BE - Plug Power - Running Out Of Funds And Non-Dilutive Financing Options

2024-01-03 10:36:25 ET

Summary

- Massive losses from operations and elevated capital expenditures have resulted in a severe liquidity crunch.

- Without raising additional capital, the company might run out of funds in the current quarter.

- Proposed, strict guidelines for claiming green hydrogen production tax credits could severely impact Plug Power's ambitious green hydrogen production and electrolyzer sales plans.

- Given the company's low debt levels and a number of equity-linked financing options, I do not expect Plug Power to file for bankruptcy anytime soon but near-term survival will likely come at the expense of massive dilution for existing shareholders.

- Considering the dismal state of the company's operations and the high likelihood of substantial, near-term dilution, investors should sell existing positions and wait for management to stabilize the ailing company and finally start executing on its promises.

Note:

I have covered Plug Power Inc. ( PLUG ) previously, so investors should view this as an update to my earlier articles on the company.

Liquidity Crunch And Going-Concern Warning

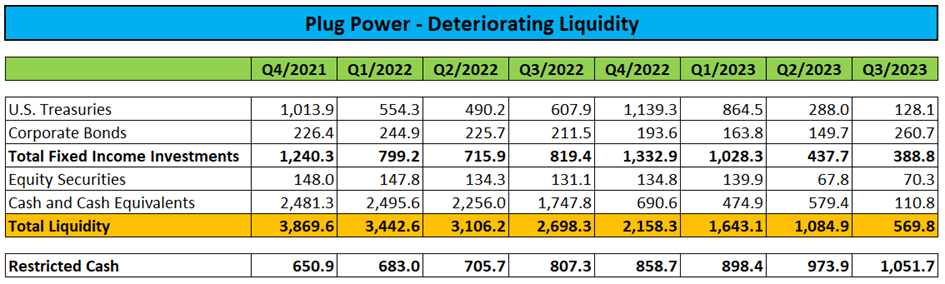

In early November, Plug Power reported another set of abysmal quarterly results with revenue missing consensus expectations by a mile and consolidated gross margin deteriorating to new multi-year lows.

The toxic combination of massive losses from operations and elevated capital expenditures as well as the ongoing requirement to provide substantial cash collateral for sale-and-leaseback transactions has resulted in the company's liquidity deteriorating by an eye-watering $3.3 billion since the beginning of 2022.

{kind=link}

At the end of Q3, available liquidity was down to approximately $570 million. Without raising additional capital, Plug Power might run out of available funds later this quarter.

In fact, the issue required management to include a going concern warning in the company's quarterly report on form 10-Q.

Analysts Losing Faith

In recent weeks, a number of Tier 1 investment banks have downgraded the stock including Morgan Stanley and Citigroup due to concerns regarding the company's ongoing execution issues and substantial, near-term liquidity needs.

Following Plug Powers Q3 report, Roth MKM analyst Craig Irwin stated the company's immediate capital needs at " sizably above $500 million " very similar to Citigroup's Vikram Bagri.

Similar to many sell-side analysts, I decided to no longer give management the benefit of the doubt and downgraded the company's shares to "Sell" in November after years of keeping a "Hold" rating on the stock.

Strict Draft Guidelines For Green Hydrogen Production Tax Credits

Adding insult to injury, the U.S. Treasury's recently published draft guidelines for claiming green hydrogen production tax credits revealed much stricter than originally anticipated requirements last week.

In fact, guidelines for calculating lifecycle emissions are now set to include some of the most controversial rules around the usage of zero-carbon electricity: additionality, geographical correlation, and hourly matching.

- Additionality requires green hydrogen being produced from new renewable energy projects.

- Geographical correlation requires the source of renewable energy to be close to the green hydrogen production facility.

- Hourly matching or temporal correlation relates to how frequently producers would have to prove that their electrolysers have been powered by 100% renewable energy (usually hourly, weekly, monthly or annually) and therefore to what extent they can use grid electricity at times when renewable energy sources aren't available, and then send the same amount of renewable energy back to the grid at a later date.

If finalized in the proposed form, the guidelines would provide a severe blow to the company's ambitious green hydrogen production and electrolyzer sales plans.

Near-Term Financing Options

However with the company's first green hydrogen plant in Georgia now already twelve months behind schedule amid a near-doubling of capital expenditures and remaining liquidity depleting fast, management will have to secure additional financing as soon as possible.

According to statements made in the Q3 shareholder letter , the company is pursuing a number of financing solutions:

- Corporate debt financing.

- Project financing and plant equity partnerships.

- A loan guarantee by the U.S. Department of Energy ("DOE").

Please note that at this point, Plug Power only carries approximately $200 million in long-term debt with the vast majority comprised of the company's 3.75% convertible notes maturing on June 1, 2025.

However, the 10-Q lists approximately $1 billion in lease and finance obligations mostly related to sale-and-leaseback transactions of equipment leased to material handling customers which are almost fully collateralized by restricted cash and security deposits (emphasis added by author):

Restricted Cash

In connection with certain of the above noted sale/leaseback agreements, cash of $539.4 million (...) was required to be restricted as security as of September 30, 2023 (...), which restricted cash will be released over the lease term. As of September 30, 2023 (...), the Company also had certain letters of credit backed by security deposits totaling $426.9 million (...), of which $396.2 million (...) are security for the above noted sale/leaseback agreements, and $30.7 million (...) are customs related letters of credit.

As of both September 30, 2023 and December 31, 2022, the Company had $76.7 million held in escrow related to the construction of certain hydrogen plants.

With that being said, let's look into the company's options in more detail:

1. Corporate Debt Financing

On the conference call , CFO Paul Middleton pointed to " expressions of offers " from financial institutions for " ABL-like facilities " and " restricted cash advance facilities ".

Indeed, asset-backed lending could be an option, particularly when considering the company's seemingly ever-increasing inventory levels:

{kind=link}

However, potential lenders are likely to struggle with appraising the liquidation value of the company's inventory, particularly when it comes to work-in-progress or finished goods but even raw materials and supplies could be an issue with the company only serving a small niche in the material handling equipment market with a fairly limited number of customers.

Given this issue, any potential inventory financing would likely be well below the usual 50% rate.

Leveraging Plug Power's restricted cash might be a more viable option as the company has already executed on a similar transaction in the past albeit at a much smaller scale with the loan being repaid from releases of the company's restricted cash over the term of the underlying sale-and-leaseback transactions.

{kind=link}

However, in addition to placing a lien on basically all of the company's assets, the lender required the company " to maintain at all times minimum unencumbered cash and cash equivalents equal or greater than the then outstanding principal balance " of the credit facility thus virtually eliminating any residual risk while charging a whopping 12% interest rate in a very low interest environment.

Considering the current interest environment, Plug Power would likely have to pay interest rates north of 15% for a similar facility today, particularly as the company wouldn't be able to comply with onerous covenants like the one discussed above.

2. Project Financing / Plant Equity Partnerships

Quite frankly, with the company having delayed its green hydrogen plant roadmap several times already and Plug Power's very first facility in Georgia still not being operational, this does not appear to be a viable short-term option.

In addition, selling equity in green hydrogen plants not anticipated to come online before 2025 doesn't look feasible either, particularly not in case the above-discussed draft guidelines being finalized without major changes.

At least in my opinion, the company would have to provide evidence that their plants are indeed working at the proposed scale and generating returns in line with management's projections before potential investors might consider stepping in.

However, without meaningful production tax credits, some of the plants currently under construction might see further delays or won't even be completed.

According to a recent news article , without a $1.5 billion loan guarantee commitment by the Department of Energy, Plug Power won't spend additional money on its New York green hydrogen plant at this time.

3. DOE Title XVII Loan Guarantee

According to CFO Paul Middleton on the Q3 conference call , the company hopes to secure conditional approval for a $1.5 billion DOE Title XVII loan guarantee " that would fund our green plants (...) from construction phase onwards" by the end of the year with funding anticipated in late Q1 or early Q2/2024.

However, this would be well behind previously-communicated expectations. Moreover, a time frame of just three months between the DOE's conditional commitment and funding looks overly ambitious again.

For example, Eos Energy Enterprises, Inc. ( EOSE ) received an approximately $400 million conditional commitment from the DOE in late August with funding not expected before Q2/2024 despite the company's zinc battery plant expansion project appearing far less complex relative to Plug Power's ambitious green hydrogen facility ramp-up plans.

Remember also that this would be project-based financing which can't be utilized for covering outsized operating losses from the company's ailing material handling business.

Other Options - Equity or Equity-Linked Securities

With the financing options outlined by management either not viable, prohibitively expensive or simply taking too long to materialize, Plug Power will likely have to resort to raising additional equity or issuing convertible debt.

1. Equity

Even with the share price near multi-year lows, the company's market capitalization remains around $3 billion, still more than sufficient to pursue an equity offering.

That said, raising between $500 million and $1 billion in an underwritten offering would be very difficult, particularly as potential Tier 1 underwriters are likely to pass on the offering this time given the company's track record and ongoing, elevated execution risk.

Establishing an " At-The-Market Equity Distribution Agreement " or "ATM-Agreement" similar to Nikola Corporation ( NKLA ) or FuelCell Energy, Inc. ( FCEL ) looks like a more viable option but the company's ability to raise a sufficient amount of funds in due time from selling a large number of shares into the open market will largely depend on trading volume.

However, with market participants' risk appetite on the rise and the stock up significantly from recent multi-year lows, the company should seriously consider working with leading investment banks to establish a large-scale ATM facility.

2. Convertible Debt

While certainly an option, a large-scale convertible notes offering would also be likely to put major pressure on the share price as evidenced by the sell-off in Rivian Automotive, Inc.'s ( RIVN ) common shares in connection with the company's 1.5 billion green convertible notes offering in early October.

As many convertible debt buyers tend to employ delta-neutral convertible arbitrage strategies which require establishing a corresponding short position in the underlying shares, the stock price would very likely take another hit upon announcement.

In addition, given the dismal state of the company's operations, terms are likely to be ugly.

Plug Power could also pursue an approach similar to Nikola Corporation by issuing debt to specialized hedge funds which would be convertible into common shares at a discount to prevailing market prices at the lender's option.

As a result, the lender would be incentivized to establish a short position in the company's common shares and subsequently issue a conversion notice to cover the position with discounted shares issued by the company.

Similar to the above-discussed ATM-Agreement, this type of financing would likely result in ongoing pressure on the company's shares as convertible noteholders maximize their profits by shorting as many common shares as possible.

3. Convertible Preferred Stock

Issuing convertible preferred stock would be very similar to selling convertible debt to a specialized lender with the slight difference that preferred equity is ranking lower in the company's capital structure and repayments are often required on a monthly basis.

Monthly installments are usually made in newly issued common shares with preferred equity holders accordingly incentivized to establish a short position in the company's common shares ahead of these dates.

The company has issued convertible preferred stock in the past, albeit at much smaller scale.

Other Options - Factoring

Similar to Bloom Energy Corporation ( BE ), Plug Power could enter into factoring agreements with financial institutions and sell an eligible part of its receivables on a regular basis. However, with a rather modest accounts receivable balance of $163.2 million at the end of Q3, proceeds from potential factoring agreements would be insufficient to cover the company's short-term financing needs.

Bottom Line

For my part, I do not expect Plug Power to enter into asset-backed lending facilities due to prohibitive terms including the likely requirement to collateralize substantially all of the company's assets.

Gaining access to project financing or selling stakes in some of Plug Power's yet-to-be-constructed green hydrogen plants isn't a viable near-term option either as potential lenders/buyers are likely to require evidence of the company's technology working at the proposed scale and generate returns at least in line with management's projections.

While a massive DOE loan guarantee would certainly be great news for the faltering build-out of the company's green hydrogen capacity, Plug Power would be precluded from utilizing these funds for covering outsized losses from operations in the core material handling business.

In addition, funding of a DOE-backed loan is not likely to happen within the time frame projected by management.

With remaining liquidity depleting quickly, Plug Power will likely have to revert to issuing equity-linked securities or outright selling new equity.

At this point, I would expect the company to utilize a near-term funding approach very similar to Nikola Corporation with a combination of open market share sales and convertible debt issuances.

Given the company's low debt levels and a number of viable near-term financing options, I do not expect Plug Power to file for bankruptcy anytime soon but near-term survival will likely come at the expense of massive dilution for existing shareholders.

Considering the dismal state of the company's operations and the high likelihood of substantial, near-term dilution, investors should sell existing positions and wait for management to stabilize the ailing company and finally start executing on its promises.

Risk Factors

With the U.S. stock market back near all-time highs amid expectations of lower interest rates next year, risk appetite among investors has increased exponentially in recent weeks thus benefiting highly speculative stocks like Plug Power.

In the current environment, even minor news could provide additional fuel to the recovery rally in the beaten down shares, not too speak of real catalysts like a large-scale DOE loan guarantee commitment.

Should management succeed in securing sufficient near-term financing without major dilution, the stock would likely get a further boost.

For further details see:

Plug Power - Running Out Of Funds And Non-Dilutive Financing Options