PII - Polaris: Cheaper Than Before But Still Not At A Discount

2023-10-04 03:16:32 ET

Summary

- Polaris has achieved organic growth but its stock price has not reflected this growth.

- The company currently invests quite heavily in capital expenditures and R&D to create further opportunities to capture market share globally.

- The stock seems pretty risky, as PII holds a good amount of debt and operates in a cyclical industry.

- Although the P/E ratio is significantly lower than historically, I don't believe the current price is a buy level yet.

Polaris ( PII ) manufactures and sells outdoors vehicles. The company has achieved a good amount of organic growth in the past years, but the growth in revenues and EPS hasn't translated into a rising stock price. As the company is facing tough upcoming quarters, the stock seems like a risky pick at the current moment. Also, although the company's stock hasn't risen, the valuation still doesn't seem too cheap - I have a hold rating for the time being.

The Company & Stock

Starting as a snowmobile manufacturer in 1954, Polaris has widened the company's offering into similar products - Polaris currently sells off-road vehicles, motorcycles, and boats as well as accessories in addition to snowmobiles. The majority of Polaris' revenues consist of the off-road vehicle segment including snowmobiles and quad bikes as well as similar products; in 2022, the segment made up around 75% of the company's product sales.

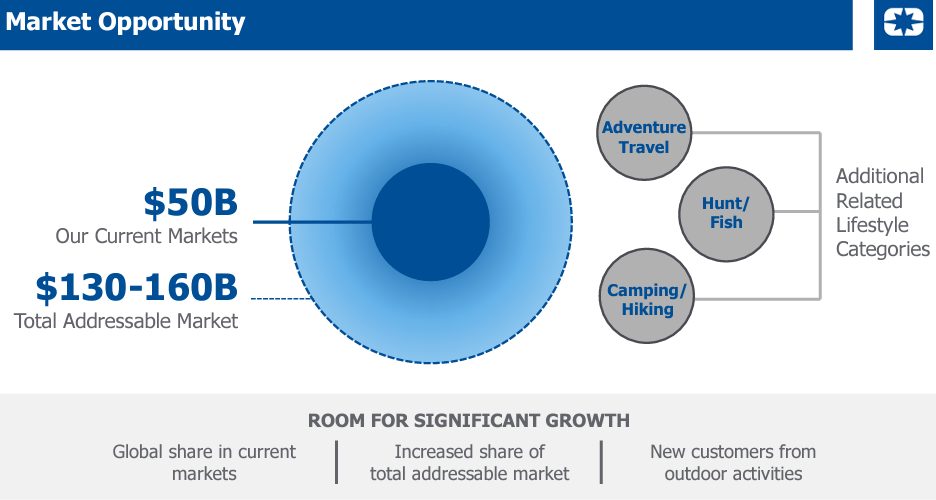

Polaris targets further growth by capturing a greater share of the total addressable market:

{kind=link}

The company invests significant amounts into R&D to improve the company's offering and to create new growth avenues through innovation.

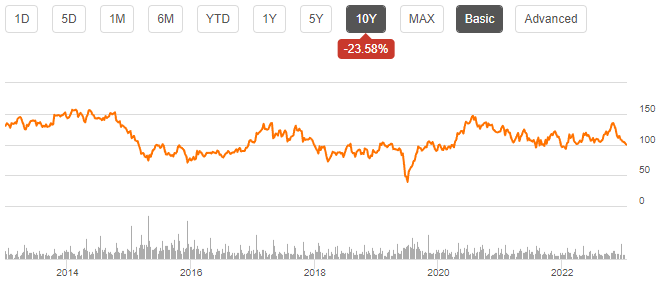

Despite the company achieving good growth in the past ten years, Polaris' stock price has decreased by around 24% in the period:

{kind=link}

The company's dividend yield doesn't really cover the poor price performance either - currently, Polaris has a modest forward dividend yield of 2.53% .

Financials

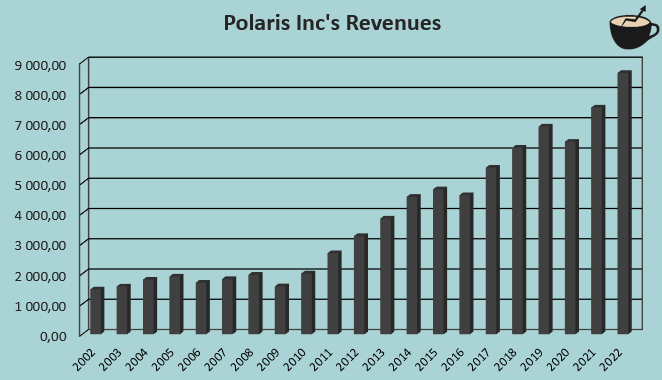

Polaris has achieved a remarkable amount of growth. The company's total revenues have grown at a compounded annual rate of 9.2% from 2002 to 2022:

{kind=link}

The last couple of years' growth has been achieved almost completely organically - Polaris' last significant acquisition was made in 2018 . Polaris does have quite a significant amount of capital expenditures as well as R&D , contributing to the organic growth - with the current investment rate, I believe Polaris should be able to achieve at least some further growth.

In the short-term Polaris' revenues seem to be in for a tougher time - the company guides for a revenue growth of 3% to 6% in 2023, and the company achieved revenue growth of 14.7% in the first half of the year - Polaris' management expects a soft market for the marine segment, contributing to the guidance that expects revenue decreases in the second half of 2023.

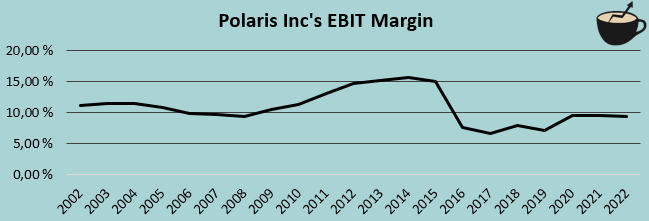

From 2002 to 2022 Polaris' average EBIT margin has been 10.8%:

{kind=link}

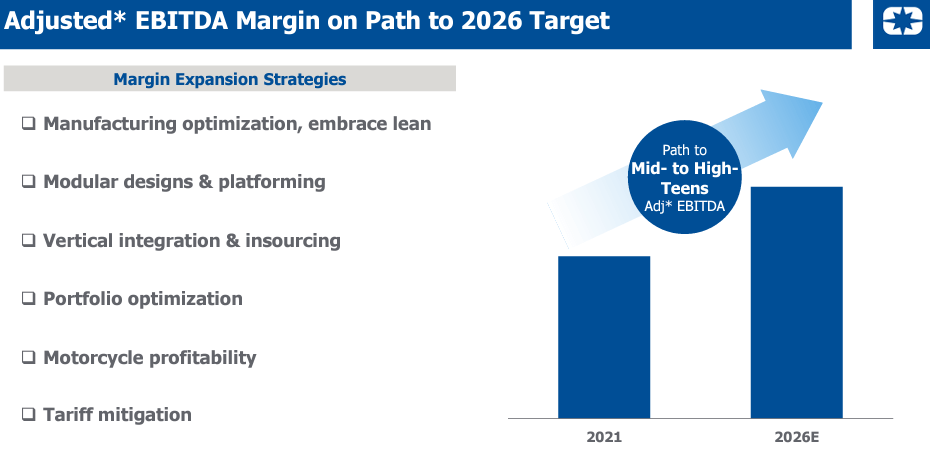

The current trailing figure of 9.4% is slightly below the long-term average. The margin is above the 2016-2022 average of 8.2%, though; in 2016, Polaris' EBIT margin fell from 15.0% in 2015 to 7.6% as a result of slightly lower revenues, a lower gross margin, as well as higher SG&A expenses. Polaris is targeting to expand its margin into one that's more in line with the long-term history:

Margin Leverage Initiatives (Polaris' CMD 2023 Presentation)

{kind=link}

Although the company has already achieved some margin leverage from 2016 levels, investors should in my opinion wait before expecting too much future expansion.

Polaris has around $2.1 billion in long-term debt on the company's balance sheet . Of the debt, around $554 million is in the current portion. The amount of debt seems quite large as Polaris' market capitalization is currently at around $5.8 billion and the company operates in a highly cyclical industry. I do believe that Polaris can manage to meet the debt payments, though, as the company does have a cash balance around $340 million and a currently healthy earnings level.

Valuation

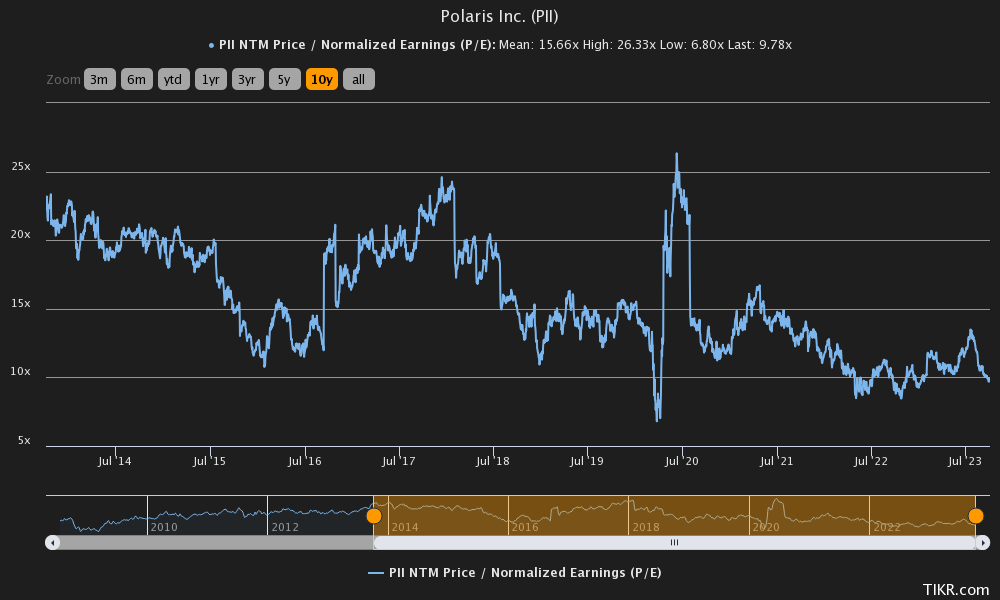

The rising earnings haven't correlated with the stock's price - as earnings have risen, Polaris' stock price has stayed mostly stable as the P/E ratio has fallen. Currently, Polaris trades at a forward price-to-earnings ratio of 9.8, around 38% below the ten-year average of 15.7:

{kind=link}

The question relies on what sort of valuation seems reasonable for Polaris: is the low P/E ratio earned as a result of tough upcoming quarters, higher interest rates, and a cyclical industry? To estimate what I believe the stock should be worth, I constructed a discounted cash flow model as usual.

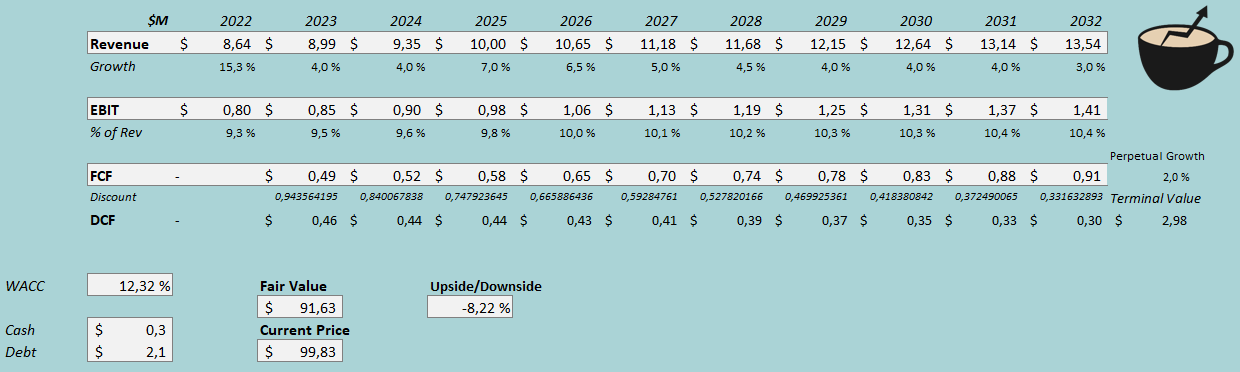

In the model, I estimate a growth of 4% for the current year - the estimate is in line with the management's current guidance. The growth rate implies a weak second half of 2023, as revenues grew by 14.7% in the first half - I estimate the tough period to last into 2024, as I estimate a growth of 4% for the year as well. Beyond 2024, I expect Polaris to execute on its plans to capture further market share, as I have a growth of 7% for 2025. After the year, I estimate the company's growth to slow down in steps into a perpetual growth of 2%.

The EBIT margin of 9.5% in 2023 is in line with Polaris' current guidance, 0.2 percentage points above 2022. Going forward from 2023, I estimate Polaris to achieve some margin expansion - in my DCF model, the EBIT margin rises by 0.9 points from 2023 into a margin of 10.4%. As Polaris invests quite heavily to achieve further growth, I estimate the company's cash flow conversion to be somewhat poor. The mentioned estimates along with a cost of capital of 12.32% craft the following DCF model scenario with a fair value estimate of $91.63, around 8% below the current price:

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2, Polaris had around $31 million in interest expenses. With the company's current amount of interest-bearing debt, Polaris' annualized interest rate comes up to 6.13%. The company uses a good amount of debt to leverage its financing - I estimate a long-term debt-to-equity ratio of 25%.

On the cost of equity side, I use the United States' 10-year bond yield of 4.71% as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate. Yahoo Finance estimates Polaris' beta at 1.68 - the company operates in a cyclical industry. Finally, I add a liquidity premium of 0.25% crafting a cost of equity of 14.89% and a WACC of 12.32%, used in the DCF model.

Takeaway

Although the P/E ratio is significantly below Polaris' long-term average, I don't think the price represents too good of an entry point yet. The company is facing tough quarters in H2/2023, and the future growth rate has somewhat of a limited visibility. The company has a somewhat high amount of debt, and operates in a cyclical industry, raising the risk level for investors. As my DCF model estimates the stock to be roughly fairly valued with a small downside, I have a hold rating for the stock.

For further details see:

Polaris: Cheaper Than Before, But Still Not At A Discount