PLM - PolyMet Mining: Things To Consider Before Jumping On The Bandwagon

Summary

- PLM's 50% stake in the NorthMet and Mesaba projects in Minnesota could provide for suitable long-term growth if it can successfully overcome two challenges.

- The NorthMet project has major federal and state permits though some of those permits are challenged under litigation, and this concern impacts the investment thesis.

- Further, PLM will need to raise significant project development CAPEX after the completion of the permitting process, and this could result in significant share value dilution.

- I see the stock as a 'hold'.

Thesis

PolyMet Mining Corp ( PLM )(POM:CA) owns a 50% JV interest in the NRCN (read: NewRange Copper Nickel) LLC., and the remaining 50% is owned by Teck Resources ( TECK ). The NRCN JV has 100% ownership over two mineral deposits in the Duluth Complex, Minnesota; NorthMet and Mesaba. Both deposits comprise copper, nickel, cobalt, and PGM (read: Platinum Group Metals) orebodies which, if developed, could be an important source of US-based clean energy mineral resources.

In this article, we look at the mining attraction of the NorthMet project in detail. Our analysis will incorporate relevant information from PLM's NI 43-101 (technical report) on the Northmet project since it is initially targeted for development. However, an important consideration for upcoming US-based mining projects is their permitting status. The NorthMet project is permitted for construction/operation subject to litigation. In other words, the project is not fully permitted. Another important consideration is securing funds for the project's significant development CAPEX. I see this as another risky area especially when the Fed's funds rate is on an upward trajectory. Our analysis will consider all these factors in tandem. Let's get into the details.

Mining Attraction of PLM's Assets

The technical report on the NorthMet project (the "Project") was released on December 30, 2022. It reveals that the Project will have a mine life of 20 years, a throughput capacity of 32 ktpd (read: thousand tons per day), and will be developed in two phases; Phase I and II. The salient features of both phases are tabulated below.

| Metric |

| Phase I |

| Phase II |

| Project CAPEX |

| $1,208 MM (Initial) |

| $325 MM (Incremental) |

| After-tax NPV@7% |

| $304 MM |

| $487 MM |

| NPV attributable to PLM (50% basis) |

| $152 MM |

| $243.5 MM |

| Project IRR |

| 11% |

| 11.5% |

| Annual Copper Equiv. Production |

| 97 Mlbs |

| 118 Mlbs |

| Cash Costs Net of By-Product Credits |

| $0.72/lb |

| -$0.11/lb |

Under Phase I , only copper and nickel concentrates would be sold. Total payable metal in the concentrates is estimated at 1,131 Mlb (read: a million pounds) copper, 133 Mlb nickel, 5.6 Mlb cobalt, and 1.14 Moz (read: a million ounces) of 3E PGM (including platinum, palladium, and gold). Note that the 3E PGM is predominantly comprised of palladium, which accounts for ~0.906 Moz.

Under Phase II, an optional hydrometallurgical plant (or HMP) will be used to treat and enrich metal concentrate into saleable products (or refined/finished products). This process will help extract and isolate PGMs, precious metals, copper, nickel, and cobalt from the concentrates.

The total payable metal in concentrates and products from the HMP is estimated at 1,194 Mlb copper, 179 Mlb nickel, 6.4 Mlb cobalt, and 1.681 Moz of 3E PGM. PLM's strategy to phase the Project's development will help de-risk the start of the HMP circuit since the initial plan of producing concentrates will use well-established technologies. Meanwhile, the company expects to cover the incremental financing for Phase II through cash generated from Phase I operations. Note that Phase II production is projected to commence from the third year of operations subject to a decision by the JV partners to advance to Phase II.

Valuation - Just about right

Given PLM's 50% ownership of the NorthMet Project, we take the Phase-II after-tax NPV at 50% value; at ~$244 MM. If we divide this number by the outstanding share count of ~102 MM we reach an NPV/share of $2.40. By comparing this number with the current share price (at the time of writing) of ~$2.37, we deduce that the stock is currently trading at ~0.98x the NPV/share of its PLM project, and is fairly valued.

However, the following additional factors shall also be considered.

1) Discount Rate: The NPV assessment assumes a discount rate of 7%. In my view, this isn't conservative enough for the following reasons:

- A low discount rate of between 6-8% suits precious metals (like gold and silver) mining companies because precious metals have low barriers to selling. I believe that base metal (copper, lead, zinc, cobalt, etc.) companies like PLM should use a discount rate between 8-10% to discount their projects.

- Although the project is in the advanced permitting stages but is not fully permitted. This increases the project risk, and hence the need to up the discount rate.

- Finally, the stage of project development matters. Since PLM is yet to reach that stage, I believe this factor also points toward an upward revision in the discount rate.

2) Metal Prices: The technical report expects that a major chunk of future revenues will be attributable to copper (53% in Phase-I, 46% in Phase II), nickel (14% in Phase-I, 16% in Phase II), and PGMs (29% in Phase-I, 34% in Phase-II). Look at the following table which compares the spot metal rates with the reference prices used to calculate the after-tax NPV.

| Metal |

| Unit |

| Price Assumption |

| Spot Price |

| Difference - Spot v/s Assumption |

| Copper |

| $/lb |

| $3.52 |

| $4.13 |

| +17% |

| Nickel |

| $/lb |

| $8.13 |

| $12.193 |

| +50% |

| Palladium |

| $/oz |

| $2,202 |

| $1,450 |

| -34% |

| Platinum |

| $/oz |

| $975 |

| $950 |

| -2.5% |

Since metal prices are the 'most sensitive' factor to NPV, I estimate the revised project NPV under Phase II of the project at $239.15 MM calculated as follows:

[$244 million X {(copper=46%X1.17)+(nickel=16%X1.50)+(palladium@90% of total PGM=34%X90%X0.66)}]

Note that the two factors discussed above indicate that PLM's share price is neither undervalued nor significantly overvalued. It's important to note that our assessment of PLM's valuation is based on the NorthMet project alone since the other project, Mesaba is currently undergoing studies regarding resource definition, mine plan, future development options, etc. As such, NPV estimates for Mesaba are not available. Nonetheless, for a balanced analysis, we need to factor in the future growth potential associated with the Mesaba project.

Mesaba's growth potential

The Mesaba project is advancing on baseline environmental studies, resource definition, and mineral processing studies. Currently, mine development options for the Mesaba project are under consideration. Nonetheless, based on its technical report , Mesaba seems to have a greater resource than the NorthMet project.

| Resource Type |

| NorthMet (or NM) |

| Mesaba |

| M&I (Measure & Indicated) |

| 701.6 Mt |

| 2,207 Mt |

| Inferred |

| 441.1 Mt |

| 1,423 Mt |

However, head grades are equally important as they impact the cost of mining operations. The average head grades for the two projects are tabulated below.

| Resource Type |

| NM-Copper |

| NM-CuEq |

| Mesaba-Copper |

| Mesaba-CuEq |

| M&I |

| 0.252% |

| 0.513% |

| 0.428% |

| NA |

| Inferred |

| 0.254% |

| 0.509% |

| 0.368% |

| NA |

From the tables above, I note the following:

- Mesaba has a greater resource (more than 3x) compared with NorthMet, in terms of both M&I and Inferred resource categories.

- Mesaba has higher copper grades than NorthMet. Mesaba's CuEq (read: Copper Equivalent) grades are yet to be revealed since PLM is advancing resource definition studies. Nonetheless, I expect Mesaba's CuEq head grades to exceed those of NorthMet since Mesaba has relatively higher copper-only grades.

My view: Overall, with a significantly higher resource base and potentially higher CuEq head grades compared with NorthMet, I believe the Mesaba project is capable of fuelling PLM's long-term growth.

Permitting - Status and Risks

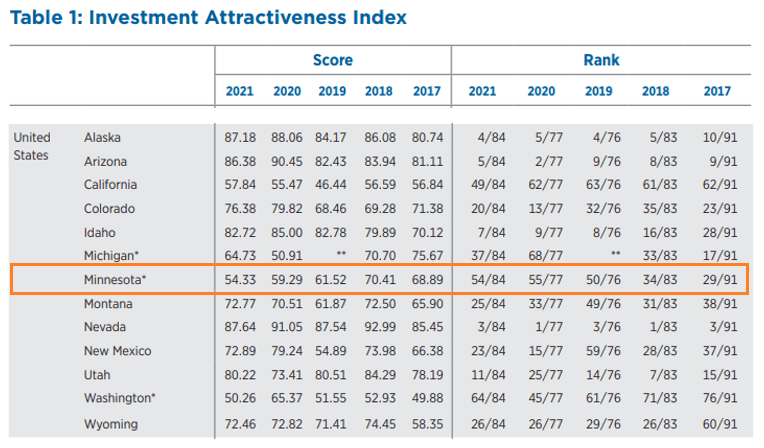

Is Minnesota an attractive mining location?

The United States is considered to be a Tier-1 (or mining-friendly) jurisdiction provided that the underlying project is fully permitted. However, not all States could be termed as Tier-1 jurisdictions. The Fraser Institute's 2021 IAI (read: Investment Attractiveness Index) indicates that Minnesota (the location of PLM's both projects) had one of the lowest IAI scores among peer States during 2021. Things could be slightly different in Fraser Institute's 2022 report (expected to be released in April 2023) but I don't expect Minnesota's score to match those of top jurisdictions (typically a value at or above 80 points). This is one thing to be kept in mind when considering mining projects in Minnesota. The 2021 report describes IAI as:

The Investment Attractiveness Index is a composite index that combines both the Policy Perception Index and results from the Best Practices Mineral Potential Index. To get a true sense of which global jurisdictions are attracting investment, both mineral potential and policy perception must be considered.

{kind=link}

Project permitting - key considerations

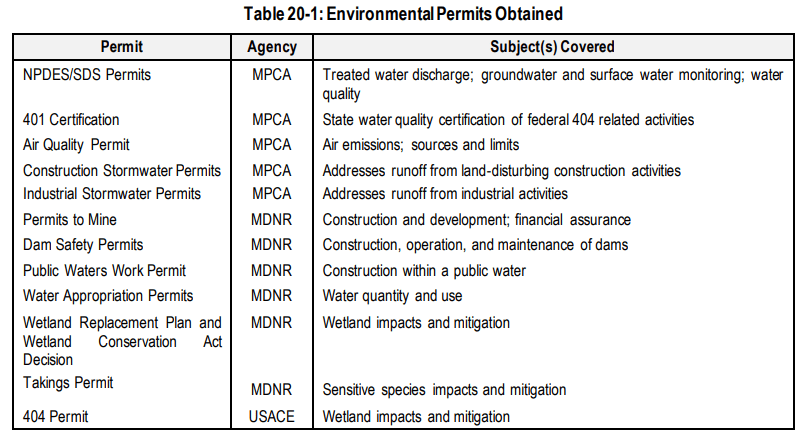

PLM released the FEIS (read: Final Environmental Impact Statement) on the NorthMet Project in 2015 which concluded that the project could be constructed and operated in a manner that meets both federal and state environmental standards and is protective of human health and the environment. PLM subsequently filed and received all the key federal and state-level permits required for the Project's construction, operations, reclamation, closure, and post-closure activities. However, three key permits (Permit to Mine, Water Discharge Permit, and Wetlands Permit) were subsequently held up in litigation. The table below presents details of the key permits obtained by PLM regarding the NorthMet Project.

{kind=link}

The company states in its NI 43-101 on the NorthMet project (relevant extracts),

The federal and state permitting process of the NorthMet Project has been completed, with all necessary permits issued. A limited number of the permits are currently held up as a result of litigation brought by project opponents.

Permitting risk remains for three (03) project permits that are currently held up in litigation or agency action as a result of litigation brought by project opponents.

While these legal challenges may not need to be complete prior to the start of project construction, it is necessary that none of the permits are still held up by litigation (e.g. remanded, suspended, or stayed).

Failure to re-secure the necessary permits could stop or delay the project.

My views: PLM states that it can proceed with project construction despite ongoing litigation, however, investors should be wary of the end result of these legal proceedings. Note that project financing (initial CAPEX of ~$1.2 BB for Phase I) can only be arranged once permitting is completely secured. An unfavorable Court decision could send the share price further south despite the fact that the stock's already trading at the lower end of its 52-week range (at $2.37). That's because NorthMet is the first of PLM's two projects that are targeted for development, and if this project is axed at the permitting stages (worst-case scenario), then it would be unwise to have high hopes for the Mesaba project which is still subject to feasibility studies.

Funding - Another Concern

As noted earlier, Phase I of the Project is estimated to incur CAPEX of ~$1.2 BB. Currently, PLM has cash worth ~$8.6 MM only. In terms of the NRCN JV agreement between PLM and TECK, both companies shall fund their pro rata share of costs (50% for each partner) related to the two projects (NorthMet and Mesaba).

That said, PLM's share of initial CAPEX comes out at ~$600 MM. Good thing is, a majority of PLM's shares (approximately 70%+) are owned by the mining giant, Glencore. Glencore has agreed to fully backstop a rights offering for proceeds of approximately $200MM to fund PLM's share of the ~$170MM NRCM JV initial works program, corporate working capital, and to repay existing indebtedness. However, this initial works program will not be directed toward project development CAPEX, rather it will be used to maintain permits, update feasibility cost estimates, undertake detailed engineering to position NorthMet for a development decision following permit clearances, and also advance Mesaba studies.

My views: It remains a significant concern how PLM will fund its proportionate share of initial project development CAPEX. With Glencore as a major shareholder, it's likely that PLM will need to make additional rights offers which will further dilute value for the minority shareholders (retail investors) but the timing of any such offer is likely to extend far into the future (due to unfavorable macroeconomic factors like metal prices). Alternately, if PLM goes for debt financing, the expected borrowing cost will be high because of the recent rate hikes by the Fed. This whole situation looks even more concerning when we recall that the Project has advanced on permitting but is subject to litigation on three key permits.

Investor Takeaway

Recall that the company claims that the litigations do not impact the JV operator's ability to construct the Project. However, a construction decision is yet to be taken. In the absence of important permits (especially the Permit to Mine) PLM will be unable to conduct mining operations even if it constructs the mine (assuming PLM manages to raise funds for project development in the future ).

In my view, PLM's 50% ownership of the NorthMet and Mesaba projects brightens the prospects of share price growth over the long term. However, in order to achieve that long-term growth, PLM will first need to overcome the following challenges:

- Obtaining clearance on the three important permits that are subject to litigation

- Taking a construction decision on the NorthMet project

- Making an arrangement for funding its proportionate share of NorthMet's initial development CAPEX

- Conducting exploration/drilling activities to better define the resource model, mine design, etc.

That said, I believe the stock is a 'hold' at present until these challenges are overcome.

For further details see:

PolyMet Mining: Things To Consider Before Jumping On The Bandwagon