AZPN - Polen US SMID Company Growth Q2 2023 Portfolio Manager Commentary

2023-07-31 22:30:00 ET

Summary

- Polen Capital is a high-conviction growth investment manager. We scour the globe in search of the highest quality, sustainable companies to invest in.

- Market sentiment can shift rapidly, but a disciplined investment process and resilient portfolio can help navigate changing narratives.

- Effective management teams and robust business models are crucial for long-term success in challenging economic backdrops.

- High-quality businesses with positive free cash flow and strong balance sheets are better equipped to make prudent decisions regarding capital allocation.

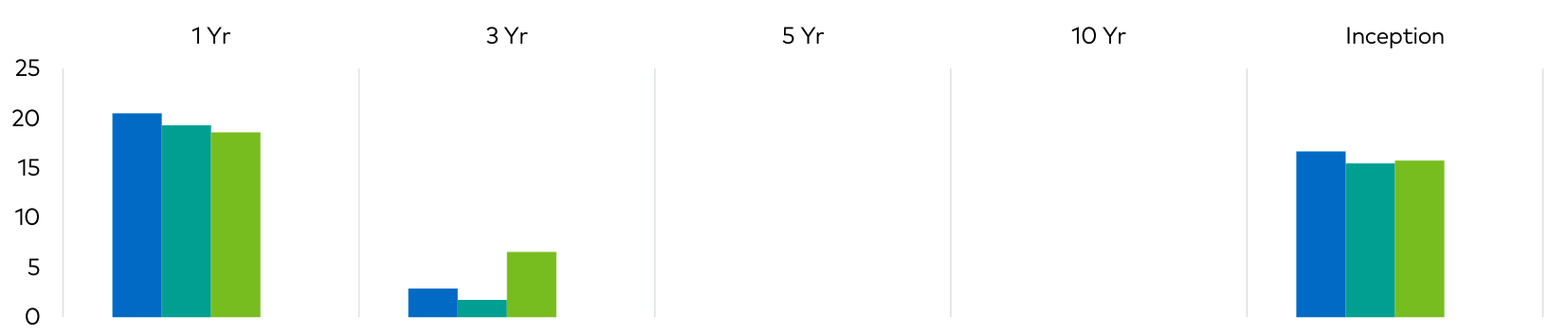

Seeks Growth & Capital Preservation (Performance (%) as of 6-30-2023)

{kind=link}

| Qtr |

| YTD |

| 1 Yr |

| 3 Yr |

| 5 Yr |

| 10 Yr |

| Inception |

| Polen US SMID Company Growth (Gross) |

| 5.94 |

| 18.45 |

| 20.50 |

| 2.86 |

| - |

| - |

| 16.66 |

| Polen US SMID Company Growth ((Net)) |

| 5.82 |

| 17.98 |

| 19.31 |

| 1.74 |

| - |

| - |

| 15.48 |

| Russell 2500 Growth |

| 6.42 |

| 13.38 |

| 18.58 |

| 6.56 |

| - |

| - |

| 15.74 |

| The performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher. Periods over one-year are annualized. Performance figures are presented gross and net of fees and have been calculated after the deduction of all transaction costs and commissions, and include the reinvestment of all income. Please reference the GIPS Report which accompanies this commentary. The commentary is not intended as a guarantee of profitable outcomes. Any forward-looking statements are based on certain expectations and assumptions that are susceptible to changes in circumstances. Opinions and views expressed constitute the judgment of Polen Capital as of the date herein, may involve a number of assumptions and estimates which are not guaranteed, and are subject to change. |

Commentary

The second quarter provided yet another demonstration of how rapidly market sentiment can shift. Whether it’s the ongoing debate over hard or soft landing, pessimism over bank failures and tightening credit standards, or optimism around AI, it is abundantly clear that market narratives can change quickly. For some, this can create a false urgency to react, leading to poor decision-making. We believe the answer to this dilemma is a time-tested and disciplined investment process and a portfolio built for resilience. This comes from our unwavering commitment to investing in what we view to be high-quality long-term compounders constructed to thrive in any environment. This allows us to cut through the noise, maintain a long-term perspective, and avoid being swayed by confusing short-term signals.

We also seek to construct the Portfolio for resiliency by investing in companies across the growth spectrum, across different sectors and industries, and at varying stages of business maturity. Although our Portfolio may be concentrated, implementing these layers of diversification can provide stability.

Our unique framework for assessing quality is called the Flywheel. It is a tool not just for identifying durable compounders but also for consistency and clarity of decision making. Recently, clients have asked how the Flywheel framework protects against more challenging economic backdrops. While all five Flywheel criteria contribute, it’s hard to overstate the importance of effective management teams, and robust business models.

We believe effective management teams play a crucial role in determining the long-term success or failure of the companies we observe. This is true in the best times, especially in more difficult periods. Reflecting on the past few years, there’s been no shortage of challenges. These included a global pandemic, supply chain disruptions, historically high inflation, rising interest rates, slowing economic growth, and a banking crisis, on top of each company’s idiosyncratic challenges. Scaling a company through these rapidly changing conditions requires making difficult decisions to address complex issues.

Successfully navigating these obstacles and seizing opportunities demands a unique combination of skills, experience, and mindset possessed by only a few management teams. To identify these effective management teams, we’re looking for specific markers. Among others, these include a track record of value-creating reinvestment, a long-term orientation, operational excellence, a demonstrated ability to be agile, a culture that attracts and retains top talent above industry standards, a measured and systematic approach to taking risks, and a guiding vision around doing the right thing. Periods like this can set the stage for a well-run company to extend its advantage vs. competitors over the long term.

Conversely, management teams that have not been battle-tested risk becoming too focused on the prevailing narrative of the day to the detriment of long-term value creation.

An emphasis on robust business models is another element of the flywheel we underscore as critically important during this unique time. Companies that have grown accustomed to the near-zero interest rate environment of the past decade are now facing a new reality. They had become reliant on easily accessible and cheap external funding, allowing unprofitable businesses to sustain themselves longer than they otherwise would have.

However, the current scenario of higher interest rates and stricter credit standards has real implications for these businesses. They now need to rein in expenses and abandon long-term value-creating projects. Becoming profitable is often more than just flipping a switch. A robust and sustainable business model results from consistent discipline applied over many years. Therefore, we exclusively focus on companies with solid balance sheets, high returns on capital, positive free cash flow, and robust underlying business models. These qualities enable our businesses to fund their own growth, even in a challenging macro environment.

During times like these, high-quality businesses can continue to invest in long- term growth initiatives, positioning themselves to gain market share from competitors.

We believe companies with positive free cash flow, which comprise 98% of our Portfolio, and strong balance sheets are better equipped to make prudent decisions regarding capital allocation.

This may involve opportunistic share repurchases, engaging in value-accretive acquisitions, investing in the brand, product development, international expansion, research and development, and more.

Following Silicon Valley Bank's failure at the end of the first quarter and the subsequent turmoil in regional banks, access to capital has become even more constrained. With over 40% of the Russell 2500 Growth unprofitable and 11% more than 5x levered, many firms will be unable to engage in these strategic behaviors. Thus, prioritizing financially resilient companies has become increasingly more essential.

As a reminder, we require that all five flywheel conditions be in place, along with at least a mid-teens internal rate of return ((IRR)), to make an investment. The current opportunity set presents opportunities above our historical IRR norms. For those who are long-term oriented, patient, and discerning, this remains an excellent time to invest in SMID cap companies.

Portfolio Performance & Attribution

During the second quarter, the U.S. SMID Company Growth Composite Portfolio (PBMIX), the “Portfolio”, returned 5.94% gross and 5.82% net of fees, respectively, compared to the 6.42% return of the Russell 2500 Growth Index (the “Index”).

The top contributors to the Portfolio’s relative performance in the second quarter included The Trade Desk ( TTD ), Dynatrace ( DT ), and Copart ( CPRT ). These were also the top contributors on an absolute basis.

The Trade Desk , a leading demand-side programmatic advertising platform, has continued to deliver strong results despite a challenging advertising environment. Additionally, as the market increasingly appreciates the real applications AI can have in some business models, The Trade Desk stands out as a leader with the opportunity to compound its advantage looking ahead. The company’s success comes from increasing penetration in the nascent connected TV (“CTV”) market, which has steadily taken share from linear television in recent years. We expect this secular tailwind to continue and dampen whatever short-term headwinds the digital advertising market might face in the coming quarters/years.

Dynatrace , a provider of cloud-based application monitoring for large corporations, was another top contributor to performance. The company delivered another set of solid results and raised revenue guidance for the quarter and year. As companies continue to migrate operations and systems to the cloud, the emergence of generative AI as a productivity- enhancing tool also significantly increases the complexity of the development and delivery of software products. This only goes to underscore Dynatrace's importance to a large cloud environment.

Lastly, Copart , a global provider of online vehicle auctions for automotive resellers, continues to compound its value in the face of difficult comparisons and used car pricing normalization. The company is benefitting from structural advantages owing to the long-term oriented investments the company has made that others in the industry have not.

The most significant detractors from the Portfolio’s relative performance in the quarter included Revolve Group ( RVLV ), ETSY , and Aspen Technology ( AZPN ) . These were also the top detractors on an absolute basis.

Revolve Group , a next-generation online retailer, established itself as a leading premium fashion destination for Millennial and Generation Z female customers. This quarter, Revolve was compared against its second biggest “re-opening” quarter last year, when revenue was up almost 60% YoY. While Revolve is undoubtedly navigating an increasingly challenging consumer backdrop, the result of revenue down 3% against these difficult comparisons was a solid outcome. Over the past 20+ years, this management team has proven adept at steering the business through challenging macro environments, and we expect them to continue making the right decisions to position the company for success over the long term.

Etsy , an online marketplace for handmade and vintage goods, saw shares decline despite reporting better-than-expected results. Investors appear to be expressing concerns around a softening macro backdrop as consumer demand shifts increasingly from goods to services. We think it’s worth taking a step back to acknowledge how impressive Etsy has retained the massive growth in gross merchandise sales following the pandemic. We continue to have confidence in the long-term trajectory of the business.

Finally, Aspen Technology , a provider of asset optimization software, was a top detractor in the period. Of note, Aspen Technology was the approach’s top relative contributor in 2022 and one of only a few names that delivered positive absolute performance amidst the challenges related to inflation and rising interest rates. The stock continued its strong run of performance into 2023 ahead of reporting 4Q22 earnings, where estimates came in lower than expectations, and management cautioned around a weaker software spending outlook for the remainder of the year and spoke of integration pains related to the Emerson transaction. We believe these issues are temporary.

Portfolio Activity

This quarter’s activity included three new initiations— Alight ( ALIT ), SiTime ( SITM ), and Morningstar ( MORN ) —along with a modest trim to our existing position in Copart .

Alight is a leading cloud-based provider of employee engagement tools and solutions for workplace benefits, payroll, administration, and wealth services. Alight was founded 25 years ago and, in keeping with the flywheel, has a long history of consistently growing recurring revenue. Over the past several years, Alight has deployed capital towards several value-add acquisitions and developing a technology platform for “business process as a service” or “BPaaS.” This has only furthered Alight’s unique positioning and opened significant growth opportunities. To give a sense of their scale, they serve 15% of the US workforce, and their solutions can be found in 50% of Fortune 500 companies. Alight’s human capital BPaaS solutions combine Software as a Service (“SaaS”) capabilities, artificial intelligence, automation, and data analytics to deliver superior outcomes across a comprehensive Portfolio of services for employees and employers. We expect Alight to drive consistent growth through upsell/cross-sell opportunities with existing clients and from new customer wins, international expansion, and M&A.

SiTime makes silicon microelectromechanical systems (“MEMS”) solutions that enable precision timing in various electronic devices. The company’s products are increasingly important as new high-tech applications and emerging industries—5G, self-driving, data centers, wearables, and the military/space market—require higher precision in timing devices and materials vs. the historical standard, quartz. As the category creator with a dominant (85%+) market share, SiTime stands well positioned to benefit as they take share from the legacy quartz timing solution, and the addressable market for their solutions continues to grow.

Morningstar is a leader in providing investment and wealth management data, software, and solutions to the financial services industry. Besides their own “Morningstar” brand, which is held in high regard by investment professionals and financial advisors for their decades-long history of providing cost-effective insight and transparency to a wide breadth of clients, they also own popular services like “Pitchbook,” “Sustainalytics” and “DBRS.” Management has spent the last four years investing heavily in several business lines (like private markets data and ESG) that have depressed margins in the near term but should provide durable growth opportunities for many years. As the company reaps the benefits from these investments over the coming years, we expect margins to track towards their prior levels of 20-25% (from current low-to-mid teens). Combined with low-double- digit revenue growth and management’s long history of opportunistic share buybacks, this should translate into ~20% EPS growth over our holding period.

By contrast, we trimmed our position in Copart . While we maintain our conviction in the long-term opportunity, the stock is up 50% YTD and the relative valuation has become less attractive. As a result, we used this trim as a source of funds to add to Alight, SiTime, and Morningstar, where the risk/reward is more compelling.

Outlook

Our outlook is unchanged from last quarter. The current environment continues to be highly uncertain. SMID cap companies as an asset class are heavily discounted relative to history. Still, risks are also significant, whether it be inflation and the path of interest rates, credit availability, or the economy.

Despite the uncertainty, we operate with clarity and conviction. We believe that owning great businesses with durable growth and high returns on capital with a significant runway for reinvestment at high returns and further buying those businesses at a discount to their long-term valuation creation potential will drive great returns for our clients.

This underscores why we stay focused on the long-term and concentrated on competitively advantaged, financially flexible businesses.

We believe that always owning businesses with solid balance sheets and the ability to reinvest in any environment trumps short- term temptations to own lower-quality businesses driven by interest rates, commodity prices, or leverage.

While the short-term view is heavily influenced by fear and uncertainty, the long-term picture is far clearer than the market would suggest (even at higher interest rates), and by and large, our long-term view and conviction in our Portfolio companies is unchanged. This allows us to confidently sift through the noise and take advantage of price dislocations.

Despite all the challenges, the opportunity set in SMID caps is attractive regarding valuation and the prospect of persistent growth. High-quality SMID cap companies have more significant latent potential for growth relative to more mature businesses. The best SMID cap growth companies can quickly reduce spending and inflect profitability if needed, given their high starting levels of investment. We believe the best-of-the-best SMID cap companies will take advantage of adjacencies and have a better potential opportunity set for value-added acquisitions. Of course, many companies do not meet this high hurdle, which is why we hold a concentrated Portfolio of companies that do not just offer growth and high returns, but also durability, robust financial models, the ability to self-fund growth, and what we believe to be superior management teams.

We believe great investing requires a clear and proven philosophy, a disciplined process, and conviction. It also requires great humility and a willingness to change your view when the evidence demands it. We look forward to keeping you updated on our views in future commentary.

Thank you for your interest in Polen Capital and the U.S. SMID Company Growth Strategy. Please contact us with any questions.

Sincerely,

Rayna Lesser Hannaway, CFA & Whitney Young Crawford

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Polen US SMID Company Growth Q2 2023 Portfolio Manager Commentary