POYYF - Polymetal May Come Back To London But There's A Catch

2023-09-29 06:43:06 ET

Summary

- Polymetal published its H1 2023 results recently.

- The company is going to sell its Russian assets.

- After delisting from the London Stock Exchange this year, Polymetal may return to LSE in the next couple of years.

Before the Russian invasion of Ukraine, Polymetal ([[POYYF]], [[AUCOY]]) was one of the two Russian gold miners, together with Polyus (OPYGY), which I covered on Seeking Alpha. My last call on the stock in 2021 was with a "buy" recommendation, though implications caused by the war made the stock rating largely irrelevant.

When the war broke out, Polymetal for some time remained one of the very last companies with Russian assets which kept trading on the London Stock Exchange and was untouched by sanctions. However, sanctions against the Russian entity of Polymetal were just a matter of time. In early August, the trading of LSE shares was suspended, and now the company has to make an important strategic choice before it returns to LSE.

Considering a recent flow of news about Polymetal, alongside a recent publication of H1 2023 results, I think it's time to revisit the stock with a fresh view of the company.

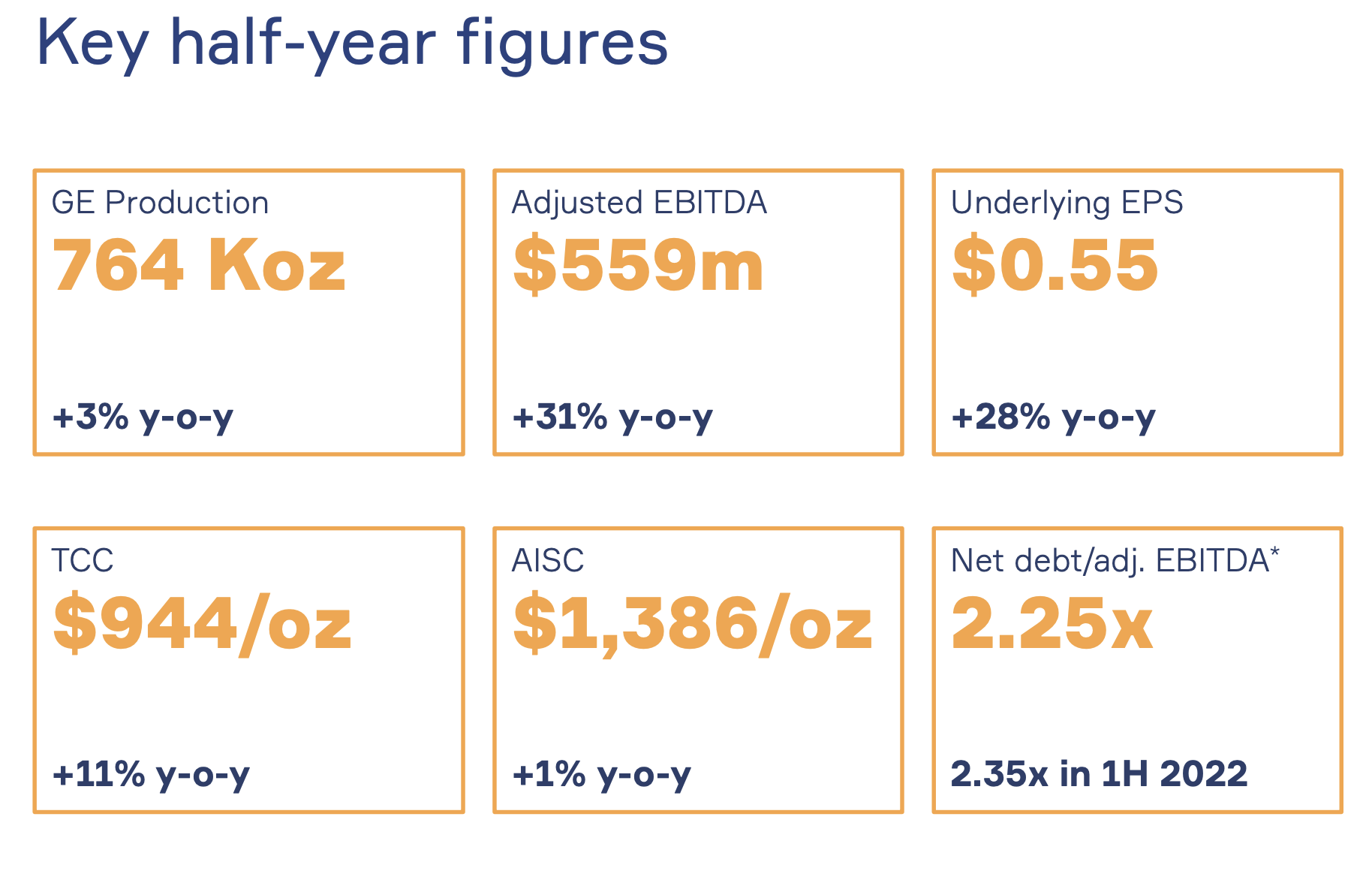

Half-Year Results

On September 25th, the company published its H1 2023 financial results, which are quite decent, in my opinion.

{kind=link}

Revenue is up 25% year-over-year to $1,315 million. Gold prices were steadily over $1900 per oz. most of the H1 2023 period, which ensured a solid half-year result.

EBITDA went up by 31% Y-o-Y to $559 million.

Adjusted Net profit is up 28% Y-o-Y to $261 million.

Total Cash Costs ((TCC)) are modestly up (+11% Y-o-Y), and this increase has been very well compensated by strong growth of financial metrics.

With a Net debt/adjusted EBITDA over 2.25x, the debt load is not low by any means. Nonetheless, it should be noted that most of the debt belongs to a Russian subsidiary of Polymetal. This factor will be important to keep in mind in further discussion.

From an operational standpoint, Polymetal has been almost unaffected by sanctions, except tolerably higher cash costs caused by more complicated logistics (purchasing equipment and spare parts through third parties) to maintain assets in Russia.

Getting Rid Of Russian Assets Is No Easy Task

For reference, Polymetal consists of two major parts: around 2/3 of its EBITDA is generated from Russian assets, and the remainder comes from assets in Kazakhstan. Both parts are managed by Polymetal International, a holding entity that recently relocated from Jersey (an island country) to Kazakhstan. Since late May, the Russian subsidiary of Polymetal, JSC Polymetal, remains under the most severe, blocking sanctions of the US.

Almost immediately after the sanctions announcement, the company said it may sell its Russian business, though as of late September, the company hasn't provided any details on a potential deal.

What factors complicate the process of selling the Russian business unit of Polymetal:

- Lack of buyers and specific conditions of a potential deal. Polymetal is the second largest gold producer in Russia, and Polyus, the biggest Russian gold producer, looks like the only company that could purchase Polymetal's assets in Russia and "digest" them financially. Polymetal could sell its assets in parts to smaller gold producers, but the management denied such an option. This leaves Polyus as the only candidate, though the CEO of Polyus said that the company hasn't got an offer from Polymetal so far.

- New export duty will require a discount for Russian assets. Starting this October, the Russian government is introducing a new flexible export duty linked to a ruble exchange rate. Polymetal may pay $30-40 million in this export duty by the end of this year and $100-130 million in 2024. This may roughly equal to 15-18% of EBITDA of the Russian segment of Polymetal. Therefore, a sale of the Russian business will inevitably require a discount.

As for Russian assets themselves, Polymetal has eight production assets and four development projects, including one of the world's largest platinum group deposits, Viksha, in Karelia.

In Russia, there are the following Polymetal assets:

- the Dukat hub (producing 18.8 million ounces of silver),

- Omolon hub (201 thousand ounces of gold),

- Albazino (249 thousand ounces of gold),

- Mayskoye (139 thousand ounces),

- Svetloye (109 thousand ounces),

- Vorontsovskoye (93 thousand ounces),

- Nezhdaninskoye (21 thousand ounces).

All numbers are as of 2021 (the most recent disclosed by the company).

In Kazakhstan, the company owns the Kyzyl deposit with a production of 360 thousand ounces, and Varvarinskoye (198 thousand ounces). Thus, gold production in Kazakhstan is only 40% of the overall gold production of Polymetal, and the rest is being produced in Russia. Not to mention that all prospective development projects are also located in Russia.

Selling the Russian business is a tough, but unavoidable option for Polymetal. The management clearly indicates the company plans to sell the Russian segment in the next 6 to 9 months. For now, the company's primary listing will stay in Kazakhstan, at AIX (Astana International Exchange).

A Comeback To LSE Is Possible, But Is It Worth It For Investors?

According to Bloomberg , CEO of Polymetal Vitaly Nesis said the company may come back to the London Stock Exchange once it sells the Russian assets. In this regard, the key concern about Polymetal is that without its Russian part, the company looks hardly interesting to investors.

Surely, there will be obvious benefits from selling the Russian business:

- A possible, almost complete reduction of debt (given it formally belongs to the Russian unit);

- Complete elimination of sanctions exposure;

- Proceeds from the sale may be used for financing new projects and paying dividends.

However, Kazakhstan is definitely not a top-tier jurisdiction for gold miners, and since my last bullish rating on the company, plenty of competitive options in the sector, like Agnico Eagle Mines ( AEM ), appeared. Once the deal is finalized, I'll be able to do a deeper analysis of a "renewed" Polymetal, but for now, there are simply too many moving parts.

If you hold Polymetal shares, I don't see reasons to sell the stock. I can't recommend buying the stock either, given there's a high degree of uncertainty regarding selling the Russian assets. The stock listing in Kazakhstan will also impair the accessibility of the stock for Western investors, limiting the pool of potential shareholders.

For further details see:

Polymetal May Come Back To London, But There's A Catch