VWAPY - Porsche Holding: What To Look For In Volkswagen And Porsche Earnings

2023-03-06 06:14:29 ET

Summary

- The net asset value discount between Porsche Holding and its holdings in Volkswagen Group and Porsche AG is 17.2bn euros, almost the same as the market cap of Porsche Holding.

- More important is that the actual cash flows from Volkswagen and Porsche are increasing.

- Volkswagen has announced strong results for the past year and optimistic guidance for 2023. We should see the same from Porsche AG.

- Volkswagen will pay a record annual dividend for 2022, resulting in a 1.37bn pay-out to Porsche Holding.

- Gradual paydown of debt through dividends received will result in an increased NAV discount and higher future cash flows.

(Note: all amounts in the article are in EUR. At the current exchange rate, this is almost equivalent to USD.)

Investment Thesis

Porsche Automobil Holding SE (Porsche Holding) (POAHF) (POAHY) is a holding company that owns Volkswagen AG shares ( OTCPK:VWAGY , OTCPK:VWAPY , OTCPK:VLKAF , OTCPK:VLKPF ), and after the IPO last year also Dr Ing hc F Porsche AG shares (Porsche AG) (DRPRY) (DRPRF) directly. Porsche AG is the company that makes the iconic sports cars.

The hard truth about Porsche Automobil Holding SE is that the holding company exists to give the Porsche/Piëch founder families control of Volkswagen Group and Porsche AG, while owning only a minority of the total capital. (I have covered the complicated ownership and governance structure of the Volkswagen and Porsche group of companies in another Seeking Alpha article . If you want to understand the details (maybe more than you want to know), I want to refer you to this article.)

The complicated ownership and governance structure warrants a discount in a sum-of-the-parts valuation, but the current net asset value discount of 17.2bn seems excessive, as it almost equals the market capitalization of Porsche Holding.

Equally or maybe even more important than a sum-of-the-parts valuation is that the actual cash flows from Volkswagen and Porsche are increasing. While the NAV discount is excessive, there is no short-term trigger to change this.

Volkswagen announced a higher than expected record annual dividend of 8.7 euro last week. This means the pay-out to Porsche Holding in 2023 will be 1.37bn. Volkswagen gave a quite optimistic guidance for 2023, meaning the higher cash flow should continue. Both Volkswagen and Porsche Holding shares increased by 10 and 6 percent on the day of the announcement, but I think there is more positive runway.

Porsche Holding financed the Porsche AG acquisition through a special dividend from Volkswagen and debt. My assessment is that after 2023 Porsche AG dividends should be enough to cover the expense that comes with the debt. Over the next years, I expect a steady increase in cash flow from Porsche AG to be available for Porsche Holding investors.

Current NAV discount

Porsche Holding net asset value is significantly below the market value of its stakes in Volkswagen and Porsche AG. The company has other much smaller holdings, but they are immaterial.

Porsche Holding controls Volkswagen as it owns the majority (53.33%) of Volkswagen AG ordinary shares, but only 33.1% of the total capital. At the current share price, this comes to a total asset value of 28.56bn.

Porsche Holding also owns 12.5% of Porsche AG directly (Volkswagen still owns 3/4). The asset value here is 14.07bn at current market prices. There is still 7.9bn of debt left that Porsche Holding took on to finance the purchase of its stake in Porsche AG.

So the total net asset value of the two holdings is 34.73bn, versus a market cap of 17.52bn. (Note - I am assuming here that the ordinary shares, which are not publicly traded, have the same price as the preferred shares.)

The low P/E ratio is only a different way of looking at the NAV discount

Porsche Holding was featured on a recent Seeking Alpha list of 10 large-cap stocks with the lowest P/E.

I do not think that this adds more decision points for investors. Porsche Holdings earnings are a proxy for the difference in share price of its holdings at the beginning and the end of the reporting period, while the cash flow is determined by the dividends received in the reporting period. In 2021 Porsche Holding reporting EPS of 14.9 euro and paid a dividend of only 2.56 euro (for the publicly listed preferred shares). The reason: Volkswagen ordinary shares were up more than 50% YoY.

Volkswagen reported strong 2022 results and 2023 guidance

Volkswagen announced preliminary 2022 numbers on March 3, and they were quite strong. One exception were deliveries, which were only 8.3mn and at a 10-year low.

What got investors really excited and made the shares go up 10% on the day of the announcement was the guidance for 2023.

Volkswagen expects a revenue increase of 15% and 9.5mn deliveries, up from 8.3mn in 2022. Volkswagen also expects a profit margin of between 7.5 and 8.5%. At the low point, this is 50pp more than in 2022.

While revenues in 2022 were strong based on an improved product and pricing mix, deliveries were the lowest in 10 years. So, it is good to see those go up again. The forecast is driven by a strong order backlog and the assumption that semiconductor supply chain and logistics issues will further ease over the year.

A look at the Volkswagen dividend

As the companies follow the usual European practice to pay annual dividends, cash flows from Volkswagen Group reach Porsche Holding shareholders with a delay - dividends for the fiscal 2022 will be paid out to Porsche Holding in 2023, and then flow to Porsche Holding shareholders in 2024 as the dividend for 2023. On the bright side, if dividends go up as they currently do, you know that the best is yet to come.

The dividend pay-out from Volkswagen has increased significantly over the last 5 years. Also, Porsche Holding increased its stake slightly from 52.2 to 53.3% from 2016 onwards, which had a positive effect on the pay-out.

With a pay-out ratio of 29.4% for 2022 the Volkswagen dividend also seems fairly safe.

In general, the Porsche Holding has paid out about what it received from Volkswagen in the previous year, within plus/minus 10-20 percent range. Besides its own cost (according to its Q3 report, the company has only 36 employees), there are usually payments from or to other holdings, but also tax payments that make up the difference.

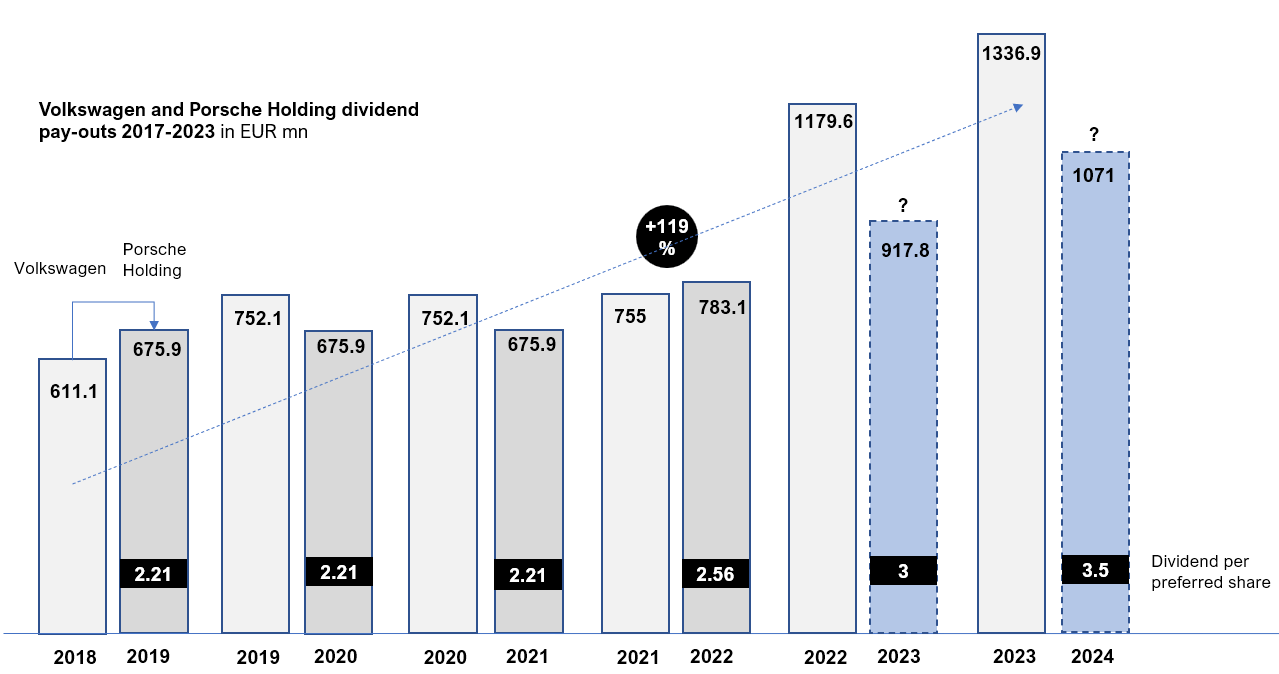

The following chart compares the regular dividend pay-out from Volkswagen ordinary shares ((VLKAF)) to the dividend pay-out by Porsche Holding. This on purpose omits the special dividend around the Porsche AG IPO last year.

Volkswagen and Porsche Holding dividend pay-out 2018-2023 (Source: Author calculations based on published company results)

{kind=link}

I assumed a Porsche Holding dividend per share of 3 euro for 2022 and 3.5 for 2023. The dividend yield would be 5.24% and 6.12%.

Whether Porsche Holding actually plans to use part of the dividend from Volkswagen to pay down debt from the Porsche AG purchase, remains to be seen. It is a key question I hope to get an answer for during the results announcement and earnings call. This is scheduled for March 23.

What dividend can Porsche Holding expect from Porsche AG?

Fortunately, calculating the expected dividend from Porsche AG is not so complicated. Porsche AG has been quite transparent here.

Porsche Holding acquired 25% + 1 share of Porsche AG ordinary shares, which gives it a 12.5% stake in Porsche AG. (It also owns 24.9% indirectly through Volkswagen, which we do not need to consider.) Ordinary shares get 1 cent less dividend than preferred shares, but this is immaterial at a share price of more than 100 euro. For simplicity, we can assume that whatever Porsche AG pays out, Porsche Holding will get 12.5% of it.

For fiscal year 2022, Porsche AG intends to pay a dividend of 911mn from capital reserves (see the FAQ section on the share-related part of the IR-website). All actual 2022 earnings will go to Porsche Holding Stuttgart GmbH, so still to Volkswagen:

For the Fiscal Year 22 Porsche AG intends to pay a first dividend (the "Dividend 2022") which would be payable in 2023 in an amount of EUR 911 million (plus the extra dividend of EUR 0.01 per Preferred Share), irrespective of the transfer of Porsche AG's earnings after taxes for the year to Porsche Holding Stuttgart GmbH under the profit and loss transfer agreement (Gewinnabführungsvertrag) between Porsche AG and Porsche Holding Stuttgart GmbH… As Porsche Holding Stuttgart GmbH is entitled to Porsche AG's entire earnings after taxes for 2022, the Dividend 2022 towards all existing shareholders will be paid by dissolving free capital reserves of Porsche AG.

Therefore, Porsche Holding should get 113.8mn this year from Porsche AG.

Going forward, Porsche AG is targeting a 50% pay-out ratio (see the same FAQs). Assuming a profit of 6bn in 2023 (probably around a 10% increase over 2022), Porsche Holding would receive 375bn. I expect this to be enough to pay the interest expense on the debt without touching the dividend from Volkswagen. Again, I hope to verify this from the 2022 results presentation and earnings call.

Which shares to buy?

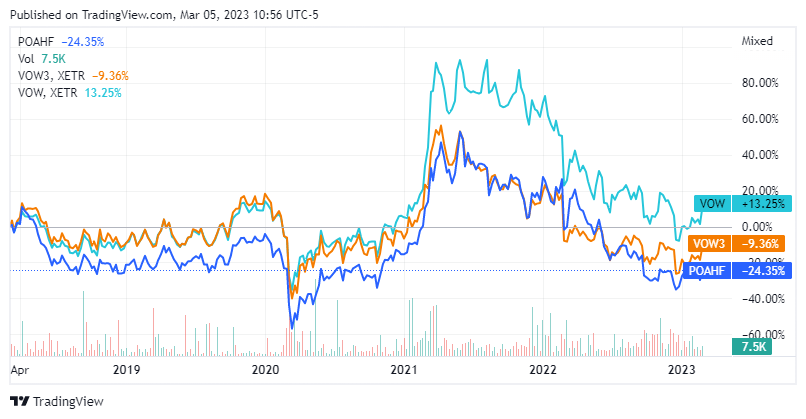

Before the Porsche AG IPO, the choice was between either Volkswagen ordinary shares ((VLKAF)), Volkswagen preferred shares ((VLKPF)), or Porsche Holding ((POAHF)). All three have corresponding ADRs (VWAPY, VWAGY, POAHY).

Over the last five years, the Volkswagen ordinary shares have outperformed the other two. As the preferred shares have now a significantly higher yield over the ordinary shares, they would be my preference.

Volkswagen ordinary shares vs. preferred shares and Porsche Holding (Source: Seeking Alpha)

{kind=link}

Since the IPO, though, my recommendation is to look at Porsche Holding as an alternative to buying Porsche AG.

If Porsche Holding shares do not appreciate relative to Porsche AG shares, a gradual pay-down of debt will result in Porsche Holding being valued about the same or less than the stake in the car manufacturer. This makes Porsche Holding a great alternative buy for those investors who believe that Porsche AG shares will do well. At the same time, investors can enjoy a dividend yield around 6% and get a third of Volkswagen for free.

Conclusion

Porsche Holding is a good long-term alternative to buying either Volkswagen or Porsche AG shares. Accordingly, the majority of the risks with Porsche Holding relate to the economic performance of those two holdings.

A final note for U.S. investors: U.S.-based investors should not buy the Porsche Holding shares directly as they are not listed in the U.S., but the ADRs ((POAHY)). As Porsche AG preferred shares do not have voting rights anyway, there is not a meaningful difference for U.S. investors.

For further details see:

Porsche Holding: What To Look For In Volkswagen And Porsche Earnings