POOL - Pool Corporation: The Last 2 Years May Have Been An Anomaly As Sales Stabilize

2024-01-10 15:34:27 ET

Summary

- Pool Corporation has benefited from pandemic-driven demand and inflation, but sales are expected to normalize and margins may decline.

- The company has manageable debt levels and strong solvency metrics, but its current ratio indicates inefficient asset management.

- Revenues have seen significant growth, but recent quarters have shown lackluster performance, and future growth is uncertain. Valuation suggests the stock is trading at a premium.

Investment Thesis

Pool Corporation ( POOL ) has seen tremendous growth in recent years due to the pandemic pent-up demand and has benefited from an increase in inflation. I believe that the company's boom years are behind them, the sales numbers will begin to normalize, and margins may continue to fall further as inflation subsides.

Briefly on the Company

Pool Corporation, as the name suggests, is the world's largest wholesale distributor of everything pool-related, which is swimming pool equipment and supplies, parts, and other related products. The company doesn't build pools or manufacture the products related, but rather a middleman between the manufacturers and customers who need all things pool. The company distributes pool chemicals, filters, pumps, lighting, liners, and even grills and outdoor furniture. It is a one-stop shop for all things related to pools.

Financials

As of Q3 2023, the company had around $85m in cash and equivalents, against around $1B in long-term debt. Compared to the available cash, that is a significant amount of debt but it's not that much compared to its market cap of around $15B. Many people will avoid companies with excess leverage; however, they would be missing out on a potential investment, especially if leverage is manageable and the company is using it smartly. There are a few metrics I like to look at to decide whether the debt on books is a problem or not. The debt-to-assets ratio has been hovering around 0.24 to 0.54 over the last five years. Anything under 0.6 I consider not overleveraged. The next metric, which is the debt-to-equity ratio also shows that the company is not overleveraged, as I deem anything under 1.5 to be acceptable. Over the last 5 years, the company has been hovering in the range of 0.65 to 3.0. The high of 3.0 was in 2018 and it has dropped significantly ever since. Lastly, I like to look at how easily can the company cover its annual debt obligations, which is the annual interest expense on debt. Many analysts consider that an interest coverage ratio of 2x is sufficient and healthy, however, I'd like to see at least a 5x, which allows for a lot more flexibility in the company's operations, for example, there is a higher chance that during the tougher times, the company will still be able to cover its obligations, whereas a 2x is a bit close for comfort. The company passes all the solvency metrics with flying colors, which tells me that the company is at no risk of being insolvent any time soon.

{kind=link}

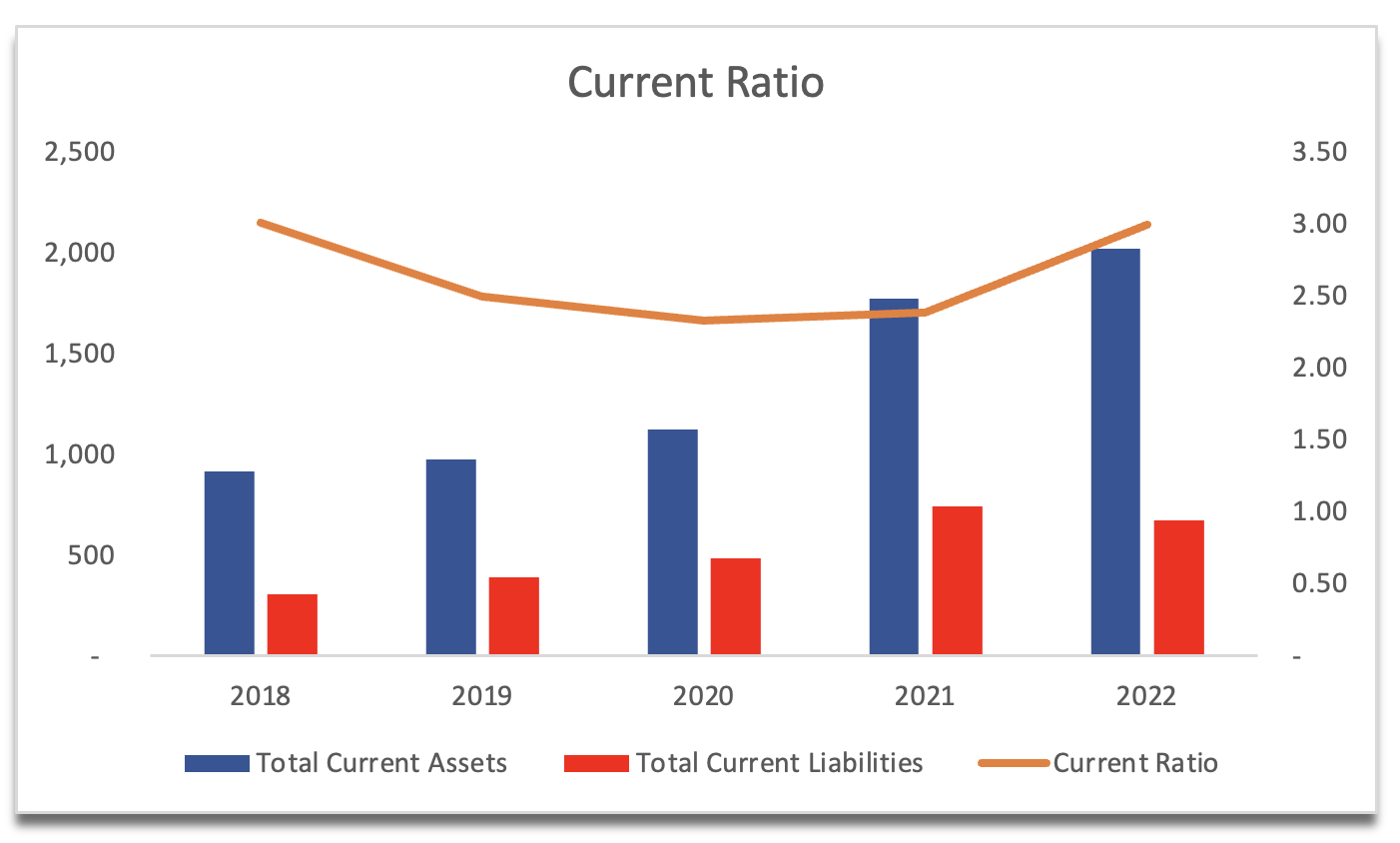

The company's current ratio has been slightly on the higher end of what I like it to be, which makes it an almost inefficient use of assets. Don't get me wrong it's still better to have a high current ratio than anything below 1, however, the company could do better at managing its assets. I consider a current ratio range of 1.5 to 2.0 to be efficient, and the good news is that it has come down in the recent quarter to 2.58 from around 3.0 as of FY22. So, it’s safe to say that the company has no liquidity issues.

{kind=link}

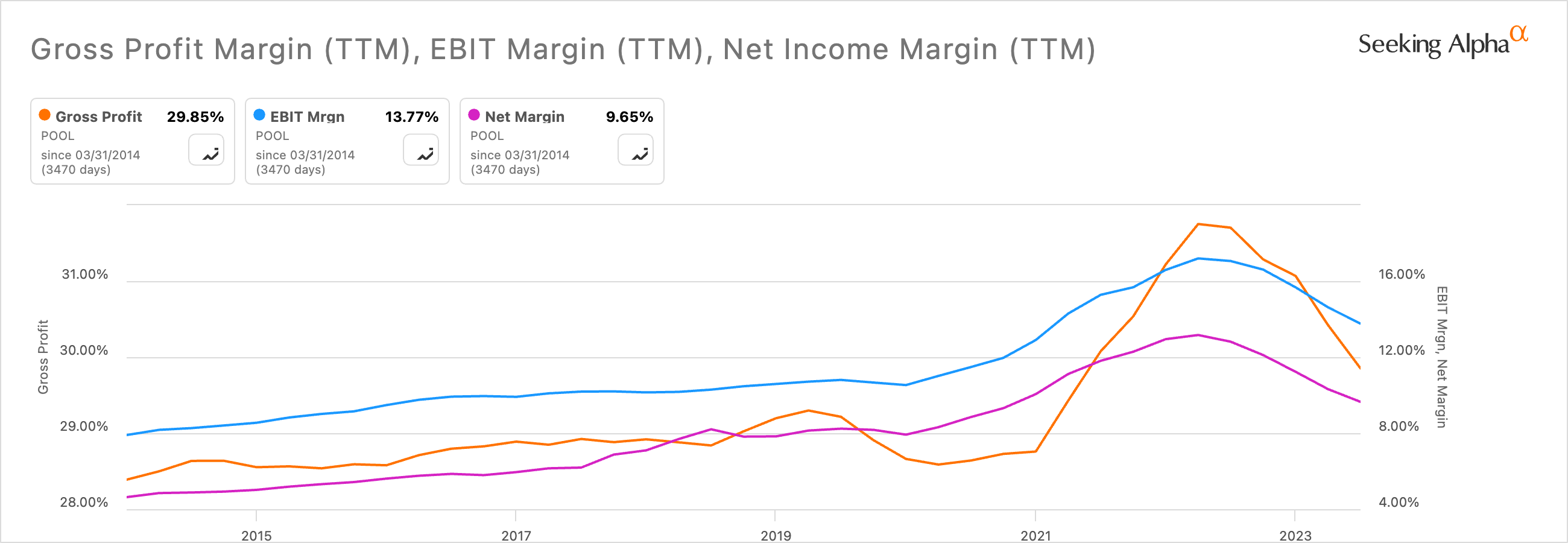

Looking at the company’s efficiency and profitability metrics, the margins have been suffering in the latest quarters. The reason for such a lackluster performance was the company had a lot of inventory buildup from before , which had to be sold at lower prices. The company is looking for at least 30% gross margins in the long term, which it has dipped below in the most recent quarter. Nevertheless, the management is confident that the company will be able to achieve this going forward.

{kind=link}

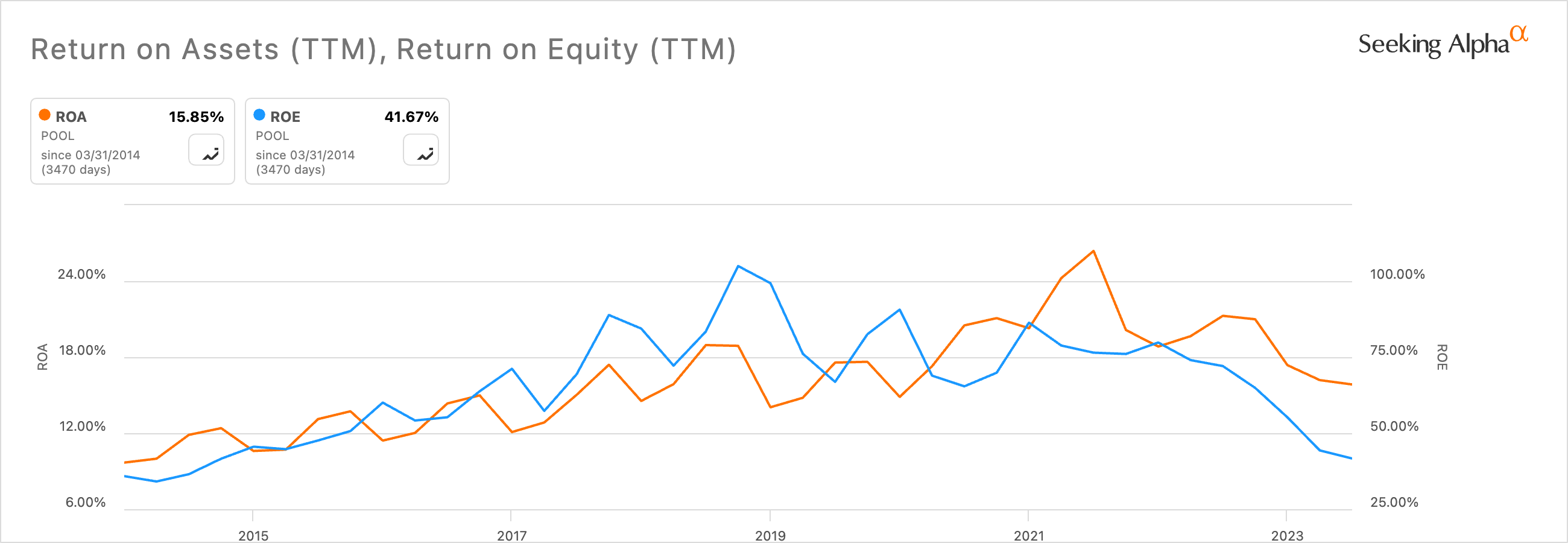

Unsurprisingly, the company’s ROA and ROE have also dipped in the most recent times, however, these are still more than acceptable in my opinion. Once the sales growth returns and margins improve, the company’s ROA and ROE will follow suit. The management seems to be good at using the shareholder capital and the company's assets efficiently, thus creating value.

{kind=link}

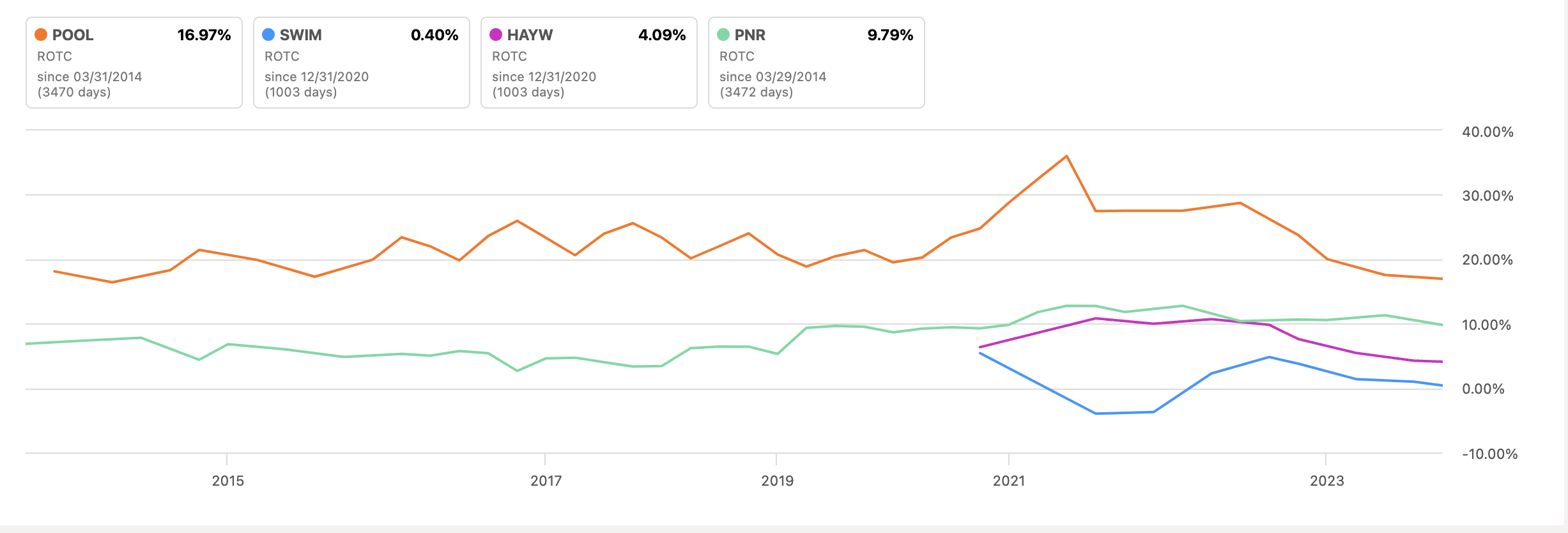

The company's return on total capital, which measures how efficiently the capital is employed, has seen a similar decline in recent quarters, however, is still very impressive. Furthermore, if we compare it to some of its competition, we can see that the company is head and shoulders above its peers, which tells us that the company has a competitive advantage and a strong moat. That is what I would expect from a company with a ticker of POOL. I would have expected a bit more from a company with a ticker symbol of SWIM also, but it is what it is.

{kind=link}

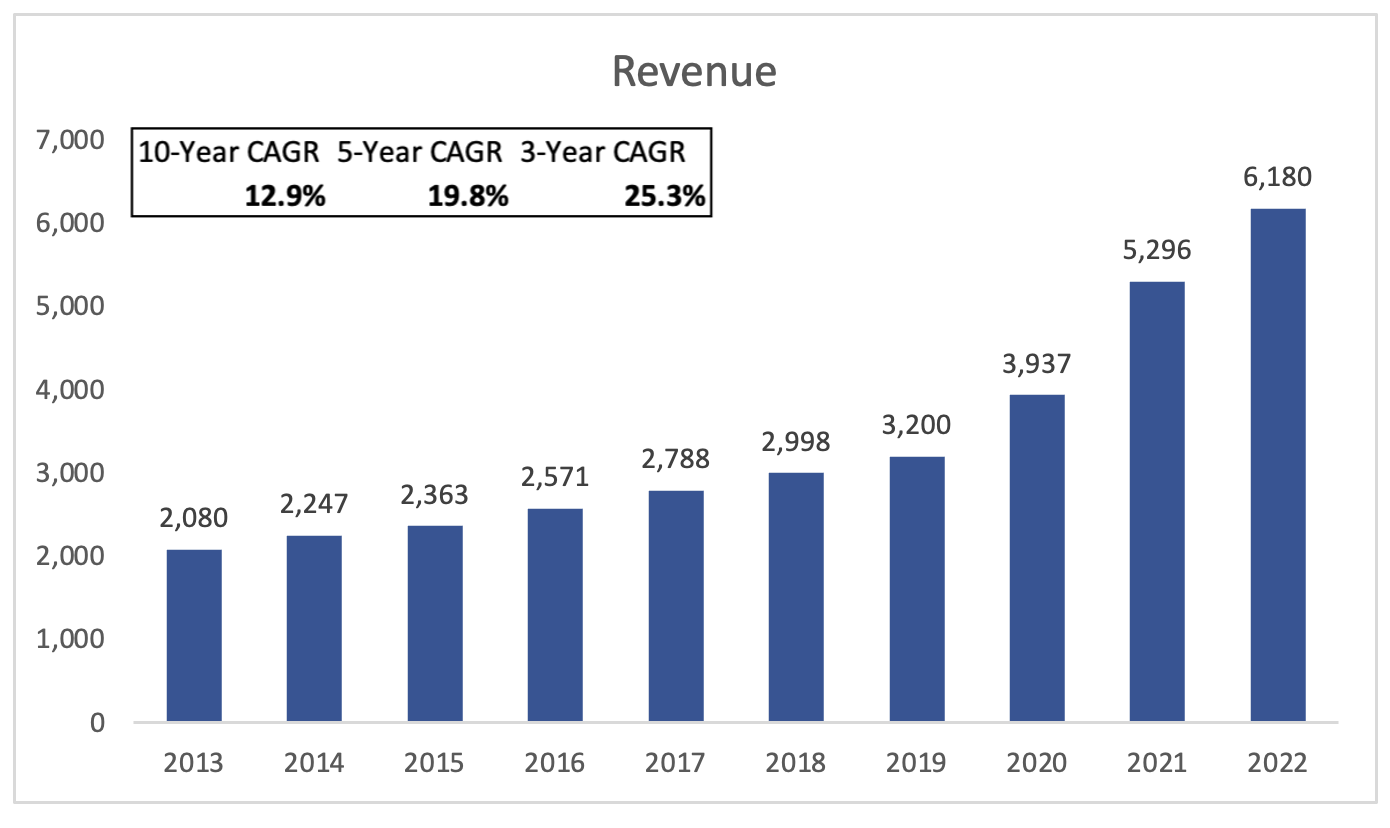

The company's revenues saw a significant increase over the last decade and more recent CAGR has been even better. Higher inflation numbers and post-lockdown demand for outdoor accessories have played a huge role as FY21 saw a massive increase in top-line growth. It was not sustainable as the growth halved from FY21 to FY22. Surprisingly, analysts' estimates are showing a 10% decline in FY23, and hardly any growth in the next two years, which doesn't match with the company's prior performance. Well, history is not an indication of future performance; however, I tend to take analyst estimates past a year with a grain of salt, since it is impossible to predict how the company will end up performing, given certain economic conditions. Since the company benefited from high inflation, I would expect now that inflation isn’t as high, revenues would suffer too.

{kind=link}

Overall, the recent quarters are not giving me high hopes of better performance for now. It seems that since the pent-up demand after the lockdowns were lifted and inflation is coming back down to what the FED wants it to be, I would expect further lackluster performance in top-line growth and probably further deterioration in margins as the company continues to sell off the lower priced inventory. The balance sheet of the company is decent, which tells me that the company wouldn't be affected by a macroeconomic downturn. The debt levels aren't too high and are manageable. Furthermore, the company's competitive advantage and the moat are the best in the business.

Valuation

I usually approach my valuation models with a conservative mindset, and this time’s no different. I don’t think I’m comfortable assuming growth in revenues at the company’s 10-year CAGR because I would like to have a bit more margin of safety. For that reason, my base case scenario CAGR is about 7% lower than its historical 10-year CAGR, which gives me quite a decent margin of safety. The company's revenues doubled in the last 5 years, and with a 5% CAGR for the next decade, it’ll take more than 10 years. To cover my bases, I also included a more conservative outcome and a more optimistic outcome. Below are those assumptions with their respective CAGRs. An added extra MoS is that even in the optimistic case, the company’s CAGR is lower than what it managed to achieve.

{kind=link}

In terms of margins and EPS, I reduced these also for the next few years, as I assume that the company may continue to suffer from lower inflation and lower demand overall, which will result in lower profitability. For extra safety, I modeled that the company will not see the efficiency and profitability it saw in the last two years because I don’t think inflation and demand will pick up considerably again. Below are those assumptions.

{kind=link}

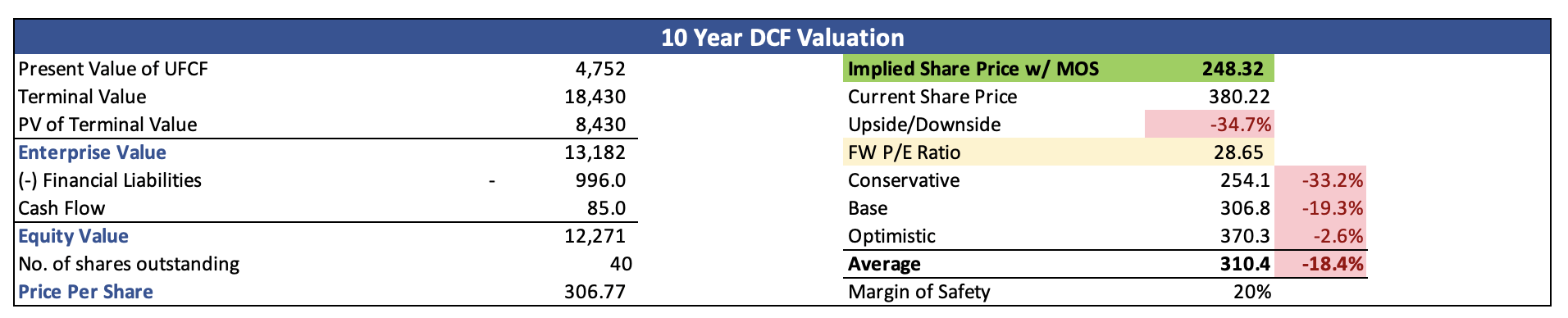

I decided to use the company’s WACC of 8.14% as my discount for the model, as I believe I’ve beaten down the estimates considerably, and assume a 2.5% terminal growth rate, as I would like the company to at least match the long-term US inflation goal. To top it all off, and to achieve that sleep-good-at-night feeling knowing that I didn’t overpay for a company, I added another 20% margin of safety to the intrinsic value calculation. With that said, POOL’s intrinsic value and what I would be willing to pay for it is around $248 a share, which means the company is trading at a decent premium to its fair value.

{kind=link}

Closing Comments

With such low-balled estimates, it is hard to find companies that pass the test. There certainly are some that do; however, POOL is not one of them right now. I would like to see how the company's revenues react to lower inflation going forward and if the company still has some lower-priced inventory to go through before regaining its profitability and efficiency. I don't think we will see the high numbers of FY21, so I would need a little bit more proof that the company is going to maintain 30% gross margins. Furthermore, I want to see how the top-line growth develops over the next couple of quarters. The lackluster growth seen for FY23 was very unusual when the company was growing at such a great pace. The company doesn't need to grow very quickly in my opinion. I would rather see more efficiencies coming through which would lead to higher profitability.

For now, there is much more uncertainty in the future, therefore, I am assigning the company a hold rating until I see some improvements in top-line growth and/or profitability.

For further details see:

Pool Corporation: The Last 2 Years May Have Been An Anomaly As Sales Stabilize