IWM - Policy Contradictions Herd Fed Policy

2023-05-26 16:03:30 ET

Summary

- Fed policy may be as much determined by what lies behind as by what lies ahead.

- Banks and other financial institutions are more damaged by past rate hikes than the Fed will admit.

- The policy paradox is that rates have been raised fast enough to do harm to financial institutions but are not high enough to cool inflation and slow growth.

- This policy dissonance leaves the Fed with few policy choices - that explains why rate hikes have slowed before real rates are positive.

As the Federal Reserve ponders what to do next with monetary policy, it continues to deal with the nagging problem of the state of banks. The Fed's just-released minutes from its May FOMC meeting made several references to the banking system being well-capitalized and stable. However, many private sector analysts have a different view on the state of the banking system.

One overarching view is that large banks are safe, largely because they are better at asset and liability management. During the period when the Fed raised rates sharply, they were better able to negotiate treacherous market conditions that saw interest rates rise sharply - much more sharply than the Fed had guided the markets to prepare for: FACT.

It is regional banks and smaller banks where the problems reside. The problem is simply that many of them now have become undercapitalized because they bought treasury securities when rates were low and expected rates to remain low and did not offload or hedge them when the Fed changed its mind to begin to raise rates - raising them sharply. Basically, this was a period in which policy guidance was quite dangerous to any financial institution that paid attention to it and believed it.

For that reason, many banks today are in much more fragile shape than monetary officials want to admit and it's one of the reasons that the Federal Reserve is underwriting repos to banks for the face value of Treasury securities on their balance sheet rather than giving them haircuts to mark them down to market.

Policy Tension

As a result of this risk, there is tension in monetary policy between how much policy may wish to raise rates to control inflation and how much policy can raise rates without creating further problems at banks. The Federal Reserve has chosen to deal with this problem by not talking about the problems of banks and by focusing on stabilizing the federal fund trade around its current level, a level that is still not clearly above the rate of inflation.

The ostrich is not really hiding…

Failing to recognize and to deal straightforwardly with a policy dilemma does not make that dilemma go away. The Federal Reserve's talk about pursuing a soft landing is a policy discussion that allows the Fed to argue that it doesn't need to raise rates anymore; it allows the Fed to claim that it is pursuing control of inflation while doing the least harm to the economy, a policy move that gives cover to the Fed's desire to not raise rates much more because of the state of health of the smaller banks.

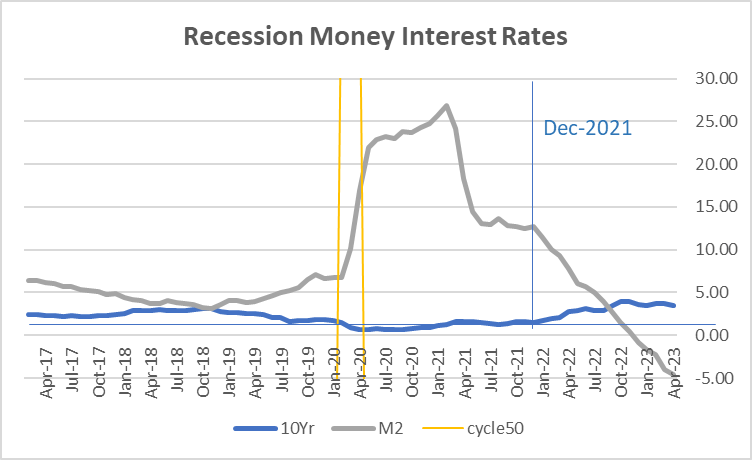

Chart one below reveals what Fed policy did as well as the lasting impact policy had on banks in today's market. The blue line shows the yield on the 10-year treasury that reached a low of 66 basis points in April 2020 and did not rise to over 1% until January 2021.

During this time money supply growth ramped up logging growth rates of over 20% year-over-year from May 2020 until March 2021 - nearly a year of 20%-plus growth.

Chart 1

Money growth VS 10-Year Note Yield (Haver Analytics and FAO Economics)

{kind=link}

That's important to banks, because when the Federal Reserve pushes money supply growth up it does this by creating deposits at banks. So, we have this period of rampant money supply growth that occurs at a time when the yield on the 10-year treasury is persistently below 1% - and of course - the yields on shorter treasuries are even lower. And because of the disruption to the economy being shut down because of COVID, there is no personal loan demand there is little business loan demand and the only asset banks can acquire to balance the massive liability growth created by the Fed's money supply growth is to buy low-yielding treasury securities.

Fed guidance: By the numbers and the dates

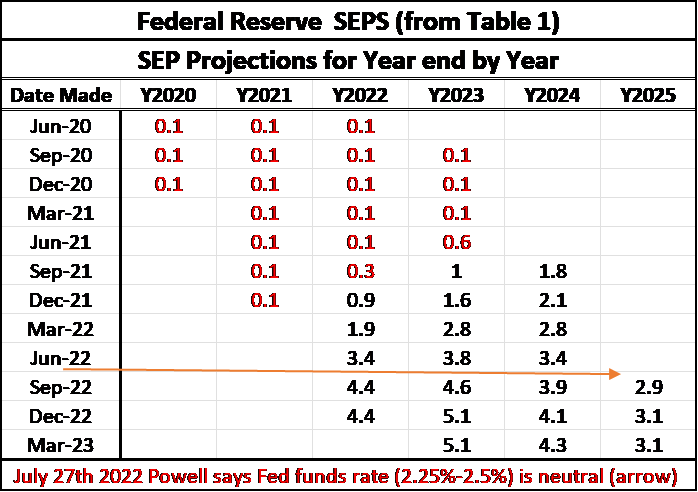

During this period the Federal Reserve was providing guidance to markets on what it expected the federal funds rate to do. The Fed provides guidance as the summary of economic projections known as SEPS that are created four times a year in March, June, September, and December.

The SEPS estimates for the Fed funds rate at the end of the year in 2020 was for a funds rate of 0.1%. The forecast for the funds rate at the end of 2021 beginning with forecasts made in June of 2020 through December of 2021 never varied from the same 0.1%. So, hey, what's the risk? Buy 10-year notes - right? Earn the slope of the yield curve!

Forecasts for the year 2022 were for a year-end funds rate of 0.1% from June 2020 through June 2021. But by September of 2021, the Fed raised the estimate for year-end Fed funds to 0.3%, in December it raised it to 0.9% and in March it raised it to 1.9%. The remaining estimates can be seen in the table below along with how the estimates changed for the Fed funds rate at the end of the year in 2023, 2024, and a few estimates for 2025.

Table 1

Federal Reserve Guidance (Federal Reserve and FAO Economics)

{kind=link}

Live in reality land and invest in fantasy land!

What these estimates underline is that the Federal Reserve was encouraging banks to believe that the federal funds rate was going to remain low. This conveniently came at a time when the money supply was ramping up, the government was running huge budget deficits, which it needed to get financed, and when credit demands in the rest of the economy had gone slack. Banks had no alternative than to buy treasury securities. Now. some are critical of banks. arguing that there are other assets they could have purchased but this is basically a 'fallacy of composition argument.' Money supply grew so much - bank deposits grew by so much - there was no other asset class that banks could have participated in to absorb the assets they need to acquire to balance the liabilities on their balance sheets. The Fed essentially was forcing banks into a certain asset management model and at the same time telling them it was going to be OK because rates would remain low.

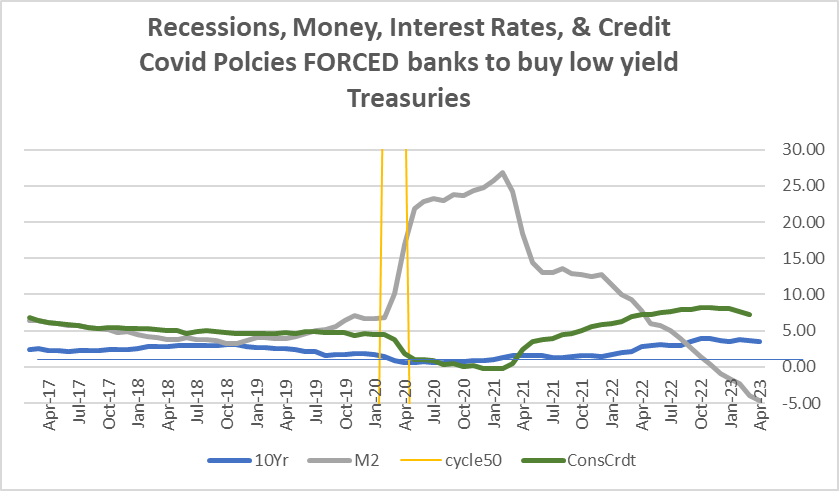

Chart 2 adds a line to this chart representing consumer credit growth, underlining the point that private sector credit growth was extremely weak, leaving banks little choice but to buy treasury securities.

Chart 2

Recession, Money, Credit, and Interest rates (Haver Analytics and FAO Economics )

{kind=link}

Not only did banks have to buy treasury securities but they had to buy them at a time that the deposit base was growing extremely rapidly so that they were having to pile on a large number of treasury securities to counterbalance the enormous deposit growth. From February of 2020 until December of 2021 the Federal Reserve raised the M2 money stock by $7 trillion. This is nearly 40% increase in the amount of M2 in the economy; the bulk of this was reflected in higher bank deposits. Prior to Covid M2 was growing at about a 5% annual rate. In less than two years the Federal Reserve ramped the money stock up so enormously it increased M2 by the amount it would normally have taken it about 6 3/4 years to accomplish. The Fed squeezed 6 3/4 years of money supply growth to a period of less than two years. And on top of this, of course, there was fiscal stimulus. Fed guidance to banks: Don't worry, buy treasuries.

This liquidity, these deposits, and Federal Reserve asset purchases and programs are still swimming around in the economy today. They reflect an important reason why the economy, after many rate hikes, refuses to slow. Of course, the second important reason the economy refuses to slow is that the Federal Reserve, despite raising interest rates enormously, has still not gotten the interest rates up above the rate of inflation so that monetary policy still is not restrictive.

The great monetary paradox

The great paradox here is that while policy is not yet restrictive in the sense of putting the nominal interest rate higher than the inflation rate, the rise in nominal Fed funds rate has been massive and that's created a tremendous problem for banks that bought treasury securities during the time that the Fed ramped up money supply growth. These problems have taken root mostly at regional and smaller banks because larger banks engaged in more active asset liability management than these other institutions and larger banks did not simply listen to the Fed to get their cue about what was going to happen in the future.

Chart 3

Fed Policy Guidance and Inflation (Haver Analytics and FAO Economics )

{kind=link}

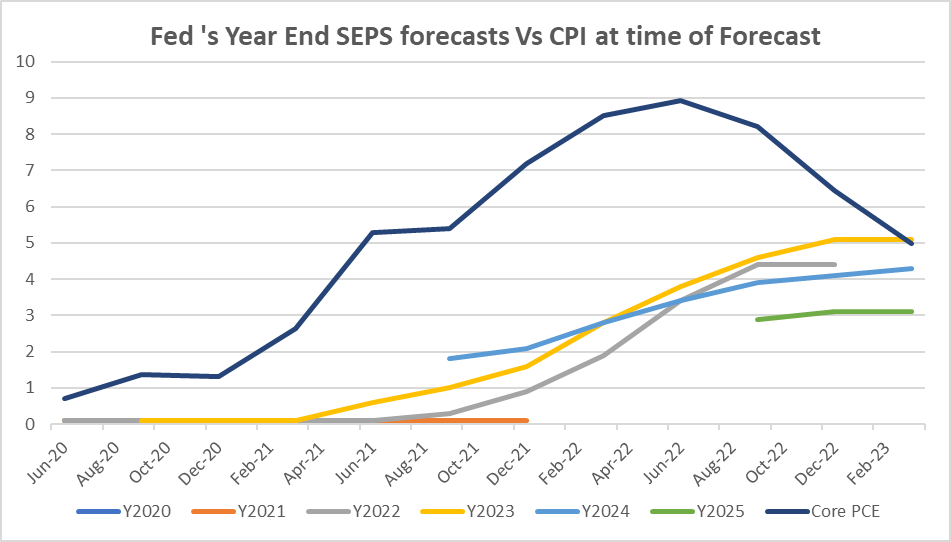

Chart 3 gives you some idea of how Fed policy fooled banks. This chart shows the Federal Reserve fed funds guidance from Table one (above; from various reports on the Fed website) plotted according to the date that the forecast was made. For example, the long yellow line represents the various forecasts that were made for the funds rate that was 'expected' at the end of 2023. Prior to 2023, you can see most of the lines were flat-lining at a year-end forecast of 0.1%. (That you can identify better in Table 1 above.) The chart picks up economic events in June of 2020 after the Covid virus had struck and the inflation rate began to move up from 1% to over 2% by early 2021 using the CPI as the inflation barometer. And even in the face of rapid inflation acceleration, the Federal Reserve continued with this extremely flat rate guidance. Remember those lines represent forecasts and are for the level of the funds rate at the end of the year for each of those years represented by different colors.

When the inflation rate rose over 5% for the first time in 2021 The Fed was only predicting a fed funds rate at the end of 2023 of 0.6%. While I was banging my head against the wall in disbelief, markets were drinking this Koll Aid. In September 2021, the inflation rate began to move above 5.4% and by that time the end-of-year fed funds rate for 2023 was being projected at 1%. Chart 3 plots the actual current CPI rate against forecasts made for the end of various years to come.

Chart 4

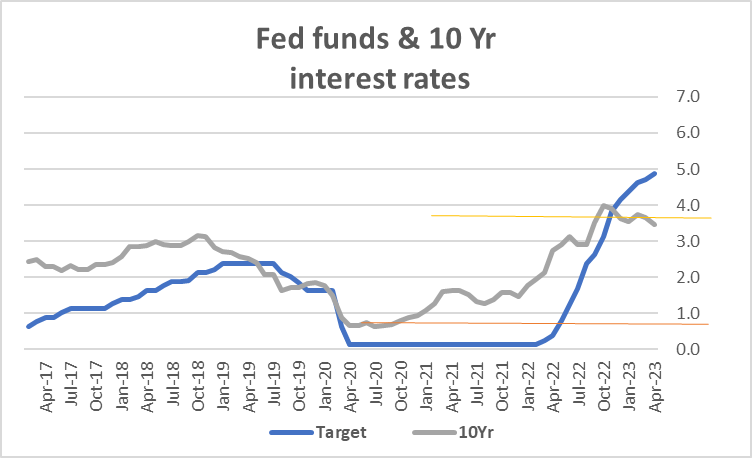

Fed Funds Vs the 10-year Treasury Note (Haver Analytics and FAO Economics )

{kind=link}

Market rates tracked Fed funds rates…not inflation

For a long time, the 10-year note tracked with the federal funds target. In 2021 the 10-year yield jumped up somewhat but still stayed below 2% and then in early 2022 as the Fed prepared to raise the funds rate 10-year and other treasury yields began to climb more significantly and now you can see the implications of that on this chart.

The difference between the two horizontal lines (Chart 4) drawn in yellow and gold represents a massive increase in yield which corresponds to a crushing decline in securities prices over this period. We have since become acquainted with the idea of banks being able to hold securities to maturity ((HTM)) and not having to mark them to market. Both banks and securities firms can do this. We have seen examples of banks small and large and have seen non-banks that have had to report footnote items that reveal where they have not marked their securities to markets and where they are carrying large implicit losses that they don't have to reflect on their balance sheet but they do have to reflect in financial footnotes. Such 'paper losses' imply some impairment to their capital position even if it isn't reflected in the accounting statements.

This is the situation of banks today. Every time the Fed raises interest rates it potentially creates a bigger gap as securities yields rise. One thing that has happened that could be favorable for banks is that the yield curve has stopped steepening and it's been flattening as the Fed has raised rates because the Fed has raised rates significantly. And, if that continues, increases in the federal funds rate will not continue to inflict further losses on bank balance sheets (or in statement footnotes) something that's very important for small and mid-sized banks in the United States. However, increasing the federal funds rate would still increase the cost of deposits to banking institutions.

Monetary policy cannot afford to be distracted by politics

The important lesson to learn here is that the Fed's forbearance in raising interest rates in the name of full employment after adopting what had been a new framework agreement under some political pressure from progressives was not a good policy. It was a policy that has subsequently led to banking failures in the U.S. and it may lead to further banking consolidations. Banking experts look at the resources of the FDIC and argue it does not have enough money to bail out or close banks and that it's more likely for that reason that there are going to be more banking combinations as the regulators will try to put smaller bad banks into combinations with larger healthier banks.

Be careful what you wish for…and more careful what you do

The irony of this is that progressives don't like the idea of losing small banks because they think that they serve the local communities better. But it's exactly their policies to lean on the Fed to be less pre-emptive with policy, to not raise interest rates when there was inflation, to try to get the unemployment rate lower, to help minorities get jobs, that has led to the situation that has put these small banks in jeopardy.

Now monetary policy tries to chart a path and has this difficult decision much like Odysseus who had to choose whether to take his risk with Scylla or Charybdis. The question is, will the Fed take its risk with inflation by not raising rates enough, or does the Fed take its chance with bank failures by raising rates to control inflation and risking more bank problems?

The soft-landing ploy

There is no easy solution here but the Fed's embrace of a soft-landing strategy gives it a policy that it can say it is pursuing that gives it a reason to not raise rates as aggressively and that helps it to protect other banks from bankruptcy but it may in fact extend the period during which inflation will remain excessive.

More of this, less of that

This is where we are with policy, and this is what I think the risk trade-off is. The Fed's persistence in embracing the language of soft-landings which have never been effective in reducing inflation makes no sense whatsoever from the standpoint of monetary policy. However, the soft-landing is an exquisite tool to cover up the policy trade-off that the Fed does not want to face up to publicly. Historically, the Federal Reserve has raised the federal funds rate well above the inflation rate to control inflation. In this cycle the Fed is, according to its own language, trying to do the least harm to the economy possible, and the question is whether it's a strategy that controls inflation fast enough.

The outcome that is tolerable is a matter of opinion...not science

In the FOMC minutes released on May 24th, Federal Reserve members seem to fall into two classes. There is one group that was concerned that core inflation was stuck and wasn't falling fast enough and that the Fed may have to raise rates further. There is another group, that seemed to have just slightly more membership, that argued that if the economy unfolded the way they currently thought, no further interest rate increases were going to be necessary.

Now, there's a lot of use of the subjunctive tense and reference to hypothetical situations, in the end, what the Fed will do will depend on how the future turns out not on today's opinions. For now, it seems that the Fed is going to try to roll the dice on doing less rather than doing more and hope that it's done enough to contain and control inflation. The Fed's actions are well short of what have been successful in the past. And the fact that market participants expect a rate cut from the Fed this year - while the Fed says that is not in the cards - is just another bit of tension the Fed is going to have to deal with. If the Fed is going to refuse to raise interest rates higher, then it's going to have to keep interest rates at this level longer. The markets are expecting rate cuts this year… someone is going to be disappointed.

Today's tradeoffs were created by yesterday's choices

The trade-offs in monetary policy currently have their roots in the Fed's past monetary policy mistakes which I believe have their roots in the political pressuring of the Fed to try to achieve an unemployment rate that was simply a rate too low. Ironically - ironically - as the Fed has raised rates we have discovered that the unemployment rate has not gone up by very much. It seems that the Fed delayed raising rates for the sake of reducing the unemployment rate for no reason what-so-ever which means we suffer this excess inflation for no good reason what-so-ever.

Summing Up

The Federal Reserve Board staff economists are predicting a recession, and, because of this, markets seem to think the Fed is going to have to provide interest rate reductions as the economy weakens. However, the message from history is quite clear that the Fed has got to keep interest rates significantly higher than the inflation rate even if the economy is in recession if it intends to control inflation. We have seen what happens particularly in the 1969-70 recession and in the 1973-75 recession when the Federal Reserve got cold feet and cut rates too soon.

Unfortunately, this is what many people expect the Fed to do this time as well, since it is pursuing a policy of a "soft-landing." We can only hope that the Fed is giving lip service to this policy and doesn't really intend to follow through with it. If the Fed does not raise rates any further and if the Fed cuts interest rates early in the cycle without keeping the federal funds rate above the inflation rate, the risk that inflation will stay painfully high for a longer period is quite likely.

Because the Fed does not communicate with us clearly and deal with the real risks that are on the table, we have a hard time knowing exactly what the Fed will do and how it will deal with challenges ahead when they emerge. The Fed has become wholly data-dependent. We no longer have any guidance from it that we can depend on. Nor do we have a fix on how the Fed will evaluate incoming data to make policy choices.

For further details see:

Policy Contradictions Herd Fed Policy