PTLO - Portillo's: Getting More Interesting But Still Not A Buy

2024-01-12 17:46:51 ET

Summary

- Portillo's shares have performed poorly, declining over -23% in the past year.

- Negative restaurant traffic and high starting valuation have contributed to poor share performance. Food and labor cost inflation could remain a headwind in 2024.

- Despite this, Portillo's has a passionate core Chicago customer base and ample opportunity for continued restaurant growth in the medium term.

- At $14.50 shares trade for ~13x 2024e EBITDA which seems about fair.

Portillo's Inc. ( PTLO ) shares have performed poorly over the past year, declining over -23% versus a 6% gain for the small-cap index ( IWM ). While operating performance for Portillo's has improved versus 2022, share performance has been poor due to:

- Negative restaurant traffic in 3Q23. While Portillo's 2023 same-store restaurant sales have been positive, this has all been due to price increases implemented over the past year to offset inflationary pressure.

- High starting valuation. Coming into 2023, Portillo's was trading at ~19x forward EV/EBITDA which was a large premium to the broader market.

- Concerns that lingering food and labor cost inflation could hamper operating performance heading into 2024.

As we sit today, with a valuation of 12.9x 2024e EBITDA I see Portillo's shares as being about fairly valued. Given Portillo's strong brand and enthusiastic Chicago customer base coupled with a sunbelt-focused restaurant expansion strategy, Portillo's is a business I'd like to own if shares were to fall further.

With PE sponsor Berkshire Partners (Berkshire bought Portillo's in 2014 and still owns ~40% of total shares) approaching the 10 years of ownership (PE funds typically have a 10-year life), I wouldn't be surprised to see selling pressure as we move through 2024, which could present an opportunity for value investors like myself to scoop up shares at a discount. I'd be interested in owning the stock if shares were to fall another 25% to $11.

Recent Results

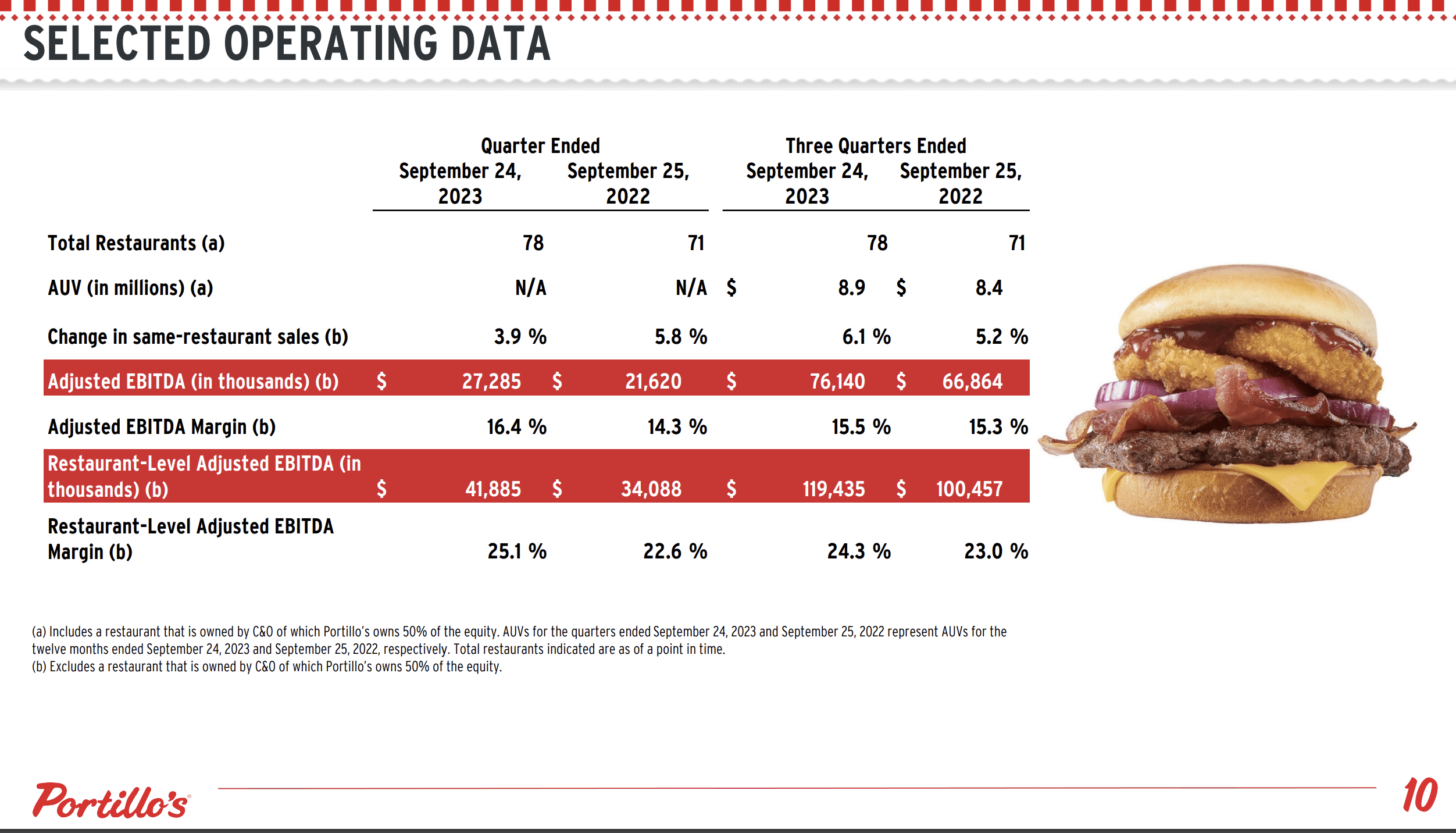

Portillo's 3Q23 & 2023 YTD Results (Portillo's 3Q23 Investor Presentation)

{kind=link}

As shown above, Portillo's has seen a nice rebound in operating performance in 2023 with solid same-store sale growth which has led to a stabilization in EBITDA margins. The company saw a decline in EBITDA in 2022 as food and labor cost pressures eroded margins. Like most restaurants, in late 2022 and early 2023, Portillo's implemented a series of menu price increases to restore profit margins.

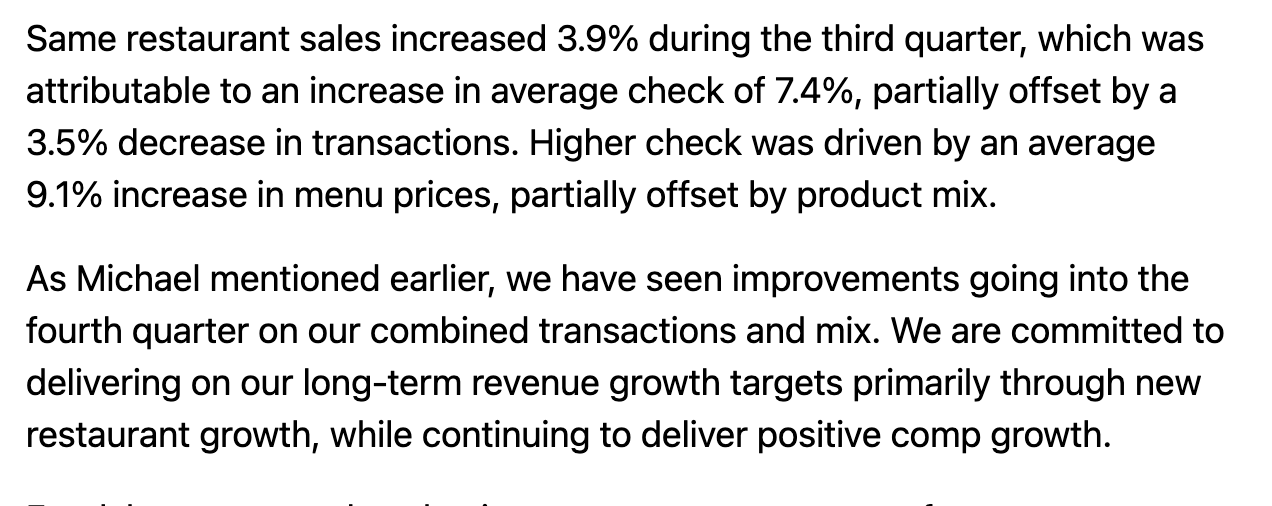

As shown below, while same-store sales have been positive, Portillo's saw a decline in transaction levels (customer count) in 3Q23. This is not unique to Portillo's - peers like Shake Shack Inc. ( SHAK ) also saw a decline in customer count in 3Q23 as inflation has pressured consumer spending.

Management commentary on Same Store Sales (3Q23 Earnings Transcript from Seeking Alpha)

{kind=link}

Growth Outlook

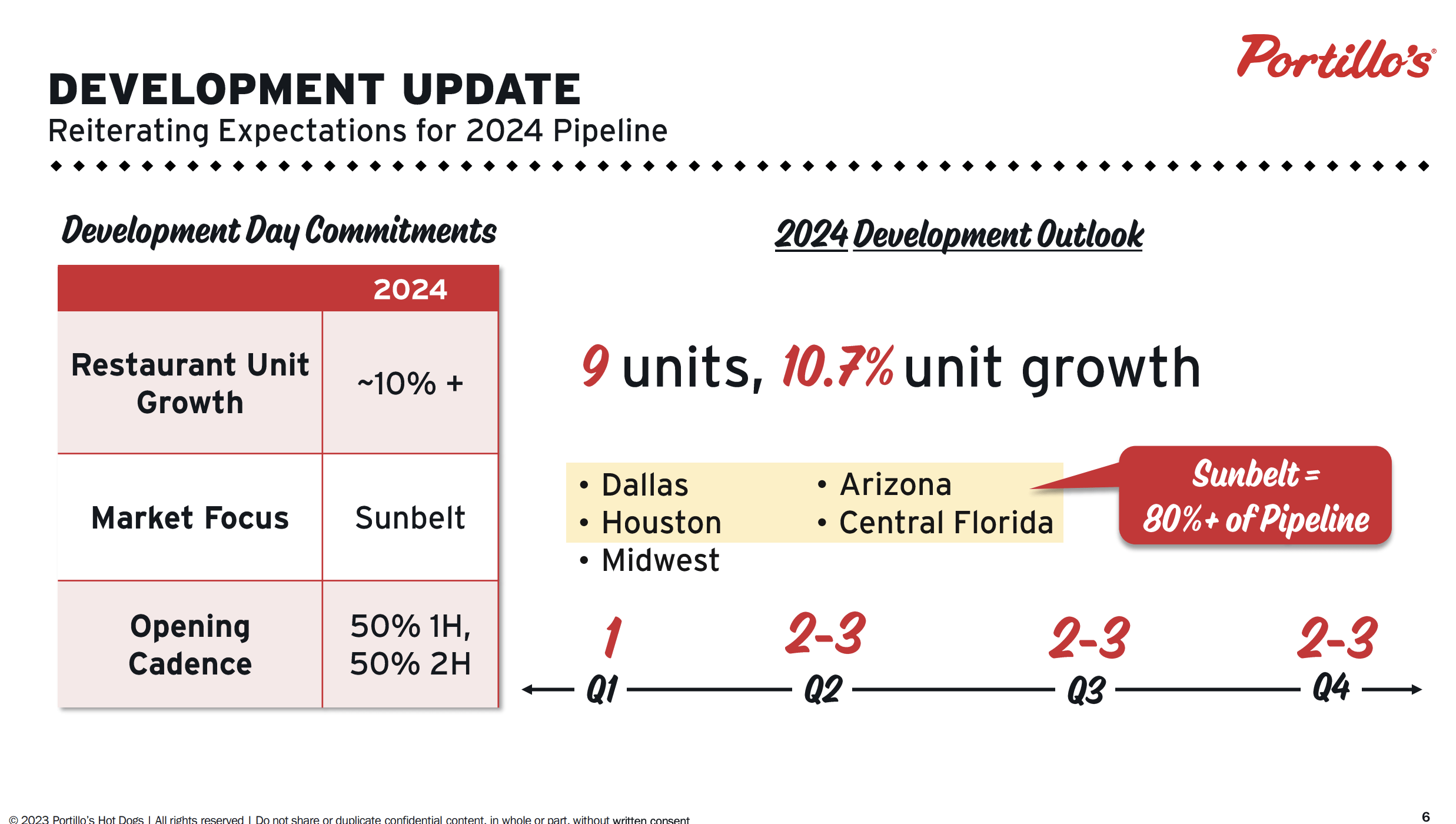

Portillo's believes that it can expand the chain from 84 restaurants today to 900 eventually. The company plans to open 9 new restaurants in 2024, focused mainly on faster-growing Sunbelt markets like Texas, Arizona, and Florida.

Portillo's 2024 Expansion Plans (Portillo's 2024 ICR Presentation)

{kind=link}

At the company's 2023 Development presentation, Portillo's outlined a more rapid expansion program whereby it seeks to increase annual restaurant growth from 10% to 12-15% over the medium term. The company will use more smaller footprint restaurants (~5,000 square feet versus legacy 8-10,000 square foot locations).

Portillo's AUV (average unit volumes) in Sunbelt markets is $6-6.5 million which compares favorably to other restaurants but is well below the ~$10 million achieved in its Chicagoland locations (where Portillo's has 50+ years of operating history and greater customer affinity/loyalty). Sunbelt locations have lower restaurant-level EBITDA margins at 17-22% versus ~30% in Chicagoland. As such, over time we should expect to continue to see group-level EBITDA margins decline as lower margin sunbelt locations represent an increasing share of overall sales.

It is also worth noting that as Portillo's achieves critical mass (management targets six restaurants in a market) in newer markets like Phoenix and Dallas, it benefits from scale (advertising, restaurant development, food prep & distribution) which should bolster margins.

Valuation

As we sit today at $14.50 per share, Portillo's trades at just under 13x 2024 EBITDA. For the foreseeable future, all operating cash flow is being used to fund new restaurant development (Portillo's guides to $90 million in 2024 capex, of which 80% is going toward new restaurants). On a maintenance capex basis (ignoring expenditure related to new restaurant development), Portillo's should generate about $0.70 per share in free cash flow in 2024, implying a valuation of ~21x free cash flow (maintenance basis) which seems fully valued considering an expected 3-4% growth rate (excluding new units).

Factoring in expected new unit development, I expect Portillo's will generate $140-150 million in 2027 EBITDA. Assuming Portillo's trades at 12-15x 2027e EBITDA suggests a 2027 fair value in the range of $17.50-$25 per share and implies 20-70% upside (6-22% annualized returns). By comparison, Shake Shack (probably the most comparable peer) trades at ~17x 2024e EBITDA (though I believe it is a bit overvalued here). All-in, I believe Portillo's is about fairly valued here at $14.50.

Conclusion

Portillo's has a passionate core Chicago customer base and appears to be having success expanding into faster growth markets. As we sit today, I see the stock as being roughly fairly valued. As noted in my introduction, I think that there is a chance we see Berkshire reduce its stake which could put pressure on the stock. As a value investor, I would be interested in owning shares at a 25% discount to my estimate of fair value - as such I'd be a buyer below $11.

For further details see:

Portillo's: Getting More Interesting But Still Not A Buy