PTLO - Portillo's: Limited Margin Of Safety At Current Levels

Summary

- Portillo's reported record revenue in Q3 but margins fell short of expectations with continued pressure from commodity/wage inflation.

- This margin pressure was exacerbated by weaker industry traffic trends and Portillo's more conservative approach to pricing to allow its relative value to shine through.

- Fortunately, we could see a better year ahead for margins as labor a availability could improve with the increase in layoffs in other sectors and commodity inflation cooling off.

- That said, while PTLO could have a better year ahead and is set to see double-digit unit growth, I don't see any margin of safety at current levels, with the stock trading above 17.0x FY2023 EV/EBITDA.

Just over five months ago, I wrote on Portillo's ( PTLO ), noting that the stock's rally above $26.00 in August was a great opportunity to sell at least 3/4 of one's position. Since then, the stock has massively underperformed its peer group, with large-cap peers like Restaurant Brands ( QSR ) up 17% in a period where Portillo's has declined 15% and suffered a 38% drawdown, more than 1.5x the decline suffered by the major market averages. The softness in the stock can be attributed to continued margin pressure due to commodity inflation coming in above expectations and the fact that PTLO wasn't cheap by any means while it hovered above $26.00, trading at a market cap north of $2.0 billion or more than 20.0x EV/EBITDA.

The good news is that traffic trends appear to be improving a little industry-wide after a tough summer due to elevated gas prices, and while Portillo's expects commodity inflation to come in at ~15% in FY2022, we are seeing inflation cool off finally. The result is that Portillo's could see a slight improvement in EBITDA margins this year after a violent decline in FY2022 (elevated labor and commodity costs). That said, although the 2023 outlook is better and the company continues to maintain an industry-leading growth rate, I still don't see any margin of safety here, and the stock is now short-term overbought after a 40% rally over the past three weeks. Let's take a closer look below:

{kind=link}

Portillo's - Michigan (Company Presentation)

Q3 Results

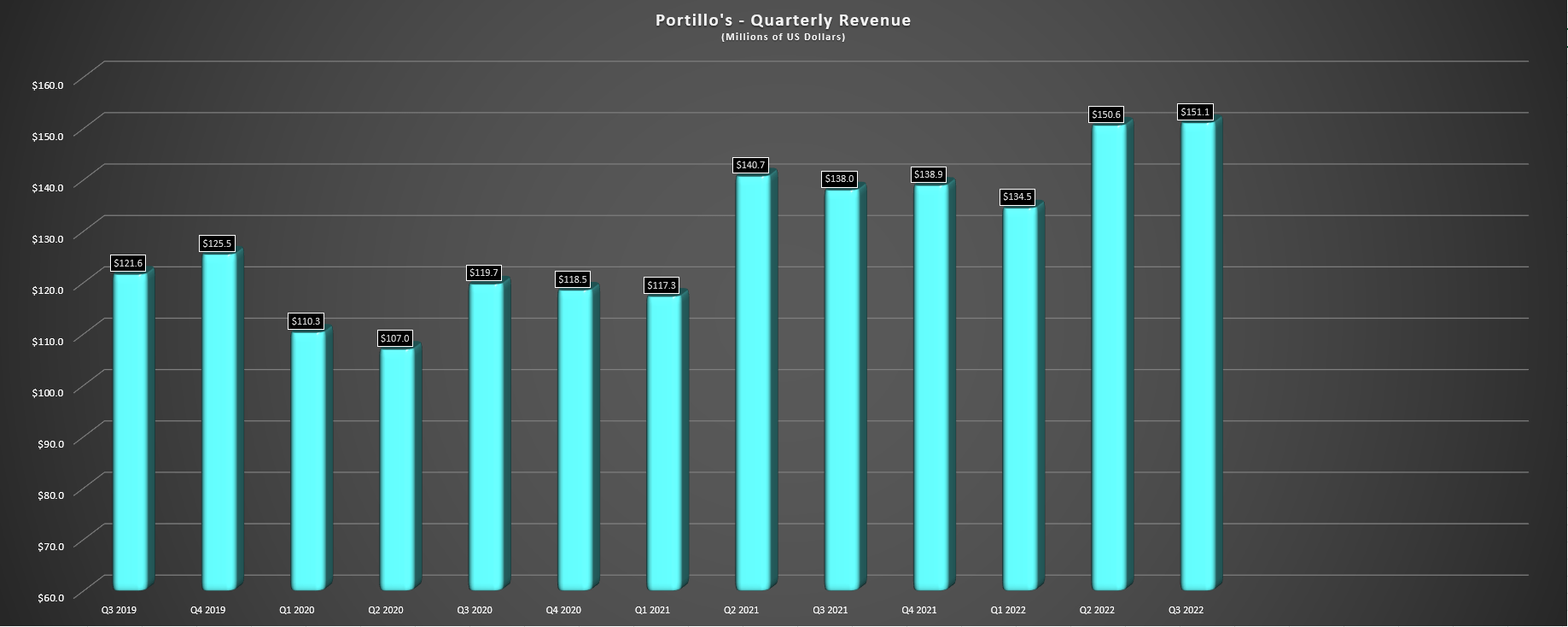

Portillo's released its Q3 results in November, reporting record quarterly revenue of $151.1 million, a 10% year increase vs. the year-ago period. This sharp increase in revenue was driven by four new restaurant openings that contributed $5.8 million in revenue and 8.2% effective pricing as the industry continues to raise prices at high single-digit to low double-digit levels to combat rising costs. Meanwhile, same-restaurant sales were up 5.8% in Q3 or 12.6% on a two-year stacked basis. Although this might appear to be a solid figure, this was primarily driven by pricing, evidenced by a 6.3% increase in average checkoff offset by a 3.3% decline in transactions. This decline in transactions is not ideal, but it is a theme we continue to see industry-wide ( [-] 4.3% traffic growth in November ).

{kind=link}

Portillo's - Quarterly Revenue (Company Filings, Author's Chart)

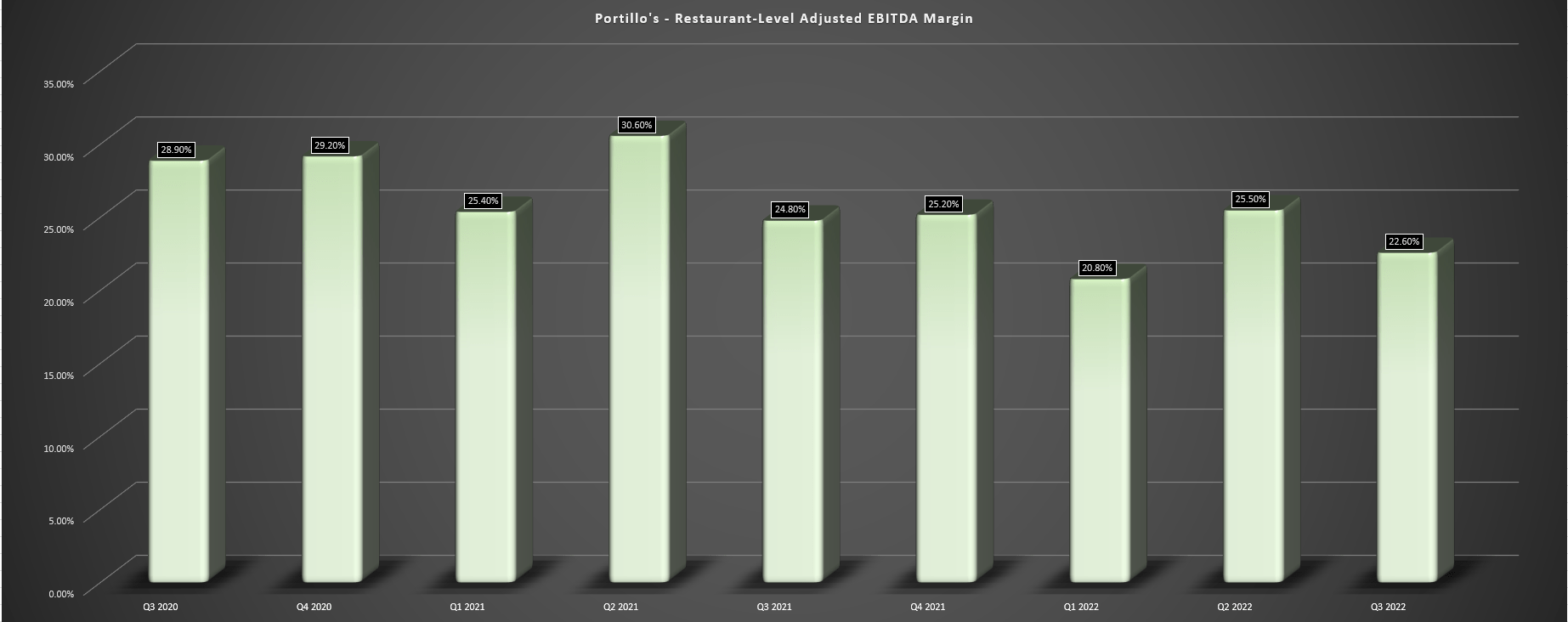

On the positive side, the company was somewhat of an outlier from a staffing standpoint, reporting that staffing was sitting at over 100% and had better turnover levels than the industry. This could be helped by continued investments in its team as Portillo's, and additional hourly rate increases were put in place at the beginning of Q3. That said, these continued investments, combined with elevated commodity inflation (15.4% increase year-over-year in Q3), have placed severe pressure on margins. As shown below, restaurant-level adjusted EBITDA margins plunged to 22.6% in Q3 (down 220 basis points year-over-year), and they were down 630 basis points on a two-year basis, which has undoubtedly taken some of the shine off a company that debuted with investors salivating over their strong margins and double-digit unit growth.

{kind=link}

Portillo's - Restaurant Level Adjusted EBITDA Margin (Company Filings, Author's Chart)

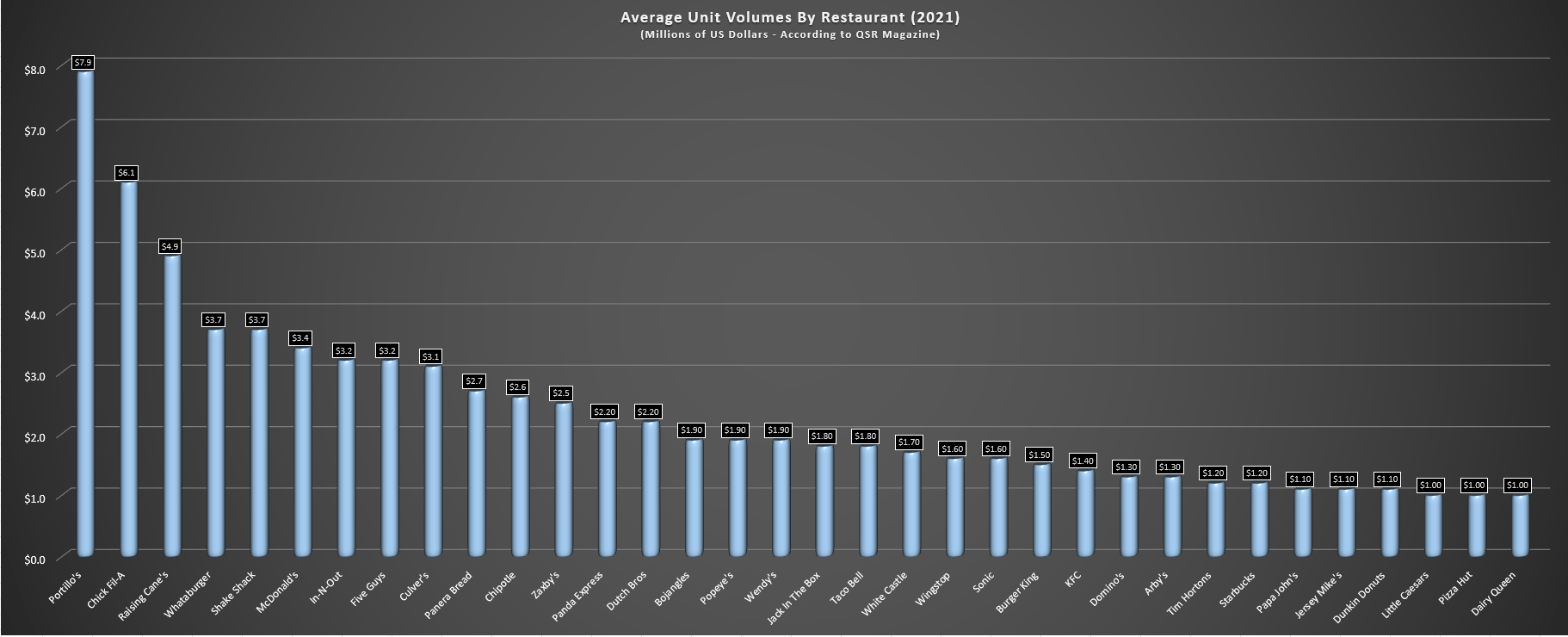

Although Portillo's continues to work on an initiative called Kitchen 23, which is a more efficient model with better labor utilization and lower equipment costs, I wouldn't expect much relief from a margin standpoint in Q4, given mid-double-digit commodity inflation and continued investments in its team members. The result is that adjusted EBITDA margins could dip to barely 14.0% in FY2022. To summarize, although Portillo's is doing a solid job growing its top line, and average unit volumes remain at industry-leading levels ($8.4 million), it's certainly been a tough two years from a profitability standpoint and higher build costs due to inflation haven't helped either.

{kind=link}

Average Unit Volumes by Restaurant (2021) (QSR Magazine, Author's Chart)

Recent Developments & Industry Trends

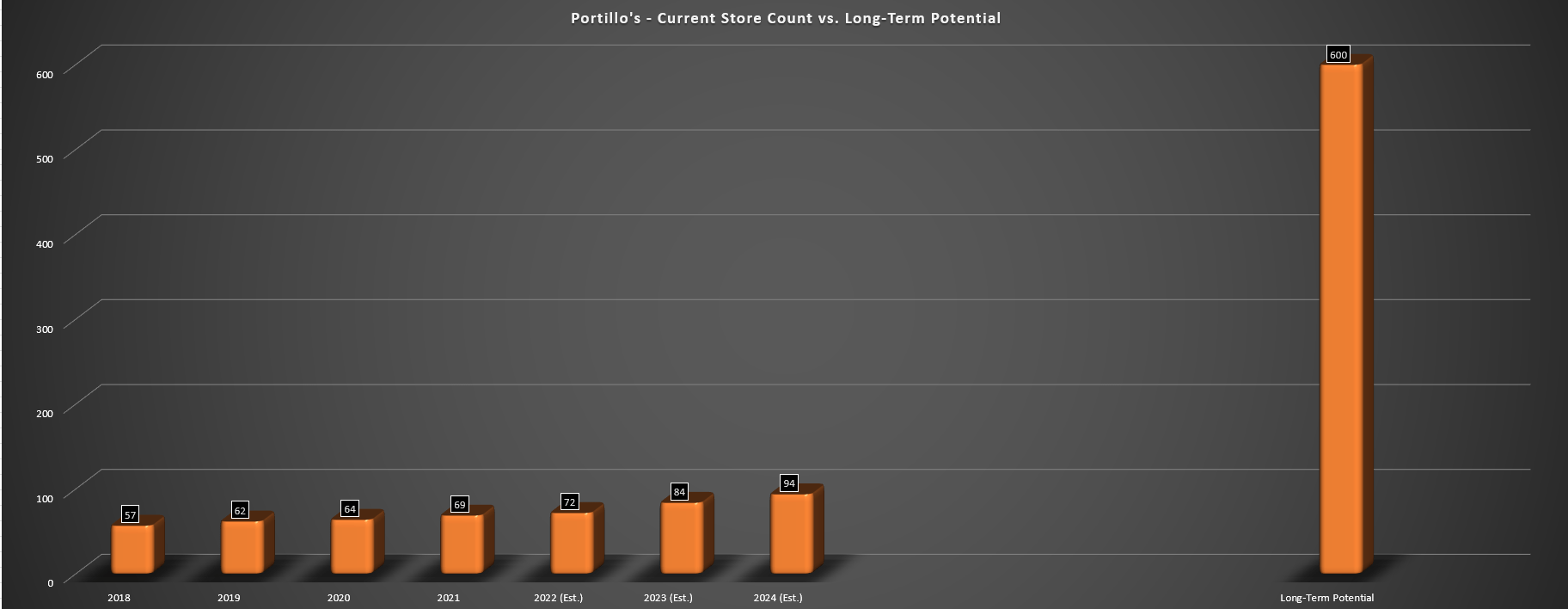

Looking at recent developments, Portillo's ended the year with 72 restaurants in 10 states (three 2022 openings pushed into early 2023), with new openings planned in Tucson and Gilbert, Arizona, plus nine new openings planned in the 2023 class. This would translate to a 12% unit growth rate assuming the mid-point of guidance (8-10 openings) is reached after adjusting for three new restaurants in the 2022 class falling just behind schedule, and a 13% growth rate if Portillo's meets the top end of guidance. The result is an ~8% compound annual growth rate since FY2018, and Portillo's expects to enjoy a 10%+ CAGR in the future and is confident it has the potential for 600+ restaurants, suggesting that this is clearly a growth story in its early innings.

{kind=link}

Portillo's - Store Count, Forward Estimates & Long-Term Potential (Company Filings, Author's Chart & Estimates)

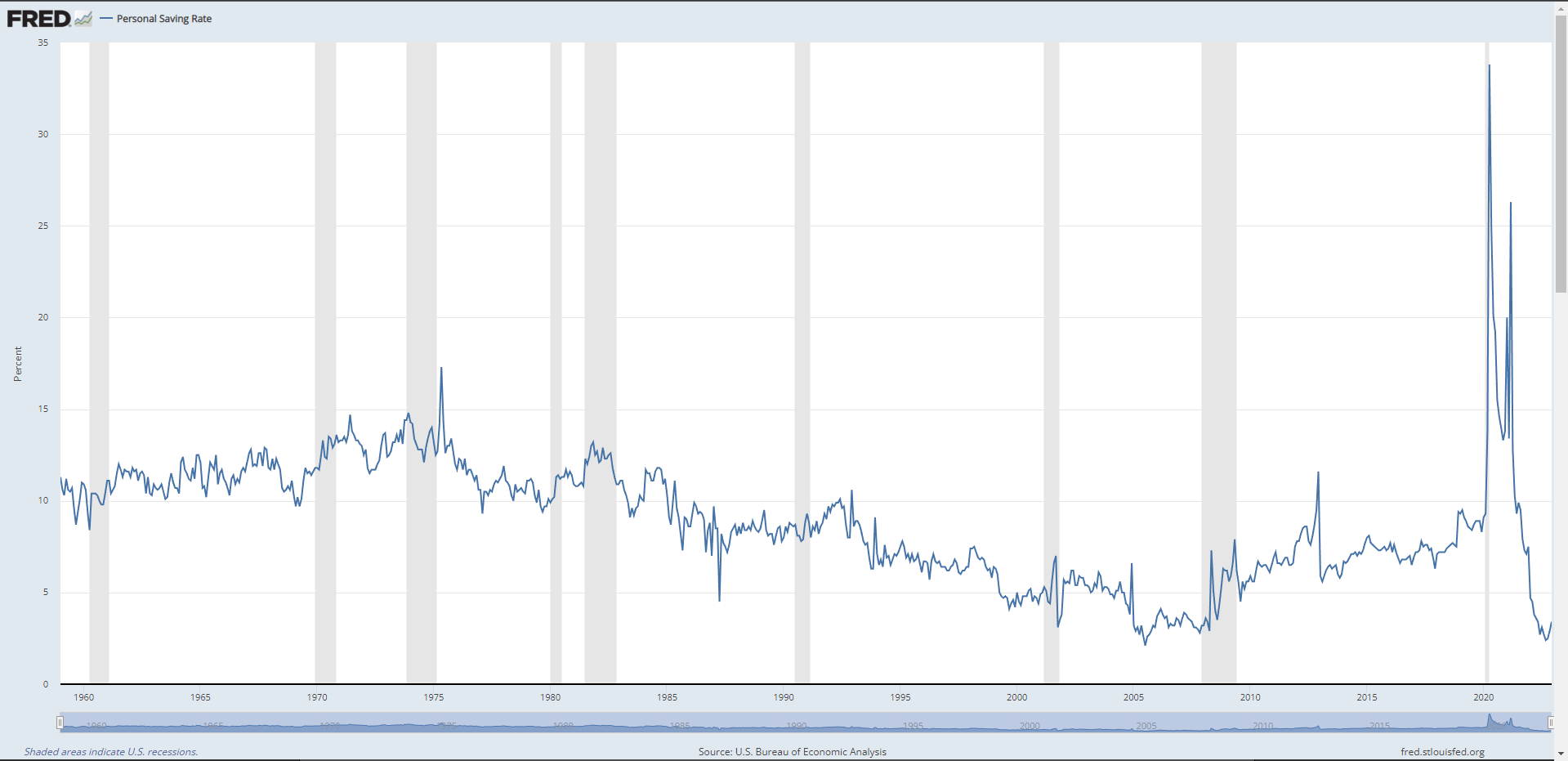

While the company's strong growth rate and considerable whitespace are positives, the industry backdrop remains challenging, with personal savings rates at multi-year lows and discretionary budgets continuing to remain under pressure. This can be attributed to rising rent/mortgage costs, higher grocery/energy costs, and general inflation, which have placed financial stress on the average consumer. Worse, we've seen a sharp reversal in the wealth effect with bear markets in equities and cryptocurrencies, plus a more negative outlook for the housing market, which certainly doesn't increase consumers' appetite to spend when they're feeling much less rich. Hence, it's little surprise that restaurant sales softened in November, with same-store traffic down 4.3%, according to Black Box Intelligence.

{kind=link}

Fred.StLouisFed.Org (Personal Savings Rates)

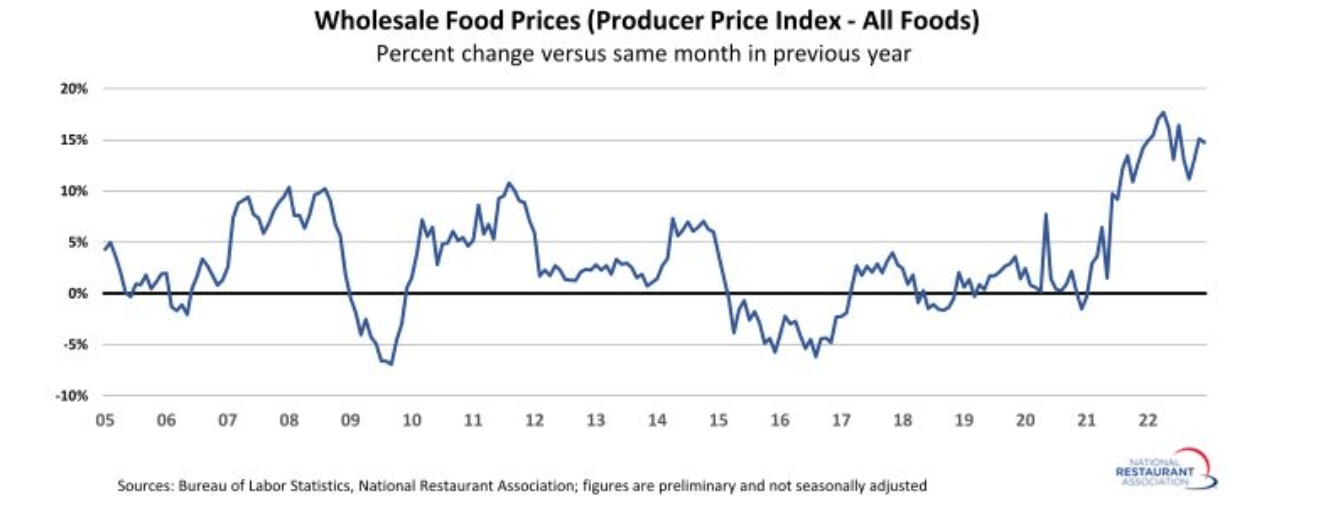

While the negative traffic growth due to inflation and lower consumer confidence are headwinds from a sales standpoint for Portillo's and other restaurant brands, the industry has also continued to see commodity and wage inflation that has bit into margins. This was evidenced by Portillo's cost of goods sold increasing 320 basis points year-over-year to 35.3% in Q3, and while labor costs were down slightly year-over-yer as a percentage of sales, they're up 30 basis points year-to-date and could climb further with the impact of recent wage hikes. The result is that Portillo's saw its restaurant-level operating margins dive to 22.6% in Q3 2022, down from 24.8% in the year-ago period. The company called out beef and chicken as two areas that had an outsized impact on its commodity basket.

{kind=link}

Wholesale Food Prices (National Restaurant Association)

Fortunately, we appear to be seeing some moderation in commodity inflation, and Portillo's is now expecting to ~5% commodity inflation in 2023, a significant improvement from ~15% last year. Meanwhile, with a substantial increase in layoffs due to the recessionary environment we appear to be in, we could see an improvement in a very tight labor situation and moderation in wage growth rates. These are both major positives for restaurant operators, as is the fact that while it may be only a small portion of costs, gas prices remain well off their highs which is a minor win for a consumer that is getting hit from all angles from an inflationary standpoint. Hence, we are seeing some tailwinds for the industry that could lead to much less margin pressure in 2023 and potentially better traffic trends in Q4/Q1 that could set up a decent earnings season.

{kind=link}

Portillo's Menu (Company Website)

Finally, it is worth noting that while some restaurant brands have been very aggressive with pricing and a select few appear to be trying to increase margins on the back of their valued and loyal guests even as some struggle financially, Portillo's has been more conservative than its quick-service peers. This is evidenced by its pricing of ~8% in Q3 2022, slightly below the industry average and miles below Chipotle ( CMG ), which ran at nearly 14% in Q4 2022 and approximately 450 basis points above the industry average. The result of this balanced approach to taking prices by Portillo's (combat inflation but ensure guests see the relative value in their menu offerings) has translated to strong guest satisfaction scores for the brand.

In fact, Portillo's noted on its most recent call that guest satisfaction scores trended higher in Q3 and are sitting at their highest levels in three years. So, while some brands may lose guests or, at a minimum, visits due to aggressive pricing if regular guests begin to feel taken advantage of in a vulnerable period (recessionary environment), I don't see this risk for Portillo's, and it's certainly positive to see that its taking care of its team members as well and investing in the right places. Now that we've established that Portillo's is a solid growth story in the quick-service space with industry-leading AUVs and a very crave-able menu (burgers, hotdogs, Italian beef sandwiches), let's dig into the valuation:

Valuation & Technical Picture

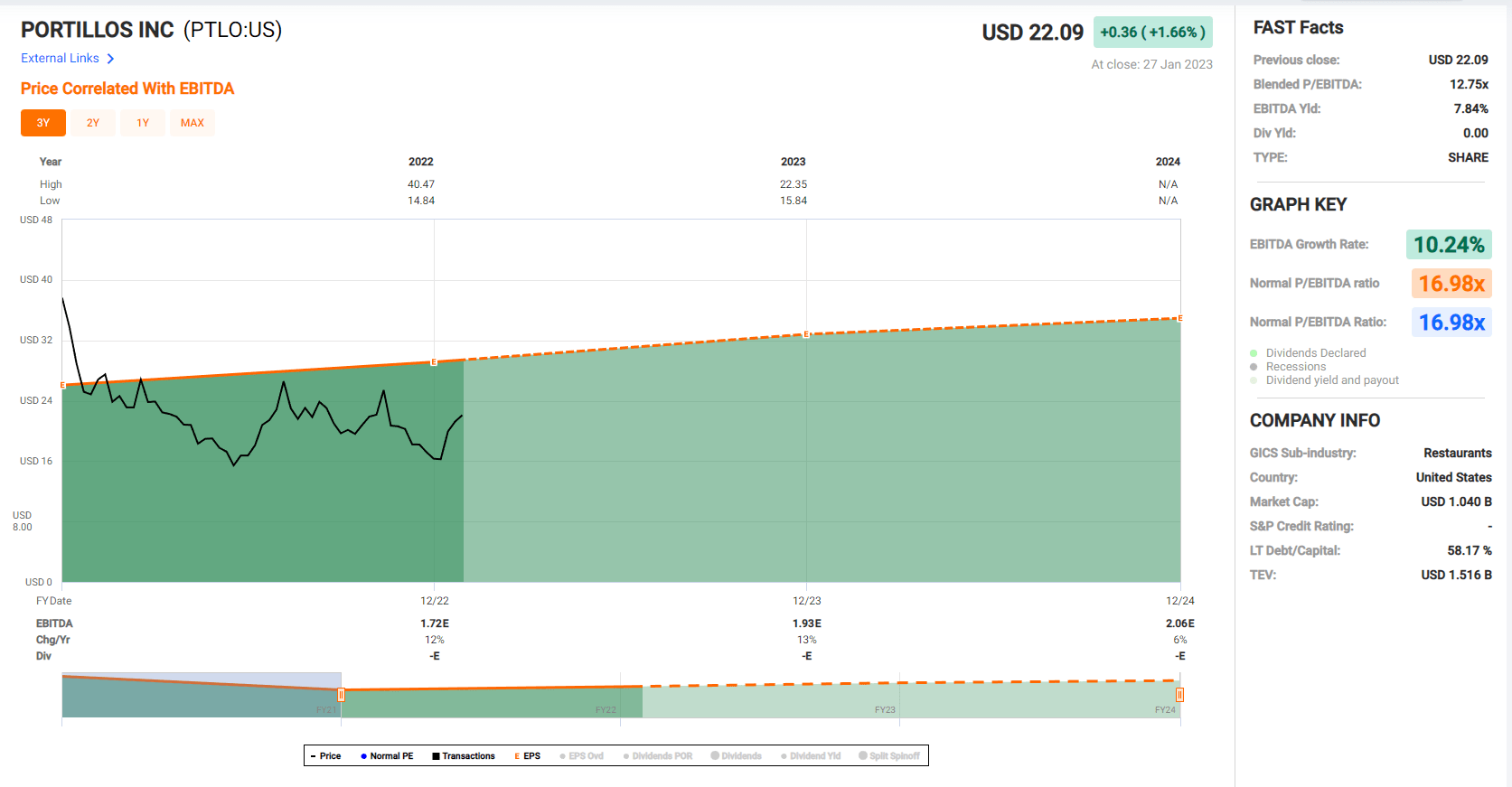

Based on ~72 million shares outstanding and a share price of $22.20, Portillo's trades at a market cap of ~$1.60 billion and an enterprise value of ~$1.88 billion. If we compare this figure to FY2023 estimates of ~$97.0 million in EBITDA, this leaves the stock trading at ~19.3x EV/EBITDA. This is not cheap for a company with a trend in declining margins, even if it is a solid growth story (10%+ unit growth) with an iconic brand. Using what I believe to be a more conservative multiple of 17.5x EBITDA and FY2023 EBITDA estimates ($97 million) and adjusting for net debt, I see a fair value for Portillo's of ~$1.42 billion, translating to a fair value of $19.70 per share. Hence, I see the stock as fully valued at current levels.

{kind=link}

PTLO Historical P/EBITDA Multiple (FASTGraphs.com)

Obviously, this doesn't mean that the stock must drop this low immediately, and with momentum behind the market currently, it's possible that Portillo's rally could continue short term. However, I prefer to pay the right price for stocks (ensure a significant margin of safety) or pass entirely. This is especially true when the Federal Reserve is hawkish, which can be a significant headwind for the market. So, based on a minimum required 25% discount to fair value to bake in some margin of safety for small-cap growth stocks, PTLO would need to dip below $14.60 to become interesting from a valuation standpoint.

{kind=link}

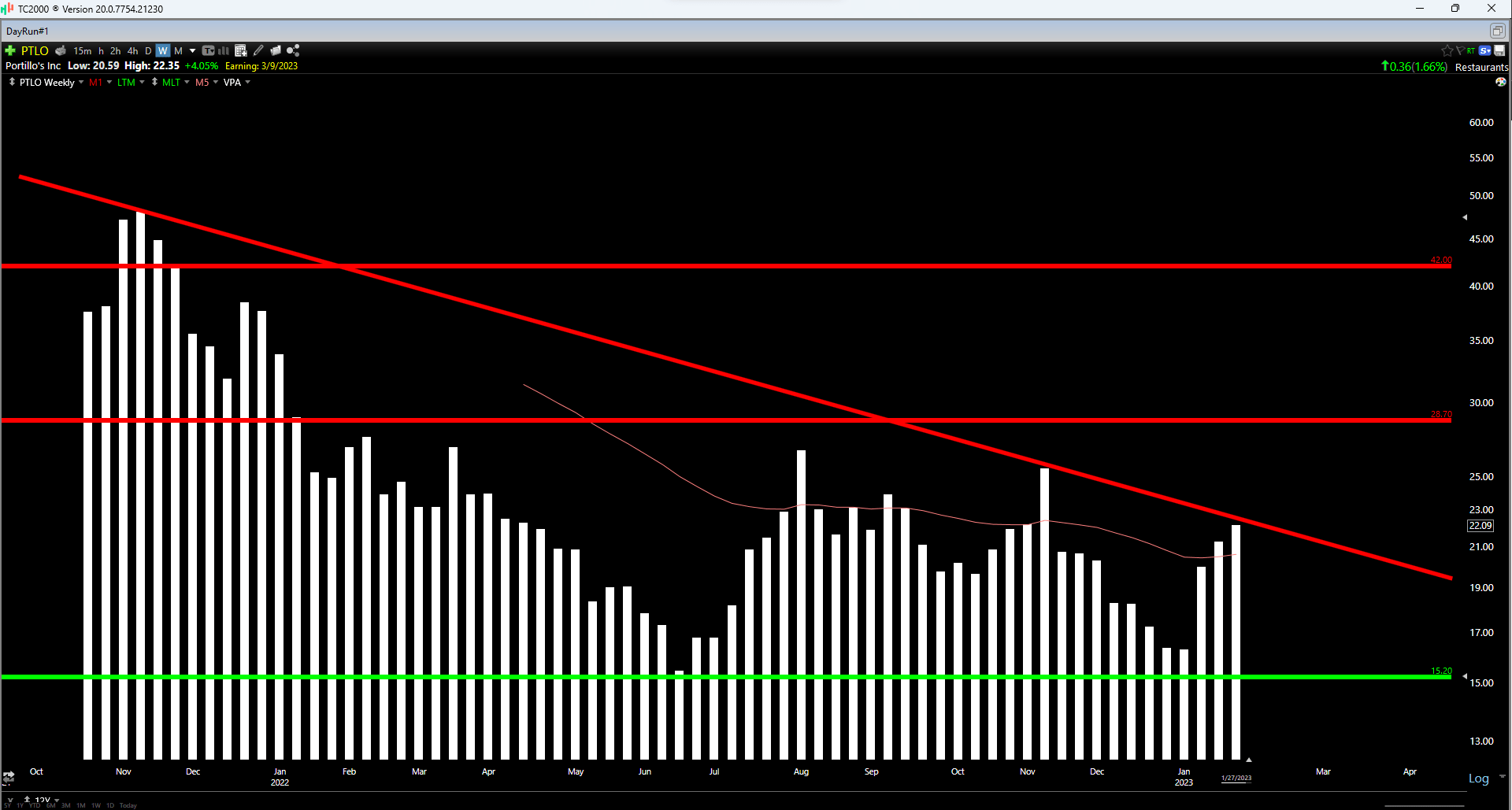

PTLO Weekly Chart (TC2000.com)

Looking at PTLO from a technical standpoint, I noted in my most recent article that the stock would become interesting near US$15.20, and the stock found its lows just above this level and has since rallied over 40%. However, the stock is now within 5% of potential downtrend line resistance and more than 45% above its next strong support level. Plus, if the stock were to push through this potential resistance area, it has major resistance at $28.70, translating to a balanced reward/risk setup at best currently ($7.00 in potential downside to support, $6.60 in potential upside to resistance). So, with the stock in the middle of its expected trading range and sitting above what I would consider conservative value, I don't see any reason to pay up for the stock here.

Summary

Portillo's had a tough year with the rest of the industry in 2022, and its sales figures might beat estimates in Q4 and Q1 if traffic trends improved in December and January. Fortunately, the company should have a better year ahead with more than 11 new openings and what should be a less challenging environment from a margin standpoint as wage/commodity inflation begin to moderate after two tough years. However, while this could keep a bid under the stock, I see PTLO as a trading vehicle only, given that I don't see any margin of safety at current levels. So, if we were to see PTLO's rally continue and it heads above $25.50 before June, I would view this as an opportunity to book profits.

For further details see:

Portillo's: Limited Margin Of Safety At Current Levels