PLYM - Plymouth: Industrial Growth Without The Industrial Multiple

2023-10-10 06:28:43 ET

Summary

- Plymouth Industrial is a small cap industrial REIT with properties in submarkets that have low supply growth and high demand.

- The combination of low vacancy rates and minimal supply will lead to market rental rate growth, potentially increasing the company's FFO/share.

- Plymouth is trading at a significantly discounted multiple compared to its peers, indicating potential for multiple expansion and upside in stock price.

Plymouth Industrial (PLYM) is a small cap industrial REIT with 34 million square feet spread over the inland U.S.

The buy thesis

PLYM is well-positioned for long term growth with properties in submarkets that seem to have dodged the new supply. The combination of low vacancy rates and minimal supply will keep market rental rates growing, potentially adding to the already large mark-to-market opportunity. As PLYM rolls its rents up about 20% over the coming years, its FFO/share should grow at a healthy clip which far exceeds what is priced in at PLYM's currently low multiple.

This thesis will delve into the following topics

- Supply growth only moderate for entire sector but particularly manageable in PLYM markets

- Current mark-to-market and potential for higher market rates

- Relative value

- Absolute value - below replacement cost

- Multiple expansion likely as historical low multiple was based on equity overhang which no longer exists

- PLYM's interest rate risk

Fundamental outlook of industrial sector

Industrial real estate has been in high demand for a long time now and the demand is expected to increase secularly as e-commerce sales continue to rise. With such highly visible tailwinds, developers try to deliver supply to keep up with demand. For a while it looked like there was going to be quite a bit of new development in the sector, but that has calmed down considerably due to interest rates.

The substantially higher interest rate environment has made financing development more challenging which seems to have discouraged a significant portion of near and medium term development. The latest numbers show only moderate supply coming to the sector.

Yardi Matrix

At a national level, developments under construction total about 3.1% of standing inventory while planned developments are for about 7% of existing supply. It is not low supply growth, but it is lower than it has been and much lower than investors had feared.

The demand side remains as strong as ever. Frankly, logistics warehouses are just an efficient way to move and store inventory. The cost per foot of warehouses is markedly lower than other types of real estate making it the ideal solution for purveyors of physical goods. Trends that are backed by rational financial thought tend to be more enduring, so I think the increased use of warehouses is here to stay. As warehouses become more automated, operating costs from labor are decreasing which makes the real estate even more economic for tenants.

With supply in check and secular demand growth, I am bullish on the industrial real estate sector in general. Within the sector, some are better positioned than others with respect to valuation and positioning. If one were to look at growth alone, Rexford ( REXR ) is probably the best. Its valuation has improved considerably as well so I think it is a good stock right now. There are, however, some even better options, in my opinion.

Plymouth is the best on the valuation side by a good margin.

{kind=link}

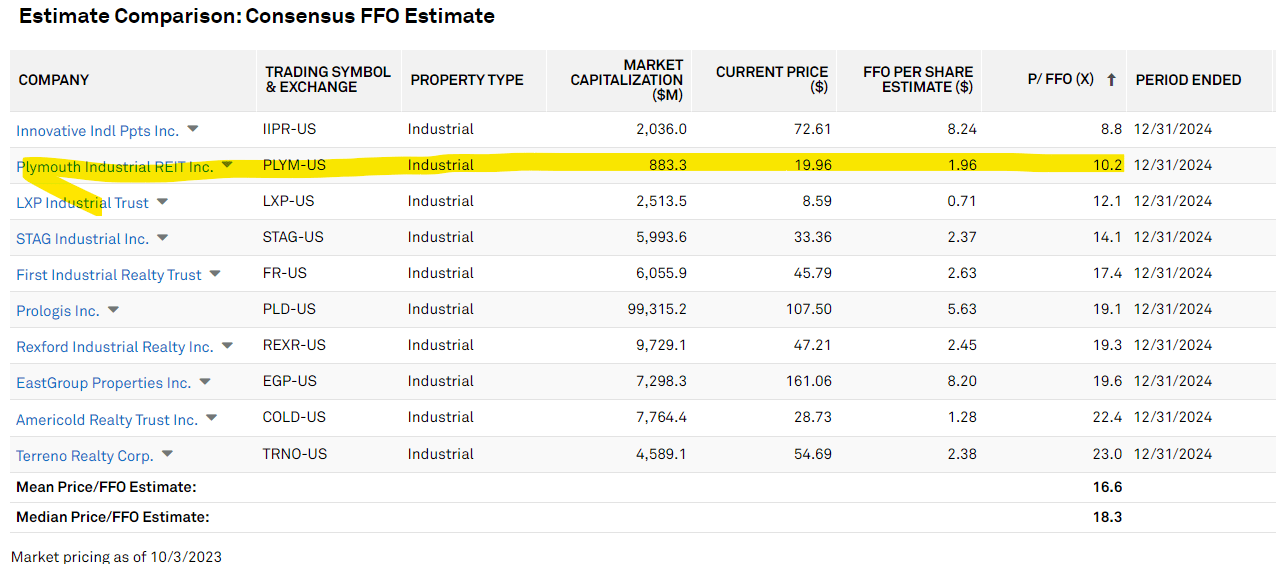

At 10.2X FFO PLYM is the lowest multiple industrial REIT. Innovative Industrial's ( IIPR ) 8.8X multiple does not count because a large portion of its revenue comes from leases that are dramatically above market rate which implies negative growth ahead. It relates to their half lease, half loan sale leasebacks which I expound upon more here .

PLYM's 10.2X compares to the sector mean and median of 16.6X and 18.3X, respectively.

This significantly discounted multiple indicates that the market considers PLYM's growth outlook to be substantially worse.

I disagree.

The market has a bad tendency to conflate luxury with quality. It automatically assumes that properties which command a higher rent per square foot are better. I think PLYM's property portfolio has some key advantages that are being overlooked. The secondary market locations and lower price point are making it incredibly resilient to whatever supply comes along.

As we said at the outset the supply growth is only moderate and I think the sector will absorb it well, but wonderful things happen when the supply growth is really low in certain submarkets which is the case for PLYM.

PLYM evades the supply

Plymouth's property map looks like this.

S&P Global Market Intelligence

These are some of the key manufacturing and distribution hubs of middle-America and some of the most direct beneficiaries of on-shoring.

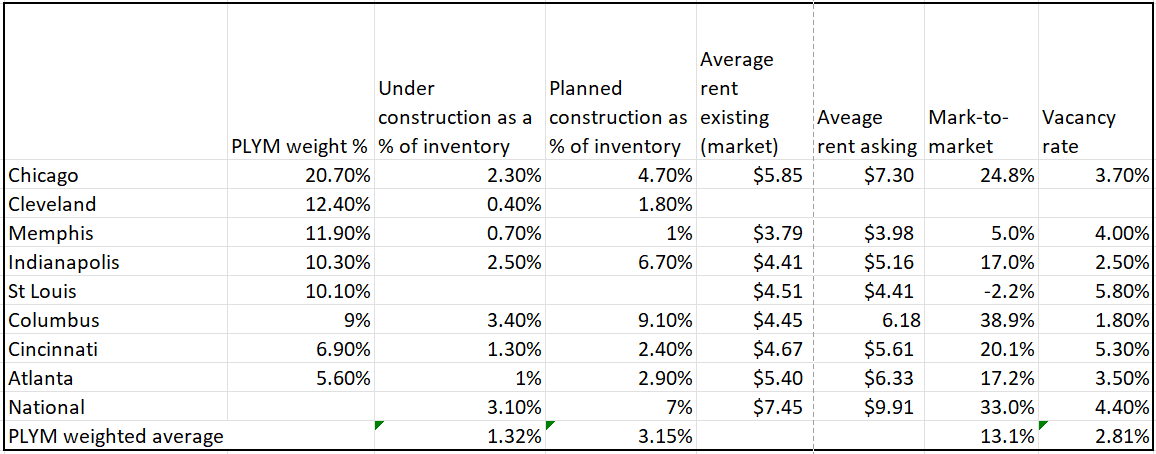

However, the growth has not been as explosive in these areas as others which has kept them out of the eyes of developers. We compiled the submarket supply data that we could find to calculate the supply hitting PLYM's markets and it is less than half of the supply growth hitting nationally.

2nd Market Capital using data compiled from company filings and industry reports

{kind=link}

Chicago, PLYM's biggest exposure at 20.7%, has only 2.3% of existing supply being built and only 4.7% planned construction. PLYM's other major markets have even less supply coming in with a weighted average of 1.32% of standing inventory under construction and only 3.15% planned development.

Additionally, PLYM's submarkets are already very low vacancy at a weighted average vacancy of 2.81% compared to the national average of 4.4%. Note that this is the submarket vacancy rate, PLYM's occupancy is 98% so it individually has slightly less vacancy.

The low vacancy rate in combination with a lack of new supply indicates market rates will grow. Market rates are already 13.1% above existing rental rates in PLYM's markets. Note that this is for the market level. Plymouth, has a higher mark to market around 20% as per CEO Jeff Witherell's comments on the latest earnings call:

"We saw a 19.3% increase in rental rates on a cash basis for the quarter and through July 31st, we have achieved a 23.1% increase on leases commencing in the second half of the year. That's in line with our commentary last quarter that we might be trending ahead of the 18% to 20% portfolio mark-to-market we have previously estimated."

PLYM's mark-to-market is likely higher than that of the submarkets due to some combination of lease vintage and property quality. REITs tend to sign longer leases and usually operate within the top quartile of property quality within submarkets.

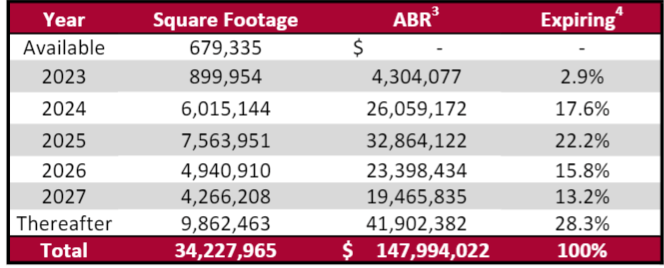

So the 20% mark-to-market is what exists today, and the combination of low vacancy and low new supply indicates market rates are likely to rise. I estimate PLYM will get about 20%-30% increase to cash rents over the next 5 years. 2024 and 2025 are particularly heavy lease rollover years which facilitates near-term rent increases

{kind=link}

Valuation

As discussed above, PLYM trades at 10.2X forward FFO while most industrial REITs trade in the 16X-19X range.

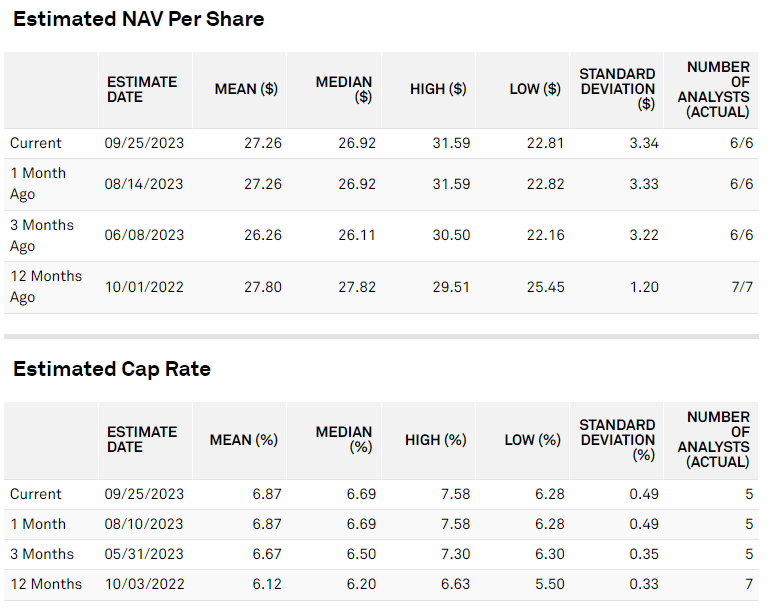

The value discount is also there on a net asset value basis. PLYM's NAV is $27.26 compared to a $20 market price. This NAV is calculated by street analysts using a 6.87% cap rate which is rather high compared to most industrial properties.

{kind=link}

That said, the submarkets in which PLYM operates do tend to have cap rates in this range so I think the NAV is about right.

Thus, PLYM is trading at 73% of NAV.

Historical valuation

Plymouth has often traded at substantial discounts to peers. For a decent chunk of the past these discounts were warranted for 2 reasons:

- Equity overhang

- High debt

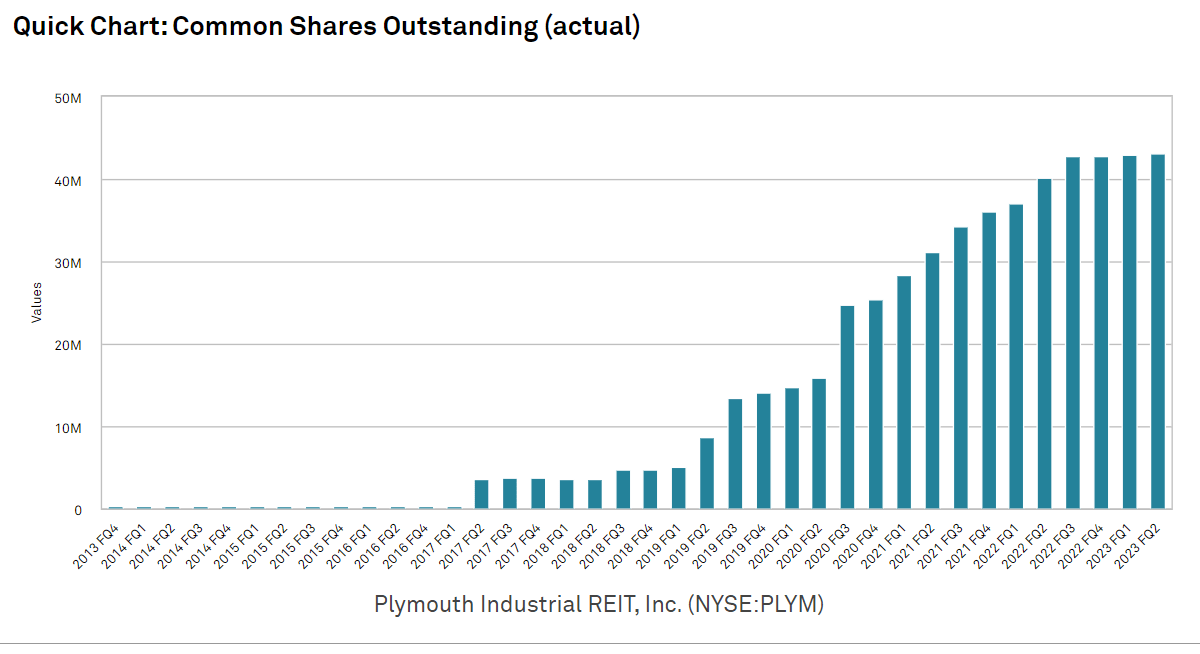

One of PLYM's early capital raises was in the form of a preferred that was initially very low cash cost of capital but accrued value over the course of its life that would eventually be paid out in equity. As the amount of equity ultimately issued would depend on the then current market price, an unknown quantum of shares were going to be issued at a future date. This is a classic equity overhang. It makes it hard for investors to value shares when they don't know the true number of shares outstanding.

Well, PLYM slowly paid down that overhang with equity issuance.

{kind=link}

Today, the overhang is completely gone. The share count is the full diluted share count with no looming issuance ahead.

When there was the overhang it made sense for the market to trade PLYM at a discount. Without the overhang I don't think the discount is warranted.

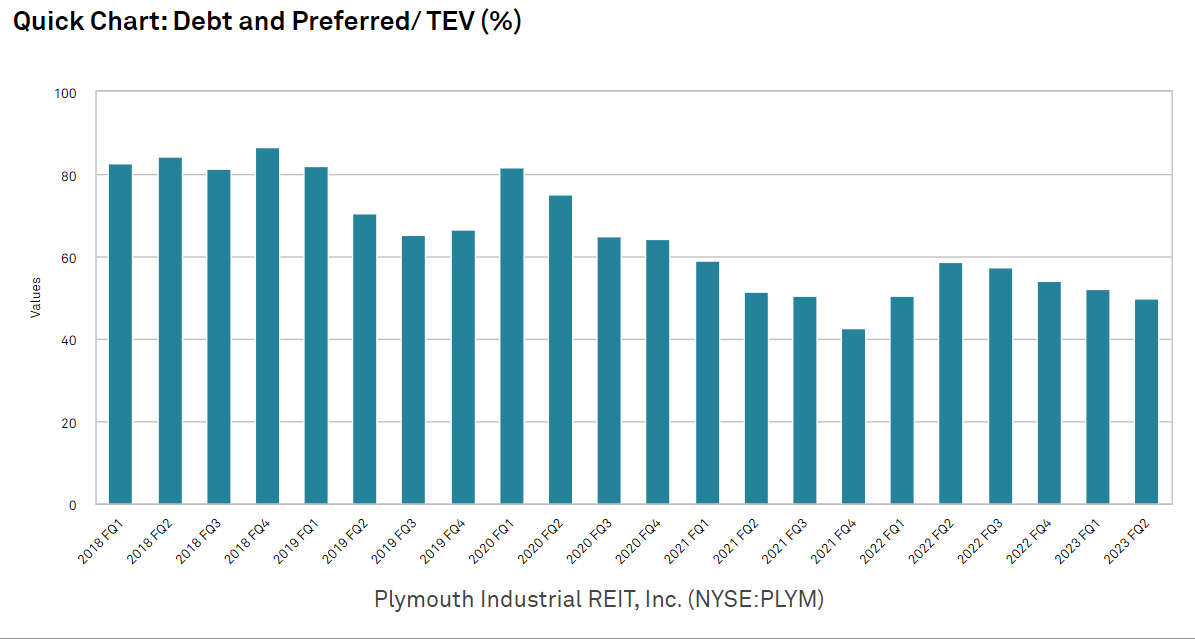

The other reason often cited for PLYM's discount is its higher leverage. This too was historically true but has since been largely cured.

{kind=link}

With property sales, including a recent extremely profitable sale of a Chicago property for $19.9 million that netted the company a 31.1% IRR, PLYM has paid down its debt to a healthy level. Its leverage is now only fractionally higher than the average industrial REIT.

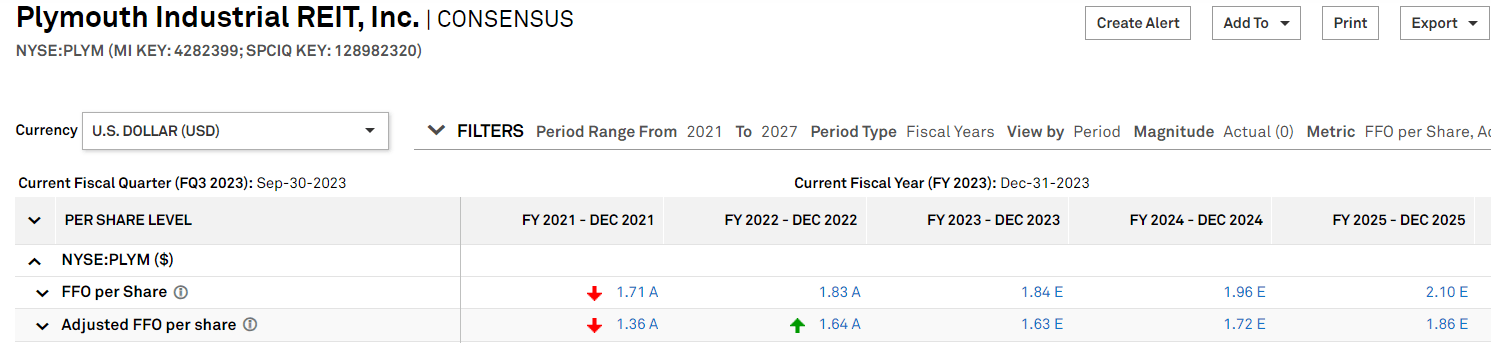

PLYM had some ailments, but it has cured them. Usually the cures of issuing equity for the overhang and overequitizing acquisitions would hurt FFO/share, but PLYM's property level performance was so exceptional that they actually grew FFO/share while making the huge balance sheet improvements.

{kind=link}

So what we are left with is an industrial REIT with well-located properties for the current environment and a strong growth outlook that trades at a highly discounted multiple. That multiple is based on an outdated perception of what the company was and is no longer applicable for what the company is today.

As such, I think PLYM's multiple will expand materially. I spot fair value at 14X-15X which implies roughly 40% upside.

Future supply

The market prefers coastal locations because the lack of available land is thought to prevent supply growth, yet it is these markets that are getting the heavy supply.

Why?

It has to do with price points. Industrial warehouses in super premium markets are so highly valued that even with land scarcity developers find ways to build. The stabilized warehouse value greatly exceeds cost of construction in those markets even if the cost of construction is a bit higher there.

Plymouth's markets have plenty of land which some people fear will lead to unfettered supply growth. The impediment to supply, however, is the differential between the value of existing real estate and cost to build.

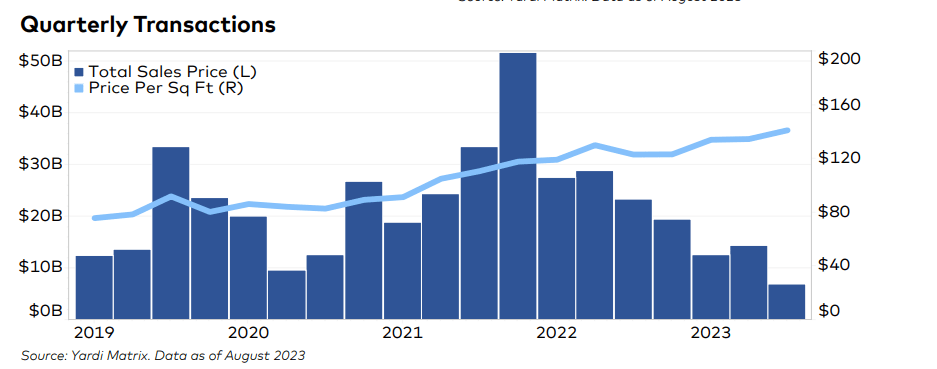

Specifically, PLYM's price point makes it largely immune to supply. PLYM trades at an enterprise value per square foot of about $50 but industrial transactions are at $140 per foot

{kind=link}

Cost to develop is roughly in that range as well.

PLYM's extremely low cost basis, having bought the majority of its properties well below replacement cost, means it can turn a healthy profit at fairly low rental rates - rental rates that don't really justify new supply.

If someone really wants exposure to middle-American industrial, they would be far better off just buying PLYM than developing. I think this makes PLYM a potential takeout target.

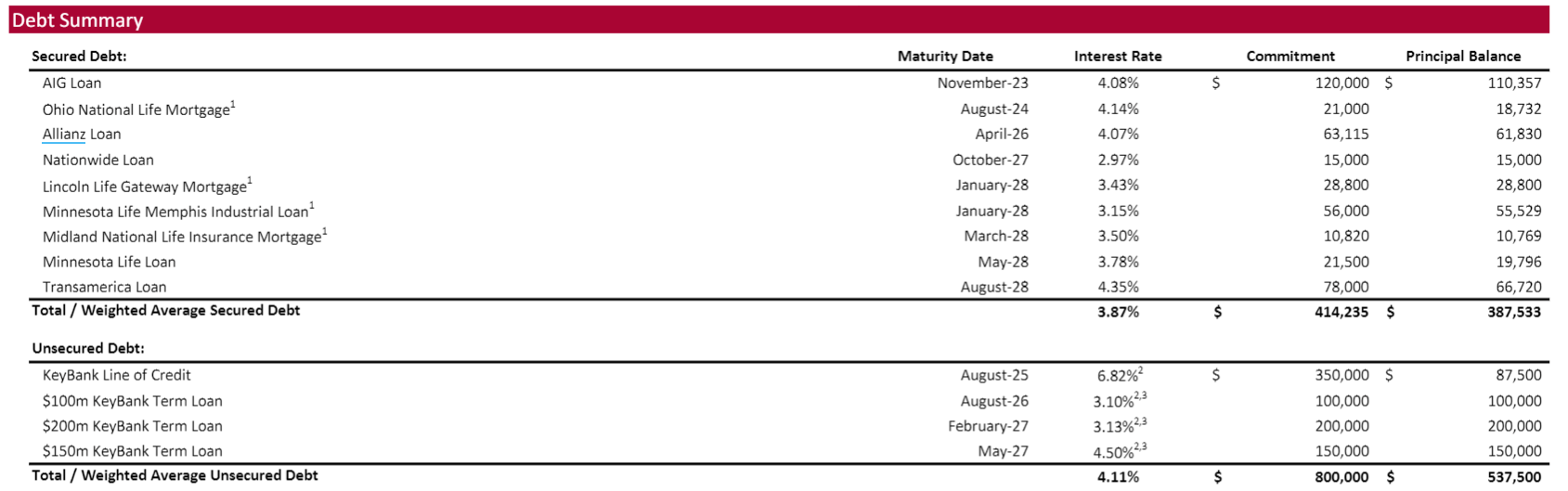

Interest rate risk

Interest expense is a concern for most of the market right now. The majority of PLYM's debt is fixed rate or swapped to fixed.

{kind=link}

Thus, it is not so much a matter of variable rate volatility but rather the refinancing risk as its low interest rate debt rolls.

Through the end of 2024 PLYM has about $141 million of cheap debt rolling which will likely have to be refinanced at higher rates. Assuming this gets refinanced 3 percentage points higher, it would be a hit of about 10 cents per share.

That cuts into growth a bit, but property level growth is enough to more than offset that. The extra cost is why I think PLYM should trade at 14X-15X instead of 18X like the rest of industrial.

For further details see:

Plymouth: Industrial Growth Without The Industrial Multiple