PMT - PMTU: Attractive Debt From This mReit

2023-12-28 05:58:51 ET

Summary

- PennyMac Mortgage Investment Trust (PMT) is a mortgage REIT with a large mortgage servicing rights business.

- PMT has issued a baby bond, PMTU, with a defined maturity date and a current yield comparable to its preferred shares.

- PMTU offers investors a low duration profile, a fixed rate, and a shallow modelled drawdown profile, making it an attractive investment.

- PMTU trades flat from an accrued interest payment perspective, with the next payment date set for the end of December but an ex-dividend date that has already passed.

Thesis

PennyMac Mortgage Investment Trust ( PMT ) is a mortgage REIT widely covered on the Seeking Alpha platform. As per the company's annual report, the entity is a:

finance company that invests primarily in mortgage-related assets. Our objective is to provide attractive risk-adjusted returns to our investors over the long-term, primarily through dividends and secondarily through capital appreciation. A significant portion of our investment portfolio is comprised of mortgage-related assets that we have created through our correspondent production activities, including mortgage servicing rights, or MSRs, subordinate MBS, and CRT arrangements, which include CRT agreements and CRT strips that absorb credit losses on certain of the loans we sold. We also invest in Agency MBS, subordinate credit-linked MBS and senior non-Agency MBS. We have also historically invested in distressed mortgage assets (distressed loans and real estate acquired in settlement of loans), which we have substantially liquidated.

What sets PMT apart, is that in addition to leveraging up Agency MBS as other mortgage REITs, it has a very large mortgage servicing rights business:

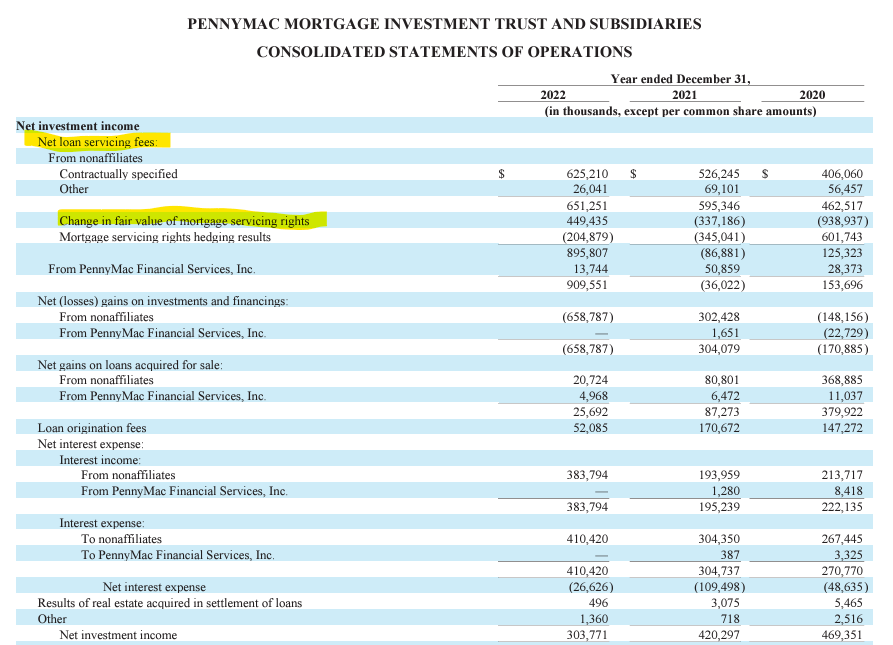

Statement of Operations (Annual Report)

{kind=link}

Servicing rights references the cash-flows to be received by an entity when it provides individuals with services around their outstanding mortgages:

Mortgage servicing rights ('MSR') refer to a contractual agreement in which the right to service an existing mortgage is sold by the original mortgage lender to another party that specializes in the various functions involved with servicing mortgages.

What is particular about MSRs is that they actually have negative duration and negative convexity through their cash-flow mechanics. When rates rise, voluntary pre-payment speeds on outstanding mortgages slow down, and the cash flows extend, increasing values. We can fully observe this in the 'Statement of Operations' above, where the MSRs posted a significant increase in fair value in 2022 as rates went up. MSRs are therefore an embedded hedge in an mREIT's balance sheet.

PMT, like any mortgage REIT, is highly leveraged. Both on an asset basis via repurchase agreements, as well as via preferred equity. The entity tried to save some cash on their fixed-to-floating preferred equity when the Libor to SOFR conversion occurred, action which has backfired via higher funding costs. As a result, we are now seeing a baby bond issuance from PMT via the PennyMac Mortgage Investment Trust 8.5% 2028 note ( PMTU ).

What is a baby bond? An exchange listed debt slice

Baby bonds are fixed-income securities that are exchange listed and have smaller par values than the usual $1,000. Generally we see them issued with a value of $25. Furthermore, as opposed to their classic counterparts, they trade flat to accrued interest, meaning there is no dirty price upon trading them. They are to a certain extent a hybrid instrument, blending in features of equity and preferred equity with bond features.

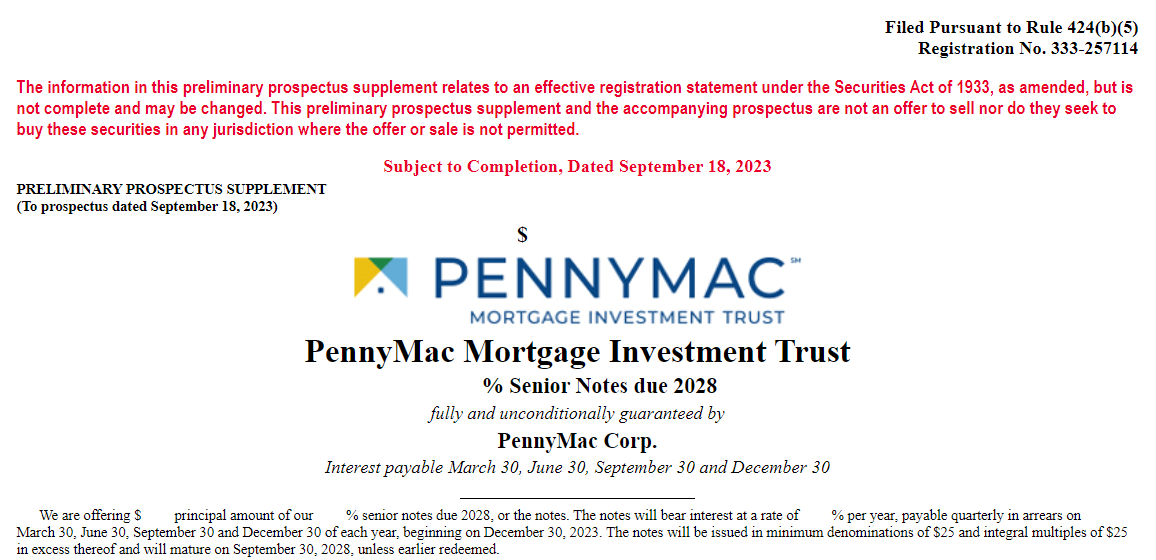

Ultimately, 'baby bonds' have a defined maturity date and trade under the format of a note, which puts them on the liability line in a company's balance sheet:

{kind=link}

PMTU matures in September 2028, and until then it will pay holders 8.5% quarterly in March, June, September and December. The new notes have a call date two years out from the issuance date:

Details (Quantumonline)

If interest rates move down as per the forward SOFR curve, we expect the entity to call the notes before the stated maturity date. The notes have a defined maturity date, and when they were issued 5-year treasuries were trading at 4.5%, meaning they were issued at a spread of roughly 4% over treasuries, or T+4%.

Similar yield to preferred shares, but a defined maturity

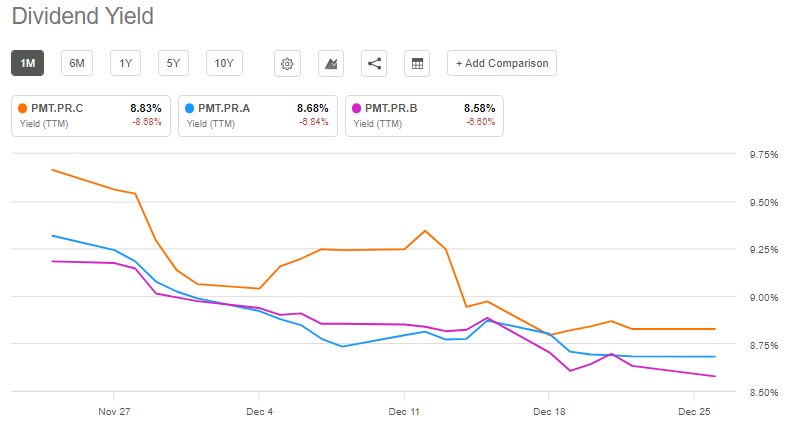

The notes are now trading very close to par, and at a current yield very much comparable with the preferred shares from PMT:

Current Yields (Seeking Alpha)

{kind=link}

Preferred shares are not liabilities for PMT, but sit in the equity line. While cumulative, they are perpetual, meaning an investor does not have a defined maturity date to get their capital back. Furthermore that translates into a long duration and high volatility. @Trapping Value penned a nice article here regarding the issues the company has created by not letting the preferred shares moving to a floating rate and keeping them fixed. This choice has reverberated into higher costs of funds for new preferred shares. The market is going to ask for compensation in exchange for the additional risk. And we are of the opinion that PMTU is a direct result of the issues faced by PMT from its choices on its preferred shares. By having a fixed rate and a defined maturity, PMTU eliminates the issues encountered by investors in the company's preferred equity.

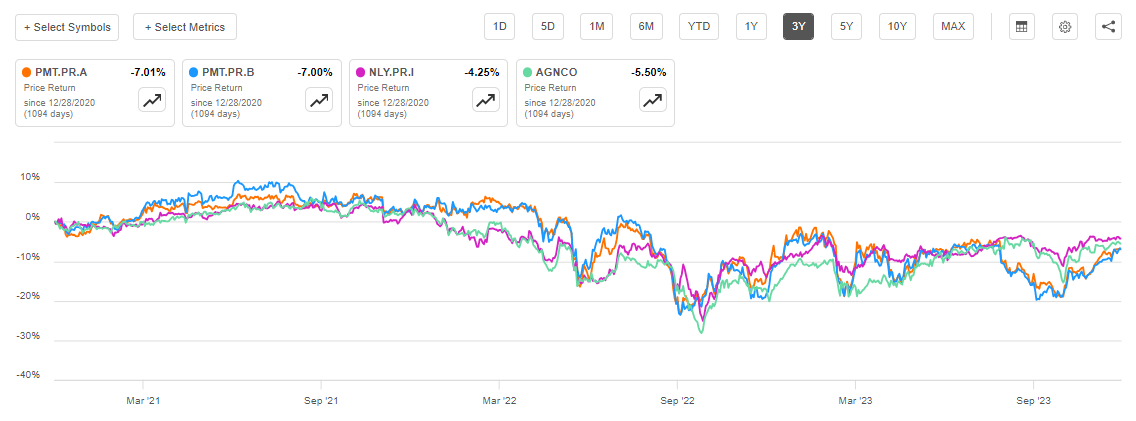

Preferred equity is a form of permanent capital for many mortgage REITs, and only Annaly ( NLY ) comes to mind when thinking about mortgage REITs who have been prescriptive about calling preferred shares after their 5-year non-call date. Many others in the market have made preferred shares as a form of permanent capital especially in today's high yield environment. A perpetual maturity date requires a higher compensation, hence the higher yields in the sector. Furthermore investors have experienced themselves the high volatility associated with mREIT preferred equity, especially in a rising rates environment:

mREIT Preferred Shares (Seeking Alpha)

{kind=link}

Even the best mREIT preferred shares have experienced -20% drawdowns in the past two years.

Why is PMTU attractive?

The note's defined maturity with its tight 2-year non-call creates a low duration profile for PMTU. We estimate the duration here to be 3.5 years, with our assumption for a call before the maturity date. A low duration profile means a low drawdown profile. We have seen this first hand in the massive yield spike in October:

When PMTU was issued at the end of September 10-year rates were 4.5%. They subsequently spiked to 5%. The duration impact to PMTU was of 50 bps from rates and a slight impact from widening credit spreads, with the note down -2.7% during October's rout. A full 100 bps rise in required rates (from both risk free rates and credit spreads) would have resulted in a -3.5% drawdown. We feel peak rates are behind us, thus any future spikes in credit spreads are going to be mitigated by lower risk free rates to a certain extent, thus having a small net impact to required discount rates. PMTU therefore should have very well contained drawdowns of maximum -7% in an adverse scenario (200 bps of blended higher required yields). You are therefore getting a junk bond yield here with an investment grade bond drawdown profile.

Conclusion

PMTU is an exchange traded bond from the PMT mREIT. The note has a defined maturity date in September 2028, and a call date starting September 2025. The bond has a current yield similar to the preferred shares from PMT, but offers investors certainty with respect to repayment and a defined yield to maturity. PMTU pays an 8.5% fixed rate, and unlike bonds trades flat (i.e. no accrued interest is paid upon trading it). Given its low duration and fixed rate, PMTU is set to have a very shallow drawdown profile per our analysis and represents an attractive and less volatile way to buy into PMT's capital structure. We like the term maturity, the high coupon and the fixed rate offered by the note given the lower forward for risk free rates.

For further details see:

PMTU: Attractive Debt From This mReit