LSRCF - Polen Capital International Growth Portfolio Manager Commentary Q2 2023

2023-07-20 22:37:00 ET

Summary

- Polen Capital is a global independently-owned growth equity boutique, led by an experienced team of investment professionals who are committed to preserving and growing the assets of our clients through a prudent and disciplined long-term investment approach.

- The top relative contributors to the Portfolio’s performance over the second quarter included Sage Group, ICON, and Shopify. These were also the top contributors on an absolute basis.

- The Portfolio continues to hold a concentrated collection of quality companies. With valuations reset lower across the Portfolio, we believe prospects for solid earnings growth over the coming three to five years are compelling.

Summary

- During the second quarter, the International Growth Composite Portfolio (the “Portfolio”) outpaced the MSCI ACWI Index.

- On the back of better-than-expected corporate results, international stocks have continued moving higher off the lows they reached in October 2022.

- The top relative contributors to the Portfolio’s performance over the second quarter included Sage Group, ICON, and Shopify. These were also the top contributors on an absolute basis.

- The most significant relative detractors from performance included Teleperformance (TLPFF), Evolution AB (EVVTY), and MercadoLibre (MELI). The top three detractors to absolute performance were slightly different, including Kering (PPRUF) instead of MercadoLibre.

- We initiated a new position in Lasertec, added to existing positions in Bunzl (BZLFF) and HDFC Bank (HDB), and trimmed existing positions in Kering, LVMH, and adidas (ADDYY). We did not eliminate any positions during the quarter.

- The Portfolio continues to hold a concentrated collection of quality companies. With valuations reset lower across the Portfolio, we believe prospects for solid earnings growth over the coming three to five years are compelling.

{kind=link}

The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Periods over one-year are annualized. Performance figures are presented gross and net of fees and have been calculated after the deduction of all transaction costs and commissions, and include the reinvestment of all income. Please reference the GIPS Report which accompanies this commentary.

The commentary is not intended as a guarantee of profitable outcomes. Any forward-looking statements are based on certain expectations and assumptions that are susceptible to changes in circumstances. Opinions and views expressed constitute the judgment of Polen Capital as of the date herein, may involve a number of assumptions and estimates which are not guaranteed, and are subject to change.

All company-specific information has been sourced from company financials as of the relevant period discussed.

Commentary

In the second quarter, international stocks continued moving higher. Since hitting lows in October of 2022, international equities have rallied more than 20%. Corporate results have been more resilient than investors feared last fall. Many economies continue to grind along at low growth rates, with higher inflation than policymakers would like. Of course, high inflation demands policy responses. These factors create a strange mix of uninspiring macro growth prospects, yet a dearth of policy accommodation on the horizon.

Fortunately, we seek to gear our concentrated Portfolio for growth rates well above what the broader economy and the international benchmark may deliver.

European markets, which rallied off the October lows, slowed in May as data began pointing to contractions in key markets like Germany and Sweden. The European Central Bank (ECB) continues to drive policy rates higher in the face of persistent inflation. U.S. market hype around artificial intelligence ((AI)) hit a fever pitch in May and may have spurred investor flows away from European equities back to the U.S.

China provides an interesting counter to many trends seen elsewhere. Markets eagerly anticipated strong post-COVID reopening growth last fall, but China’s reopening has been a dud. Note how COVID responses in China ran counter to supporting consumer spending - a sharp departure from the combined monetary and fiscal largesse many Western countries used during the pandemic. Of course, Western policies played significant roles in stoking inflation. Now, more than six months after reopening, China’s inflation statistics are grinding towards outright deflation each month. A battery of other issues matter in China, so we can’t pin poor growth and inflation solely on COVID responses.

However, juxtaposing China’s weak inflation with the West’s persistent inflation does prompt questions about the government’s stance towards consumer spending as an economic driver.

We believe the Portfolio, now trading at slightly more than 20x forward price-to-earnings (P/E) is compellingly valued as it continues to be geared for weighted average growth at above- market rates. We believe the Portfolio is well stocked with competitively advantaged businesses.

Our optimism about the Portfolio over the coming five years stems from our view of each company’s strengths and growth potential.

As ever, we remain confident in the philosophy driving our approach to growth investing.

Portfolio Performance & Attribution

During the second quarter, the International Growth Composite Portfolio (the “Portfolio”) returned 5.92% gross and 5.70% net of fees, respectively, compared to the 2.44% return of the MSCI ACWI ex US Index (the “Index”).

The top three contributors to relative performance during the second quarter were Sage Group (SGGEF) , ICON (ICLR) , and Shopify (SHOP) . These were also the top contributors on an absolute basis.

Sage Group reported favorable 1H23 results during the quarter, with recurring revenues growing 12%. Additionally, management raised full-year revenue guidance. The company’s cloud solutions continue to gain traction with customers and should continue to drive overall sales growth in the double-digit range. ICON’s stock price rebounded during the second quarter after a weak start to the year. Despite a challenging backdrop for biotech funding, the company continues to generate mid-single-digit organic revenue growth. Further, its acquisition of PRA Health has now been completed, positioning ICON as the number two global player in the contract research organization (“CRO”) industry. Finally, Shopify’s stock price has seen strong performance during both the second quarter and on a year-to-date basis. The company’s profitability should continue to improve from here, and the e- commerce market has been reaccelerating, as expected.

Additionally, the recent announcement that the company would divest its dilutive fulfillment operations should further augment long-term margins and was well-received by shareholders.

The top three detractors to performance on a relative basis during the second quarter were Teleperformance , Evolution AB , and MercadoLibre . The top three detractors to performance on an absolute basis during the second quarter were Teleperformance , MercadoLibre , and Kering .

Teleperformance , the world’s leading outsourced customer service provider, was the largest detractor to relative performance during the second quarter. The company’s stock price has been under pressure the past few months—a weaker IT services backdrop combined with concerns about generative AI disrupting Teleperformance’s business model have negatively impacted short-term returns. Despite this near-term weakness, we continue to have conviction that Teleperformance is, at a minimum, capable of high-single-digit revenue organic revenue growth, and we view the concerns around generative AI to be overblown. In our opinion, the stock’s current NTM P/E of ~10x is compellingly undervalued.

The next two largest relative performance detractors during the second quarter were Evolution AB and MercadoLibre , respectively. Both businesses continue to perform well, and recent underperformance appears to be more a case of the stock prices “taking a breather” after very strong performance in the first quarter of this year.

Portfolio Activity

During the quarter, we initiated a new position in Lasertec (LSRCF) , added to existing positions in Bunzl and HDFC Bank , and trimmed existing positions in Kering , LVMH , and a didas . We did not eliminate any positions during the quarter.

Lasertec , a Japan-based semi-cap equipment company, was the only new addition during 2Q23. It is the leading global provider of actinic photo-mask inspection ((APMI)) machinery to the semiconductor industry. Lasertec operates in an important niche that is focused on process standardization and efficiency in manufacturing. The company’s machines are often the best way for leading-edge chip manufacturers to inspect the photomasks (which can be thought of like photo negatives) that are used to imprint the smallest features onto the surface of wafers. As ASML’s extreme ultraviolet lithography (“EUV”) becomes the new standard in the process of creating leading-edge chips that are smaller and more powerful, there’s naturally a higher utilization of EUV photomasks, which in turn requires greater inspection volumes. We believe Lasertec trades at an attractive valuation considering the >35% earnings growth we expect it to deliver over the next few years from secular growth tailwinds.

Regarding the additions to existing positions in Bunzl and HDFC Bank , the thesis remains unchanged. With Bunzl, a UK-based value-added distributor serving various industries, the company has driven consistent double-digit growth over the past few decades on the back of modest organic growth and solid inorganic growth fueled by skilled capital allocation. At a stage in the economic cycle where it’s likely that more target companies might be willing to sell, our research shows that Bunzl is well-positioned to make opportunistic acquisitions with significant balance sheet capacity. With HDFC Bank, the company will close its merger with its former parent (HDFC Limited) in the second half of 2023, and this should continue to drive scale and breadth. Further, India’s economy is in better shape than many around the world, supported by lower debt levels, younger demographics, and higher average growth rates. These factors combined could make India a market of relative strength in the coming five years.

We funded the additions to these positions through the trims to our existing positions in Kering , LVMH , and adidas . With the luxury conglomerates, after a period of significant outperformance and rising valuations, we believe the go-forward earnings growth and returns for both companies could be more modest. That said, we still have high conviction in the companies’ strong competitive advantages and in their ability to continue compounding capital over the medium term. As it pertains to Adidas, we trimmed the position back after a significant rebound from the lows reached late last year. New management has been a welcome change after a few significant missteps. While we are very excited about the path set forth by new CEO Bjorn Gulden, we also acknowledge it will take time to turn the ship. We believe the benefits of scale and brand recognition will enable positive change at Adidas and will continue to monitor progress on the path to recovery from here.

Outlook

Policy makers are compelled act to counter inflation. Employment may be sacrificed to tame it. Should this come to pass, then economic growth could suffer. Weak economic growth prospects and above-average inflation rates in most markets are not the best combination for business expansion. Stagflation requires a selective approach to stock investment as pockets of strength can drive Portfolio returns. Despite an uninspiring macro backdrop, we believe the Portfolio is well positioned to deliver robust growth over the coming five years.

Team Update

Effective June 30, 2023, Bryan Power joined Damon Ficklin and Jeff Mueller as co-portfolio manager of the Global Growth strategy. Jeff Mueller has decided to retire for family reasons and will relinquish his responsibilities on the Large Company Growth Team effective December 31, 2023. While saddened by his departure, we celebrate Jeff's decade-long contribution and commitment to Polen Capital. We also appreciate him supporting this transition through the end of the year. Given Bryan’s strong analytical work and thought leadership on the team, he was promoted to the Director of Research on January 1, 2022, where he has been responsible for managing the Large Company Growth Team Analysts and our global research effort. Bryan will continue to serve as the Director of Research and is well prepared to succeed Jeff as co-portfolio manager for Global Growth.

We have built a deep bench of experienced talent on the Large Company Growth Team that allows us to adapt over time. Please join us in congratulating Bryan on his promotion and wishing Jeff and his family all the best.

{kind=link}

{kind=link}

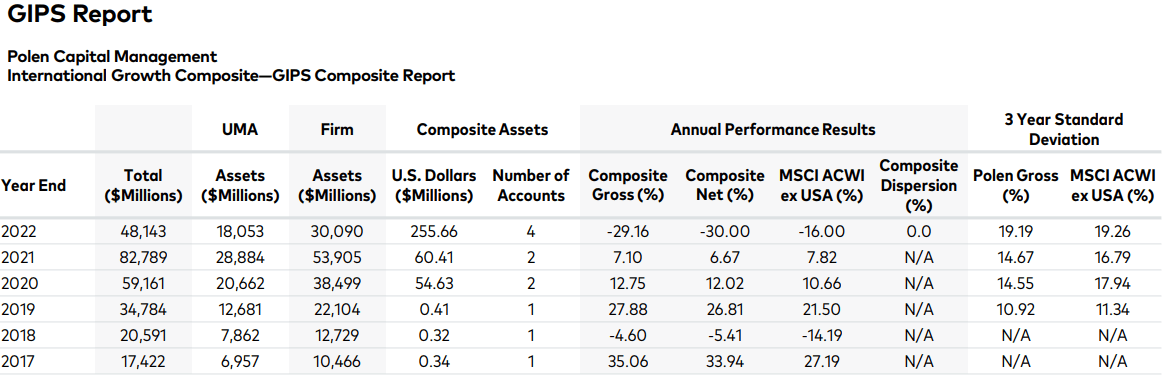

1 A 3 Year Standard Deviation is not available for 2017 and 2018 due to 36 monthly returns are not available.

Some versions of this GIPS Report previously included assets of the Firm's wholly-owned subsidiary in the 2022 Firm Assets figure, in error. The figure above has been corrected to no longer count assets at the subsidiary level. Total assets and UMA assets are supplemental information to the GIPS Composite Report. N/A - There are five or fewer accounts in the composite the entire year. While pitch books are updated quarterly to include composite performance through the most recent quarter, we use the GIPS Report that includes annual returns only. To minimize the risk of error we update the GIPS Report annually. This is typically updated by the end of the first quarter.

GIPS Report

The International Growth Composite created and incepted on January 1, 2017 contains fully discretionary international growth accounts that are not managed within a wrap fee structure and for comparison purposes is measured against MSCI ACWI (ex-USA). Effective January 2022, fully discretionary large cap equity accounts managed as part of our International Growth strategy that adhere to the rules and regulations applicable to registered investment companies subject to the U.S. Investment Company Act of 1940 and the Polen International Growth Collective Investment Trust were included into the International Growth Composite. The accounts comprising the portfolios are highly concentrated and are not constrained by EU diversification regulations.

Polen Capital Management claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Polen Capital Management has been independently verified for the periods April 1, 1992 through June 30, 2022. The verification reports are available upon request. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm's policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm- wide basis. Verification does not provide assurance on the accuracy of any specific performance report.

Polen Capital Management is an independent registered investment adviser. Polen Capital Management invests exclusively in equity portfolios consisting of high-quality companies but also has a subsidiary, Polen Capital Credit, LLC, that specializes in high yield securities and special situations investing. A list of all composite and pooled fund investment strategies offered by the firm, with a description of each strategy, is available upon request. In July 2007, the firm was reorganized from an S-corporation into an LLC and changed names from Polen Capital Management, Inc. to Polen Capital Management, LLC. Results are based on fully discretionary accounts under management, including those accounts no longer with the firm.

Effective January 1, 2022, composite policy requires the temporary removal of any portfolio incurring a client initiated significant net cash inflow or outflow of 10% or greater of portfolio assets. The U.S. Dollar is the currency used to express performance. Returns are presented gross and net of management fees and include the reinvestment of all income. Net of fee performance was calculated using either actual management fees or highest fees for fund structures. The annual composite dispersion presented is an asset-weighted standard deviation using returns presented gross of management fees calculated for the accounts in the composite the entire year. Policies for valuing investments, calculating performance, and preparing GIPS Reports are available upon request.

The separate account management fee schedule is as follows: Institutional: Per annum fees for managing accounts are 85 basis points (0.85%) on the first $50 Million and 65 basis points (0.65%) on all assets above $50 Million of assets under management. HNW: Per annum fees for managing accounts are 160 basis points (1.60%) of the first $500,000 of assets under management and 110 basis points (1.10%) of amounts above $500,000 of assets under management. Actual investment advisory fees incurred by clients may vary.

The per annum fee schedule for managing the Polen International Growth Fund, which is included in the International Growth Composite, is 85 basis points (.85%). The total annual fund operating expenses are up to 135 basis points (1.35%). As of 4/30/2022, the mutual fund expense ratio goes up to 1.29%. This figure may vary from year to year. The per annum all-in fee* schedule for managing the Polen International Growth Collective Investment Trust, which is included in the International Growth Composite, goes up to 70 basis points (.70%). *The all-in fee (which is similar to a total expense ratio) includes all administrative and operational expenses of the fund as well as the Polen Capital management fee.

Past performance does not guarantee future results and future accuracy and profitable results cannot be guaranteed. Performance figures are presented gross and net of management fees and have been calculated after the deduction of all transaction costs and commissions. Portfolio returns are net of all foreign non-reclaimable withholding taxes. Reclaimable withholding taxes are reflected as income if and when received. Polen Capital is an SEC registered investment advisor and its investment advisory fees are described in its Form ADV Part 2A. The advisory fees will reduce clients’ returns. The chart below depicts the effect of a 1% management fee on the growth of one dollar over a 10 year period at 10% (9% after fees) and 20% (19% after fees) assumed rates of return.

The MSCI ACWI ex USA Index is a market capitalization weighted equity index that measures the performance of large and mid-cap segments across developed and emerging market countries (excluding the U.S). The index is maintained by Morgan Stanley Capital International.

The volatility and other material characteristics of the indices referenced may be materially different from the performance achieved. In addition, the composite’s holdings may be materially different from those within the index. Indices are unmanaged and one cannot invest directly in an index.

The information provided in this document should not be construed as a recommendation to purchase or sell any particular security. There is no assurance that any securities discussed herein will remain in the composite or that the securities sold will not be repurchased. The securities discussed do not represent the composite’s entire portfolio. Actual holdings will vary depending on the size of the account, cash flows, and restrictions. It should not be assumed that any of the securities transactions or holdings discussed will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

A complete list of our past specific recommendations for the last year is available upon request.

{kind=link}

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Polen Capital International Growth Portfolio Manager Commentary Q2 2023