POYYF - Polymetal International: A Work In Progress

2023-03-20 07:16:28 ET

Summary

- Polymetal recently released its financial results for the full year 2022.

- Declining grades, accumulated inventories, domestic inflation, and an unfavourable exchange rate weighted heavily on financial results, with a negative free cash flow of $445 million.

- It is important to disentangle temporary headwinds from more permanent changes in the company's profitability.

- I expect Polymetal to return to strong profitability in 2023, helped in particular by a weaker rouble and a stronger gold price.

- If gold averages $2000 per ounce and the RUB/USD remains around the current level, I estimate that Polymetal could generate in 2023 around $600 million in free cash flow, or roughly half its current market capitalization.

Polymetal International ([[AUCOY]], [[POYYF]], POLY.L) has just released its financial results for 2022. While there are no significant updates related to its operations, investors got better visibility on the post-war profitability potential of the company. I strongly believe Polymetal has reached an inflection point, and 2023 is going to be a much better year. At the same time, a return to the pre-war days remains unlikely in the short term.

I have recently encountered the argument that, since gold is again close to the $2,000 per ounce level, but many gold producers are significantly below their 2020 peaks, then it automatically means that they are extremely undervalued. Such an argument ignores the fact that the last 3 years have seen a dramatic compression of margins for most miners. The new AISC sector average is more than 20% higher, while the gold price has not been able to sustain new highs for any extended period of time. While inflationary pressures, particularly energy cost inflation, may be in the process of reversing (at least temporarily), and the gold price looks on a firmer footing, the fact remains that any valuation framework must take into account the effect of changing costs of production.

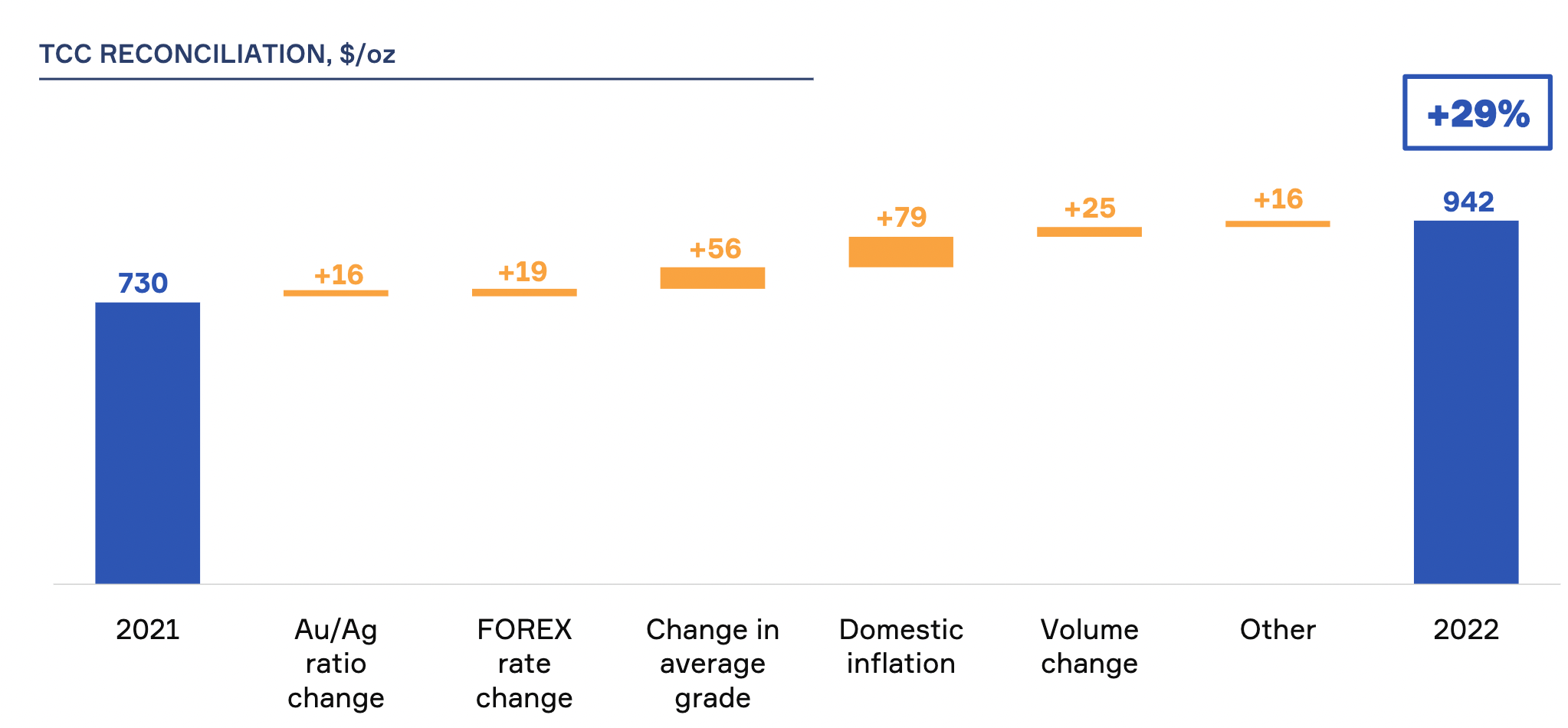

This is particularly true in the case of Polymetal. The Ukraine war has forced the company to decouple from western suppliers, as well as completely alter its export channels. This has led to a buildup in inventory, which has been only partially unwound. In addition, Polymetal has had to battle significant domestic inflation, in Russia and even more so in Kazakhstan. Finally, its profitability has been negatively impacted by exchange rate effects. The result has been a 29% increase in total cash costs (from $730 per ounce to $942) and a 31% increase in AISC (from $1,030 per ounce to $1,344). With the AISC sector average currently close to $1,250 per ounce, Polymetal has transitioned to a higher than average cost producer.

The effect on financial metrics has been evident. While the average realized metal prices were only slightly lower (gold was down 2% from $1,792 to $1,764 per ounce; silver was down 12% from $24.8 to $21.9 per ounce), free cash flow went from $418 million in 2021, to negative $445 million in 2022. Even more concerningly, debt has increased significantly, as the company drew down its credit lines just after the beginning of the war. The ratio of net debt to adjusted EBITDA more than doubled, from 1.13x to 2.35x (for comparison, the company is targeting a ratio below 1.5x in order to resume dividend payments).

Therefore, at first sight, the overall picture is not reassuring. At the same time, it is important to disentangle the effects of temporary headwinds, which are going to reverse in the future, from the more permanent effects, which are going to impact the steady-state profitability of the company going forward.

In the first group of effects, we find everything related to the immediate operational challenges faced by Polymetal as a result of the sanctions. For instance, because of sanctions on Russian gold, the company was unable to sell bullion on the LME and had to arrange for alternative sale channels in the Middle East and China. This created a gap between production and sales in the second and third quarters of 2022. In the fourth quarter, Polymetal almost completely sold down its accumulated inventory. Since total production was 1.712 million gold-equivalent ounces, but sales were only 1.622 million ounces, we can infer that there was a net metal inventory increase of 90 thousand ounces. Polymetal expects to fully unwind the buildup in metal inventory during the first half of 2023, which will boost in particular financial results for the seasonally weaker first quarter of the year. It is also interesting to note that the company explicitly avoided selling its gold to Russian counterparties at a discount, and as a result was able to realize prices that closely tracked international market prices. In fact, the average realized price was $1,764 per ounce, which is just 2% below the average market price of $1,802 per ounce. This difference can be attributed to the fact that sales were skewed to the second half of the year, when gold prices were weaker. A second effect that significantly impacted free cash flow, but that is temporary, is the buildup in working capital excluding metal inventories. Because sanctions disrupted the usual logistical channels, Polymetal opted to increase its inventory of consumables and spare parts beyond its short-term needs. Altogether, changes in working capital caused a $473 million impact on operating cash flow.

Before changes in working capital, operating cash flow in 2022 was $679 million, versus $1,192 million in 2021. Here we can see in particular the impact of the increase in cost of sales and total cash costs per ounce. This topic is quite crucial and is a function of two main factors: inflationary pressures and foreign exchange effects. Both are going to be relevant going forward. Most of the company's expenses are denominated in local currencies (while revenues and most of its borrowings are denominated in dollars). This leaves the company vulnerable to both domestic inflation and changes in foreign exchange. Last year saw the quite unusual combination of higher inflation and a stronger rouble. In 2022, Russia and Kazakhstan experienced strong double-digit inflation (at its peak, inflation reached 12% in Russia and 20% in Kazakhstan). Particularly impactful was the growth in domestic diesel prices, but inflationary pressures were evident also in the services and labor sectors. In addition, the imposition of sanctions caused a sharp increase in logistical costs and the price of consumables, such as explosives, cyanide, and equipment spares. At the same time, the rouble appreciated about 7% against the dollar: the average annual rate stood at 68.6 RUB/$ (2021: 73.7 RUB/$). This increase in operating costs was partially offset in Kazakhstan by a weaker tenge exchange rate of 461 KZT/$ (2021: 426 KZT/$). Altogether, domestic inflation caused a 10.8% increase in total cash costs, while foreign exchange effects caused a 2.6% increase.

Changes in total cash costs (Company's presentation)

{kind=link}

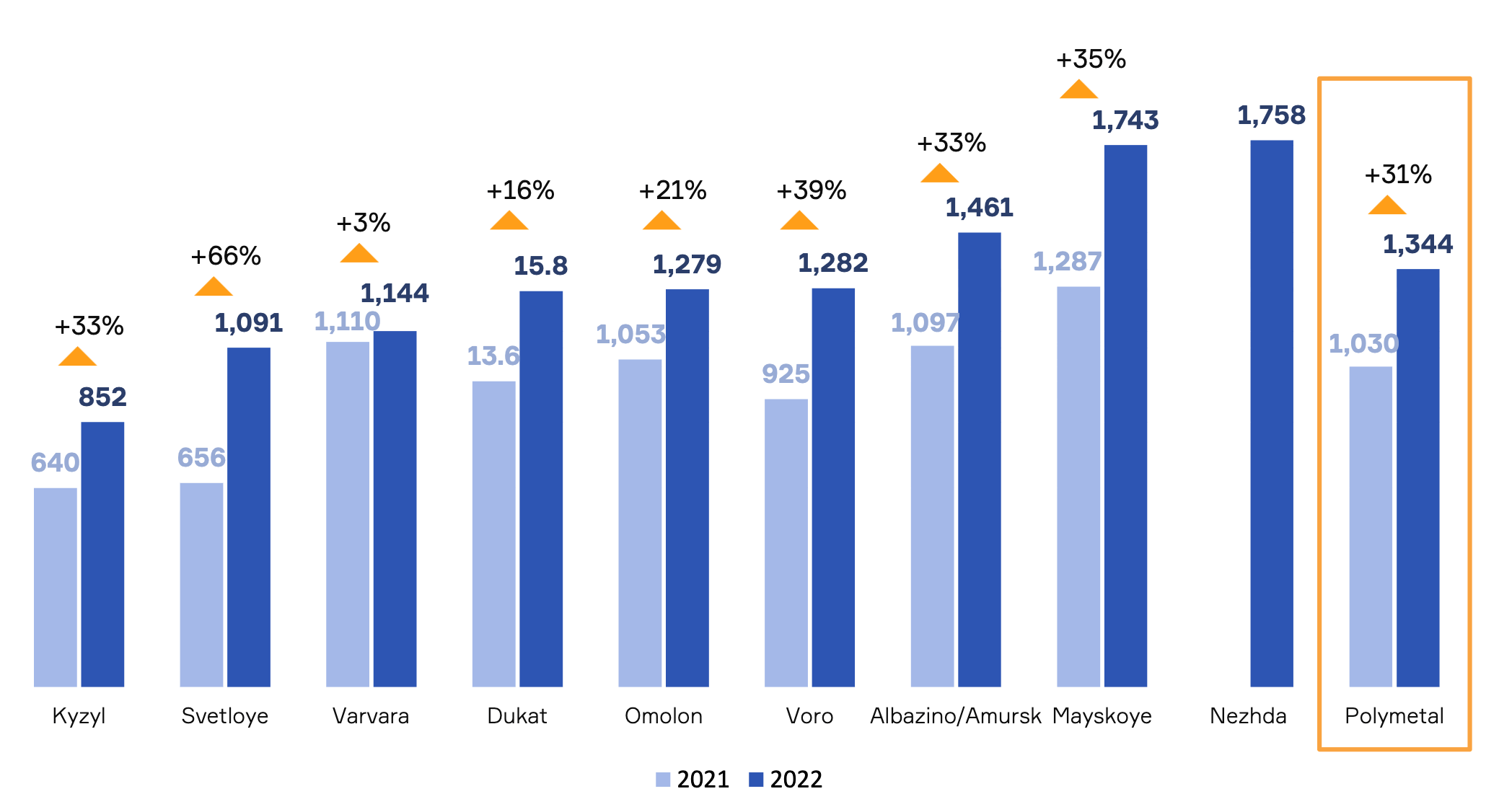

Another important source of increase in cash costs (+7.6%) was the lower average grade. In 2022, the average grade equalled 3.6 gold-equivalent g/t, down 4% compared with 2021. This decrease was mostly planned. Polymetal is in the process of compensating declining grades at its more mature assets (Kyzyl, Dukat, Varvara, and Albazino) with the ramping up of new operations (Nezhda, Kutyn). In particular, 2022 was the first year of operation at Nezhda. While at the moment Nezhda is a high cost operation, with TCC of $1,138 and AISC of $1,758 per ounce in 2022, it is still going through an optimization phase, and has incurred significant capital costs due to increased stripping and infrastructural investments. In 2023, AISC is expected to drop significantly, to around $1,200 per ounce.

AISC by operation (Company's presentation)

{kind=link}

Finally, a look at the future. There is no significant update concerning the process of redomiciliation of the company, except that consultations are in progress and a detailed proposal will be submitted to shareholders. As discussed in my previous article , the change of jurisdiction is crucial to unlock again dividend payments and other corporate actions, such as the spin off or the sales of the Russian assets. News regarding the sales of the Russian assets to Highland Gold was dismissed during the call. It was also mentioned that the current premium listing on the London Stock Exchange will not be maintained, which is obviously bad news, but was already highly likely.

For 2023, Polymetal is guiding for roughly flat production of 1.7 million ounces. A similar dynamic as last year is expected to play out, with grade-driven production declines at Dukat, Albazino and Varvara being compensated by Kutyn, Nezhda and the new Voro flotation plant. Capital expenditures will be similar to this year, between $700 to $750 million. Of this, around 65% consists of non-discretionary expenses required to maintain stable production, and the rest is focused on several optimization projects and other growth initiatives. First and foremost, there is the new POX-2 facility at Amursk for the treatment of refractory ores, which is expected to drive a $100-150 reduction in AISC and, despite logistical challenges, is still on track to be fully commissioned in Q2 2024. There is also the new silver mine at Prognoz (first ore mined in Q4 2023), the backfill plant at Mayskoye (commissioning scheduled in 2024), and the Voro flotation plant (start-up scheduled for Q2 2023). Overall, Polymetal continues to deliver a strong performance from an operational standpoint, despite a challenging environment.

Concerning the valuation, the company currently has a market capitalization of around $1.2 billion. However, it also has $3 billion in long-term debt, of which 65% is denominated in dollars. Because of the difficulties in obtaining dollar-denominated loans, the company is in the process of refinancing part of the debt in renminbi. As a result, the average cost of debt is increasing, currently standing at around 5.5% (significantly up from 2.9% in 2021). Looking at the maturity profile, we see that the 2023 repayments are fully covered by the current $630 million cash position. However, 2024 in particular is going to see repayments of more than $730 million.

Debt breakdown (Company's presentation)

{kind=link}

Based on the company's guidance concerning production volumes, cash costs and capital expenditures, I estimate that Polymetal should be able to generate around $600 million in free cash flow during 2023. This estimate is based on a RUB/USD exchange rate of 77 and average realized gold price of $2,000 per ounce. Given that the balance sheet looks stretched at the moment, I would prefer to see the company use the cash flow to deleverage, rather than to immediately resume dividend payments, especially if increasing the maturity profile will lead to a higher cost of debt. In any case, the CEO mentioned that he expected Polymetal to be in the position of resuming dividend payments at some point during the year, conditional on the redomiciliation being successfully completed.

In conclusion, Polymetal remains a work in progress. I am convinced that we have reached a turning point and that the downside from here is limited. With the rouble sliding and the gold price on a firmer footing, 2023 could be a record year for the company in terms of free cash flow generation. This creates an asymmetric opportunity for patient investors. At the same time, there remains a significant degree of risk. The change in jurisdiction will probably make the company untradable for some time for most investors. The company is exposed to changes in the exchange rates and to domestic inflation. The debt burden is significant. Yet, I remain optimistic, a consequence of my long-term bullish view on gold and trust in the quality of this management team.

For further details see:

Polymetal International: A Work In Progress