PNM - PNM Resources: The Risks Do Not Appear To Be Priced In Today

2023-03-08 19:05:01 ET

Summary

- PNM Resources, Inc.'s fourth-quarter results showed the general financial stability that we typically expect from utility companies.

- The company has benefited from the general population growth of both Texas and New Mexico, which is expected to continue in 2023.

- The merger with Avangrid still goes without an update, casting doubt on whether it will ever be accomplished.

- The company's debt load is a little higher than we really like to see, but it does not look too bad.

- The PNM Resources, Inc. stock price looks incredibly expensive considering the risks here.

On Friday, February 24, 2023, Albuquerque, New Mexico-based electric utility PNM Resources, Inc. ( PNM ) announced its fourth-quarter 2022 earnings results. At first glance, these results certainly appeared quite reasonable, as the company managed to beat the expectations of its analysts in terms of both revenues and net income. We also see here that the company’s financial performance showed a great deal of stability compared to the prior-year quarter, which is something that we tend to appreciate with electric utilities.

Unfortunately, the biggest concerns that we discussed in my previous articles regarding this company remain valid, as PNM Resources has no real strategy for the expansion of renewable energy on its grid apart from a merger with Avangrid ( AGR ). It remains uncertain whether this merger will actually happen, which could leave this company potentially appearing very backward relative to its peers over the coming months.

Earnings Results Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from PNM Resources’ fourth-quarter 2022 earnings report:

- PNM Resources reported total revenue of $575.8 million in the fourth quarter of 2022. This represents a 32.64% increase over the $434.1 million that the company reported in the prior-year quarter.

- The company reported an operating income of $54.0 million in the reporting period. This compares quite favorably to the $36.7 million that the company reported in the year-ago quarter.

- PNM Resources stated that no update on the required regulatory approval for the merger with Avangrid has been forthcoming from regulators or from the appeals court.

- The company reported an operating cash flow of $139.8 million during the most recent quarter. This was in line with the $139.4 million that it reported in the equivalent quarter of last year.

- PNM Resources reported a net income of $15.7 million in the fourth quarter of 2022. This represents a 40.18% increase over the $11.2 million that the company reported in the fourth quarter of 2021.

As mentioned, one of the defining characteristics of electric utilities like PNM Resources is that their finances tend to be remarkably stable over time. The biggest reason for this is that the provision of electricity is generally considered to be a necessity so most people will prioritize paying their electric bills over making other expenses. In addition, various government programs exist to help people pay their utility bills, which helps reduce the risk that someone will be unable to pay in a bad economy or similar event.

However, we rarely see people significantly increase their electric consumption during strong economies, so we are unlikely to see electric utilities significantly benefit in those environments. Thus, stability is pretty much what we expect. We certainly see that in these results as the company’s operating income, operating cash flow, and net income are all reasonably close to the numbers that it posted in the year-ago quarter, with a small growth margin.

That is something that is quite nice to see in the current market environment. The Federal Reserve has repeatedly stated that it is attempting to push the United States into a mild recession in order to stop the incredibly high rate of inflation plaguing it. We have seen some signs that it may be succeeding as there are some signs that American consumers may finally be starting to slow down their spending. It is almost certain that any slowdown will only affect those companies selling things that people can do without.

A utility will still get paid. After all, how many people could easily function in today’s society without electric service to their homes or businesses? Thus, PNM Resources should be better positioned to weather consumer weakness than a company that is dependent on these people spending money on luxury gadgets.

Naturally, we want to see more than mere stability from our investments. We like to see the companies that we are invested in grow and prosper. Fortunately, PNM Resources is positioned to do exactly that. One way that it is doing this is by increasing its customer base. This is something that could be at least somewhat unique as not all electric utilities have been benefiting from customer growth over the past few years.

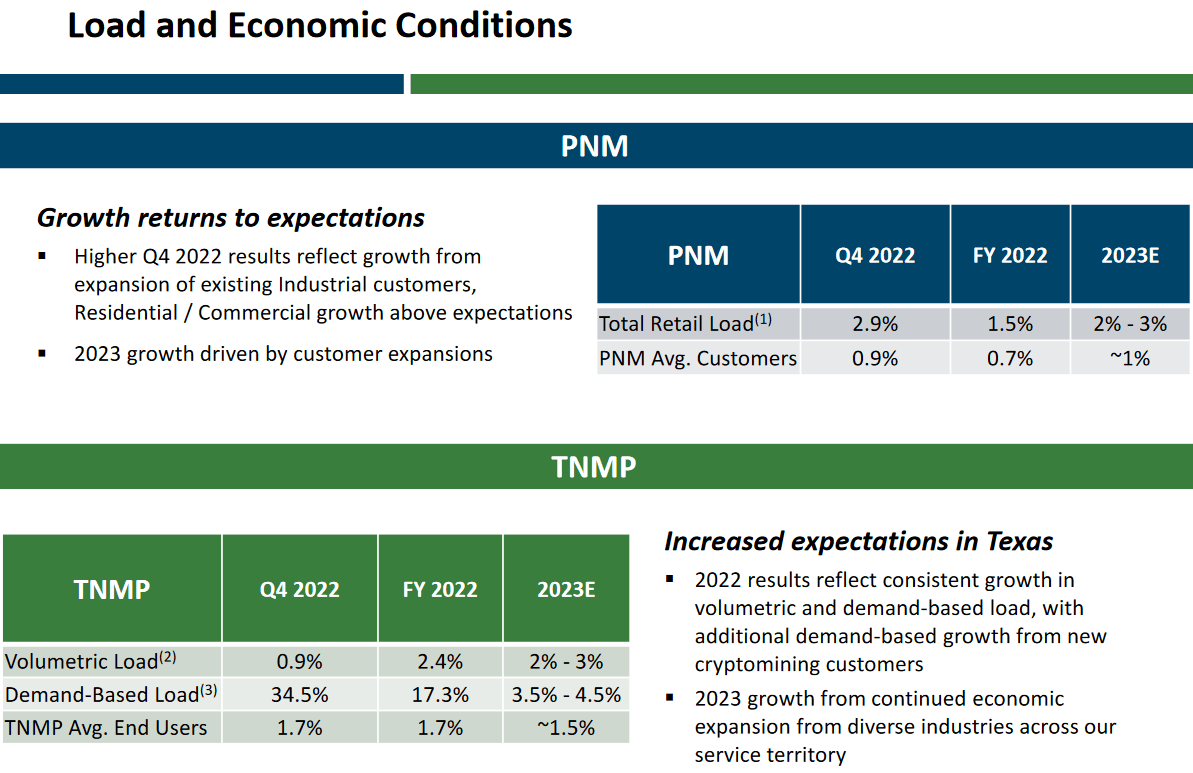

However, Texas and to a lesser degree New Mexico have been seeing their populations grow as people flee some of the high-tax northern states for warm climates and a cheaper cost of living. Over the course of 2022, PNM Resources increased its customer base by 0.7% in New Mexico and by 1.7% in Texas. The company expects that this growth will continue in 2023:

{kind=link}

One thing that we can see here too is that the actual consumption of electricity grew more rapidly than the customer base in both states. This was particularly noticeable in Texas, which saw tremendous growth due to a surge in electric demand by cryptocurrency miners in the state. Unfortunately, it seems unlikely that the company will benefit from that particular demand engine in 2023 as the economics of cryptocurrency mining have greatly soured as the prices of these digital assets have declined over the past eighteen months. PNM Resources appears to note that above as its projections for consumption growth in 2023 are much lower than it experienced in 2022, but the company should still see customer growth that will drive some increase in consumption.

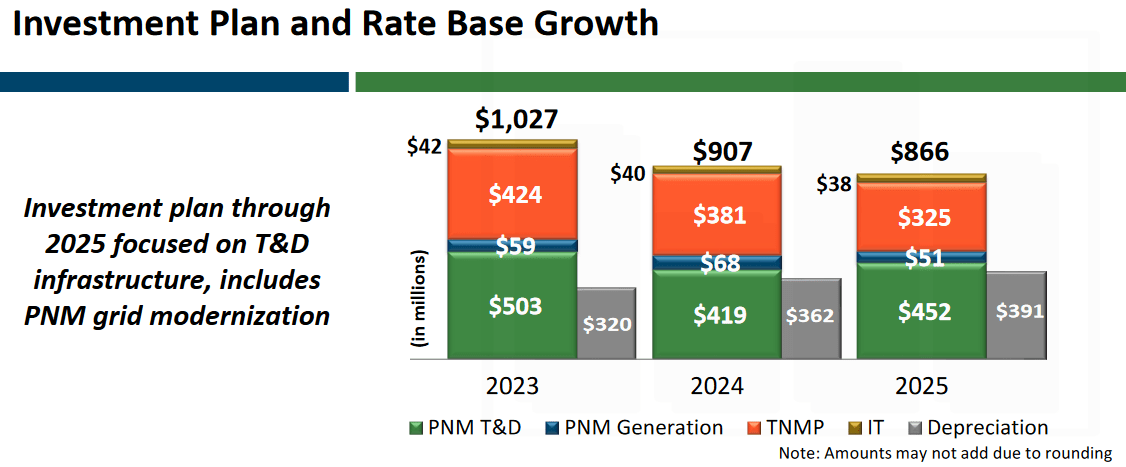

As we can see above, the growth in electric consumption demand is not likely to be sufficient to allow the company to deliver anywhere near the growth rates that many investors want to see a company deliver. Fortunately, PNM Resources does have another method that it can use to deliver earnings growth. This is by growing its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return.

As this rate of return is a percentage, any increase to its size allows the company to increase or adjust the prices that it charges its customers in order to earn that specified rate of return. The usual way that a utility will grow its rate base is by investing money into upgrading, modernizing, or expanding its utility infrastructure. PNM Resources is planning to do exactly this as the company has currently budgeted between $800 million and $1.1 billion during each of the next three years toward this task:

{kind=link}

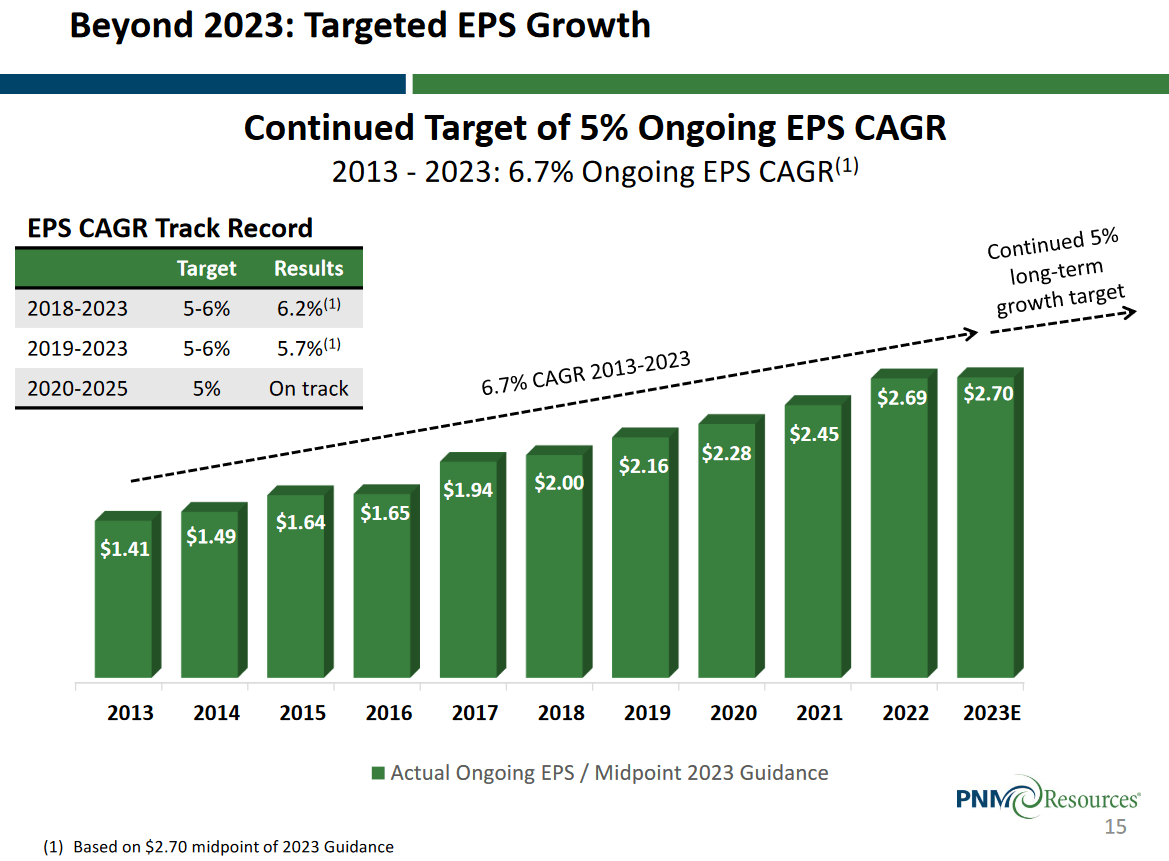

This should cause the company’s rate base to grow at an 8% compound annual growth rate over the period. However, the company does not expect that its earnings per share will grow at nearly the same rate.

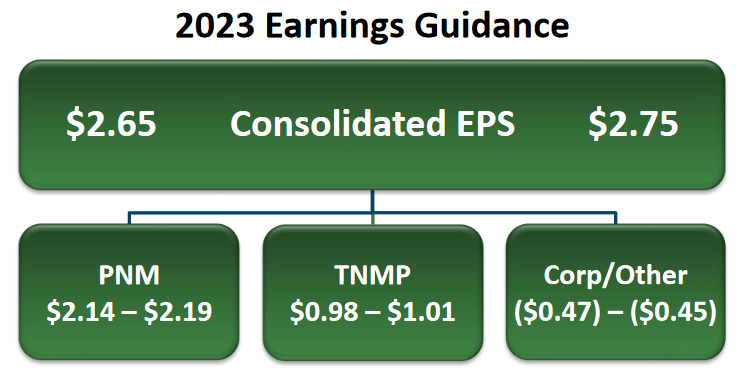

The company’s guidance provided in these results points to rather weak year-over-year growth. It stated in its earnings report that it expects to earn between $2.65 and $2.75 per share for the full-year 2023 period:

{kind=link}

The company’s ongoing reported earnings per share were $2.69 for the full-year 2022 period so it seems apparent that the company does not expect substantial earnings growth. However, the guidance midpoint is still a bit above what it actually had in 2022 so investors should be able to expect a small amount of growth here.

However, the long-term story may be a bit better. As already mentioned, PNM Resources is likely to grow its rate base at an 8% compound annual growth rate over the next three years. However, this does not mean that its earnings per share will grow at the same rate. One reason for this is that the company will need to finance the investments that it makes to grow its rate base. While it will likely finance much of it through the issuance of debt, the company is also likely to do some equity issuance in order to keep its debt ratios at a reasonable level. That will have the effect of diluting some of the benefits of the rate base growth. PNM Resources expects that it will grow its earnings per share at a 5% compound annual growth rate over the long term:

{kind=link}

This is, unfortunately, a bit lower than what many other electric utilities have guided for going forward. However, the 3.01% current dividend yield somewhat accounts for that and gives us an 8% expected average annual total return. That is certainly not too bad for an electric utility, but it is also not as attractive as the 10% that some of its peers have promised.

In previous articles on PNM Resources, I stated that the company’s plan to integrate renewables into its infrastructure is much less developed than its peers. Although the company has stated that it intends to be at zero carbon emissions by 2040, it has not offered any method through which it will accomplish that goal other than shutting down its remaining coal-fired generation plants. This is why the merger with Avangrid is so important since Avangrid is one of the largest developers of renewable energy in the country. Unfortunately, we still have no update on that merger. In its earnings press release , the company made the following statement:

“On January 3, 2022, PNM Resources and AVANGRID announced an amendment and extension of their merger agreement through April 20, 2023, and an appeal of the NMPRC decision with the New Mexico Supreme Court. The Court’s briefing schedule concluded in August 2022. No response has been provided on the companies’ request for oral argument. There is no statutory deadline for the Court to respond to the request for oral argument nor to act on the appeal.”

It seems likely that something will at least be heard within the next month since that is the deadline for the merger agreement. I will admit that I am not particularly optimistic though and PNM Resources will likely be forced to re-evaluate its own long-term plans. Any investors in the company will likely want to keep a close eye on this as it is something that is quite important for this company’s long-term future.

Financial Considerations

It is always important that we investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a business than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the money to repay the existing debt, which could cause a company’s interest expenses to increase following the rollover in certain market conditions.

That is something that could be very important today as the Federal Reserve has been hiking interest rates throughout the economy and shows no particular willingness to change this policy. In addition to this, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flow to decline could push it into financial distress if it has too much debt. Although utilities like PNM Resources tend to have remarkably stable cash flows, this is still a risk that we should not ignore as bankruptcies have occurred in the sector.

One ratio that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company’s equity can cover its debt obligations in the event of a bankruptcy or liquidation event. This second point may be more important.

As of December 31, 2022, PNM Resources had a net debt of $4.3778 billion compared to shareholders’ equity of $2.2565 billion. This gives the company a net debt-to-equity ratio of 1.94 today. That is a bit higher than the 1.86 ratio that the company had at the end of the third quarter, but this increase is small enough that it could be explained by any number of factors that should not necessarily cause alarm. Here is how PNM Resources compares to some of its peers:

| Company |

| Net Debt-to-Equity |

| PNM Resources |

| 1.94 |

| DTE Energy ( DTE ) |

| 1.85 |

| Eversource Energy ( ES ) |

| 1.45 |

| Exelon Corporation ( EXC ) |

| 1.61 |

| NextEra Energy ( NEE ) |

| 1.29 |

| CMS Energy ( CMS ) |

| 1.87 |

This is somewhat concerning, as PNM Resources currently has more leverage than any of its peers. This could be a sign that the company is employing too much debt in its financial structure and thus exposing its investors to unnecessary risks related to that debt. With that said though, it is not too far above DTE Energy and CMS Energy’s ratios and DTE Energy actually had a much higher ratio prior to the fourth quarter of 2022. Overall, this is probably okay, but I would still feel more comfortable if the company reduced its debt somewhat.

Valuation

It is always critical that we do not overpay for any company in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of an electric utility like PNM Resources, one method to value it is by looking at the price-to-earnings growth ratio. The price-to-earnings growth ratio is a modified version of the familiar price-to-earnings ratio that takes a company’s earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, very few companies have such a low ratio, particularly in today’s still-overvalued market. Thus, the best way to use this ratio today is to compare it with the company’s peers and see which stock offers the most attractive relative valuation.

According to Zacks Investment Research , PNM Resources will grow its earnings per share at a 4.22% rate over the next three to five years. This is not too far out of line with the 5% growth rate that the company’s own management is projecting, so it is probably a reasonable estimate. That would give the company a price-to-earnings growth ratio of 4.35 at the current stock price. Here is how that compares to the company’s peer group:

| Company |

| PEG Ratio |

| PNM Resources |

| 4.35 |

| DTE Energy |

| 2.85 |

| Eversource Energy |

| 2.60 |

| Exelon Corporation |

| 2.63 |

| NextEra Energy |

| 2.62 |

| CMS Energy |

| 2.38 |

This certainly points to some concern as PNM Resources appears to be substantially overvalued at the current price. All of its peers look to be providing a more attractive valuation at their current level, which when combined with the risks associated with the possible failure of the merger and the company’s lack of direction may make this a stock to avoid, at least until the price comes down a bit.

Conclusion

In conclusion, PNM Resources, Inc.’s most recent results generally gave us what we expected to see. The company delivered relatively stable cash flow and earnings year-over-year and is well-positioned to do the same in 2023 and beyond. The only real concerns here are that there is still a great deal of uncertainty surrounding the pending merger with Avangrid, which may even end up failing to happen. It also appears that PNM Resources, Inc. stock is richly valued relative to its peers, so it might be a good idea to sit on the sidelines until some of the risks fade away or the stock price declines before buying shares.

For further details see:

PNM Resources: The Risks Do Not Appear To Be Priced In Today