ABB - Poor Earnings Shallow Recession To Drag S&P 500 Initially But I Expect Strong Recovery To 4151 By Year-End 2023

Summary

- I expect S&P 500 2024 forward earnings to be $237.2, which in my opinion, should fetch 17.5X, a multiple more in line with 3.5-4%, 10-year treasuries.

- I also expect S&P 500 earnings to decline by 5% to about $210 in 2023 and then recover by 13% on a smaller base to $237 in 2024.

- In my view, the stock market in 2023 will be a trader's market, offering opportunities to both shorts and longs.

- I believe that the S&P should test its Oct 2022 low of 3,577 in the first 4 months of 2023.

- If one were to buy and hold at today's index of 3,837, the one-year return at a target of 4,151 works out to 8%, or if averaged out lower to 3,600, it works out to 15%.

I Expect A Slow Burn with S&P 500 Earnings Dropping to $210 in 2023

Company management and analysts have not been forthcoming enough in reducing S&P 500 ( SP500 ) earnings estimates, and are still fostering hopes of earnings not declining significantly in 2023. It is indeed delusional as Morgan Stanley's Lisa Shalett puts it, that CEOs and subsequently, analysts haven't lowered 2023 and 2024 earnings estimates commensurately - even as many confidently predict a recession. I expect inflation, which caused a single digit revenue increase for S&P 500 companies to reduce gradually in 2023. The 6-8% increase in CPI and CPE throughout 2022, which depleted customers wallets, also contributed strongly to the S&P 500 top line. We paid higher at the pump and at the grocery store because companies passed along these costs to us, their customers. This is highly unlikely to happen in 2023, especially on a higher base. In fact, excess inventory and lower demand should lead to lower prices across the board.

I see the slow reaction from investors and traders to lower earnings guidance as the biggest threat to the market in the first quarter of 2023. For now, however, it feels like a slow burn till Q4-22 earnings season starts in earnest in the third week of Jan 2023, when Q1-2023 and full year 2023 guidance finally tips over and the disappointment hits the markets like a freight train.

It is not that analysts have been sleeping, they did mark earnings down 5.6% for Q4 2022 in October and November.

According to FactSet the Q4 bottom-up EPS estimate (which is an aggregation of the median EPS estimates for Q4 for all the companies in the index) decreased by 5.6% (to $54.58 from $57.79) from September 30 to November 30. Thus, the decline in the bottom-up EPS estimate recorded during the first two months of the fourth quarter was larger than the 5-year average, the 10-year average, the 15-year average, and the 20-year average. The fourth quarter also marked the largest decrease in the bottom-up EPS estimate during the first two months of a quarter since Q2 2020 (-35.9%).

The bottom-up EPS estimate for CY 2023 declined by 3.6% (to $232.52 from $241.22) from September 30 to November 30."

As of now, in my opinion, consensus bottoms up revenue estimates of $232.52 are still way too high and don't reflect weaknesses in the energy, real estate, technology and communication sectors:

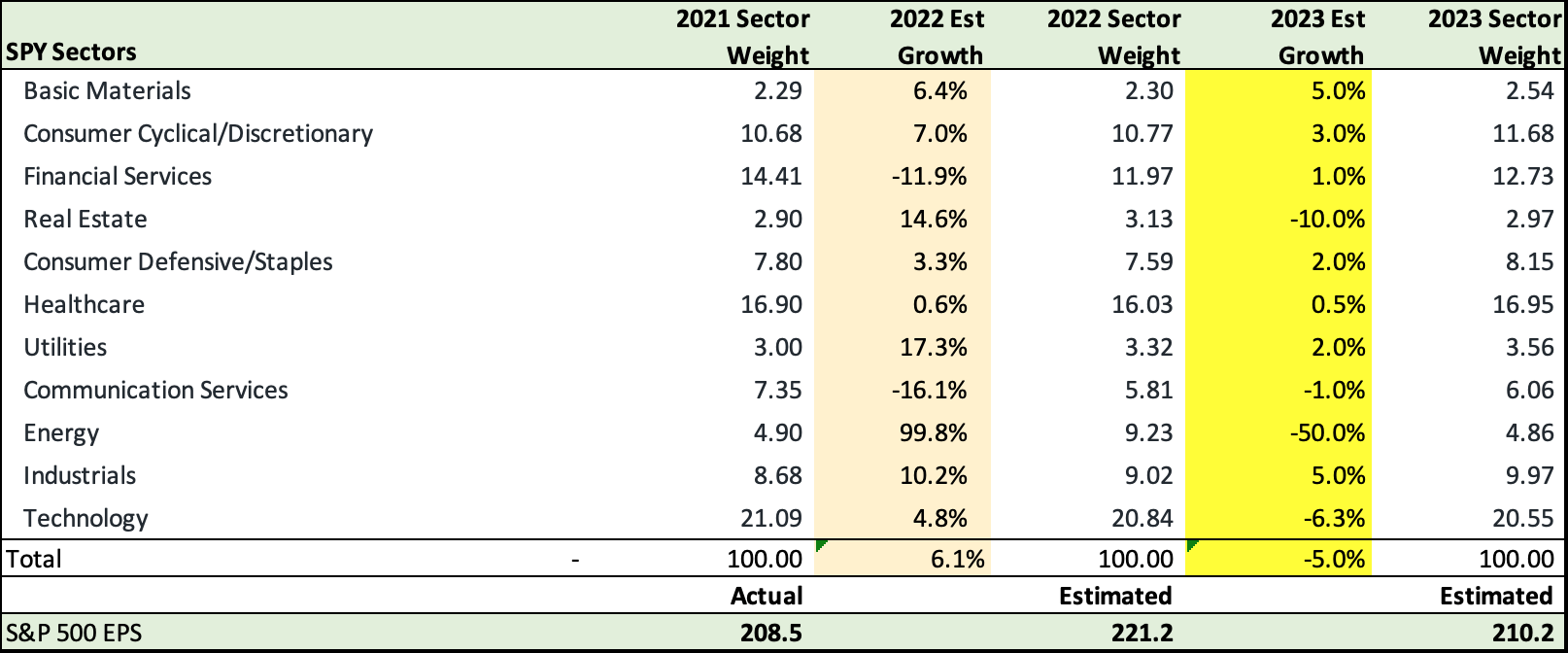

Here are my S&P 500 sector specific growth rates estimates that point to a 5% lower YoY 2023 earnings of $210 compared to 2022.

S&P 500 earnings By Sector ( FactSet, Bloomberg, The Heisenberg Report, Fountainhead )

{kind=link}

In my opinion, these are the sectors that should weigh strongest on the S&P 500 in 2023.

- High oil prices, which led to a massive 100% increase in Energy earnings will see a 50% reversal to earnings in 2023 and bring its sector weighting back to the more normal 5%.

- Real Estate, which saw gains of 15% in 2022 should fall with the housing bust and drop 10% in 2023.

- Consumer cyclicals should also lose much of its inflationary gains of 2022 with tepid growth of 3% in 2023.

- Technology, the highest weighting, which still eked out an estimated gain of 4.8% is likely to lose about 6.3% in 2023.

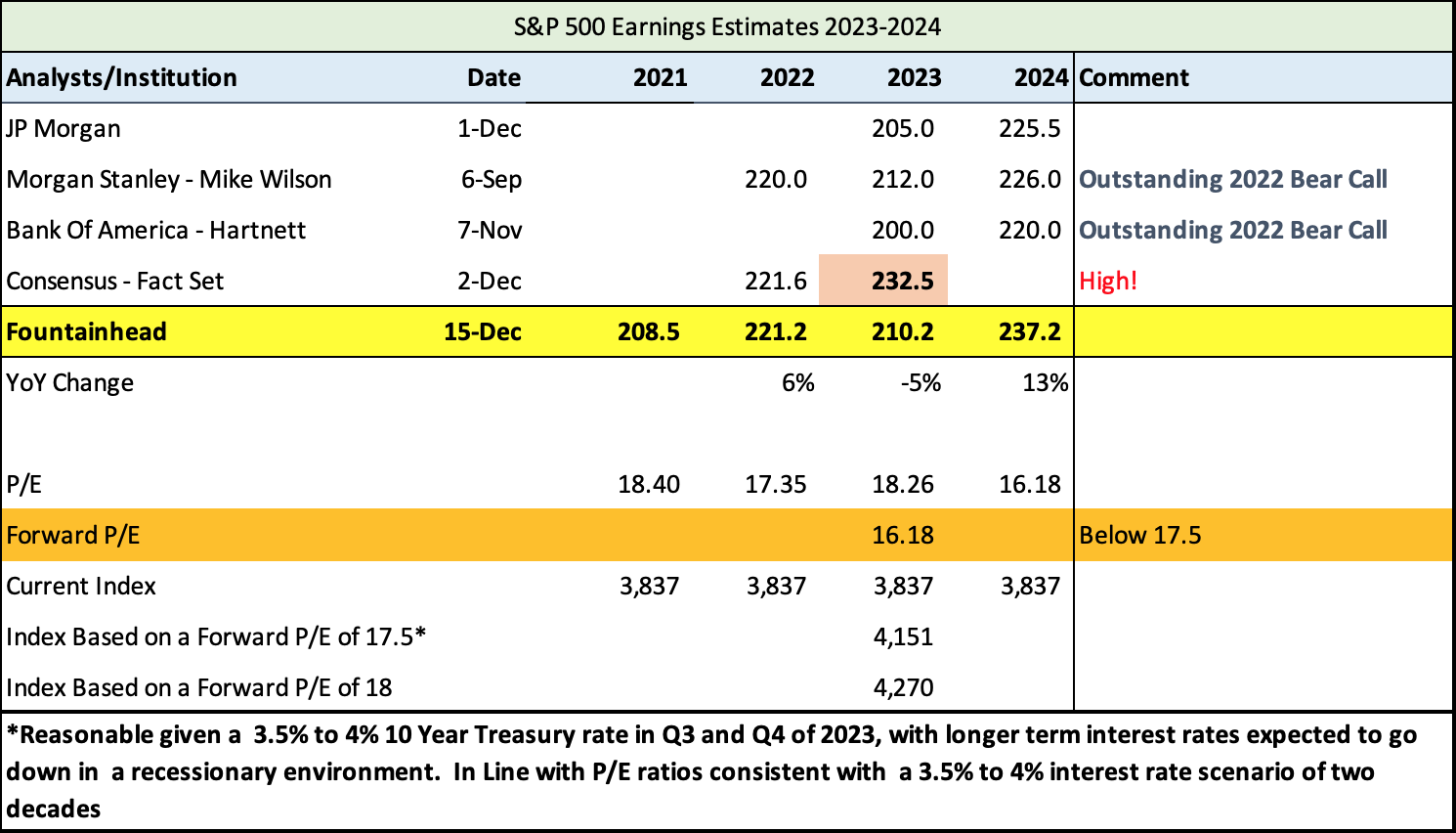

I Expect Growth to Resume in 2024

S&P 500 Earnings Estimate 2023 ( FactSet, The Heisenberg Report, Bloomberg, Seeking Alpha, Fountainhead )

{kind=link}

I stacked up my estimates against consensus and Morgan Stanley and Bank of America, whose analysts had outstanding bear calls for 2022. I'm not as bearish as Bank of America, which has an EPS estimate of just 200, but also looks for a return to growth of 10% in 2024. My own growth estimates for 2024 are higher at 13% for three reasons -

a) Technology and Communications, the two biggest sectors, will return to higher growth.

b) I don't anticipate the labor market to falter beyond an unemployment rate of 5.5 %

c) In my view, there will be "normal" inflation of 3% going forward, hence I do expect it to show in the nominal earnings numbers.

{kind=link}

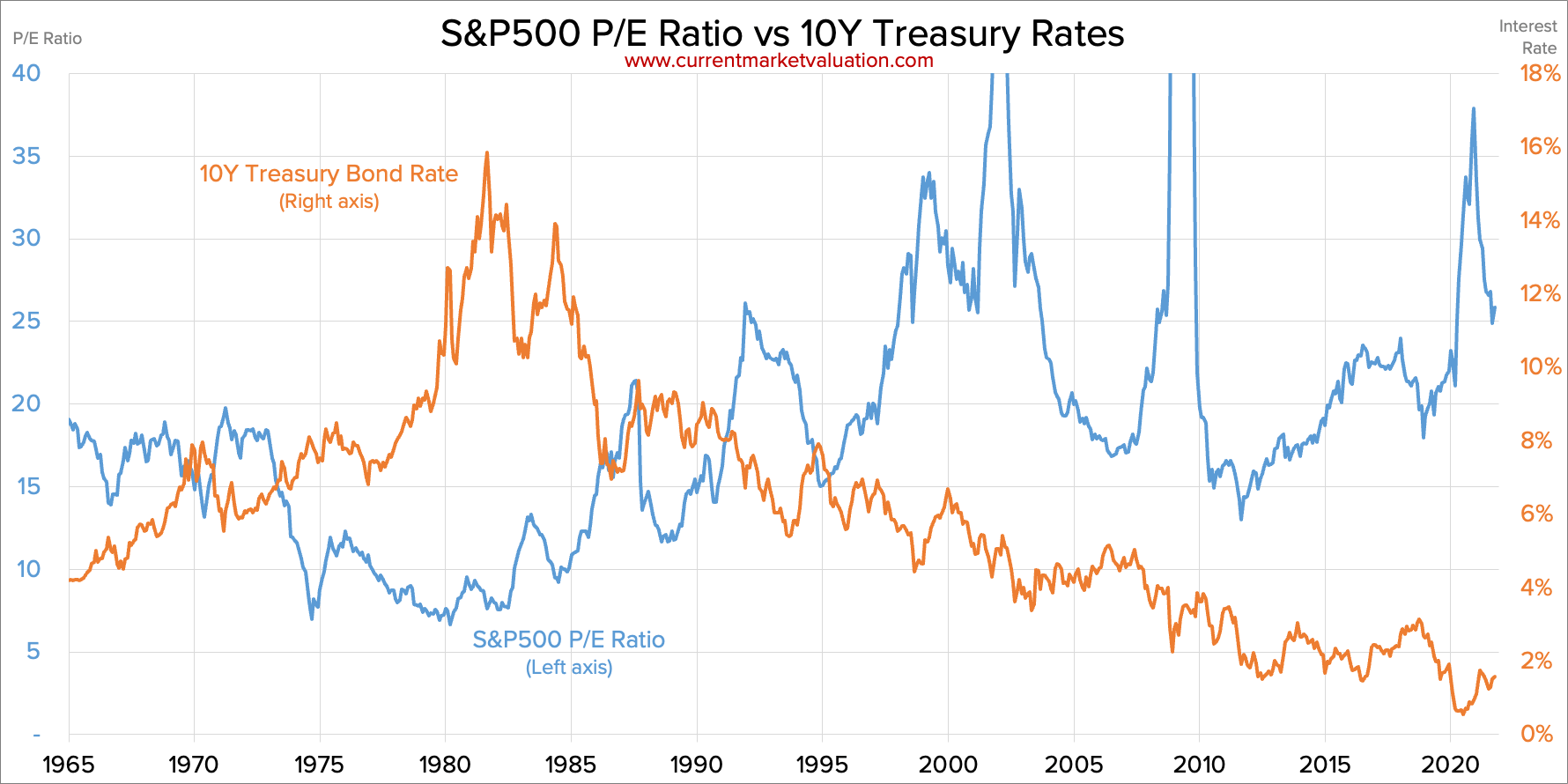

S&P 500 PE V Interest Rates (Current Market Valuation)

A Conservative Multiple and Growth Rate

Based on the historical chart above, in 1995, the 10-year treasury was above 6% and then fell to a low of 2% during the Great Financial Crisis, ranging between 3.5% to 4.5% for the most part in those 15 years. During this period, the S&P 500 P/E ranged between 15 and 25 for the most part except for those two years when earnings plummeted during the GFC. The "supposedly high" 10-year interest rate of 3.5%, which has given investors so much consternation was "normal" for 15 years and we still had P/E's of 15+ during that time. Therefore, I believe that a P/E of 17.5 around the end of 2023 with a trending decline in interest rates in 2024 is not a big ask at all - if anything I may be conservative.

Going forward, I'm not looking at P/E's beyond 18, which would make us guilty of a recency bias. In the greatest bond market in history, before inflation reared its ugly head, after the GFC, 10-year treasuries ranged between 2% and 4% and of course between 0.5% and 2% during COVID, which led to the S&P at 4,800 having a trailing P/E of 23 on a 2021 EPS of $209! If it looks like an asset bubble, if it walks like an asset bubble... That should be a clear warning!

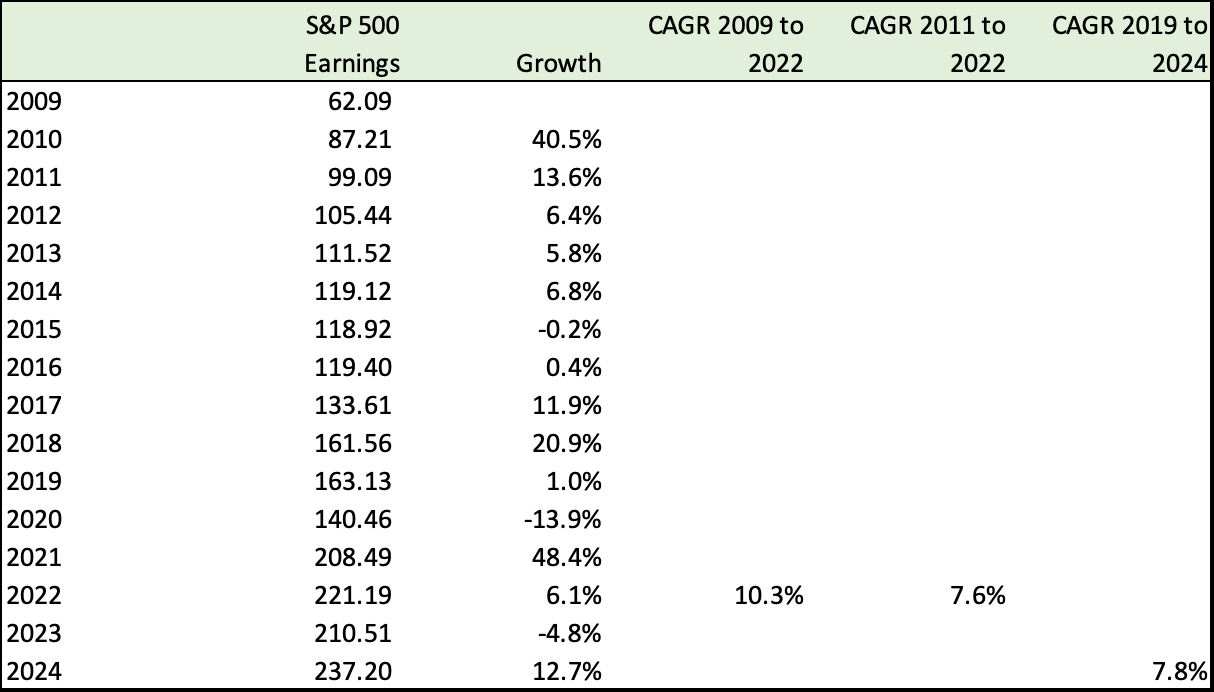

Also from an earnings standpoint, if you smoothen out COVID fluctuations, the 5 year 2019-2024 earnings CAGR is only 7.8%, which is consistent with the 2011-2022 growth of 7.6%. I'm not taking the higher 2009-2022 rate because post GFC the base of 62.09 was extremely low and it distorts the historical trend.

{kind=link}

S&P 500 Earnings (Fountainhead, Yahoo Finance, Yardeni)

I believe The Fed Pivot is not Pivotal

I actually believe that the Fed pivot is not pivotal, and instead of navel-gazing as to when Powell will blink in the face of recession, we should be looking at a new, "new normal" of 10 year treasuries ranging between 3.75% to 4.5% in the first half of 2023 and flattening to 3.5% to 4% in Q3 and Q4 2023 with a likely decrease in 2024. As we saw from the chart above, we have survived and thrived in 3.5 to 4% interest rates - if you're not looking for outlandish "Stimmy" valuations! Instead I would rather focus on finding a) Great investments and b) Scouting for bargains which will be available in spades in 2023 and c) Putting strict limits to take profits when either we've reached our price target or the market has given it an absurd valuation.

I expect the Fed's 2% Target Inflation Rate To be Ditched - Live With the New Normal

I believe the Fed will explicitly or implicitly ditch its 2% target inflation rate. With the PCE (the Fed's preferred inflation gauge) running at 6% Year on Year, it doesn't make sense to target 2% knowing that you'd have to set a nominal interest rate of 8% to reach that target. The PCE actually peaked at a 7% YoY increase in June 2022 and while confident of a decline, I don't believe it will go below 3-4% for the most part of 2023. Wage and shelter inflation are far stickier than commodity and supply chain inflation.

We tend to forget that the Fed hikes have a limited impact - their biggest impact and effectiveness is in pricking asset bubbles, ironically the same ones that they helped create! And to a large extent, in 2022 the markets have been punished for irrational exuberance, for buying the dip and paying excessive multiples without realizing that interest rates cannot stay at zero forever.

To that extent and if that is their mandate - they have been successful in spades. Every asset class has dropped in 2022.

Forget about the pivots and when the Feds will stop increasing rates; I think the focus should be to accept that inflation is not likely to reduce in a hurry - I don’t believe the Feds can actually reduce wage growth way the way they can puncture asset bubbles.

The Feds also have a hard time fighting inflation caused by supply chain disruptions and geopolitical tensions. For example, the Fed can do little to influence oil prices, which are again dictated by the monopolistic OPEC. Sure, higher interest rates make capital investment more expensive, thereby preventing over capacity, but simply not making capital available also has the opposite effect - you are reducing capital expenditure, which means existing manufacturers or material producers and miners can charge more without worrying about new capacity coming up soon again. I don’t believe higher interest rates are going to reduce material and commodity prices in a big way. It’s counterproductive.

To the Fed's credit - it is crucial to understand that the Fed is seen to be fighting inflation. Entrenched inflation expectations are worse because they predicate human behavior, which means instead of spending, we hoard since we expect prices to go up even further, which then creates a vicious inflationary spiral. Or we postpone, which reduces demand in the economy, not because prices have gone up recently, but we want to buy when things are cheaper. Besides, the Fed has to be that one institution, which should be seen as winning the fight on inflation - even if they attack in a "whack a mole" fashion. I believe the outcomes will be selective and the biggest influence will be on asset prices, and with more than a 30% drop in the NASDAQ Composite Index ( COMP.IND ) and 20% in the S&P 500 the Fed has already achieved that.

The Fed has also done a reasonable job in reducing the housing bubble. With mortgage rates ratcheting to over 7 percent, it has shaken out a fair amount of excessive speculation. The Fed's second goal was to reduce shelter inflation/renters inflation, which usually occurs with a time lag, and I believe this should happen in Q2 of 2023, simply because leases are annual affairs and will show up in the statistics with a lag even if this is already happening. Shelter inflation is the biggest part of our monthly budget and we should see some improvements in 2023, which will continue to reduce inflation.

The last frontier - High wages. As unfortunate as it sounds, the Fed has a mandate to reduce jobs to meet their inflation targets. Currently, they expect the unemployment rate to increase to about 5% from the existing 3.6%. However, I believe wage inflation will be stubborn because a) there has been a labor shortfall because of a marked decrease in immigration due to COVID and b) there has been a steady outflow of labor from the market due to early retirement and a reluctance to work in COVID like conditions. We still have 1.9 positions to 1 available person based on JOLTS reports (Job Openings to Labor Turnover). I suspect that the Fed will baulk at achieving this target - the specter of a recession and joblessness will outweigh the need to bring inflation to the targeted rate, there will be political pressure as we head to an election year in 2024 and lastly, Fed members are old enough to remember the jobless recovery of the Obama years - higher unemployment is not a desired outcome. It takes years to recover from that!

The Fed also needs to be careful to avoid overtightening impulses

It is so difficult to wean off our dependency on ZIRP (Zero Interest Rate Policy) and the Feds need to ensure that we in the US don't have the same fallout the UK did when pension funds suddenly had no buyers or liquidity before the Reserve Bank of England stepped in. To quote Marko Kolanovic, Chief Global Strategist of JP Morgan Chase on the same...

The financial system over the past ~15 years evolved around an environment of near-zero interest rates. This includes leverage, functioning of arbitrage channels and strategies that rely on leverage, new models of liquidity provision, liquidity risk of private assets, systematic investing, etc. Together, these can give rise to a self-reinforcing feedback loop of volatility-liquidity-positioning. This type of market interdependencies, which are a feature of financial markets built around a near-zero rate environment, can cause selloffs such as the one at the end of 2018 and on a number of other occasions. These financial risks can lead to contagion and are not captured by low-frequency economics (e.g., ‘Phillips curve,’ etc.). In an environment of deteriorating fundamentals, quantitative tightening and an abrupt increase of interest rates, these risks could emerge much sooner than, for example, an increase in unemployment or decrease in inflation.

I do believe that in the face of declining earnings and lower GDP growth rates, the Feds will not risk sudden tightening impulses, especially now that they have committed to smaller rates for longer periods, which has resulted in the markets pricing a terminal rate of 5.1% instead of 4.8% from September.

Trading and Investment Strategy for 2023

I expect the S&P 500 to test its June 16th low of 3,667 and the October 10th close of 3,577, by the 1st quarter of 2023. Technically, since its high of 4,797 on Jan 3rd, 2022, the S&P 500 has been making lower tops and lower bottoms in a bear market and while the rallies have been fast and furious, they're also typical of bear market rallies.

{kind=link}

S&P 500 Index ( Barchart )

I believe that we are headed for a short and shallow recession in 2023, based on at least these indicators:

- The Yield (2 Year v 10 Year) curve is inverted at its deepest since 1981. In my opinion, Inverted yield curves are good predictors of recessions, (not infallible but right more than 65% of the time)

- Oil is down more than 40% from its peak.

- China reopening is still doubtful and sluggish for 2023.

- US Pending home sales fell 37% YoY in October.

- ISM manufacturing new orders are down for 3 consecutive months.

I have about 25% of my portfolio in cash and plan to add 10-15% more in 2023.

S&P 500 - I'll start nibbling around 3,650. I'm not a good market timer and even though I believe 3,577 is a good support level, I believe the downside risks don't extend beyond 10% and hope to deploy 90% of cash between 3,450 and 3,650, keeping 10% for special situations. I strongly believe that the S&P 500 pre Covid peak of 3,380 should hold as a key support for the index.

Tech Stocks - I believe the focus in 2023-2024 should return to high quality tech, especially stocks that lost 50 to 70% from their peak.

NVIDIA ( NVDA ) - great long term investment, most innovative chip company, abundant growth opportunities. I've owned it for a long time and recommended it in October. I got a good price around $118-$120, but am keeping a lookout to add more if it breaks $150. The stock tends to get expensive fast because it is volatile - it was over $180 just a few days ago, so keep limits.

ASML Holding ( ASML ) - A veritable monopoly in Ultra Violet lithographic machines, this is another buy on declines, and should do very well in the next 5-7 years.

Teradyne ( TER ) - Another favorite in the semi's space, part of a duopoly fo r Automated Test Equipment - this is still reasonably priced and I continue to add more.

Apple ( AAPL ) - Besieged by production issues out of China, which will resolve over time, this is also worth buying on declines.

I will also add Netflix ( NFLX ) on declines - I believe the advertising model has legs. Adobe Inc. ( ADBE ) is a very well-managed company, also attractive even though its growth rate has slowed some.

I'm not a big fan of cyclicals and in a recession they will get hit, but ABB Ltd ( ABB ), is well managed and holds up well in bad times - researching it in more detail.

Conclusion - I expect the S&P 500 to close at 4,151 at the end of 2023

2023 is going to be very difficult to make money in - I guess that's a major understatement!

I have a two-year outlook - I'm not trying to time the market by shorting the S&P 500 to 3,500. Instead, I would prefer to be patient, setting lower limits. Assuming 2024 earnings of $237 and 2025 earnings of $256 (8% growth - around the long-term average) I expect an index of 4,607 - hoping to have some real animal spirits back in the market in 2024, instead of the "will he, won't he" day traders parsing Fedspeak. This returns about 1,100 on a base of 3,500 or 14.7% per year. That's a great return for the index. Returns on individual stocks, especially tech would be higher (of course, higher risk as well).

In my viewpoint, we're extremely likely to see earnings decline in 2023 and a recession - I've actually listed a very short list of recession indicators and will expand more just on the recession in another article. Wading through weak guidance, falling home prices, higher unemployment should be gut wrenching and will require a lot of patience. However, this is not the Great Financial Crisis, nor the Volcker 70's inflation and thankfully a huge chunk of the irrational exuberance has already been taken out of the indices with the S&P 500 down 21% from its high and the NASDAQ Composite down more than 30% from its all-time high. Most of the damage is done and the downside is limited, and while inflation will persist above the Fed's target, the focus will shift to staving off a recession.

I believe a P/E of 17.5 to 18 is reasonable given historical trends and expect the S&P 500 to close around 4,151 based on a 2024 EPS of $237 at the end of 2023 and 4,607 based on a 2025 EPS of $256 at the end of 2024.

Happy investing and happy holidays to all.

Editor's Note: This article was submitted as part of Seeking Alpha’s 2023 Market Prediction contest. Do you have a conviction view for the S&P 500 next year? If so, click here to find out more and submit your article today!

For further details see:

Poor Earnings, Shallow Recession To Drag S&P 500 Initially, But I Expect Strong Recovery To 4,151 By Year-End 2023