positive catalyst for the stock, potentially meeting the FDA's criteria for a pivotal registration trial.

- Robust Financial Health: Despite a Q1 net loss of $37.5MM, largely tied to increased OpEx, Pliant's solid cash position of $577MM should underpin clinical activities through 2H26.

- We uphold our buy rating for PLRX stock due to the overlooked clinical benefits of BEXO, the upcoming BEACON-IPF trial potential, and robust financial health.

Q1 earnings and update to our thesis

Pliant Therapeutics ( PLRX ) reported Q1 earnings on May 9th; in light of Pliant Therapeutics' latest financial performance and clinical developments, we maintain a buy rating on the stock. The company's 1Q23 earnings report showed a net loss of $37.5m, largely due to increased OpEx. However, the reported cash position of $577m is expected to support the company's operation 2H26 (considering their quarterly OPEX burn of around $30-40m), underscoring the company's robust financial health.

Oversold after Phase 2 data

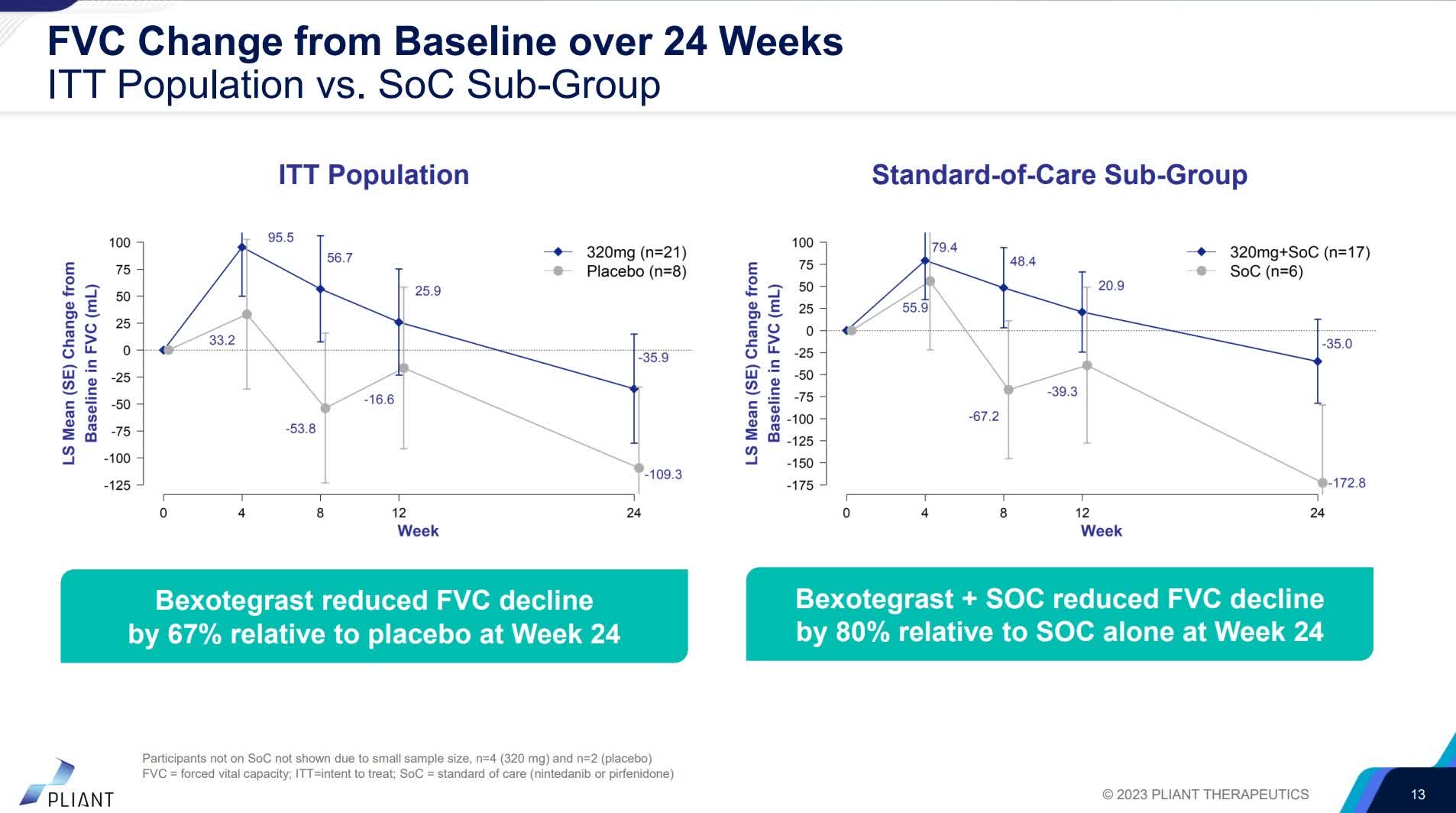

PLRX's valuation has seen a significant decline post the Phase 2 data for its 320MG BEXO (bexotegrast) in Idiopathic Pulmonary Fibrosis ((IPF)). Despite an apparent undershoot in absolute FVC (Forced Vital Capacity) values, the data still demonstrate a trend of lesser decline versus placebo. Moreover, around half of the patients on BEXO displayed FVC improvements from baseline, contrasting with all placebo patients showing FVC decline. This indicates a potential slowing of disease progression, which is further reinforced by a reduction in cough severity, an independent predictor of disease severity/mortality.

Considering that current standard of care such as Ofev only slows down the disease progression by 50%, anything superior to a 50% rate of decline should be a win for Pliant, albeit the drug did not show an "absolute improvement" like the previous data readout.

{kind=link}

Phase 2 IPF data (Pliant company presentation.)

While investors may be wary of the valuation dip, we argue that the stock is oversold. The market seems to have overlooked the sustained FVC benefit and excellent safety profile of BEXO from the 24-week IPF data. Furthermore, we believe the Phase 2b BEACON-IPF trial, starting in mid-2023, could provide a significant positive catalyst for the stock. This trial may meet the FDA's criteria for one of two required positive pivotal trials for registration, which will provide a clear path for approval which would be important for the market to build conviction on the candidate moving forward. PLRX expects significant clinical advancements, including the INTEGRIS-PSC topline data in 3Q23 and the initiation of a Phase 2b BEACON-IPF trial in mid-2023. These anticipated milestones could dramatically impact the company's valuation and quickly change the sentiment.

Risks

-

Clinical Trial Uncertainties: Pliant's future largely depends on the outcomes of their upcoming clinical trials, such as the BEACON-IPF trial for bexotegrast. Any unfavorable results, unexpected side effects, or failure to meet endpoints could significantly hamper the company's prospects and impact the stock price.

-

Regulatory Risks: The potential for regulatory approval delays or rejections is a critical risk. Specifically, the FDA's and EMA's acceptance of the BEACON-IPF trial as one of the two pivotal trials required for registration is not guaranteed. If the agencies reject this proposition, Pliant's path to market may be longer and more costly than anticipated.

-

Cash Burn Rate: Despite having a robust cash position, Pliant's high operational expenditures could pose a risk if its clinical trials extend beyond anticipated timelines or the company fails to secure additional funding. Increased expenditures without a corresponding revenue stream could exhaust the company's cash reserves and require further capital raising.

Conclusion

Net-net, we uphold our buy rating despite initial investor apprehension following a valuation dip after Phase 2 data on BEXO in IPF. We perceive the stock as oversold. The overlooked FVC benefits and clean safety profile of BEXO, coupled with the potential of the upcoming Phase 2b BEACON-IPF trial, underscores our confidence in Pliant's prospects. While clinical risk remains especially considering the company is pursuing IPF (notorious biotech graveyard indication), we anticipate that Pliant's forthcoming clinical milestones could profoundly shift the company's valuation and market sentiment. Furthermore, we find the firm's sturdy cash position of $577MM, which is enough to fuel clinical advancements until 2H'26, reassuring and believe short-term dilution due to public offering is a low probability event.

For further details see:

Pliant Therapeutics: Trading In Oversold Territory, Buying The Dip