PLYM - Plymouth Industrial: A Quality REIT With A Debt Profile Waiting To Unfold (Rating Downgrade)

2023-08-08 05:26:32 ET

Summary

- Despite recent outperformance, shares in Plymouth Industrial still trade at a forward multiple that is well below its peers in the industrial sector.

- A higher debt load is one reason shares have commanded a discount.

- In recent news, however, the company announced that they would redeem all their outstanding preferred shares. The effect of this would be a reduction in total leverage.

- While I view PLYM stock favorably, I believe the recent run-up warrants a pause on any new or further initiation.

Plymouth Industrial ( PLYM ) has outperformed much of their peer set on a YTD basis. The company benefits from a unique geographic footprint that includes key logistical hubs, which are likely to see continued growth due to recent nearshoring trends.

Rents have grown accordingly, and occupancy levels remain at peak levels. The company is also making positive progress in their development pipeline. Following the recent run-up in shares, management opportunistically capitalized on favorable stock pricing for an equity raise, the purpose of which was to redeem their outstanding preferred shares.

At present, the trading multiple of about 12x forward funds from operations (“FFO”) is still well-below peers. Others, such as First Industrial ( FR ), EastGroup Properties ( EGP ), and Rexford Industrial ( REXR ), all command averages in the mid-20x range. Similar-sized peer, LXP Industrial ( LXP ), even trades at about 14.5x.

However, the recent equity raise combined with the strong share price gains may indicate shares are fairly valued at current pricing. And despite the discount, I, nevertheless, believe shares are best left on hold due to the stock's recent performance and outstanding uncertainties pertaining to active lease-up and property sale efforts.

PLYM Q2 Results

At the end of June 30 , PLYM’s same-property portfolio was 98.9% occupied. This is slightly above the high end of their full-year target , which currently stands at a midpoint of 98.6%.

During the quarter, their same-property portfolio generated cash basis growth in net operating income (“NOI”) of 6%, moderately lower than their full year 7.5% targeted midpoint. The weaker growth rate was due to timing of certain expenses, such as repairs and maintenance and real estate tax assessments. By year end, however, PLYM still expects to hit their targeted growth rate.

Plymouth continued to make progress in addressing their upcoming lease expirations. So far, they’ve addressed nearly 90% of their 2023 expirations and about a quarter of those due in 2024. For those leases commencing in Q2, the team realized a blended 19.3% cash basis increase in rents. On a separate basis, PLYM locked in increases of 36% on new leases and 11.2% on renewals.

PLYM Q2FY23 Investor Supplement - Lease Expiration Schedule

For those leases commencing in the second half of the year, PLYM achieved a 23% increase in rents, above the previously estimated 18% to 20% portfolio mark-to-market. And looking at all leases commencing in 2023, the company expects to realize an aggregate cash basis increase of 20%.

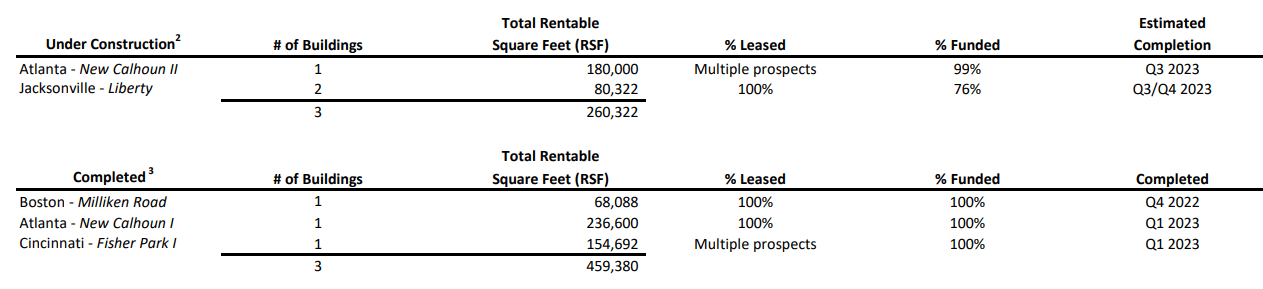

In the development pipeline, PLYM had three properties under construction and set to fully deliver this fiscal year. The two properties in Jacksonville are 100% leased and will deliver sometime in the coming months.

PLYM Q2FY23 Investor Supplement - Summary Of Developments

{kind=link}

Lease-up at the property in Atlanta, on the other hand, is still underway. Given the market, I expect PLYM to eventually have the property fully leased. Likewise, PLYM is still working on leasing the Cincinnati property that was delivered in the first quarter of the year. The delays here are in-line with the longer decision-making timetables that have become more prevalent in the sector in recent months.

Pending Redemption Of 7.5% Series A Preferred Stock

PLYM announced on August 2 that they would redeem all their 7.5% Series A Preferred Stock ( PLYM.PA ) for a total of +$48.8M. This represents a redemption price of $25/share. Existing holders of record at the close of August 25 would then be entitled to a final dividend payout of $0.34647/share on September 6.

This decision was due in part to improving their capital structure. As it is, the company has reduced their leverage metric including the preferreds for five straight quarters. The current path could have taken them to a 7x multiple by year end. Elimination of the preferreds could thus ensure the company running below 7x moving forward.

From a funding perspective, PLYM intends on utilizing their stock issuance program, as well as asset disposition. The ATM program was already utilized during Q2 and part of July for a total of +$27M. Within the next 60 days, PLYM is also expecting to close on the sale of one of their properties. Following the sale, PLYM will use the proceeds to eliminate the secured debt on the property and will apply the remaining balance to the redemption of the preferred stock.

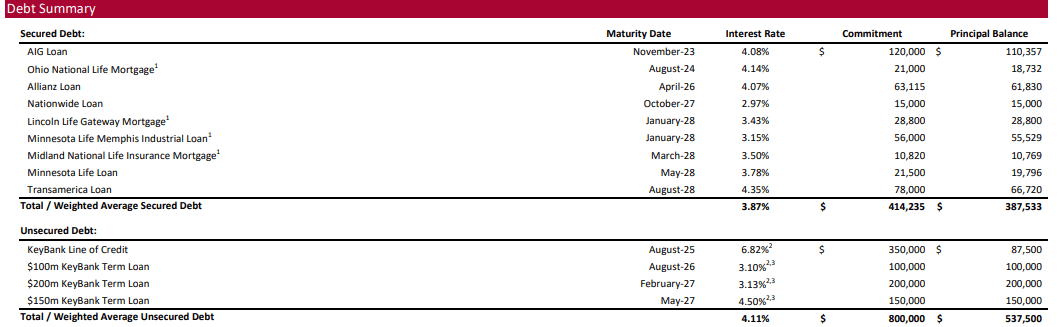

Given the timing of the sale, little was disclosed other than to say that the transaction was in progress. Investors should expect more details on the company’s Q3 release. Looking ahead, PLYM does have an upcoming maturity of +$110M in November. Progress on this will also likely be provided in the next quarter’s discussion.

PLYM Q2FY23 Investor Supplement - Summary Of Total Outstanding Debt

{kind=link}

Is PLYM Stock A Buy, Sell, Or Hold?

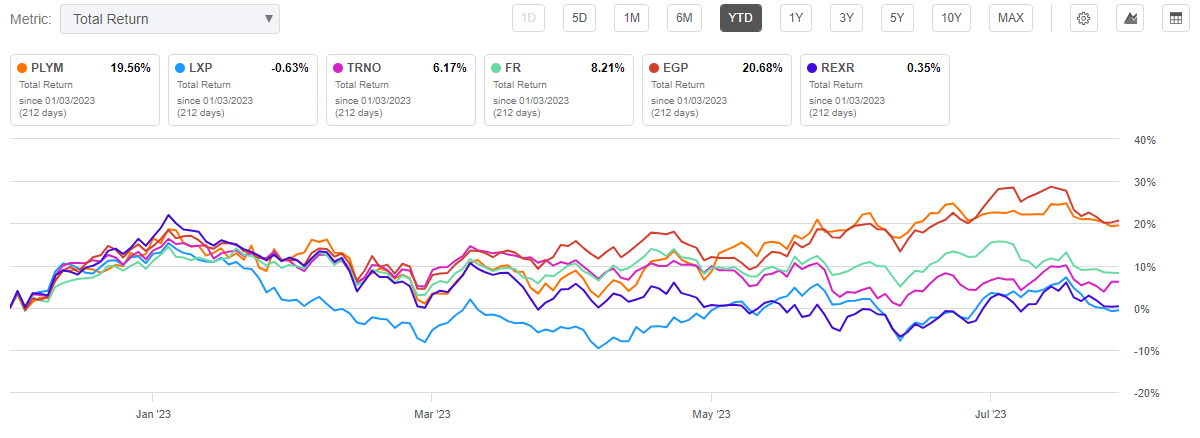

Shares of Plymouth Industrial have performed strongly since my last update . The stock is up double-digits compared to an 8.5% gain in the S&P 500 ( SPY ) over the same period. PLYM is also outperforming most other industrial components, with YTD gains of nearly 20%.

Seeking Alpha - YTD Returns Of PLYM Compared To Peers

{kind=link}

The recent run-up and the decision to issue stock to fund their redemption of their preferred shares lead me to believe that shares are valued fairly. CEO, Jeff Witherell, had previously targeted equity issuances at the $25-$27/share range. With the stock a few dollars shy of that target, PLYM was likely correct in trying to capitalize on favorable pricing while they still had it.

I view the outlook as positive for PLYM and am bullish on their unique geographic presence, which is centered around key logistical hubs that are likely to gain prominence as companies continue their nearshoring efforts.

But PLYM is still trying to lease a property that was delivered in the first quarter of the year. Additionally, they have another property that is set to deliver without being fully leased. Furthermore, they’ve made good progress on addressing upcoming expirations, but they’re not as far along on the 2024 leases.

In my view, this adds an element of uncertainty that is worth a pause until further information is provided. Sometime this quarter, the sale of one of their properties will likely close. Details will then be provided on the Q3 release. Investors can then use that to better assess the value of PLYM’s shares. Until then, I view PLYM as best kept on hold.

For further details see:

Plymouth Industrial: A Quality REIT With A Debt Profile Waiting To Unfold (Rating Downgrade)