BPOP - Popular Inc. Q2 Earnings: Growth Dividends And Undervaluation

2023-07-27 11:42:43 ET

Summary

- Popular Inc. reported strong Q2 earnings, beating expectations in terms of GAAP EPS and revenue.

- The company saw a modest dip in net income and increased operating costs, but its performance, price appreciation, and dividend growth make it an attractive investment opportunity.

- Popular Inc. is forecasting an upturn in non-interest income and plans to increase dividends later in the year.

Thesis

Popular, Inc.'s (BPOP) recent Q2 earnings release revealed GAAP EPS of $2.10, beating by $0.28, and revenue of $692.14M, beating by $16.46M. This showcases consistent growth in various aspects, including net interest income and loan balances. In this analysis, I argue that despite a modest dip in net income and increased operating costs, the company's performance, medium-term price appreciation, and dividend growth make it an attractive investment opportunity.

Company Profile

Popular, Inc. and its subsidiaries provide a comprehensive array of banking products and services in Puerto Rico, the United States and British Virgin Islands. Their offerings include deposit accounts, loans for both individuals and businesses, investment banking services, insurance services and online banking - they were founded in 1893, with their headquarters located in Hato Rey in Puerto Rico.

Popular, Inc.'s Q2 2023 Earnings Highlights

In Popular Inc.'s latest financial report, the company disclosed a modest dip in Q2 net income, coming in at $151 million compared to the preceding quarter's $159 million. Net interest income maintained its footing at $532 million, matching the previous quarter's figure. Non-interest income, although experiencing a nominal decline to $160 million, a mere $2 million less than in Q1, demonstrated a $5 million ascendance when the influence of an insurance claim reimbursement from Q1 is removed. This uptick is driven by an enhancement in service charges and other service fees, courtesy of amplified customer engagement.

The company reported a reduction in provisions for credit losses, from $48 million in Q1 down to $37 million. In parallel, operating costs ascended to $640 million in Q2, a $20 million increase attributed largely to professional service charges in areas such as regulatory compliance, cybersecurity, and escalated technology and software costs.

Public sector deposits swelled by $3 billion in comparison to Q1, hitting a total of $18.5 billion by the close of Q2. According to management, even though the volatility of these deposits could potentially influence profitability, the company's liquidity remains unaffected due to Puerto Rican law necessitating that they are fully collateralized. Concurrently, loan balances demonstrated an encouraging trend, showing a $693 million increase compared to Q1, signaling a strong demand for credit.

Projected outlooks show Popular Inc. forecasting an upturn in non-interest income for upcoming quarters, predicting a range of $155 to $160 million, topping their earlier estimate of $150 million. This anticipated increase is traced back to two game-changing strategies, including a pricing upgrade in their commercial cash management in Puerto Rico, and the launch of a commercial credit card aimed at local SMEs, both of which have catalyzed a spike in additional fee income.

And as we shift our gaze to the rest of 2023, Popular Inc. has disclosed that they will refrain from share repurchases due to instabilities in interest rates, economic conditions, and the potential for regulatory revisions. Despite this, a dividend increase is on the cards for later in the year. The company's perspective on capital return in the long term stays consistent, with an expectation that their regulatory capital ratio will gradually align with their industry counterparts. For the current year, the effective tax rate is projected to lie between 22% and 25%, a marginally tighter range than the earlier projected 21% to 26%.

Performance

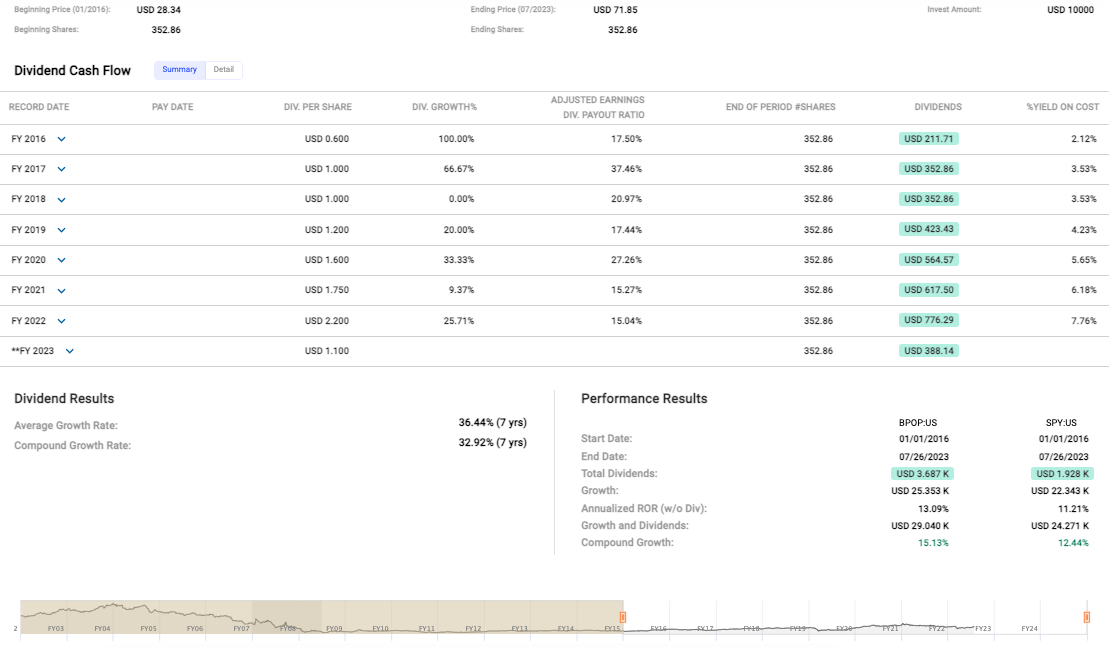

The company's price appreciation in the medium-term (from January 2016 to July 2023) has been stellar, showing a significant increase from $28.34 to $71.85, and in terms of pure growth, it has outperformed the S&P 500 Index with a compound growth rate of 15.13% compared to 12.44% for the index.

{kind=link}

The dividend data is equally impressive with an average growth rate of 36.44% in dividends, indicating the company's strong commitment towards returning capital to shareholders.

Valuation

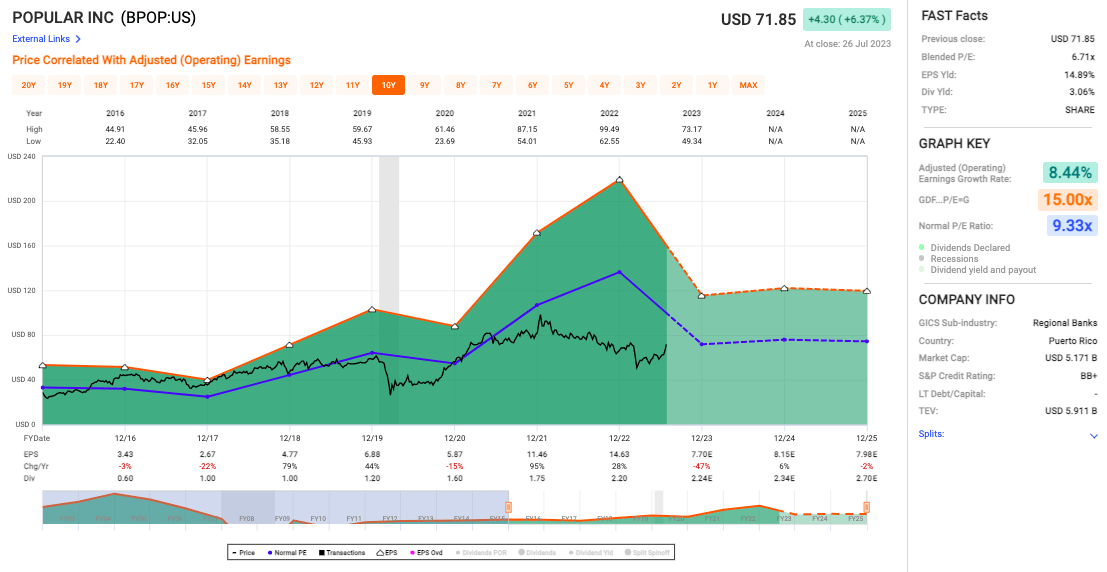

BPOP's P/E ratio is significantly lower than the normal P/E ratio of 9.33x, suggesting that the stock is undervalued, which is further backed up by a compelling EPS yield of 14.89%.

{kind=link}

And at 8.44%, Popular's adjusted earnings growth rate isn't exactly staggering, but it still represents an impressive and sustainable expansion trend coupled with a fairly healthy dividend yield at 3.06%

Risks & Headwinds

As noted in the highlights, the reported net income has fallen from $159 million in Q1 to $151 million in Q2, a noticeable reduction which could potentially raise a few eyebrows among some investors. This downturn, albeit moderate, could point to potential challenges in preserving a consistent profitability trajectory and, if they persist, can affect investor sentiment.

Looking at operating expenses, the company has registered an uptick of $20 million from Q1 to Q2. Coupling this with a separate cost of $7 million related to transformation-related outlays, it brings to light possible issues in the company's cost-management approach.

The company's deposit mix also shows signs of a potentially challenging environment ahead. A considerable drop of $624 million in non-interest-bearing deposits was observed this quarter. This shortfall, despite being offset to some degree by increases in time and saving deposits, raises issues.

Lastly, the company has signaled uncertainty regarding its share repurchase activities for the remaining part of 2023, citing ongoing uncertainties as the primary reason. For some investors, this could be a significant factor, especially those banking on share buybacks to boost their returns.

Final Takeaway

I would rate Popular Inc. stock as a "Buy." The company has demonstrated consistent growth in customer engagement, robust demand for credit, and a successful enhancement in service charges and other fees. Despite a moderate dip in net income and increased operating costs, the firm's impressive medium-term price appreciation, compelling valuation, and strong dividend growth signal a sound investment. Potential Popular, Inc. headwinds such as reduced net income and share repurchase uncertainty are noteworthy, but they seem manageable given the firm's overall positive trajectory and growth strategies.

For further details see:

Popular Inc. Q2 Earnings: Growth, Dividends, And Undervaluation