XLF - PNC Financial: The Regional Leader In The Banking Crisis

2023-03-27 12:00:00 ET

Summary

- In March, PNC Financial outperformed its peers in the iShares Regional Banks ETF, demonstrating the market's confidence in its leadership prowess.

- Even though the bank remains resilient, a potentially worse economic downturn or a further spread of the banking crisis could still affect its stability.

- Its AFS and HTM securities incurred unrealized losses exceeding $9B. Moreover, it held uninsured deposits representing a sizeable 46% of its total deposits, raising concerns about its recent deposits outflow.

- Can PNC outshine its competitors during the crisis and emerge stronger, cementing its market leadership? It's crucial to assess whether PNC has what it takes to weather the storm and come out on top.

- With an NTM adjusted P/E of 8.3x, it seems the market has already factored in a significant decline in future earnings.

The PNC Financial Services Group, Inc. ( PNC ) is the leading constituent in the iShares U.S. Regional Banks ETF ( IAT ), accounting for 13.8% of its total exposure as of March 22.

The banking crisis has significantly affected PNC and its peer group in the IAT as market operators prepare for more pain.

However, does PNC deserve its battering, despite posting a well-diversified business model? It drives its growth through its retail and commercial segment, augmented by its asset management group.

Its scale has also helped it to deliver on " many expense-saving initiatives." As such, PNC has been a consistent outperformer against its regional banking peers represented in the IAT over the past ten years.

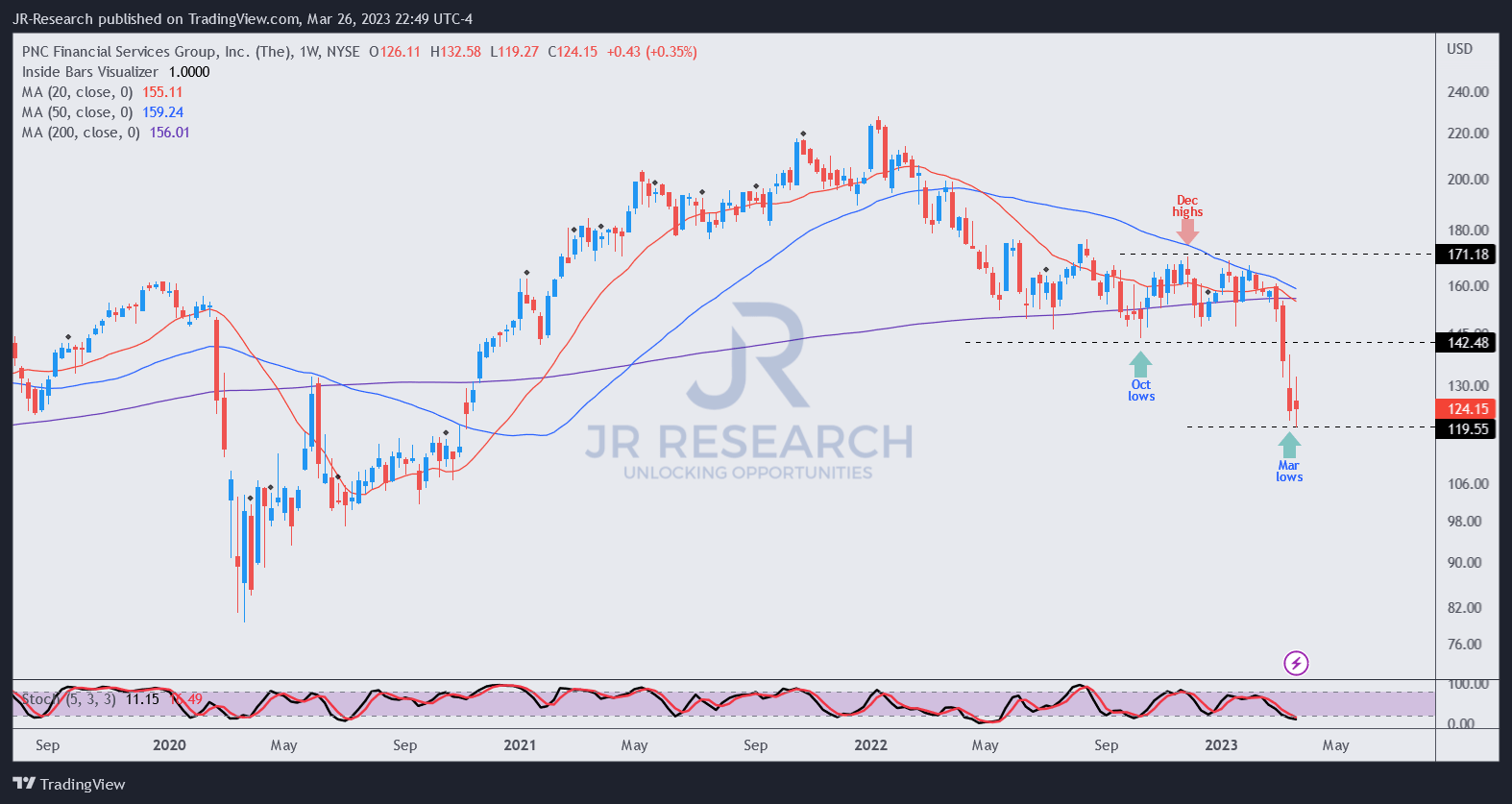

As seen above. PNC posted a 10Y total return of 9.5%, well above the IAT's 4.8% over the same period. Despite that, the recent hit to its performance due to the banking crisis was keenly felt as PNC fell to levels last seen in November 2020.

Therefore, its valuation has also collapsed significantly, as PNC last traded at an NTM adjusted P/E of 8.3x, in line with the two standard deviation zone under its 10Y average.

In other words, we believe the market is likely expecting a significant hit to its forward earnings, pricing it in even before analysts can revise it.

Despite that, PNC is still trading at a discount against its IAT peers' average (9.6x).

Therefore, the critical question facing investors is whether the reward/risk is attractive now, even as investors question the safety of its deposits and the threats emanating from its debt securities and commercial loans?

The challenge of deposit outflows is not new to PNC but likely accelerated following the collapse of Silicon Valley Bank or SVB ( SIVB ) and Signature Bank ( SBNY ).

The bank posted total deposits of $436.3B as of the end of 2022, down 4.6% YoY. PNC attributed the decline " to lower commercial and consumer deposits, reflecting competitive pricing dynamics and inflationary pressures."

It also increased its borrowed funds dramatically by 91% YoY, likely to help improve its liquidity position. However, investors should note that the bank also highlighted that its deposit base provides "relatively stable and low-cost funding."

As such, we will need to parse more information to assess the earnings impact on the bank, given the banking crisis on its deposit base and borrowings. Notably, it raised its FHLB borrowings by $32B as of the end of 2022, which cost an average rate of 4.6%.

In other words, it's an expensive cost of funding. As such, we believe the market's assessment of a marked earnings impact (as seen in its valuation write-down) is justified.

However, the question is, how big could this hole be?

PNC held about $200B in uninsured deposits, representing 46% of its total deposit base. PacWest Bancorp's ( PACW ) recent update suggests it lost about 47% of its uninsured deposits from the end of 2022 to March 20, 2023.

Hence, we believe PNC could also be significantly impacted, which will need a close assessment when the bank subsequently updates.

Moreover, it reported nearly $143.7B (amortized cost) in the available-for-sale or AFS and held-to-maturity or HTM portfolio. It represented about 26% of its total assets and therefore is pretty significant.

However, the fair value of the combined portfolio was about 93.6% of its amortized cost, indicating about $9.26B in unrealized losses. Hence, the hit could still be pretty steep if the bank faces a liquidity crisis, behooving them to realize some losses.

In addition, its commercial loan book represented nearly 70% of its total loans of $326B. A further fallout in the commercial space, driven by a worse economic recession than anticipated, could also cause further strains on its valuation.

Notwithstanding, PNC's report at the end of 2022 demonstrated its high-quality underwriting standards as its credit quality improved, as seen in its nonperforming assets, total loan delinquencies, ACL, and net charge-offs. Morningstar also highlighted: "PNC has demonstrated superior underwriting abilities compared to its peers."

Still, we would have preferred that company insiders demonstrated more conviction over its shares by making more insider purchases, given the recent steep decline.

Accordingly, the net insider purchases after sales metric is nearly -$500K . As such, it's much less convincing compared to PACW and Charles Schwab ( SCHW ) insiders, who made a series of purchases and zero sales since the fallout of SVB and SBNY.

{kind=link}

Despite that, the steep fall in PNC has likely reflected significant stress in its books and forward earnings. Yet, despite the banking crisis, the market doesn't seem to think that PNC could fare worse than its IAT peers, as it outperformed them in March.

Moreover, we have yet to glean any highly negative reports suggesting that PNC could face the crisis that engulfed FRC, which would have increased the risks significantly for investors.

As such, we assessed that PNC offers investors an attractive proposition at its current valuation to play the mean-reversion opportunity from its recent decline.

However, investors looking for price action validation will need to remain patient as we have yet to glean constructive signals.

Rating: Buy.

Important Note: Investors are reminded to do their own due diligence and not rely on the information provided as financial advice. The rating is also not intended to time a specific entry/exit at the point of writing unless otherwise specified.

For further details see:

PNC Financial: The Regional Leader In The Banking Crisis