DRI - Portillo's: Patience Required

2023-09-25 14:47:05 ET

Summary

- Portillo's Inc. has underperformed its peers, sliding ~30% in the past eight months.

- And while its Q2 results showed decent same-restaurant sales growth, the Q4 outlook is foggy with weakening traffic trends industry-wide in Q3 that could persist.

- In this update, we'll look at Portillo's valuation after the drop and its path to improving unit economics to see whether the stock is worthy of buying on this dip.

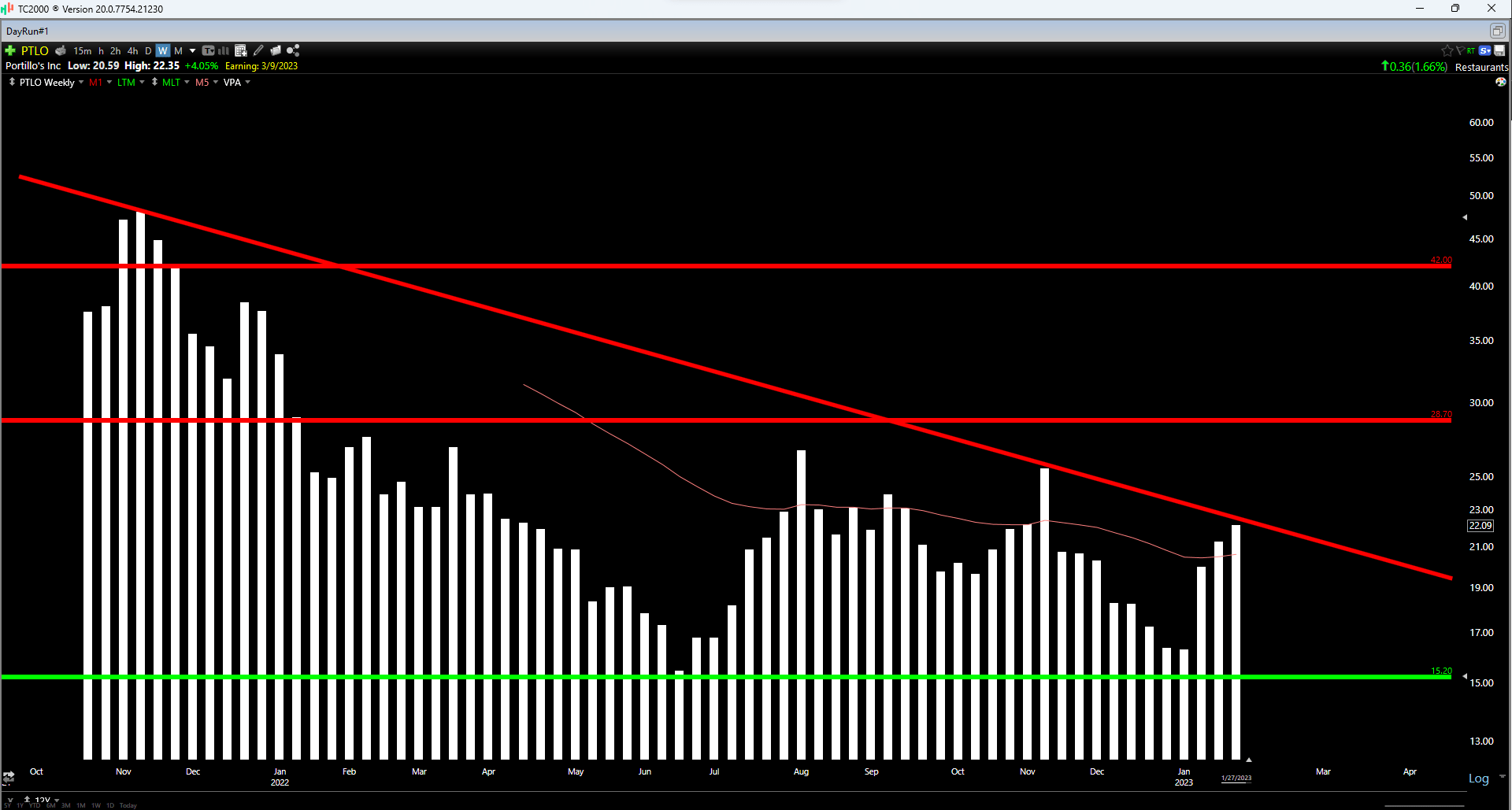

Just over six months ago, I wrote on Portillo's Inc. ( PTLO ), noting that there was no reason to chase the stock above US$22.00 with no margin of safety present, and with the stock running right into downtrend line resistance at the US$22.20 level. The unpalatable valuation stemmed from the stock trading at over 19.0x EV/EBITDA, a premium to more established brands generating significant free cash flow like Restaurant Brands International ( QSR ).

Since then, Portillo's has massively underperformed its peer group, sliding ~30% vs. a ~6% decline in the AdvisorShares Restaurant ETF ( EATZ ). On a positive note, the stock is getting closer to support, suggesting it could get a bounce short term, but from a valuation standpoint, it's tough to make a case for a long-term bottom in the stock just yet.

{kind=link}

Recent Results & Q3 Outlook

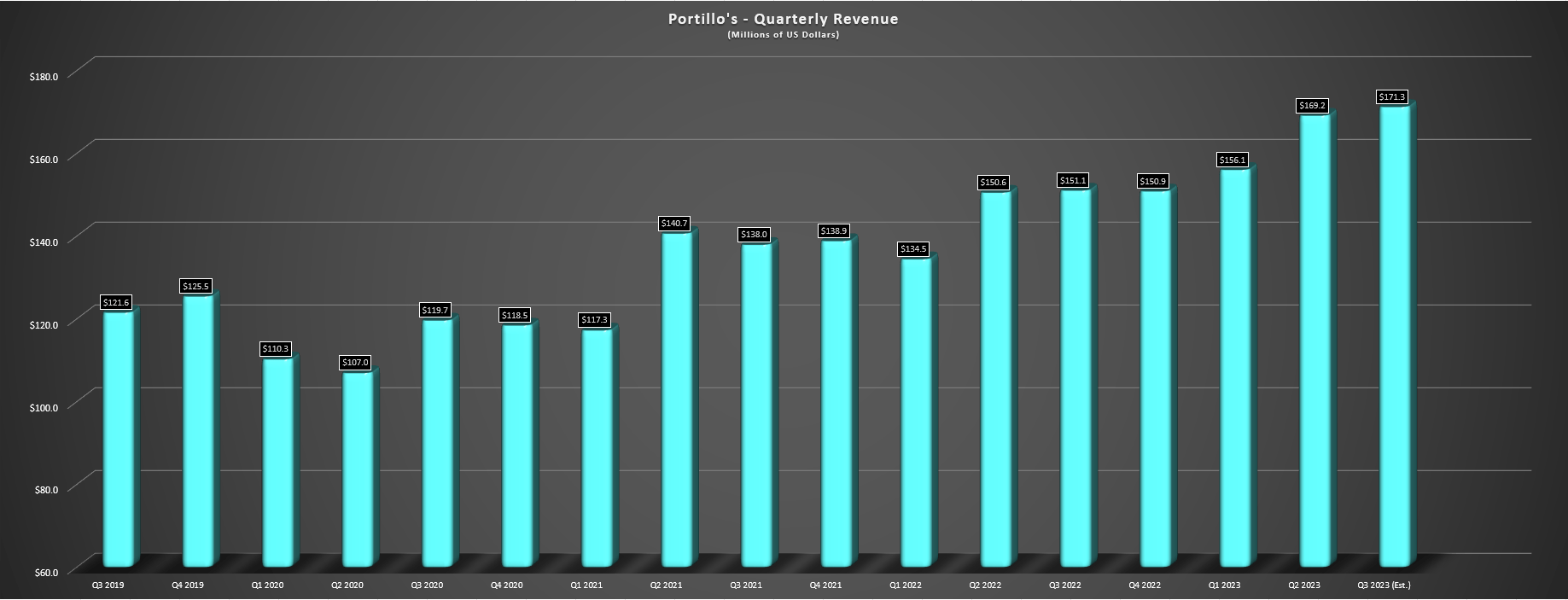

Portillo's released its Q2 results in early August, reporting a 12% increase in quarterly revenue to a new record of $169.2 million on the back of 5.9% same-restaurant sales growth and new restaurant openings. While this represented a decent same-restaurant sales figure, Portillo's did benefit from being up against relatively easy comps in Q2 2022 (1.9% growth), and it also benefited from two pricing increases year-to-date of ~2.0% in January and ~3.0% in May, with a partial benefit from the latter in the Q2 results. And digging into the numbers a little closer, the average check may have been up 7.1%, which benefited from pricing of 9.9% with a negative offset from product mix, but transactions were down 1.2% year-over-year, despite lapping a 5.6% transaction decline in Q2 2022. Overall, these results were a little below my expectations and mixed, though the company did note that it expected to see some cannibalization of sales from recently opened restaurants.

Portillo's - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

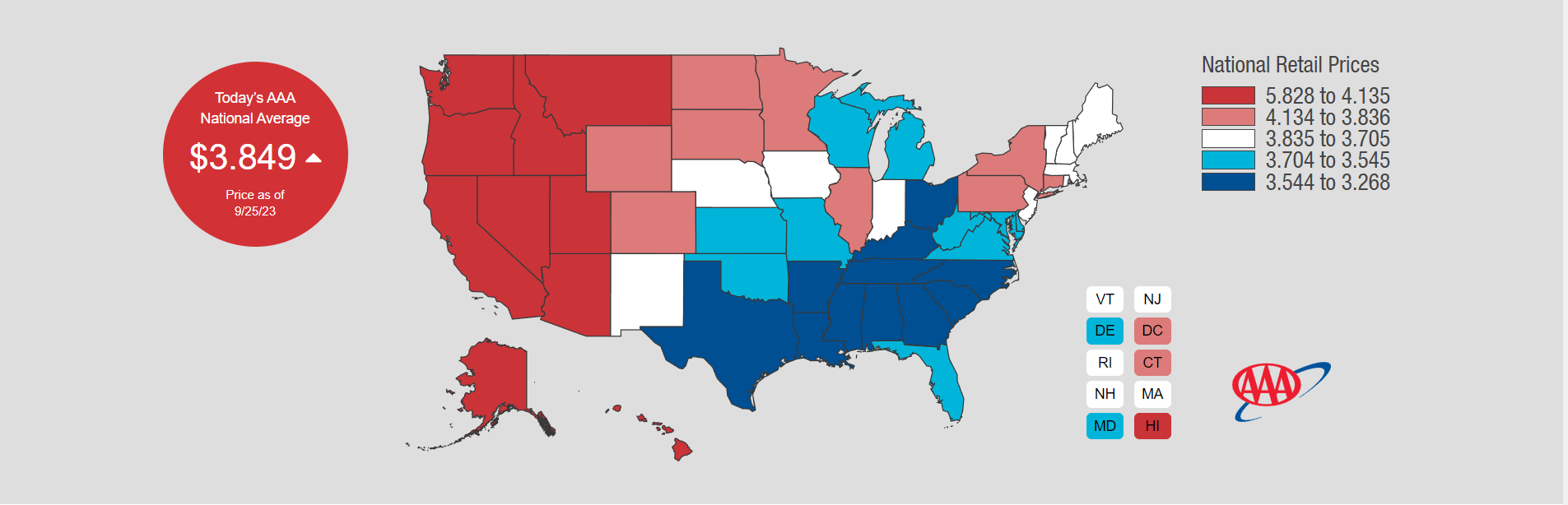

Looking at the chart above, Q3 revenue estimates are sitting at ~$171.0 million, pointing to ~13% growth year-over-year, which would translate to a slight acceleration in sales growth sequentially. And while it's possible that Portillo's could meet these estimates in Q3, there looks to be some risk to the Q4 results, and it's possible that commentary may not be as positive as some investors are hoping. This is because the industry is now facing a new headwind from rising gas prices ($3.85/gallon up from $3.65/gallon average in Q2) that can impact dining out sentiment and pinch disposable income, even if Portillo's core markets are well below the national average.

In addition, traffic appears to be tapering off for both fast-food and casual dining industry-wide, with this confirmed by Darden Restaurants ( DRI ) in its most recent results, with its CEO Rick Cardenas stating the following:

"Overall, we think the consumers continues to be resilient, but there seems to be a little bit more selective. We are seeing a little softness versus last year with household incomes above $125,000 and that primarily affects our fine dining brands, but it does affect all of our brands....The consumer is starting to have a little bit less confidence and they're a little bit more selective. And so we're going to continue to work on what we've worked on. But I think that pricing in the industry may have caused a little bit of this, but we've been pricing well below the industry and we feel good about where our pricing position is compared to everybody else and we're just going to execute."

- Darden Q1 Conference Call .

{kind=link}

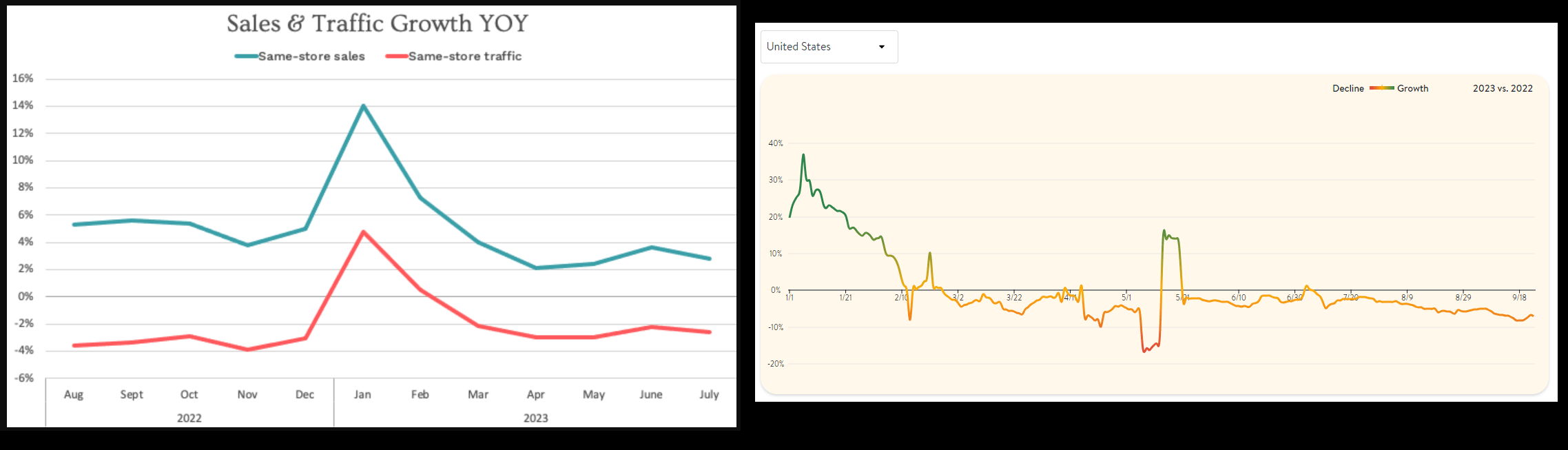

If we look at industry trends to gain a little deeper insight, Black Box Intelligence (GuestXM) noted that comparable traffic was down 2.6% in July to finish, and while quick-service was the best-performing group, it doesn't look like we've seen much improvement since then in seated diners (OpenTable) or sales and traffic growth according to GuestXM. In fact, traffic appears to have decelerated from the brief up-tick in June and gotten worse as Q3 has progressed, potentially lending itself to the rising gas prices in Q3, sticky overall inflation, and the Federal Reserve which continues to attempt to stamp out inflation but is keeping a boot on the neck of the average consumer in the process. And while Portillo's benefits from strong brand loyalty which helps from a selectivity standpoint (cited by Darden's CEO about consumers being more judicious), it's tough be bullish about September and Q4 sales for the industry looking at the below traffic trends. Plus, if consumers are tight, trading down is an additional risk even if traffic is only down slightly.

Black Box Restaurant Sales & Traffic & Open Table Change in Seated Diners - OpenTable.com, GuestXM.com

{kind=link}

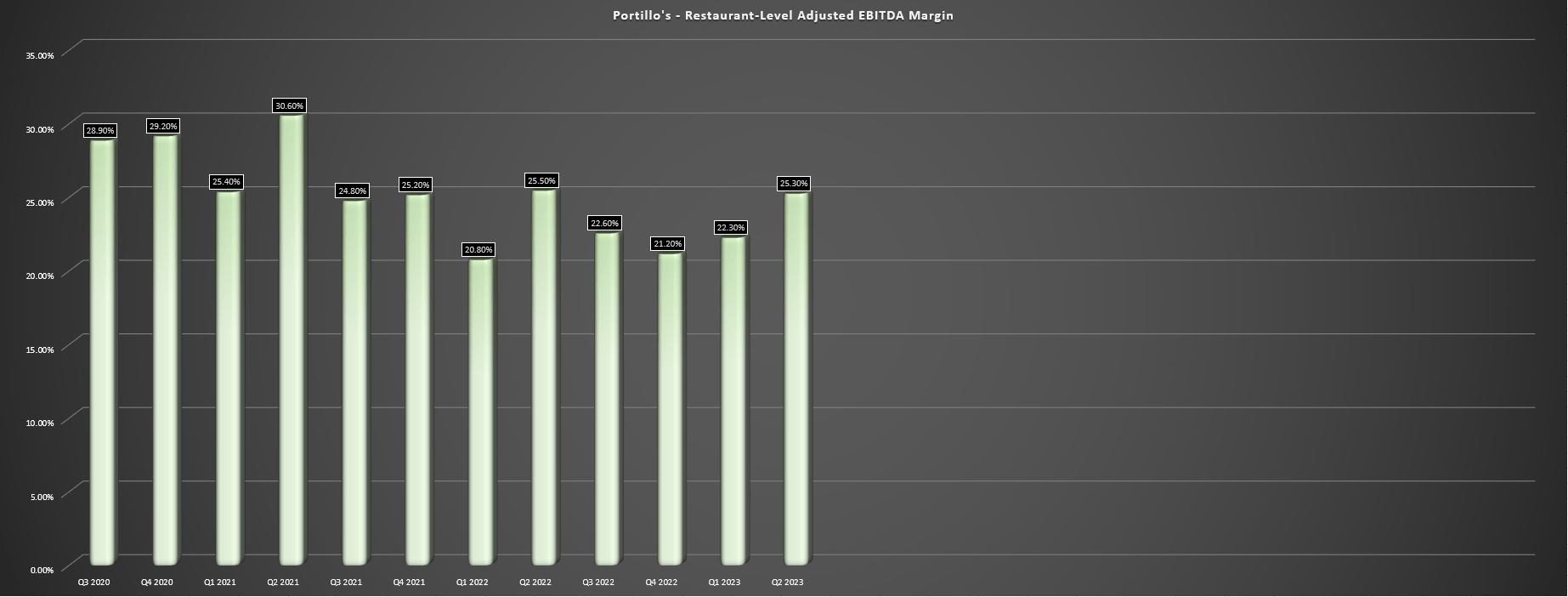

On a positive note, turnover appears to be improved industry-wide judging by company commentary, and while Portillo's commodity inflation was above my expectations in H1 at 7.1% (despite lapping 15% in H1-2022), the company does expect moderation in H2. That said, the impact of commodity inflation and labor inflation (including wage investments in team members subsequent its Q2 quarter-end) suggesting continued pressure on margins vs. previous expectations pre-IPO debut. This is especially true when operating expenses are also taking a hit due to higher utility and repair & maintenance costs, a trend consistent with other industries as well. And as we can see, the result is that restaurant-level adjusted EBITDA margins have sunk over 500 basis points on a two-year basis (25.3% vs. 30.6%), impacting the company's net income which came in at ~$6.8 million in Q2 2023 on sales of ~$170 million or just $0.12 per share.

Portillo's - Adjusted EBITDA Margins - Company Filings, Author's Chart

{kind=link}

Recent Developments

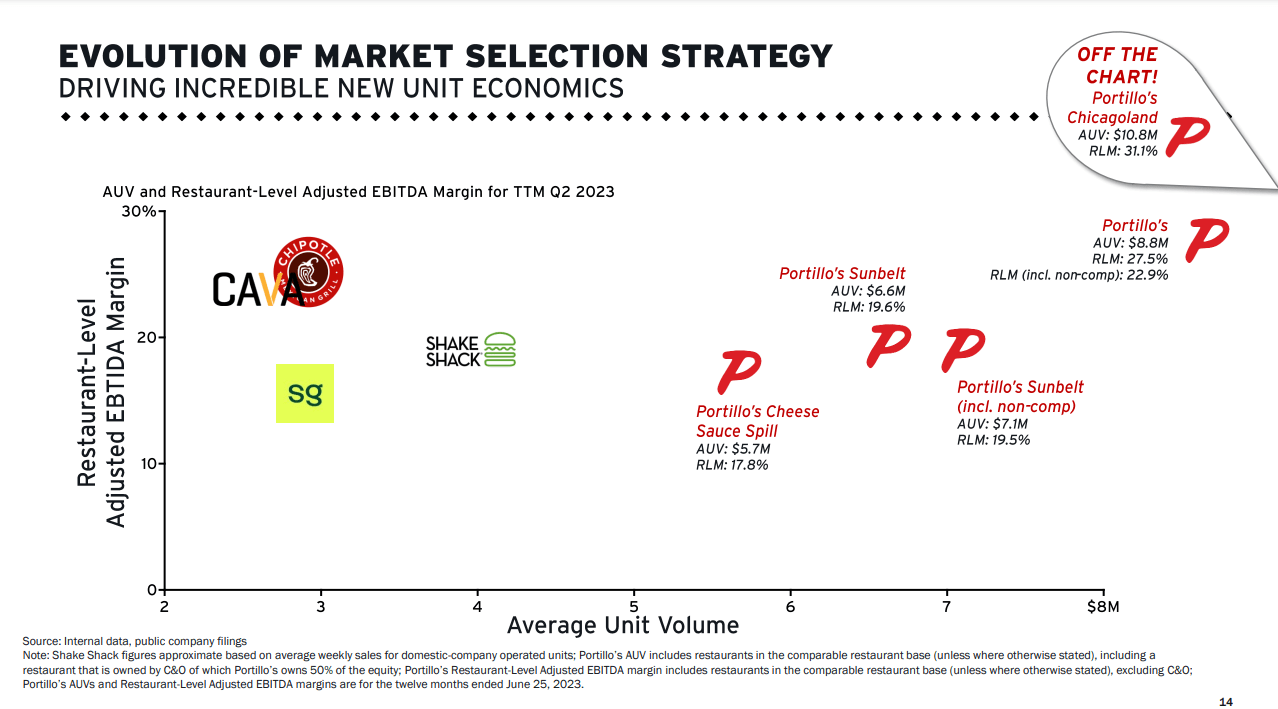

Fortunately, Portillo's has unveiled a plan to improve its unit economics despite the severe impact of inflationary pressures, and it still boasts some of the best unit economics sector-wide in the Retail Sector ( XRT ). This is evidenced by its industry-leading average unit volumes [AUVs] of ~$8.8 million across its system and impressive ~31% restaurant-level margins in Chicagoland (27.5% system-wide). However, restaurant cash-on-cash returns are expected to be improved by a lower capital cost to build each restaurant, helping to claw back some of the drag from inflationary pressures shown below. In fact, the company's new Kitchen 23' setup is expected to benefit from higher production capacity, better equipment positioning and improved service to off-premise guests with the deletion of over 3,000 square feet in space per unit, and shortening the production line by 40 feet (65 feet vs. 105 feet previously), resulting in a $100,000 decline in equipment cost alone.

{kind=link}

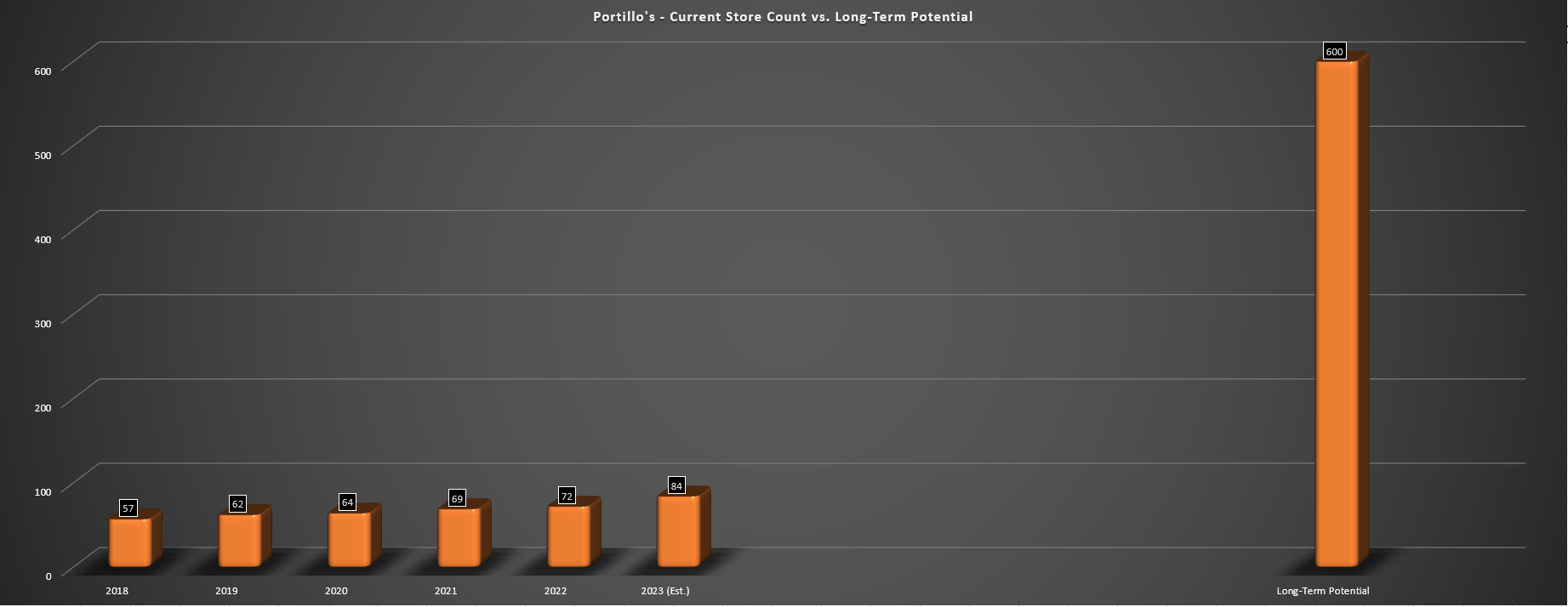

Portillo's noted in its recent presentation results that this is expected to potentially improve Year 3 cash on cash returns to 28-31% (~25% previous targeted Year 3 returns) and we could see a further decline in build costs per restaurant as part of its Restaurant of the Future concept. If successful, the result would be a ~$1.5 million decline in capital costs to build each restaurant from the 2022 class, resulting in savings of up to $18 million per annum in construction costs assuming at least 12 new restaurants added per year post-2025. Plus, from a unit growth, the company has provided an outlook of 10% unit growth in 2024, 12% in 2025 and 12-15% in 2026, placing it among the top growth stories industry-wide like Kura Sushi ( KRUS ), Dutch Bros ( BROS ) and others. Finally, Portillo's smaller boxes could lend itself to a larger system long-term, with the potential to surpass its previous outlook of 600 restaurants in the United States (new total addressable market, or TAM, is 1,700 store potential).

Portillo's - 2023 Estimated Store Count vs. Long-Term Potential - Company Filings, Company's Long-Term Outlook, Author's Chart

{kind=link}

As highlighted in the above chart, Portillo's has a busy H2 2023 with 8 new restaurants expected to be opened implied by the 84 restaurants at year-end, setting the company up for another record year in 2024. And with the combination of better cash on cash returns and steadily growing AUVs, there is certainly reason to be optimistic, with this being an example of growth that makes sense vs. other brands like Sweetgreen ( SG ) that are growing despite relatively weak unit economics.

That said, the market has not been willing to pay up for growth stories, and certainly not long-term growth stories, focused on free cash flow today instead in most cases (ex-AI). So, while Portillo's may have a bright future and the Kitchen of the Future sounds promising, it's not clear whether this will translate into share price appreciation immediately, nor is it clear if Portillo's can reverse its trend of underperformance.

Let's take a look at the valuation below to see whether investors are getting a margin of safety for this future growth:

Valuation

Based on ~73 million shares and a share price of US$15.55, Portillo's trades at a market cap of ~$1.14 billion and an enterprise value of ~$1.65 billion. This is a much more reasonable valuation for a company expected to generate ~$770 million in sales next year based on current estimates. However, given the significant expenditures for growth (new builds) and the declining margin profile of its pre-IPO figures because of inflationary pressures, Portillo's is trading at a steep valuation relative to what's available elsewhere in the market, sitting at over 60x FY2024 free cash flow estimates. And while this might seem like a reasonable multiple for a company with a double-digit unit growth rate and improving unit economics, I would argue that this is a steep price to pay for any company, especially in the current interest rate environment. In fact, I would argue that given the higher for longer outlook and recent rate hikes, a more reasonable multiple would be a maximum multiple of 25x free cash flow or 14.0x EV/EBITDA, a normalization from the regular 25x+ EV/EBITDA multiples enjoyed by growth stories in the sector over the last decade (low interest rate environment).

{kind=link}

Given this outlook and the higher for longer rhetoric by the Federal Reserve which has weighed on growth stock multiples, I think it's better to err on the side of caution, especially when it comes to the less loved small-cap sector unless a meaningful margin of safety is present. And even if we use a 16.5x EV/EBITDA multiple and ignore free cash flow multiples because of the more strained near-term free cash flow picture (significant construction expenses for a relatively small system of 80 restaurants) and FY2024 estimates, this points to a fair value for the stock of US$18.20 - 17% upside from current levels. However, I am looking for a minimum 30% discount to fair value for small-cap growth stories to ensure an adequate margin of safety. And after applying this discount, Portillo's ideal buy zone comes in at US$12.75 or lower, suggesting that the stock will either need more time to grow into its valuation to justify a long position, or break its all-time lows to enter a low-risk buy zone.

Obviously, I could be wrong on this view, and as stated previously, the stock has found itself oversold as we head into late September ahead of its expected Q3 results in early November. This suggests that the stock could enjoy a bounce and it may be a decent swing-trading opportunity, with a swing buy zone of US$14.90 if it touches this level before November.

However, from an investment standpoint , I see far more attractive bets elsewhere in the sector, with examples including Pet Valu (PTVLF) ( PET:CA ) at ~13x FY2024 earnings estimates while paying a ~1.7% dividend yield with a primarily franchisor model, leaving it with a large margin of safety relative to its historical earnings multiple of ~30, and what I believe to be a more conservative earnings multiple of 21.0. Among other sectors, B2Gold ( BTG ) stands out as attractively valued with a ~5.4% dividend yield trading at just ~6.5x FY2025 free cash flow estimates.

Summary

Portillo's has suffered like many other small-cap names in the current market, but unlike some of its peers, Portillo's continues to trade at relatively lofty valuations comparatively even if we adjust for its significant growth profile. This is because there are several names available in the small-cap space across other sectors at double-digit free cash flow yields, and while Portillo's is undoubtedly cheap relative to its long-term potential, the market is not paying up for future growth today and there's no reason to believe that setup will change on a dime.

Hence, I would not be surprised to see Portillo's Inc. stock ultimately trade lower from these levels, even after what's been a torturous ~70% correction despite its solid execution. That said, from a trading standpoint, the stock would become attractive below US$14.90 if it reaches this level before November, so I may consider the stock as a swing trading opportunity if this weakness persists.

For further details see:

Portillo's: Patience Required