VNQ - Portfolio Reveal: 5 REITs To Potentially Earn $1000 Every Month

2023-11-23 08:05:00 ET

Summary

- REIT dividend yields are historically high.

- Share prices have crashed even as interest rates keep on rising.

- I present a REIT portfolio to earn $1,000 of monthly dividend income.

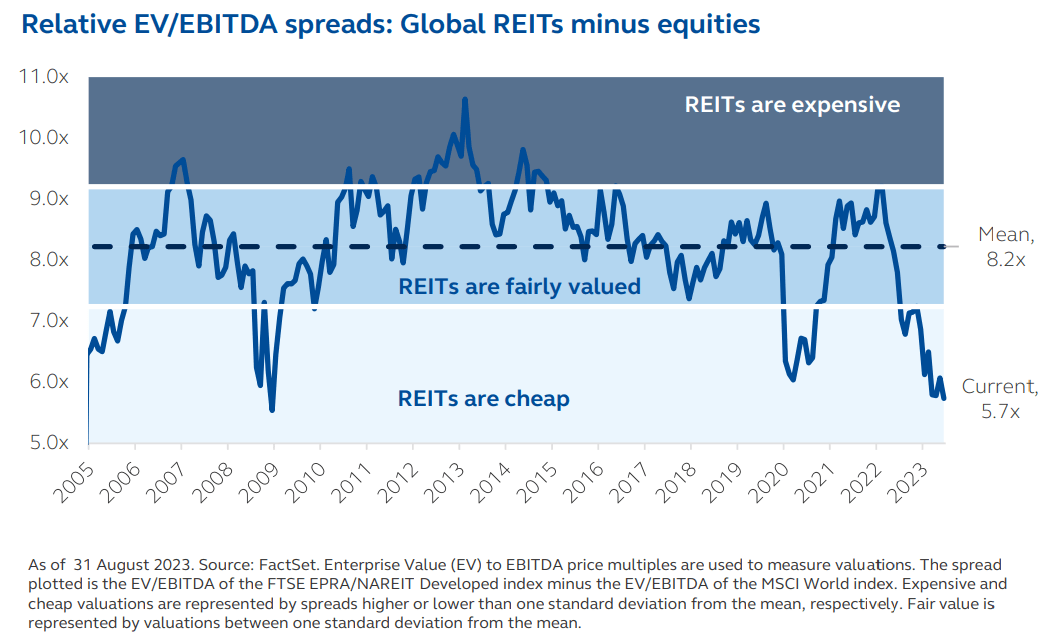

Over the past 2 years, REIT ( VNQ ) share prices have crashed even as their dividend payments kept on rising:

As a result, REITs are today priced at their highest dividend yields in many years, and earning $1,000 of monthly dividend income by investing in REITs is more attainable than you may think.

While it may have required a very substantial amount of capital just a couple of years ago... today, all it takes is about ~$140,000 if you invest in the right REITs.

Let's take a look at an example.

Below, you will find a well-diversified REIT portfolio that's able to generate a sustainable and growing $1,000 of monthly dividend income from a meager $139,534 investment:

| Ticker |

| Type |

| Dividend Yield |

| Crown Castle ( CCI ) |

| Cell Tower |

| 6.1% |

| EPR Properties ( EPR ) |

| Net Lease |

| 7.5% |

| Gladstone Commercial Series O Pref ( GOODO ) |

| Industrial |

| 8.6% |

| KKR Real Estate Finance Series A Pref ( KREF.PR.A ) |

| Mortgage |

| 9.2% |

| NewLake Capital Partners ( NLCP ) |

| Cannabis |

| 11.6% |

We used an equal weighting to keep it simple but you could have easily earned even more income by allocating more heavily towards the higher-yielding picks.

The portfolio offers an 8.6% average dividend yield with an equal weighting, resulting in $1,000 per month with just $139,534.

You will also note that we are achieving this with REITs that are in a good position to keep paying and even growing their dividend income over time.

Crown Castle ( CCI ) is the safest of the group, in our opinion. It is a mega-cap, investment-grade rated REIT that earns highly defensive cash flow from infrastructure-like assets. It has a strong track record of growing its dividend by 9% per year, and the management has guided it to start growing its dividend by 7-8% annually in 2026. That seems feasible to us given that CCI has already contracted most of its growth for the future years, the 5G tailwind keeps attracting more investments into this infrastructure, and the REIT has a strong balance sheet and reasonable payout ratio. The market dislikes the lack of growth over the next 2 years, but this is just a temporary slowdown that's caused by T-Mobile's ( TMUS ) recent acquisition of Sprint. As you remove the impact of lease cancellations, its growth will reaccelerate and the stock will likely rerate a lot higher as well. We expect 50% upside and while you wait, you earn a 6.1% dividend yield.

{kind=link}

EPR Properties ( EPR ) is a bit riskier, but it still remains a high-quality REIT. It owns a diversified portfolio of experiential net lease properties that generates highly consistent and predictable rental income from 10+ year-long leases that include contractual annual rent hikes. It has a strong investment grade rated balance sheet, it is experiencing steady cash flow growth, and its payout ratio is today historically low at just 70%. The REIT hiked its dividend this year and it is in a strong position to hike it again in 2024. The market worries about its movie theater portfolio, but even those assets have a positive rent coverage, and its leases with AMC (AMC) and Regal have already been renegotiated. We believe that the stock is undervalued by 20-30% and it offers a 7.5% dividend yield.

EPR Properties

Gladstone Commercial Series O Preferred Shares ( GOODO ): GOOD is a smaller REIT than EPR and CCI and smaller size comes with higher risk. But its business is on strong footings. GOOD owns mostly industrial properties that benefit from the growing trends of e-commerce and onshoring. Moreover, it has no major debt maturities for years to come and the REIT retains a good amount of cash flow to gradually pay down debt. We chose to invest in its preferred equity because it pays a higher yield at 8.6% and it enjoys better margin of safety. We think that as interest rates eventually return to lower levels and/or as GOOD keeps reducing its leverage, the market will eventually reprice it at closer to its par value, unlocking 20-30% of additional upside. So while the dividend of the preferred stock won't grow, there is some additional upside, which could allow us to sell some stock to reinvest elsewhere to grow our dividend income over time.

Gladstone Commercial

KKR Real Estate Finance Series A Preferred Shares ( KREF.PR.A ): The story is similar to that of GOODO. The REIT itself is a bit riskier because it is smaller in size and uses more leverage than the average, but we go up its capital stack and invest in its preferred equity to enjoy greater margin of safety and earn a higher yield. KREF is a mortgage REIT and what we like about it is that it only makes senior debt investments and most of its loans are backed by residential properties. Some occasional defaults are inevitable, but we think that KKR's team is in a good position to workout such situations. After all, KKR ( KKR ) is one of the world's leading private equity firms, they have good collateral, and their ~60-70% LTVs provide buffer to mitigate losses. Just like GOODO, the preferred stock is here also priced at a large discount to par, offering about 20% upside potential in the coming years. While you wait, you earn a 9.2% dividend yield.

{kind=link}

Finally, NewLake Capital Partners ( NLCP ), our highest-yielding REIT, is likely also the riskiest of the portfolio. But even here, we think that the REIT is more resilient than what the market gives it credit for, and a dividend cut seems unlikely to us. On the contrary, NLCP has been steadily growing its dividend in recent years, and today, it even has sufficient liquidity to buy back shares. NLCP owns net lease properties just like EPR, but it is riskier because its tenants are cannabis companies. They are riskier tenants and it is likely to face more frequent tenant difficulties. However, what the market appears to have missed is that NLCP mitigates these risks by focusing on limited-license states, leasing space to stronger operators, diversifying by markets, and maintaining a pristine balance sheet with zero debt and significant liquidity. This puts it in a strong position to work out the occasional lease defaults. Since its properties are in limited license jurisdictions, they should be desirable to other tenants as well, as long as there is growing demand for cannabis. Today, the REIT's payout ratio is just 80% and the REIT is able to use the remaining 20% to buy back shares since it has zero debt. Its cash flow has grown by 5% this year and more growth is expected in 2024. Therefore, a dividend cut seems unlikely to us. How many debt-free and growing companies do you know that offer an 11.6% dividend yield?

NewLake Capital

So here you have a portfolio that's capable of earning $1,000 per month of dividend income with just $139,534.

We believe that this dividend income should be sustainable and grow further from here. Moreover, the portfolio should also appreciate in value as the market sentiment for REITs improves in the coming years. After all, it is unlikely to get much worse from here given that it is already at its lowest since the great financial crisis:

{kind=link}

For further details see:

Portfolio Reveal: 5 REITs To Potentially Earn $1,000 Every Month