PRCH - Porch Group Focuses On Profitability As Housing Market Activity Slows

2023-11-29 10:56:25 ET

Summary

- Porch Group, Inc. beat consensus earnings estimates in Q3 2023 and is focused on improving profitability rather than volume growth.

- The global home insurance market is expected to reach $395 billion by 2027, driving growth opportunities for Porch Group.

- The company's recent financial trends show growth in total revenue and progress towards breakeven earnings per share in Q3 2023.

- Given a slowing housing transaction market, I'm Neutral [Hold] on Porch Group, Inc. shares for the near term.

A Quick Take On Porch Group

Porch Group ( PRCH ) reported its Q3 2023 financial results on November 7, 2023, beating consensus earnings estimates.

The firm provides software solutions to the home service market and insurance coverage to homeowners in the United States.

Management is focused on improving profitability rather than volume growth, so the question is whether housing market troubles can be offset by improved profitability.

For the near term, I’m Neutral [Hold] on Porch Group, Inc. stock until we gain further visibility into its progress.

Porch Group Overview And Market

Seattle, Washington-based Porch Group was founded in 2011 and provides home service providers with software solutions to help them connect with and manage customer processes.

PRCH also provides a range of insurance coverage services to homeowners in the United States.

The firm is headed by founder, Chairman and CEO Matt Ehrlichman, who was previously Chief Strategy Officer at The Active Network and co-founder of Thriva.

The company’s primary offerings include the following:

-

Vertical software - various types

-

Homeowners insurance products.

According to a 2021 market research report by Allied Market Research, the global home insurance market was an estimated $225 billion in 2019 and is forecast to reach $395 billion by 2027.

This represents a forecast CAGR of 7.3% from 2020 to 2027.

The main drivers for this expected growth are an expected increase in the number of households, growing government initiatives and an increasing frequency in disasters.

Also, new technological innovations are expected to provide avenues for further growth in the industry.

Major competitive or other industry participants include:

-

Allstate

-

American International Group

-

AXA

-

Chubb

-

Liberty Mutual Insurance

-

State Farm

-

Progressive

-

Geico

-

Others.

Porch Group’s Recent Financial Trends

Total revenue by quarter (blue columns) has grown sharply in the most recent quarter; Operating income by quarter (red line) has almost achieved breakeven in Q3 2023:

Seeking Alpha

Gross profit margin by quarter (green line) has been volatile in recent quarters; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have trended lower more recently:

Seeking Alpha

Earnings per share (Diluted) have remained negative but making progress toward breakeven in Q3 2023:

Seeking Alpha

(All data in the above charts is GAAP.)

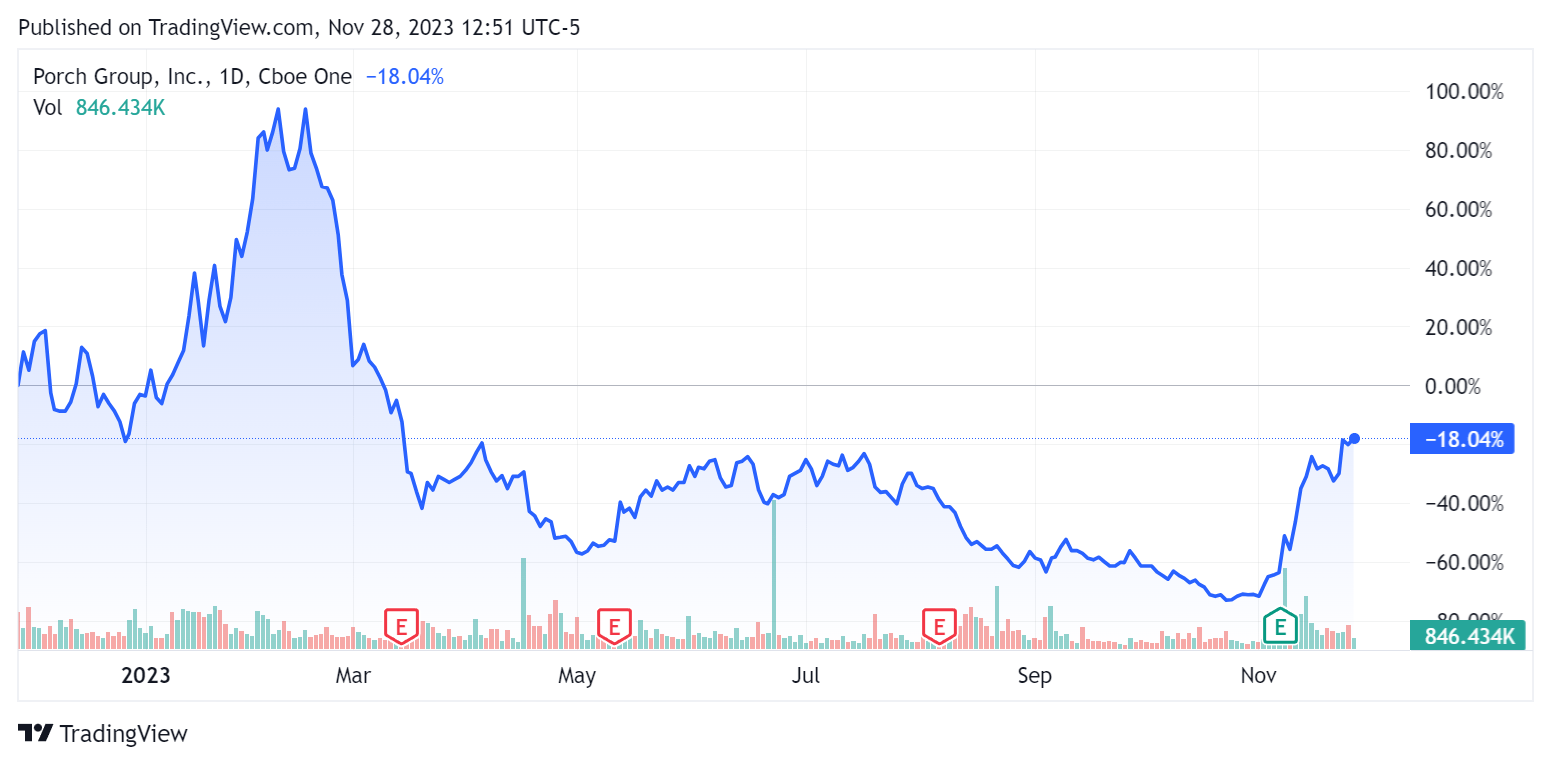

In the past 12 months, PRCH’s stock price has fallen a net of 18.04%:

{kind=link}

For balance sheet results, the firm ended the quarter with $371.7 million in cash, equivalents and short-term investments and $432.8 million in total debt, of which $1.6 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $66.4 million, during which capital expenditures were $1.1 million. The company paid $26.7 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Porch Group

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 0.6 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 0.4 |

| Revenue Growth Rate |

| 44.2% |

| Net Income Margin |

| -44.0% |

| EBITDA % |

| -38.0% |

| Market Capitalization |

| $156,220,000 |

| Enterprise Value |

| $219,260,000 |

| Operating Cash Flow |

| $67,510,000 |

| Earnings Per Share (Fully Diluted) |

| -$1.77 |

| Forward EPS Estimate |

| -$0.89 |

| Free Cash Flow Per Share |

| $0.59 |

| R&D / Revenue |

| 15.2% |

| SA Quant Score |

| Hold - 3.41 |

(Source - Seeking Alpha.)

Commentary On Porch Group

In its last earnings call (Source - Seeking Alpha ), covering Q3 2023’s results, management’s prepared remarks highlighted the ability for the firm to pass through pricing increases for its insurance premiums and software offerings.

Additionally, the firm’s insurance segment has been able to increase its risk exclusions and raise deductibles.

However, the company has suffered from various loss events due to weather and from an alleged global fraud by one of its reinsurance partners, Vesttoo.

In the aftermath, the firm’s insurance carrier was placed under supervision by the TDI, although that supervision has since been removed.

In the process, the company has begun to connect some homeowners with third-party insurance agencies and has seen "higher conversion rates overall with a lower cost structure. These partnerships are progressing nicely and performing well."

Management expects further homeowners insurance premium increases in 2024 and is focused more on underwriting profitability than increasing volume, so revenue growth from this segment may be less than in previous periods.

In the earnings call, I tracked the frequency of various keywords and terms used by management and analysts:

Seeking Alpha

The firm continues to face challenges due to a higher interest rate environment, which negatively impacts the U.S. housing business, reducing sales volumes.

Analysts asked leadership about its proprietary data advantages, operating leverage and vertical software outlook.

Management said it is actively rolling out its unique data capture and analysis capabilities to additional states beyond the 12 it currently is utilizing its data in.

On operating leverage going forward, the company is intent on producing good returns based on expense control and disciplined underwriting decisions, both for new business and on renewals of existing clients.

For its vertical software segment, management believes it has been resilient despite a negative housing environment and lower housing transactions.

Total revenue for Q3 2023 rose 67.4% year-over-year, while gross profit margin increased by 1.7%.

Premium retention was 100%, with premium increases offsetting non-renewals. Management did not disclose retention figures for the software segment.

Selling and G&A expenses as a percentage of revenue fell by 17.5% YoY while operating income nearly achieved breakeven on an improved focus on profitability.

The company's financial position is strong, with ample cash against its long-term debt and strong free cash flow.

Looking ahead, management’s plan to increase the use of its data approach to quantifying risk and correctly pricing for that risk appears to be already bearing fruit.

The company recently decided to exit the state of Georgia as that state did not approve of the firm’s rate increase submission.

So, PRCH will likely see a reduction in revenue growth but an improvement in profitability outlook.

The question for investors is whether the U.S. housing market transaction volumes will continue to decline more than the firm’s ability to improve its profitability in the quarters ahead.

For now, I’m Neutral [Hold] on Porch Group, Inc. shares due to the uncertainty around that question.

For further details see:

Porch Group Focuses On Profitability As Housing Market Activity Slows