PLYM - Plymouth Industrial: A Value REIT In The Industrials Sector

- Plymouth Industrial is a smaller REIT in the Industrials sector that has a strong presence in "The Golden Triangle" region of the U.S, an area with critical strategic value.

- The company's portfolio is 97.3% occupied with a nearly 100% collection rate from a diverse group of reliable tenants, one of which includes the FedEx Corporation.

- Recent earnings touted strong rental growth rates, with cash re-leasing spreads at over 20%.

- Shares are currently trading at a discount to related peers and are down 35% YTD.

- For REIT investors seeking a bargain in the Industrials sector, PLYM offers a compelling case for material upside.

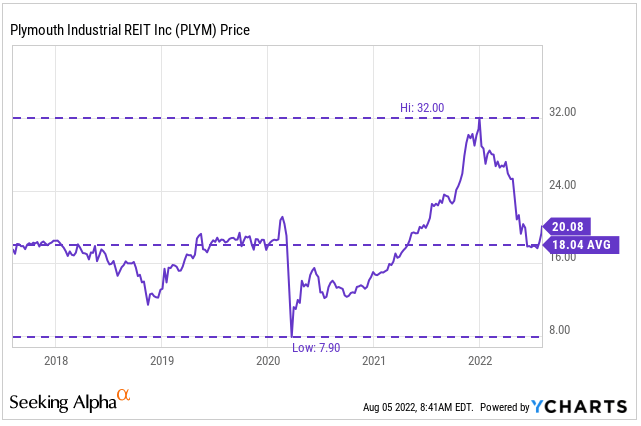

Plymouth Industrial ( PLYM ) is a real estate investment trust ("REIT") that is up over 15% on the month but still down 35% YTD.

YCharts - PLYM's Recent Share Price History

{kind=link}

Coming off their most recent earnings release, the company remains well positioned to continue benefitting from the elevated demand for industrial space. The company's focus on Tier II markets that are located away from the coastlines is also a unique competitive edge that will prove advantageous in current market conditions. A dearth of supply accompanied by more stringent capital requirements is yet another tailwind for the company.

While more well-known industrials, such as Prologis ( PLD ), Duke Realty ( DRE ) and STAG Industrial ( STAG ) command the most attention among investors, PLYM is one that may be getting too overlooked. Shares are currently trading near the lower end of their yearly range and at just 11.1x forward core funds from operations ("FFO"). This is a notable discount to the other comparable peers, most of whom are trading at a multiple of at least 15x forward FFO. For investors seeking a sector bargain, PLYM offers an attractive opportunity for significant upside.

A Smaller REIT Operating In "The Golden Triangle"

PLYM is a smaller industrial REIT whose market cap is about +$800M. This is on par with other smaller names , such as Industrial Logistics ( ILPT ), but considerably smaller than STAG, who has a current cap of +$6B. At a cap of nearly +$100B, PLD is well out of range for comparison.

Seeking Alpha Peer Comparison Tool - Market Cap

{kind=link}

Within their portfolio, PLYM currently owns and manages 207 industrial buildings located primarily in "The Golden Triangle" ("GT"), which is an area of the U.S. that has critical strategic value . For one, the region contains over 70% of the country's population and includes more than half the U.S. GDP within its boundaries. In addition, it contains more ports than any other region in the country and includes five of the seven Class I railroads. While the coasts do have a commanding presence for logistics, the Golden Triangle is fast becoming an epicenter for expansion.

Ford ( F ), for example, recently announced that their BlueOval City Electric Vehicle Center would be located just outside of Memphis, Tennessee. In addition, Intel ( INTC ) had previously announced their decision to build two semiconductor fabrication plants in Columbus, Ohio. The buildout of these facilities will support the creation of new jobs and continued move-ins to the region, which has already seen average population growth over the last five years of 5.1%.

August 2022 Investor Presentation - Map of The Golden Triangle

The Sudden Attractiveness of Tier II Markets

PLYM's history of investing in Tier II markets, which are those characterized by older properties and smaller tenants, among other traits, is a strategy that will likely pay off in coming periods. As companies, such as F and INTC, continue to expand into the GT, the relative affordability of the region compared to Tier I markets will enable PLYM's tenants to better absorb higher rental rates.

Tier II markets, for example, have lower average labor costs and an industrial worker-to-business ratio of 4x those of Tier I markets. In addition, the cost of living is significantly lower, further enabling employers to better manage their labor costs.

With supply growth limited due to various macroeconomic factors, one of which is current capital constrictions on development, the value of PLYM's existing properties should increase or remain supported at the very least. As the industrial-based business community and the overall population continues to expand into the region, PLYM's rental growth should remain supported by the heightened demand for warehouse space.

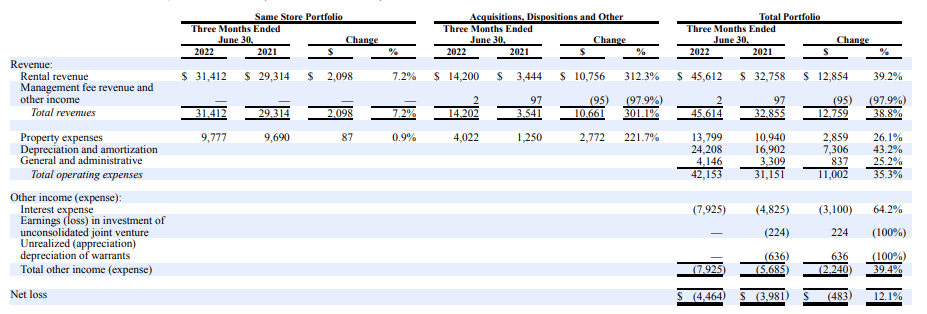

Solid Overall Quarterly Results

Q2FY22 results were generally positive. Total revenues were up nearly 40% YOY, driven primarily by the contributions from newly acquired properties. In the same-store portfolio, total revenues were up 7% due to rent escalation and greater tenant reimbursements for expenses incurred on their net leases. Compared to estimates, total revenues came in +$1M better than expected .

While total operating expenses were also up significantly during the period, the rate of growth was less than the growth in revenues. Additionally, the largest driver of expense growth was depreciation and amortization ("D&A"), which was up 43% during the quarter due to the additional properties in service during the comparable period. Since this line item is added back to other relevant earnings metrics, it's not a particularly useful category for analysis on the top line.

PLYM did incur a 64% increase in interest expense as a result of additional borrowings associated with their acquisition activities. This increase resulted in the company posting a net loss for the quarter of ($4.5M). This loss was 12.1% more than the same period last year, which was also down due to higher interest expense.

Q2FY22 Form 10-Q - Summary of Results of Operations

{kind=link}

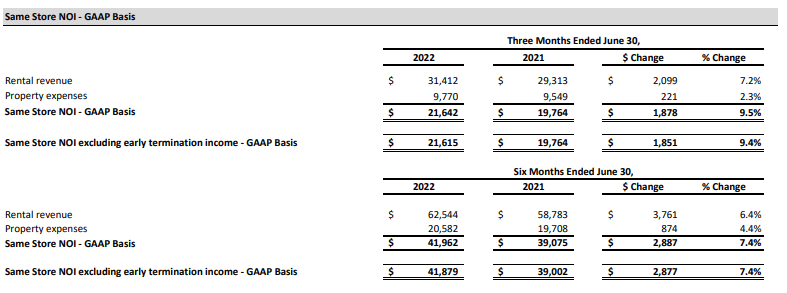

When excluding D&A and interest, the results are markedly stronger. Quarterly same-store Net Operating Income ("NOI") was up nearly 10% on a GAAP basis and about 7.5% on a cash basis. Over the first half of the year, same-store NOI is now up double-digits on a cash basis.

Q2FY22 Investor Presentation - Summary of Same-Store NOI Growth

{kind=link}

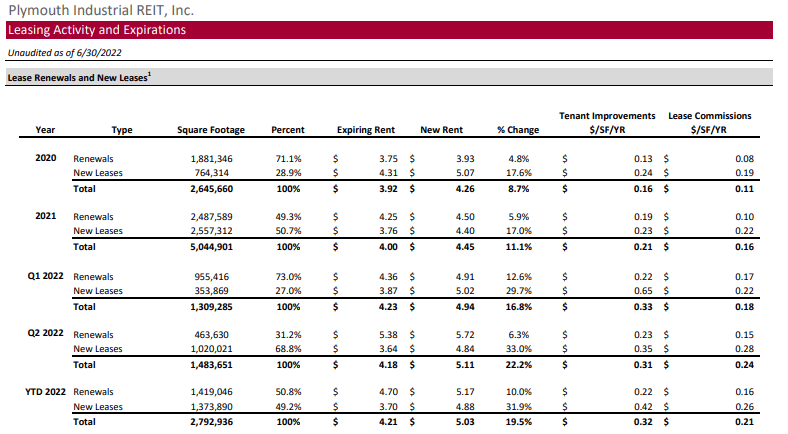

Still Reporting Double-Digit Rent Growth

The strength in NOI growth is attributable to the company's ability to consistently grow rents. YTD, rents are up 19.5% . And in Q2, alone, rents increased 22.2%. Additionally, the company had a renewal rate of 33% in Q2 and a rate of 51% through the first half of the year. This places the company in a strong position for the remainder of the year.

Q2FY22 Investor Presentation - Summary of Leasing Activity

{kind=link}

Through July, PLYM has also executed on leases representing 92% of the total square feet set to expire in 2022. The renewal rate for these transactions was 71%. From an overall expiration schedule, 36% of annualized base rent ("ABR") is set to expire prior to 2025. This presents an attractive mark-to-market opportunity for the company, given the current trajectory of their leasing activity.

Q2FY22 Investor Presentation - Lease Expiration Schedule

The Slowdown in Acquisitions Is Not A Negative

PLYM has clearly benefitted from the accretive effect of past acquisitions . Activity, however, appears to be slowing due to current market conditions, which is causing a re-evaluation of in-going cap rates and resulting in a pause in overall activity. In the current quarter, the company did complete +$65M in acquisitions, nevertheless, but it was lower than what management had expected to complete.

For PLYM, the slowdown may be best, as the company does operate on a higher degree of leverage. At more than 7x EBITDA, net debt is considerably higher than the company's peer group.

August 2022 Investor Presentation - Net Debt Multiple of PLYM Compared to Peers

With no significant maturities, however, debt-related risks in the near-medium term are minimal. Additionally, about 80% of their debt is fixed-rate, which minimizes their risks pertaining to the volatility of higher interest rates.

Q2FY22 Investor Supplement - Debt Maturity Schedule

Forward guidance does call for significantly higher interest expense. But at 3.5x coverage, their earnings are still more than sufficient to cover their reoccurring interest obligations.

Q2FY22 Investor Supplement - Full-Year 2022 Guidance

{kind=link}

While a greater portion of operating funds will be devoted to debt service, income-investors should not fear a reduction in the dividend payout.

Currently, the annual payout is $0.88, representing a yield of about 4.3%. Not only is this fully covered by forward FFO, but it is also comfortably covered by the more conservative AFFO, with a payout ratio of just over 50%.

An Industrial REIT At A Bargain Price

PLYM is a small industrial REIT that is being too overlooked by investors. Its strong presence in the Golden Triangle region of the U.S. will prove to be a key competitive strength as the industrial-based community, such as Ford and Intel, continue to expand into the area, bringing with them a growing population of employees.

The general affordability of the region compared to the coasts enables PLYM's tenants to better absorb continuous rental rate growth, which is likely to remain supported by heightened demand due to the continuing popularity of E-commerce and recent onshoring trends. Rental growth will also remain supported by limited supply that is further constrained by tightening financial conditions for new development.

At a 97.3% occupancy level and with cash collections running at nearly 100%, there are limited concerns regarding the health of the portfolio. Furthermore, shorter lease durations and a sizeable portion of expirations prior to 2025 provide an attractive mark-up opportunity when the time arises.

The company does have a significantly higher debt load than related peers, and their future earnings potential will take a hit due to the related debt servicing costs. However, there are no significant near-term debt maturities and current EBITDAre still comfortably covers their interest obligations. Additionally, income-focused investors are unlikely to be impacted by the higher expected interest expenses, as the dividend payout is wholly covered by adjusted FFO.

At current pricing, PLYM is trading at an implied cap rate of about 7.2%, which is significantly higher than the related peer set. Additionally, shares are trading at a discounted forward multiple of 11.1x FFO.

August 2022 Investor Presentation - Implied Cap Rate of PLYM Compared to Peers

At a 15x multiple, shares would be valued at approximately $27/share. This would imply a cap rate of 6.1%, which is, indeed, higher than most of the smaller peer population but slightly higher than the current rate for STAG. Given the company's strong presence in the Golden Triangle, this multiple is reasonable. For investors, this would represent upside of over 30%, in addition to dividend payments that are current yielding nearly 4.50%. For those seeking industrial exposure on the cheap, PLYM is one not to overlook.

For further details see:

Plymouth Industrial: A Value REIT In The Industrials Sector