PTLO - Portillo's Has A Runway For Growth But Can It Provide Return To The Common Shareholder?

2023-04-14 11:53:10 ET

Summary

- Portillo's is a Chicago staple, selling classics like Chicago Dogs, and Italian Beef sandwiches.

- The company wants to aggressively open stores across the country.

- After the IPO, Portillo's has finally returned profits to the common shareholder, making the valuation much more worthy.

Introduction

The first time I ate a Chicago Dog changed how I would eat hot dogs forever; plain ketchup and mustard don't satisfy me any longer. Chicago street food staples are some of the best the country has to offer. Portillo's ( PTLO ) is a namesake in the city but has been trying to grow outward to provide these delicious regional eats to the entire United States. Currently, in just nine states, Portillo's has an aggressive growth plan and is funding it through the IPO and secondary offerings of the past two years. With this growth potential and the retirement of redeemable preferred shares eating away common shareholders' profits, the company should see strong earnings growth.

IPO, Business, & Financial Results

In late 2021, Portillo's had an IPO, which put this up-and-coming restaurant on the public markets. Then in late 2022, the company had a secondary offering to raise more funds. The reason for these actions was to raise money to fund growth and pay down debt. In the end, the public company fully manages the operating business but only owns 67%, while the pre-IPO LLC members own 33%.

Portillo's has set out three main priorities upon the creation of the new holding company. The business wants to expand the restaurant base by 10% per year, see positive same-store sales yearly, and drive profitability. These goals are believed to power growth for the future.

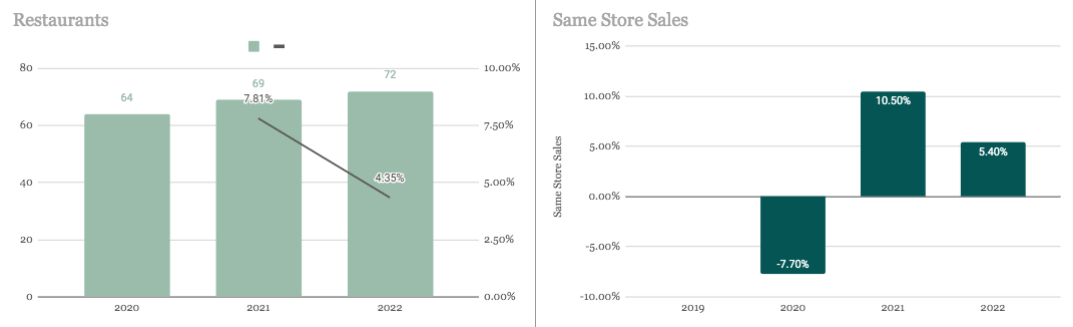

Portillo's Revenue (SEC.gov) Portillo's Restaurants & Same Store Sales (SEC.gov)

{kind=link}

Now, looking into the business operations and metrics, has Portillo's been growing at the rates set out above? Revenue has grown at a CAGR of 5.21% and bounced back from the pandemic lows of 2020 strong. The business has grown its store count by eight for a rate of just 4%. This is very shy of the 10% goal. Same-store sales since the pandemic have been great, with positive results in the past two years. Overall, Portillo's is growing the business, opening stores, and seeing good sales in both existing and new stores. The business is not quite meeting the store growth goal, but this is not a big deal in my eyes.

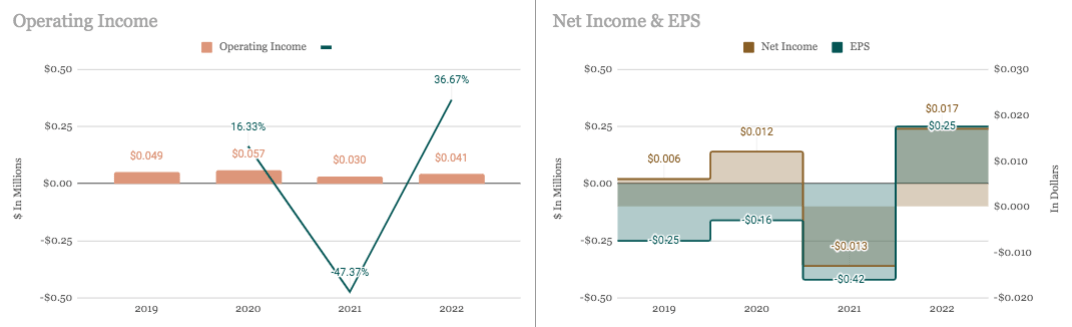

Portillo's Operating & Net Income (SEC.gov) Portillo's Margins (SEC.gov)

{kind=link}

On the other hand, operating income has struggled to get any momentum. This is due to increased costs, as can be seen in the COGS margin trend. In particular, 2022 COGS increased by 22.5% due to inflation. Also affecting operating income was a 118.5% increase in SG&A due to stock-based compensation charges tied to the IPO. This major cost increase in 2021 and the COGS increases in 2022 have made net income attributable to the whole business choppy too. Right now, it is a bit hard to gauge the past growth on a year-to-year basis, but since 2019 operating income has declined while net income has grown.

But as mentioned before, 33% of the business is still owned by non-controlling entities, meaning the net income attributable to the shareholder is lower. And until 2022, Portillo's was posting a loss for these shareholders. But in 2022, the tides seem to have changed a bit. The company posted the first-ever profits for their shareholders by not having increased stock compensation costs from the IPO and drastically lowering interest expenses with IPO funds. The business also repaid all redeemable preferred shares in 2021, which were eating $20 million a year out of the bottom line. With these actions, it seems Portillo's is driving growth for its shareholders.

Balance Sheet

With the IPO, Portillo's wanted to pay down debt and expand the business. The debt-to-equity is now at 1.96x, which is not bad at all and offers room for higher debt loads as growth continues. Also, the current ratio is solid at 0.85x, showing the business can meet current obligations. This balance sheet is healthy and offers room for Portillo's to grow without putting financial stability at risk.

Valuation

As of writing, Portillo's is trading around the $20 per share mark. At this level, the business trades at a P/E of 80x. This is very high, and to get a PEG at 2x 40% per year growth would need to be booked. I think the valuation is a little rich right now, but from 2019 to 2022 net income has grown at a rate close to 30%. So, if the business has finally figured out how to return profits to the common shareholder, then bottom-line growth could see this same growth rate or more. The growth potential of this business is high, and therefore I see Portillo's as just a little over fair value.

Conclusion

Overall, Portillo's has a lot of runway to grow. And the business has sights out on an aggressive growth plan. While the business has had road bumps in returning earnings to the common shareholder the past few years, it seems this issue may be in the past now. I think at the current valuation, Portillo's is a little overvalued but could still offer a great return if growth pans out.

For further details see:

Portillo's Has A Runway For Growth, But Can It Provide Return To The Common Shareholder?