PDLB - Ponce Financial Group: Cheap But Not Without A Reason

2023-09-28 07:54:20 ET

Summary

- Ponce Financial Group is a small holding company that owns a bank with a market capitalization of $167.5 million.

- The bank has seen growth in loans, deposits, securities, and cash balances, but its financial performance has been volatile.

- The company has taken on a significant amount of debt, which raises concerns and outweighs the positive aspects of its growth.

As a general rule of thumb, I tend to stay away from companies that have a market capitalization lower than $200 million. And even then, I am quite selective. But every so often, I come across a company that I will make an exception for. One such firm happens to be Ponce Financial Group ( PDLB ), a very small holding company that owns a bank and that happens to have a market capitalization of $167.5 million as of this writing.

What initially drew me to the bank is the fact that it is trading at a price that is well below its tangible book value per share, which does indicate some upside potential. However, the bank also has some other issues. For instance, it has a large amount of debt on its books and its financial performance from quarter to quarter or year to year has not been exactly ideal. Given these factors, I would argue that there is a lot of risk bottled up into this small firm and, for most investors, the reward likely won't be worth assuming that risk. At the end of the day, this has led me to rate the enterprise a 'hold' for now, though it wouldn't take me much to downgrade it to something more bearish.

A bank with issues

Ponce Financial Group emerged when its predecessor, Ponce Bank Mutual Holding Company completed a conversion and reorganization and then subsequently merged with a bank called PDL Community Bancorp. This occurred back in January of 2022. Today, the institution operates 13 full-service banking offices and six mortgage loan offices. All of these locations are split between parts of New York and New Jersey. But the vast majority of its exposure is to the former, with the Bronx hosting four branches and Queens and Brooklyn both hosting three.

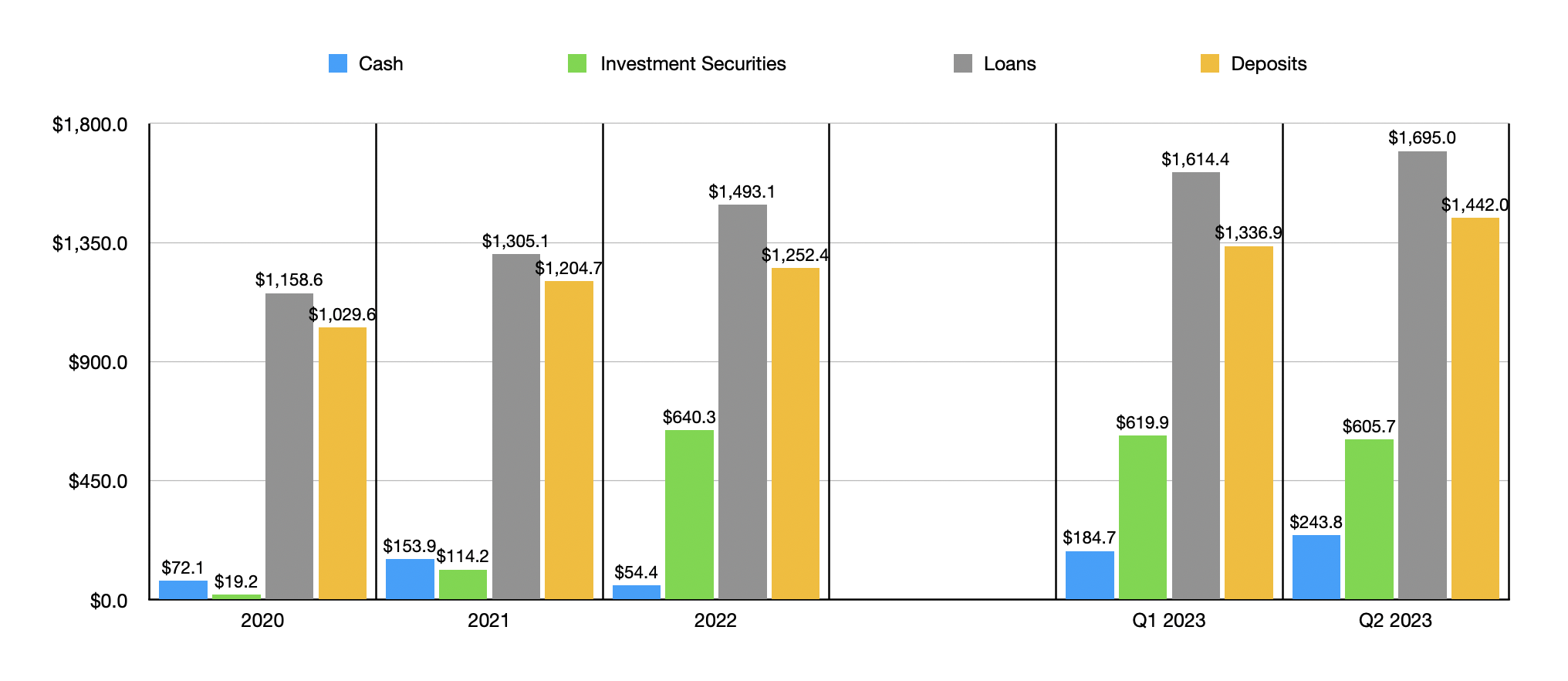

Through these locations, the company engages in traditional commercial banking activities. It accepts deposits from the public, including both commercial customers and consumers. It then allocates this capital toward those who need it, usually in the form of loans. Examples have included mortgage loans, construction and land loans, business loans, consumer loans, and more. Though a smaller piece of the company, it does engage in the purchase of securities for the purpose of generating attractive returns. This is a part of the enterprise that has actually grown significantly in recent years. Back in 2020, it had only $19.2 million dedicated to securities. By the end of the second quarter of this year, that number had grown to $605.7 million.

{kind=link}

The value of its securities is not the only thing that has grown in recent years. Back in 2020, the bank had loans totaling only $1.16 billion. Loans had grown to $1.49 billion by the end of 2022 before climbing to nearly $1.70 billion by the end of the second quarter of this year. Although the company is diverse in the composition of its loans, the vast majority of this portfolio involves mortgage loans, with multifamily residential properties leading the way at $550 million. No another $351.8 million involves investor owned one to four family residential properties, and non-residential properties come in third place at $317.4 million. Only a small portion of its loans, approximately 1.9% in all, fall outside of the mortgage category. And these consist of business loans and consumer loans.

The overall rise in loans was only made possible by an increase in the value of deposits. After all, deposits are often what are used as fuel when it comes to the banking sector. At the end of 2020, total deposits at the bank came in at $1.03 billion. They grew to $1.25 billion at the end of 2022 before climbing further to $1.44 billion at the end of the second quarter. This is impressive considering how many other banks saw deposits drop because of the banking crisis earlier this year. On top of this, as of the end of the most recent quarter, only 22.5% of Ponce Financial Group's deposits are classified as uninsured. Given all that is going on in the banking sector, I prefer a reading of 30% or lower.

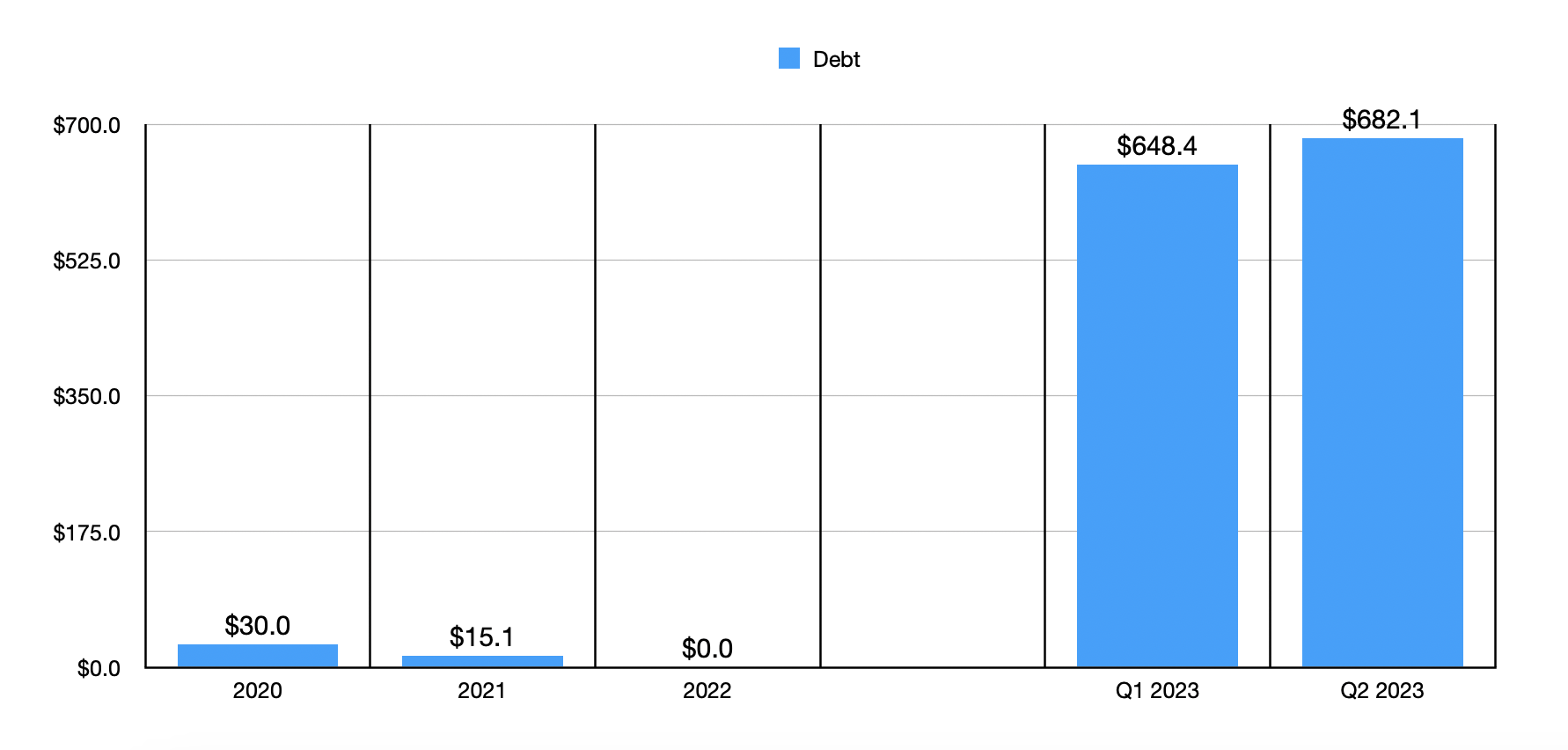

So far, all of this looks positive. The company even can brag that the value of cash on its books has increased nicely as well. At the end of last year, cash and cash equivalents totaled $54.4 million. They had grown to $243.8 million by the end of the most recent quarter. But this starts to touch on the broader problem, which is that some of the increase recently in the company's financial position has happened because management has taken on a meaningful amount of debt. At the end of last year, the company had no debt on its books. And in the span of two quarters, debt had grown to $682.1 million.

{kind=link}

The increase in debt was not the only interesting development. At the end of 2021, the company had nothing in the way of preferred stock. But in 2022, it issued $225 million worth of preferred units to the US Treasury as part of an $8.7 billion investment by the Treasury aimed at encouraging institutions to provide loans, grants, and other activities, to small businesses, minority owned businesses, and individuals in low income and underserved communities. Unlike the debt picture, I don't view this as particularly negative. This is especially true because, during the first two years, there was a 0% dividend rate on the preferred units. And after that window of time, that rate will increase to between 0.5% and 2% per annum. Given who the other party is in this transaction and those terms, I actually view this as a positive development on its own.

{kind=link}

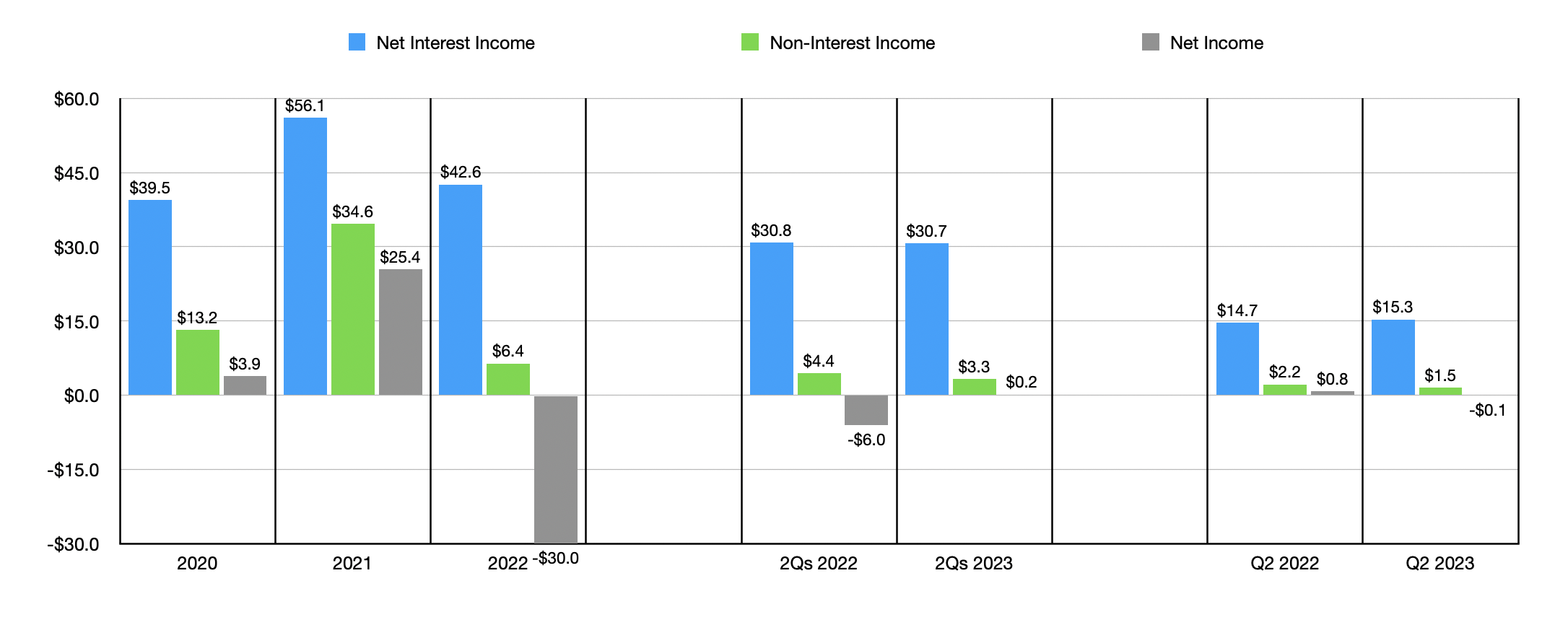

The general increase in the company's asset base should be viewed as a positive thing. However, financial performance over the past few years has been all over the map. Net interest income, for instance, rose from $39.5 million in 2020 to $56.1 million in 2021. Then, in 2022, it fell to $42.6 million. As the chart above illustrates, non-interest income and net profits have also been incredibly volatile. An entire article could probably be written just on the various fluctuations that were responsible for the company's financial condition gyrating this much. Regarding the big loss in 2022, however, there were a couple of key drivers there.

As an example, during that year, the company reported a $17.9 million write off associated with Grain and it allocated about $5 million to charitable causes to the Ponce De Leon Foundation. An increase on the interest cost on borrowings, as well as higher amounts that the company had to pay on both borrowings and deposits (excluding certificates of deposit), played a role here. For those not aware, Grain was a startup company in the fintech space that aimed to provide a mobile application for the underbanked, minorities, and other disadvantaged parties. However, around $25.5 million of the microloans that the fintech platform issued were deemed to be fraudulent. So Ponce Financial Group had to eat a good portion of that loss.

As you can see in the prior chart, financial results for Ponce Financial Group continued to be volatile into the current fiscal year. Net interest income and non-interest income were both down in the first half of 2023 compared to the same time last year. However, its bottom line results did improve slightly. The other good thing is that, despite this volatility, the bank has been successful in continuing to increase its book value per share. By the end of the second quarter of this year, book value per share for the enterprise had grown to $10.94. That's up slightly from the $10.77 that the institution saw in 2022.

Speaking of book value, it would be helpful for us to discuss how shares look from a pricing perspective. Normally, I would want to value a company in this space using its price to earnings multiple. But given the volatility of profits from year to year, I don't believe that this would be All that useful. Perhaps the best way is to compare the company to its book value. In that case, shares are trading at a 29.5% discount to what the value of the company's assets are listed for on a net basis.

Takeaway

In my opinion, Ponce Financial Group it's definitely an intriguing prospect. Loans, deposits, securities, and cash balances, have all increased nicely over the past few years. The general trend has continued into the current fiscal year. The preferred stock is interesting because of the terms it was issued under. And I like the uninsured deposit exposure of the institution. At the same time, the value investor in me is a stickler for consistent financial performance. When you combine that with the debt on the company's books, that outweighs the positives that I am looking at. As such, I do believe that a 'hold' rating is appropriate right now.

For further details see:

Ponce Financial Group: Cheap, But Not Without A Reason