PSNYW - Polestar: Reduced Guidance Is Not A Game-Changer

2023-11-30 02:38:39 ET

Summary

- Polestar expects to deliver 60,000 electric vehicles in FY 2023, lower than the previous guidance of 60,000-70,000.

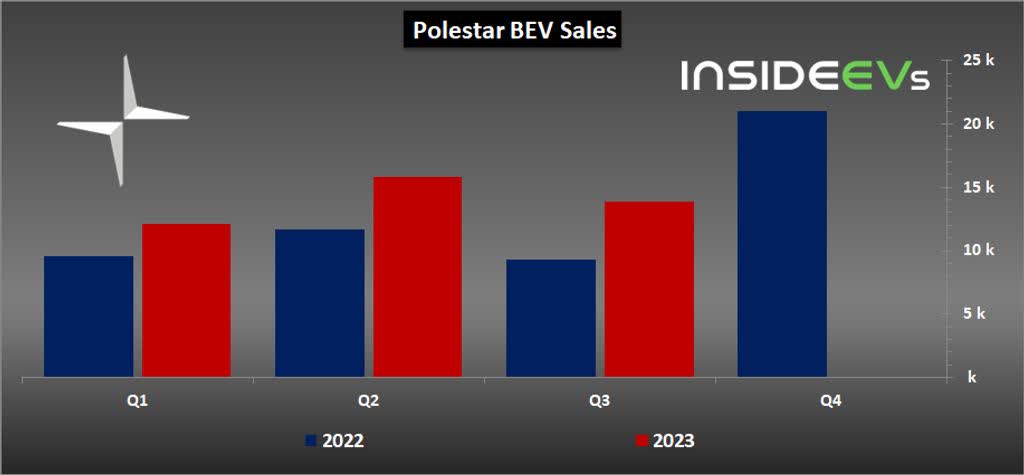

- The company delivered 13,900 EVs in Q3, showing a 50% YoY growth rate, driven by strong demand for the Polestar 2.

- Polestar's revenues are growing rapidly and the firm maintained positive gross profits, setting it apart from competitors.

- Shares are trading well below the 1-year average P/S ratio.

Swedish electric-vehicle company Polestar ( PSNY ) earlier this month reported a steep increase in revenues for the third-quarter and the electric vehicle maker issued a new forecast for its full-year expected deliveries. The EV company now projects 60,000 electric vehicles will be delivered to customers in FY 2023, compared to a previous forecast of 60,000-70,000 electric vehicles. Despite the softer guidance, Polestar sees significant top line and delivery momentum and already generates positive gross profits... two facts which I believe are not reflected in the EV company's valuation. I consider Polestar a speculative buy for investors, but only for those that have a high risk tolerance and a stomach for a high level of volatility.

Previous rating

I rated Polestar a buy at the beginning of September after the company issued second-quarter results and recommended investors to buy the drop . Since September, Polestar has revalued sharply lower, however, in part due to expectations of slowing delivery growth going forward as well as broadly deteriorating investor sentiment in the EV market.

Despite a significant price decline of 37% since my last work, Polestar is still expected to aggressively grow its deliveries. In my opinion, strong delivery growth and pricing strength for the Polestar 2 as well as new product launches could help drive a revaluation of Polestar's shares. In July, I rated Polestar a hold due to slowing production growth. Although the firm lowered its production outlook again this time, Polestar is nearing the launch of new EV products next year and the revaluation to the downside has made shares of Polestar much cheaper as well.

Updated production guidance for FY 2023

Polestar delivered 13,900 electric vehicles in the third-quarter, showing a year over year growth rate of 50% due to strong customer demand and sales momentum for its flagship product, the Polestar 2. The growth in global deliveries is especially noteworthy because other EV companies, like Lucid Group ( LCID ) and Fisker ( FSR ) appear to be struggling with weaker than expected demand for their EV products.

{kind=link}

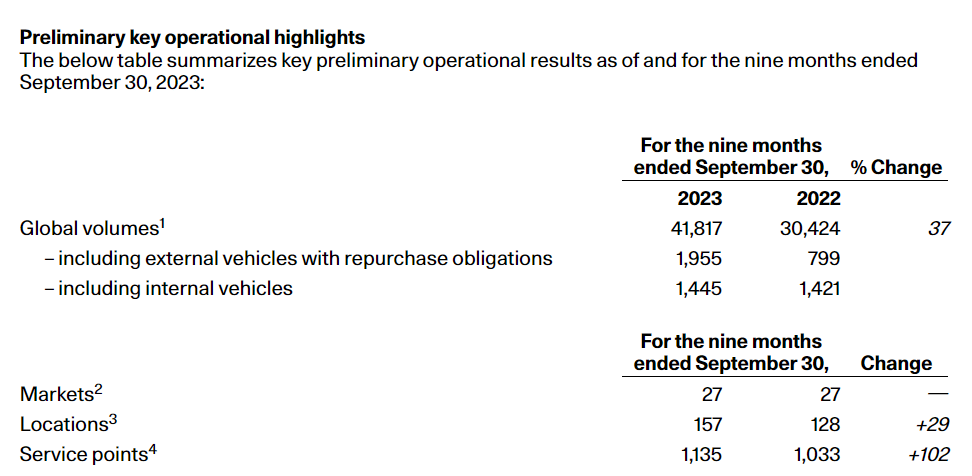

In the first nine months of the year, Polestar delivered 41,817 electric vehicles, showing a 37% year over year increase. Importantly, the increase in deliveries was due solely to growth in existing markets, not through new market additions.

Polestar updated its guidance this month and said it would now target a delivery volume of 60,000 electric vehicles in FY 2023. Polestar previously guided for a delivery volume 60,000 to 70,000 electric vehicles. The new guidance implies that the EV company will have to deliver another 18,300 electric vehicles in the fourth-quarter. Polestar lowered its production outlook in order to grow more slowly and become more focused on controlling costs.

Other EV companies have also reduced their outlooks (but not all), especially Lucid Group comes to mind which now sees a 8,000-8,500 EV production volume, down from 10k. Rivian Automotive raised its production outlook by 2k units which is the reason I see the EV firm as the most promising EV stock in the large-cap categor y.

In the year-earlier period, in FY 2022, Polestar had a global delivery volume of 51,500 electric vehicles and the company saw 80% year over year growth. With an estimated delivery volume of 60,000 EVs, Polestar is now expected to generate 17% Y/Y growth.

{kind=link}

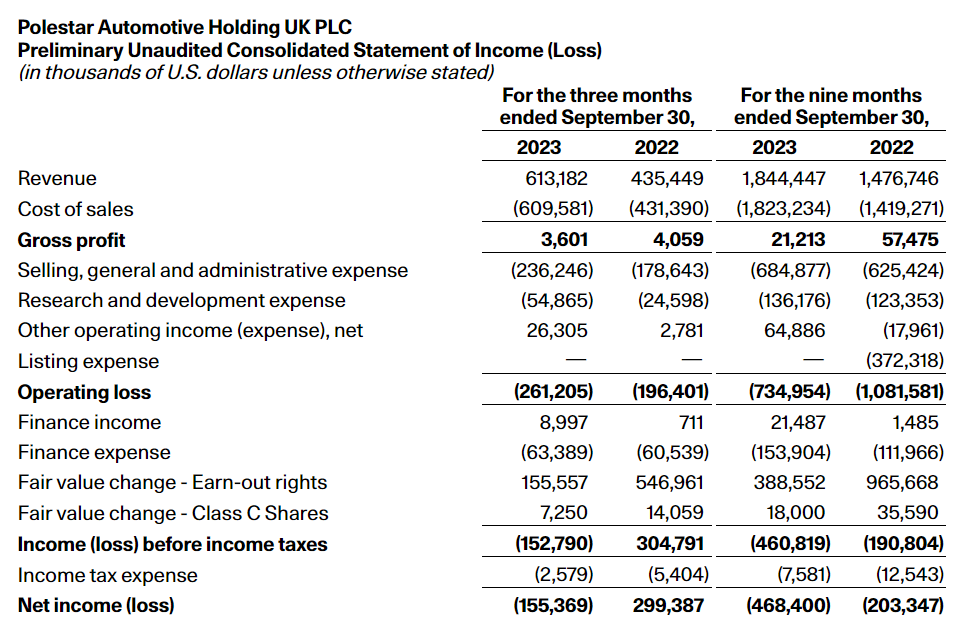

Despite the hit to guidance, Polestar continues to have considerable top line momentum which is the reason why I confirm my buy rating after all. Polestar’s revenues increased 41% year over year in the third-quarter to $613.2M and the electric vehicle start-up again achieved a positive gross profit on its operations… which is something that sets the company apart from its rivals. Delivery growth and pricing strength (Polestar increased prices for its EV products in 2023) for the Polestar 2 are driving top line gains for Polestar. The EV company also said that it plans to achieve a 2% gross margin on a consolidated basis in FY 2023.

{kind=link}

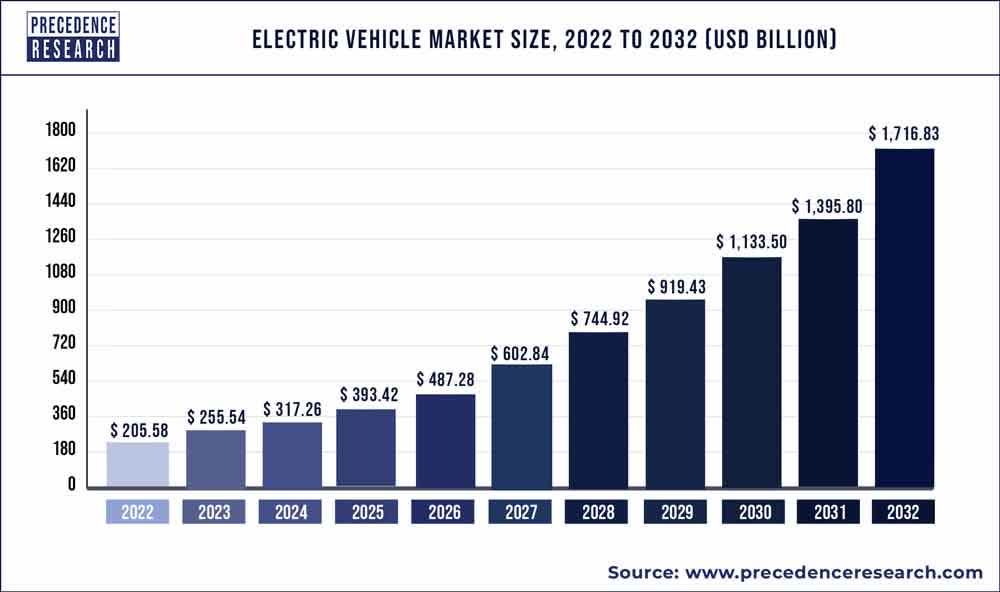

The long term potential in the EV market, however, is favorable to Polestar as well as other electric vehicle start-ups with a projected annual growth rate of 23% between FY 2022 and FY 2032. In FY 2022, Polestar grew significantly faster than the market, but this growth, as the production outlook indicated, is set to moderate going forward.

{kind=link}

Good liquidity position, nearing cash flow break-even in FY 2025

Polestar has two advantages over other EV start-ups: the company is backed by car company Volvo (which recently provided another $200 million in additional loan capacity to the start-up) and it has a considerable amount of cash on its balance sheet that gives it a large liquidity run-way.

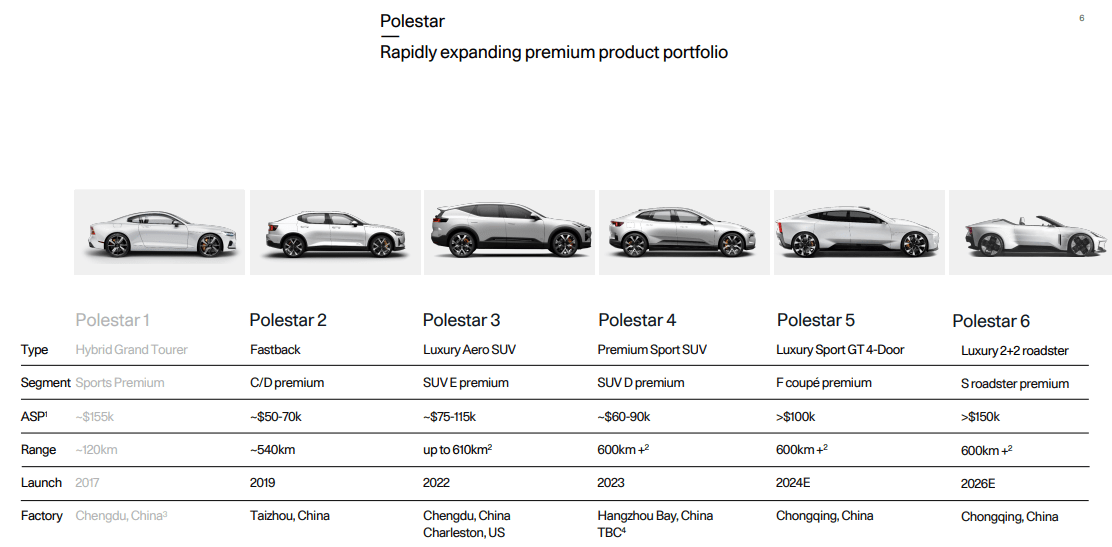

At the end of the third-quarter, Polestar had $951 million in cash on its balance sheet compared to $974M at the end of last year. Polestar achieves significant negative free cash flows from its operations (YTD $1.3B negative), however, as it ramps up production and prepares to launch the new Polestar 4, an SUV coupé, and the Polestar 5, an electric four-door GT. With a denser product portfolio, Polestar has a change to accelerate its revenue growth next year.

{kind=link}

Polestar depended on net new financing cash flows (+$1.5B YTD) to finance its cash burn related to the production and delivery ramp.

Polestar's negative operating and free cash flows are set to persist until at least FY 2025 as the company has said that it see a $1.3B additional financing need until it reaches cash flow break-even (expected for FY 2025). The survival of Polestar will depend on the company being able to raise additional liquidity successfully.

Why Polestar Could Be Ripe For An Upside Revaluation

The estimated growth rate for Polestar's revenues in FY 2024 is 89% as the EV company executes on its global delivery plan and launches new products. The firm’s strongest product is currently the Polestar 2, but Polestar is set to launch new electric vehicle models this year and the EV portfolio is broadening. The EV company, however, did see a downside trend in revenue estimates as investors and analysts have become more skeptical about delivery ramps this year.

Polestar is currently valued at a 0.86X P/S ratio, less than half of its 1-year average P/S ratio. Lucid Group still trades at an excessive multiplier and I recently wrote why my patience has been exhausted . Fisker is even cheaper than Polestar, with a P/S ratio of 0.33X, and I doubled down on the shares recently, despite a lowered production outlook. I explained here , why. I believe Fisker should, if the delivery ramp goes as planned and the company meets its production target, should be able to trade at its average P/S ratio of the last year. My fair value estimate is approximately $4.60, based off of Polestar's previous trading history.

New product launches as well as the realization that Polestar's revenue potential has become too cheap may drive shares of Polestar into a new up-leg. Given that the firm has a cashed up investor, Volvo, in its corner, I also believe that investors are overreacting to concerns about the financing of Polestar's slower production ramp.

Polestar’s risk profile

I see two specific risks for Polestar: 1) Polestar did soften its delivery target for FY 2023 and the company settled for the lower range of its previous guidance range. Slower production and delivery growth would likely negatively impact the pricing of Polestar’s shares. 2) Falling demand and pricing weakness in the EV market could affect Polestar’s margin development and weigh on overall profitability. Polestar is not yet profitable (on a net income and FCF basis), but it has positive gross profits. If those gross profits were to disappear, investors might apply a Fisker-like discount to the EV maker's shares.

Final thoughts

Polestar softened its delivery target for FY 2023 from 60,000 to 70,000 vehicles to the lower end of this range: 60,000. Last year’s delivery volume was 51,500 electric vehicles, so delivery growth rates are expected to slow considerably this year. Revenues are still growing fast, however, and Polestar has considerable resources available (including the backing of Volvo) that suggest that the firm can continue to ramp its EV production. Gross profits are also in the green, which is a positive, and I expect Polestar to be among the first EV companies that could achieve consistent operating profitability. The shares, in my opinion, remain a speculative buy!

For further details see:

Polestar: Reduced Guidance Is Not A Game-Changer