GELYF - Polestar: 44000 Vehicles And More Than $2 Billion Behind

Summary

- Polestar delivered 21,000 vehicles in the fourth quarter, more than doubling volumes from the third quarter. Full-year deliveries totaled 51,500 vehicles, beating its revised guidance of 50,000 vehicles.

- The company has guided full-year 2023 deliveries of 80,000 vehicles, a y/y increase of ~60%.

- The figure significantly underdelivers on Polestar's initial guide for full-year 2023 volumes, likely due to ongoing COVID-related disruptions, macro headwinds, and other ramp-up inefficiencies.

- The following analysis will discuss the drivers of related sales losses for the year, and gauge their potential implications on the Polestar stock's near-term performance outlook.

Polestar ( PSNY ) was the latest EV maker to announce preliminary fourth quarter and full year 2022 vehicle delivery results. Despite cutting its guidance earlier in the year from initial projections of 65,000 vehicle deliveries to 50,000, citing protracted supply chain disruptions, the company ended the year strong with 51,500 vehicles delivered to represent an impressive increase of 80% y/y. The outperformance was a breath of fresh air following consecutive misses observed at EV pioneer Tesla ( TSLA ) and rival upstart Rivian ( RIVN ) last week, which increased investors' angst over demand risks in the nascent industry that has previously been viewed as a relatively more resilient corner of the broader auto sector.

Yet, Polestar has also taken the liberty to quietly slash its earlier guidance for full year 2023 deliveries of 124,000 vehicles per the March 2022 Investor Presentation to now just 80,000 vehicles - an approximate 35% downward adjustment that would represent y/y delivery growth of 55%. While we had largely anticipated Polestar to underperform its initial delivery targets set out in the March 2022 Investor Presentation, considering the typical trend of overpromises and underdelivery in its preceding SPAC peers, the newly adjusted guidance for 80,000 vehicle deliveries this year further undercuts already conservative expectations. This is likely due to continued ramp-up inefficiencies in production due to protracted auto supply chain constraints, as well as on-and-off COVID disruptions in its core manufacturing hubs shared with key backers Geely ( GELYF / GELYY ) and Volvo ( VLVOF / VLVCY ) across China. In addition, newly announced plans to launch the Polestar 4 before the end of the year per the company's latest press release and updated Investor Presentation also signals that start of production ("SOP") on the vehicle and subsequent deliveries will not ensue until at least mid to late 2024, unlike Polestar's initial guidance for nominal deliveries of the newest vehicle in its line-up to take place before the end of the current year.

The following analysis will look into plausible explanations for Polestar's recently slashed full year 2023 delivery guidance - spanning the continuation of unprecedented auto supply chain disruptions, changing EV demand trends due to looming macro risks, as well as other potential ramp-up execution risks - and gauge their related implications on the Polestar stock's near-term performance.

An Overview of FY 2022 Deliveries and Revisiting Our FY 2023 Forecast

Polestar delivered 51,500 vehicles in 2022, up 80% y/y and better than management had previously expected due to the lingering after-effect of China's on-and-off COVID disruptions. Much of the delivered volumes are likely represented by the Polestar 2 - its first fully electric sedan - as sales of the predecessor Polestar 1 hybrid continue to phase out following discontinued productions last year. And based on the average vehicle selling price of about $46,000 in the third quarter (i.e., vehicle sales revenue of $425.3 million booked on deliveries of 9,215 vehicles ), the 21,000 vehicles delivered in the fourth quarter is likely to have brought in close to $1 billion in quarterly vehicle sales - a key milestone that beats rival upstarts Rivian and Lucid ( LCID ). This would also potentially bring Polestar's full year 2022 vehicle sales close to current consensus estimates of $2.4 billion .

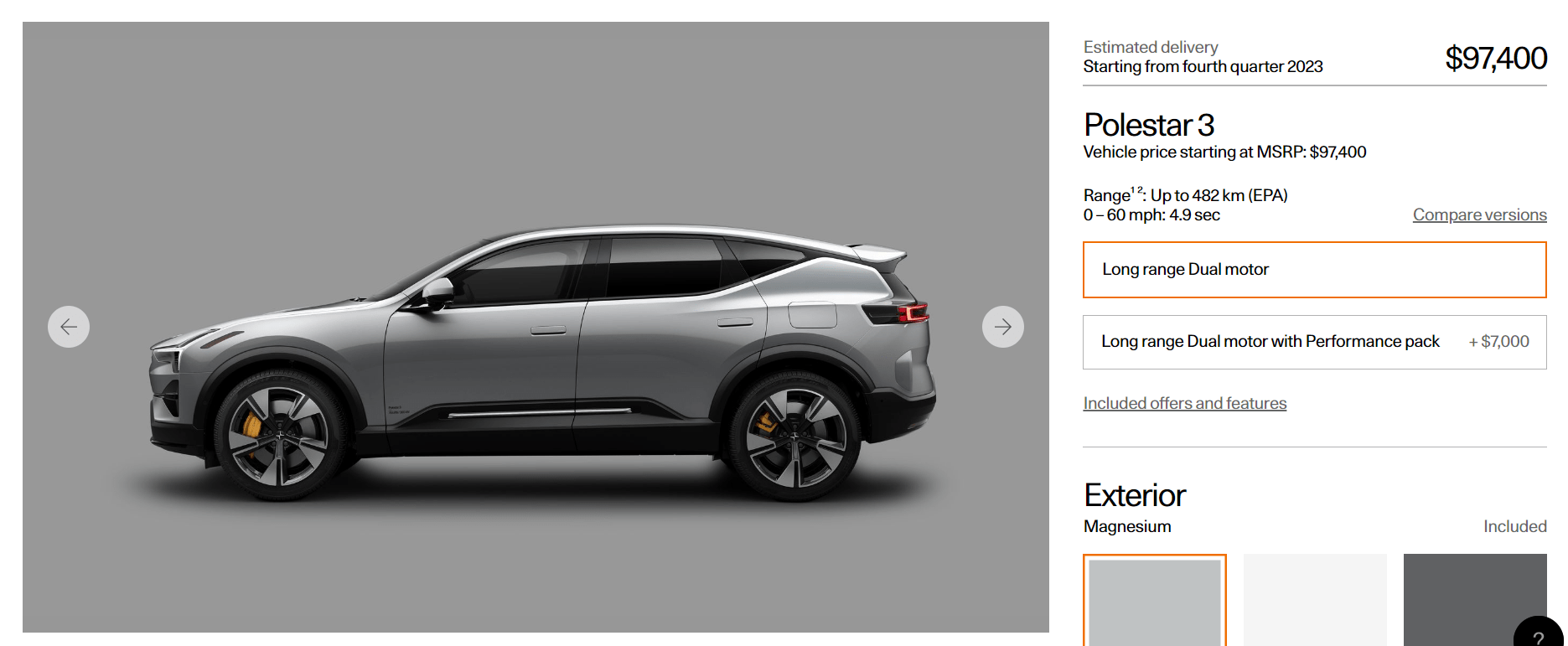

And revisiting our previous forecast for Polestar - we had initially projected full year 2023 vehicle deliveries to reach 93,000 units, a 25% cut from the company's initial guidance of 124,000 units to account for the high probability of under delivery based on observed trends across its preceding SPAC EV peers due to both overly aggressive promises as well as unforeseen supply chain bottlenecks that have been the bane of the broader auto industry's existence over the past two years. Our initial forecast had included consideration of strong Polestar 3 SUV sales given the segment's traction across Polestar's core American, European and Chinese markets. We had also previously baked in nominal deliveries on the Polestar 4 in our forecast to be consistent with management's initial guidance for sales of 6,000 units to take place by the end of 2023. But it seems that only a launch for the upcoming premium electric SUV is in the books for the current year, with SOP and deliveries unlikely to begin until at least mid or late 2024 - a similar launch-production-delivery timeline as the Polestar 3 SUV, which only recently began taking reservations in October 2022 with initial deliveries not expected until the fourth quarter of 2023 per Polestar's website:

Estimated Polestar 3 Delivery Timeline (Polestar.com)

{kind=link}

Some of the lost production and delivery volumes in 2022 due to acute supply chain and logistics bottlenecks are likely to have spilled over to 2023 as well, highlighting the inevitable headache of ramp-up inefficiencies at Polestar, even though it already shares manufacturing with experienced automakers like Volvo and Geely. Ongoing COVID disruptions in China entering into the new year likely play a role in the modest full year 2023 delivery guide as well.

China's abrupt reversal of its yearslong adherence to stringent COVID Zero rules late last year has kept its latest infection rates elevated. The outbreak is likely to be further exacerbated by the anticipated "travel rush during the upcoming Lunar New Year" - China's largest festive holiday second to its weekslong National Day celebrations in the fall - which will continue to draw uncertainties over production ramp-up progress at Polestar's core production hub shared with Volvo in Taizhou for the Polestar 2. The main production facility, which is located in China's Zhejiang province near Shanghai, is currently reeling from persistently elevated new daily case counts, heightening Polestar's vulnerability to absenteeism and other COVID-related disruptions to operations within the near term. The prevalent spread of COVID in China's Sichuan province, which is where Polestar's shared Chengdu production facility with Geely is located, also sheds uncertainty on whether the SOP timeline for the Polestar 3 SUVs in mid-2023 will proceed as planned. Specifically, Polestar 3 SOP is expected to begin in mid-2023 at the Volvo-owned Chengdu facility, which will supply the initial global deliveries beginning in late 2023, and in 2024 at the Volvo-owned Charleston facility.

Polestar's full year 2023 delivery guidance is currently set at 80,000 vehicles, which would represent y/y volume growth of more than 55%. Although still impressive, the figure actually represents a 35% discount from management's initial delivery projections of 124,000 vehicles for full year 2023. Estimated revenue of more than $3.7 billion on the 80,000-vehicle delivery guide based on the third quarter's average vehicle sale price (without inclusion of later year deliveries on the more expensive Polestar 3 SUVs) is also a far cry from previous projections of more than $6 billion, representing a cost of as much as $2 billion resulting from ongoing COVID disruptions to operations, looming macro challenges, as well as other ramp-up inefficiencies.

The Near-Term Macro Overhang on Sales

The U.S.

The U.S. auto market, which is where Polestar currently makes a meaningful portion of its sales (about a quarter as of 3Q22), is already starting to show cracks in demand as the burden of rising interest rates and inflationary pressures weigh on prospective purchase decisions.

As discussed in some of our recent coverage on EV stocks like Rivian and Lucid, the average MSRP for a brand-new EV in the U.S. is now north of $66,000 due to supply constraints that have turned buyers in the market into price takers. And monthly financing payments - the preferred purchase method for American car owners - have only soared towards record levels of more than $717 on average, up from the $300-range in 2010, with close to 20% of new vehicle owners now paying monthly financing instalments of more than $1,000 compared to just 10.5% in 2021. This is consistent with record-setting average annual percentage rates ("ARR") on auto loans that now sit comfortably at the 6.5% level as of December, versus 5.7% just three months ago. Cumulative outstanding U.S. auto loans now exceed $1.5 trillion , and steadily climbing towards the $2 trillion mark to rival against student loans - the second largest contributor to cumulative American debt balances - as Fed rate hikes continue at an aggressive pace to counter generation-high inflation.

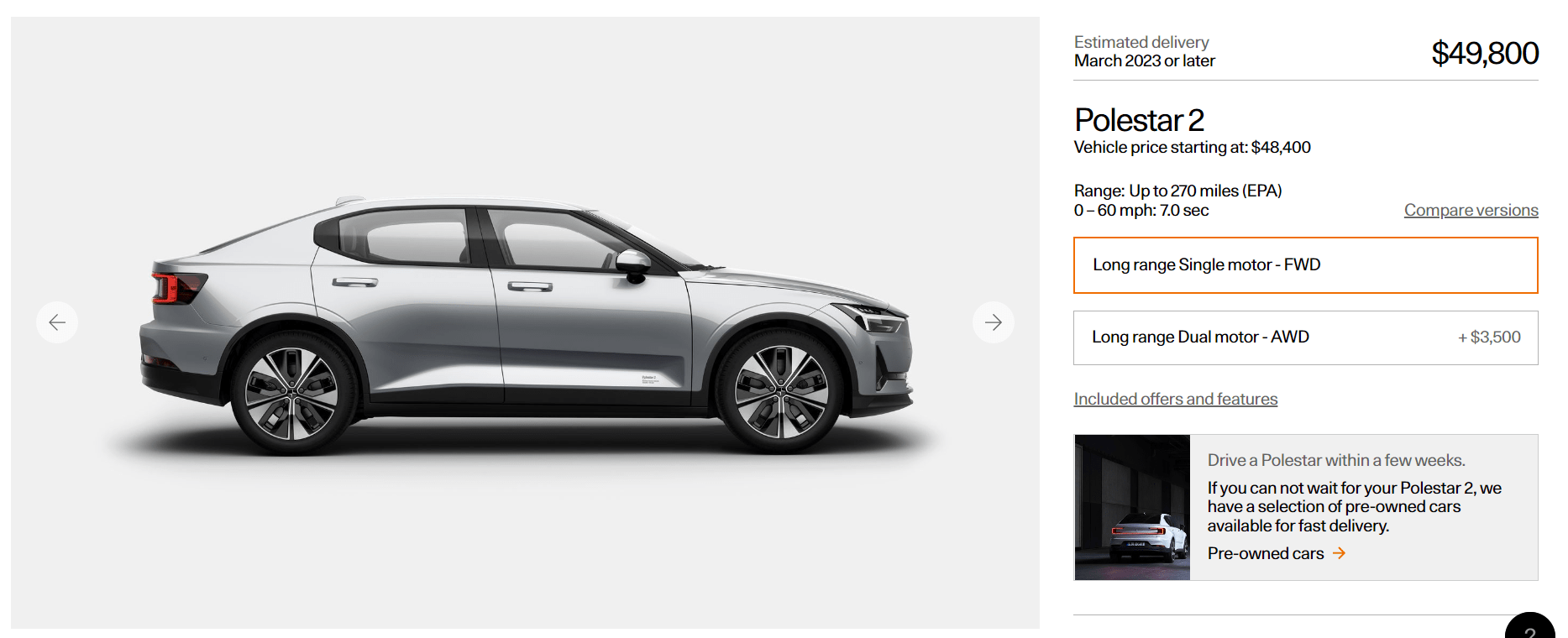

While Polestar has yet to provide details on its reservation backlog for the Polestar 2 and the newest Polestar 3, production ramp-up likely remains the key focus while near-term demand risks take a backseat. This is a similar case to its younger EV manufacturing peers, where demand continues to outpace supply, unlike industry leader Tesla. Delivery wait times for new orders on the Polestar 2 is now estimated for March 2023 or later based on Polestar's official website, which is consistent with commentary regarding recurring delivery delays from prospective buyers that have recently placed an order on the electric sedan.

Estimated Polestar 2 Delivery Timeline (Polestar.com)

{kind=link}

As we have recently shared in a coverage on rival EV upstart Lucid, we believe delivery ramp-up will be as important as production ramp-up within the foreseeable future as competition gains momentum in the nascent industry. The longer prospective buyers are left waiting for vehicle deliveries, the higher the risks of market share loss altogether:

Given the looming economic downturn and increasing competition, delaying deliveries and conversion of reservations to sales could elevate risks of customer loss altogether. Specifically, new vehicle pre-order volumes are already showing cracks in auto demand, as surging borrowing costs and sticker prices continue to deter buyers.

Source: " Lucid: 2 Critical Near-Term Watch Items "

And the implications there are simple. With more than 20 new EV models coming to the American auto market this year, and the looming weight of an economic downturn within the near term, Polestar faces increasing competition from both rival EV pure-plays and incumbent legacy automakers alike. And its mid-market Polestar 2 offering also faces relatively higher vulnerability to looming consumer weakness, as the typical middle-class household that the vehicle appeals to remains most recession-prone - more than three-quarters of American middle-class households have already resorted to belt-tightening due to the weight of persistent inflation and rising borrowing costs.

This makes ramping up deliveries, in addition to productions, key to accelerating conversion of reservations to realized sales and market share gains before they are lost to competition. And Polestar appears to be delivering in that aspect. The company delivered 21,000 vehicles in the fourth quarter, more than doubling the some-9,200 vehicles delivered in the third quarter. We view this as an impressive feat given protracted period-end logistics constraints chimed by even more experienced and higher volume automakers like Tesla and GM ( GM ), as well as younger automakers like Rivian and Lucid in prior quarters - especially given acute COVID disruptions in China near year-end, where production of the Polestar 2 is located.

The " steep dive " in shipping prices from Asia to the U.S. in recent months from record levels that surpassed $10,000 for 40-foot containers to now in the $1,000 range is also favourable for Polestar's profit margins. The company is currently one of the few EV upstarts that boast a positive, though nominal, auto gross profit margin, which is a plus under today's market climate where investors prefer growth that is accompanied by visibility into bottom line expansion.

Europe

In Europe, affordability is becoming the dominant theme in auto markets, including the more resilient EV corner. The region currently represents about 45% of Polestar's sales, subjecting it to the acute headwinds of a looming recession in Europe's key economies this year. While EV penetration rates continue to etch meaningful improvements across some of Polestar's largest markets in the region - including Norway, Sweden, Germany, and the UK - new auto registrations are likely to remain subdued this year due to the double-whammy of protracted supply chain constraints and lowered affordability amid growing consumer weakness.

In Germany - Polestar's second largest EU market after Sweden - fourth quarter new car registrations continue to underperform pre-pandemic levels by almost a fifth (-18% vs. 4Q19), despite improving to the same degree y/y (+18% vs. 4Q21). But full year registrations in 2022 remain a whopping 30% lower than pre-pandemic levels, and 4% lower from 2021, underscoring the rising threat of looming recession headwinds. And in the UK - Polestar's third largest EU market - near-term demand trends are not looking bright despite improving EV penetration rates. Specifically, EVs accounted for approximately 17% of full year 2022 new car sales in the UK and overtook diesel vehicle sales for the first time. But two-thirds of related EV sales were attributable to commercial buyers, suggesting "rising consumer weakness" facing Polestar this year in the region.

As mentioned in the earlier section, Polestar's electric sedan is currently priced as a mid-market offering, which increases its vulnerability to weakening consumption across the more recession-prone middle-class household. With affordability now at the center of new car purchase decisions across the EU and rising raw material costs - particularly in key battery raw materials like lithium - sales in the region will likely offset some of the margin tailwinds from U.S. sales discussed in the earlier section. While Polestar is likely still a supply-constrained automaker, near-term weakness expected in its core EU market will likely weigh on its order book growth within the foreseeable future.

China

In contrast, China accounts for a relatively nominal (<1%) portion of Polestar's consolidated sales despite it housing the bulk of the company's production operations. While market participants are largely betting on a recovery in the region - the fastest-growing and largest EV market in the world - to restore EV demand and compensate for growing weakness in Europe and the U.S. within the near-term, Polestar is unlikely to benefit significantly from said anticipated trends.

Yet, over the longer term, China could become a potentially meaningful market for Polestar. With China currently prioritizing restoration of economic growth in the region by incentivizing increased consumption and investments coming out of a yearslong COVID shut-out from the world and a protracted property sector slump, which accumulated household savings of $1.8 trillion last year will be the key to, EV demand in the region is expected to remain robust over the longer-term.

The Bottom Line

Polestar's upcoming earnings call will likely be a tell-tale on everything from order book growth to gauge demand resilience against looming macroeconomic headwinds, to its liquidity stance as well as production and delivery ramp-up progress to ensure adequate capturing of market share within the increasingly saturated EV market.

As discussed in our previous coverage on the stock, investors' speculation that the company may be cash-strapped remains an overhang on Polestar's near-term valuation prospects. The company had just under $1 billion in cash and cash equivalents as of the third quarter end, with a quarterly cash burn rate of more than $600,000 in the period ended September 30, 2022. Despite having recently secured $1.6 billion from a "financing and liquidity support package from major shareholders" - including an "18-month term loan facility with Volvo Cars" sized at $800 million, and a "commitment from PSD Investment…to provide direct and indirect financing and liquidity support" sized at another $800 million - Polestar only has "sufficient funds through 2023". Although the latest development underscores the importance of having strong backing from reputable investors counting Volvo and Geely, Polestar's tight capital structure makes checking off its Polestar 2 and Polestar 3 production and delivery ramp-up efforts and achieving full year deliveries of 80,000 vehicles at the minimum a critical priority.

Paired with looming macro uncertainties beyond the EV maker's control, execution risks remain elevated for the stock. This accordingly subjects Polestars' shares to increased volatility in the near term, in tandem with persistent risk-off market sentiment for long-duration assets that have their valuation prospects pinned on the prospect of cash flows further out in the future. On this basis, we remain skewed towards the $9 bear case PT previously discussed on the stock, as market participants continue to mull on Polestar's favourable longer-term growth prospects against near-term execution challenges.

For further details see:

Polestar: 44,000 Vehicles And More Than $2 Billion Behind