FE - Portland General Electric: Q2 Results Show Stability And Risks From Renewables

2023-08-04 13:54:26 ET

Summary

- Portland General Electric Company's Q2 2023 earnings beat revenue expectations but missed on earnings.

- The company's revenues showed stability with a 9.64% increase year-over-year.

- Rising electric demand from semiconductor manufacturers and technology firms may contribute to future growth prospects.

- The company's expenses skyrocketed due to insufficient generation from its renewable infrastructure, resulting in a significant drag on earnings.

- The 4.06% yield appears secure and the stock is fairly valued today.

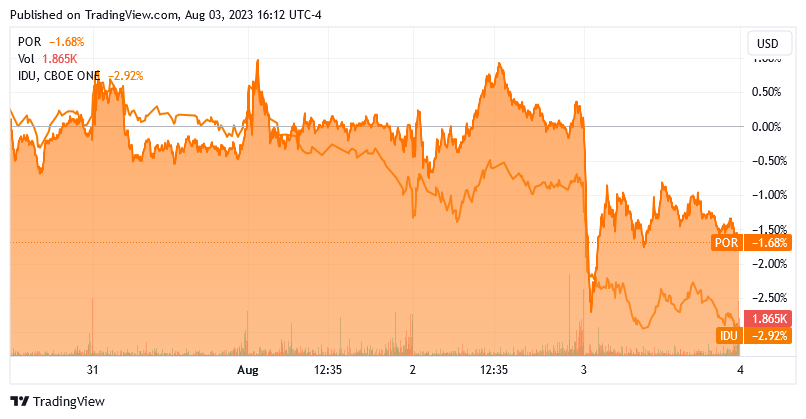

On Thursday, July 27, 2023, Oregon-based regulated electric utility Portland General Electric Company ( POR ) announced its second-quarter 2023 earnings results. At first glance, these results were mixed, as the company managed to beat the revenue expectations of its analysts but missed on earnings. For its part, the market appeared to be lukewarm on these results as Portland General Electric has traded down over the past five days but it outperformed the U.S. Utility Index ( IDU ):

{kind=link}

As I have mentioned in various previous articles, one of the defining characteristics of utilities like Portland General Electric is that they exhibit remarkably stable cash flows over time. This is regardless of any changes in the macroeconomic environment, which has made these stocks very popular among retirees and other people that want a conservative investment that does not require much attention. Portland General Electric's second-quarter results fit pretty well with this thesis overall as the company managed to deliver a moderate amount of year-over-year revenue growth. The results were hardly perfect though, as both net income and operating cash flow were down relative to the prior-year quarter. Overall though, the company looks like a reasonable way to earn a 3.98% dividend yield today along with the moderate growth that we typically expect from stocks in this industry.

Earnings Results Analysis

As regular readers are no doubt well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as provide a framework for the resultant analysis. Therefore, here are the highlights from Portland General Electric Company's second-quarter 2023 earnings results:

- Portland General Electric Company brought in total revenues of $648.0 million in the second quarter of 2023. This represents a 9.64% increase over the $591.0 million that the company brought in during the prior-year quarter.

- The company reported an operating income of $83.0 million in the reporting period. This compares rather unfavorably to the $113.0 million operating income that the company reported in the year-ago quarter.

- Portland General Electric Company continued to advance on its "green power" agenda, which included purchasing a 75-megawatt battery storage system.

- The company reported an operating cash flow of $182.0 million during the current quarter. This represents a 9.90% decline over the $202.0 million that the company reported in the equivalent quarter of last year.

- Portland General Electric Company reported a net income of $39.0 million in the second quarter of 2023. This represents a 39.06% decrease over the $64.0 million that the company earned in the second quarter of 2022.

In the introduction to this article, I stated that utility companies generally enjoy fairly stable financial performance over time. We can see this to a certain degree in Portland General Electric's second-quarter earnings results. In particular, the company's revenues showed reasonable stability as they increased by 9.64% year-over-year. This is not a one-off occurrence, however. In fact, as we can see here, Portland General Electric's revenue tends to enjoy remarkable stability over time:

{kind=link}

As we can clearly see, the company's revenues pretty consistently come in between $550 million and $750 million during any given quarter. This is in spite of the fact that the overall economy changed a lot during the period. After all, in December 2020, the economy was still reeling from the effects of the COVID-19 shutdowns and inflation was relatively low. This changed a lot in 2021 when inflation began to show itself and in 2022 when the Federal Reserve started raising interest rates to slow the economy and combat inflation.

The reason why Portland General Electric Company's finances tend to remain relatively stable over time is that the company provides a product that is generally considered to be a necessity for our modern way of life. After all, just about everybody has electric service to their homes and businesses. For the most part, people expect that any indoor location they visit will have electricity for lights, charging cellular telephones, and many other purposes. As such, most people will prioritize paying their electric bills ahead of making discretionary expenses during periods in which money gets tight. As I mentioned in a recent blog post , money has gotten very tight for many people who are struggling to feed themselves amidst the highest inflation that the nation has seen in decades. As such, we can logically expect that discretionary spending will take a nosedive at some point in the near future. However, a company like Portland General Electric should experience minimal impact from this. That is a characteristic of a company that we very much want to own during such a scenario.

Unfortunately, we can see that Portland General Electric's profits and cash flows did not hold up nearly as well as its revenues did over the past year. This is disappointing, but management provided a reason for this in the earnings press release :

Total revenues increased, driven by higher demand from digital and semiconductor customers. Purchased power and fuel expense increased primarily due to less favorable power market conditions driven by substantial changes in regional hydro conditions. Operating and administrative expenses increased due to higher grid maintenance and resiliency costs and higher generation maintenance costs driven by significantly higher thermal operating rates. Other income increased due to gains on non-qualified benefit plan assets from improved market performance.

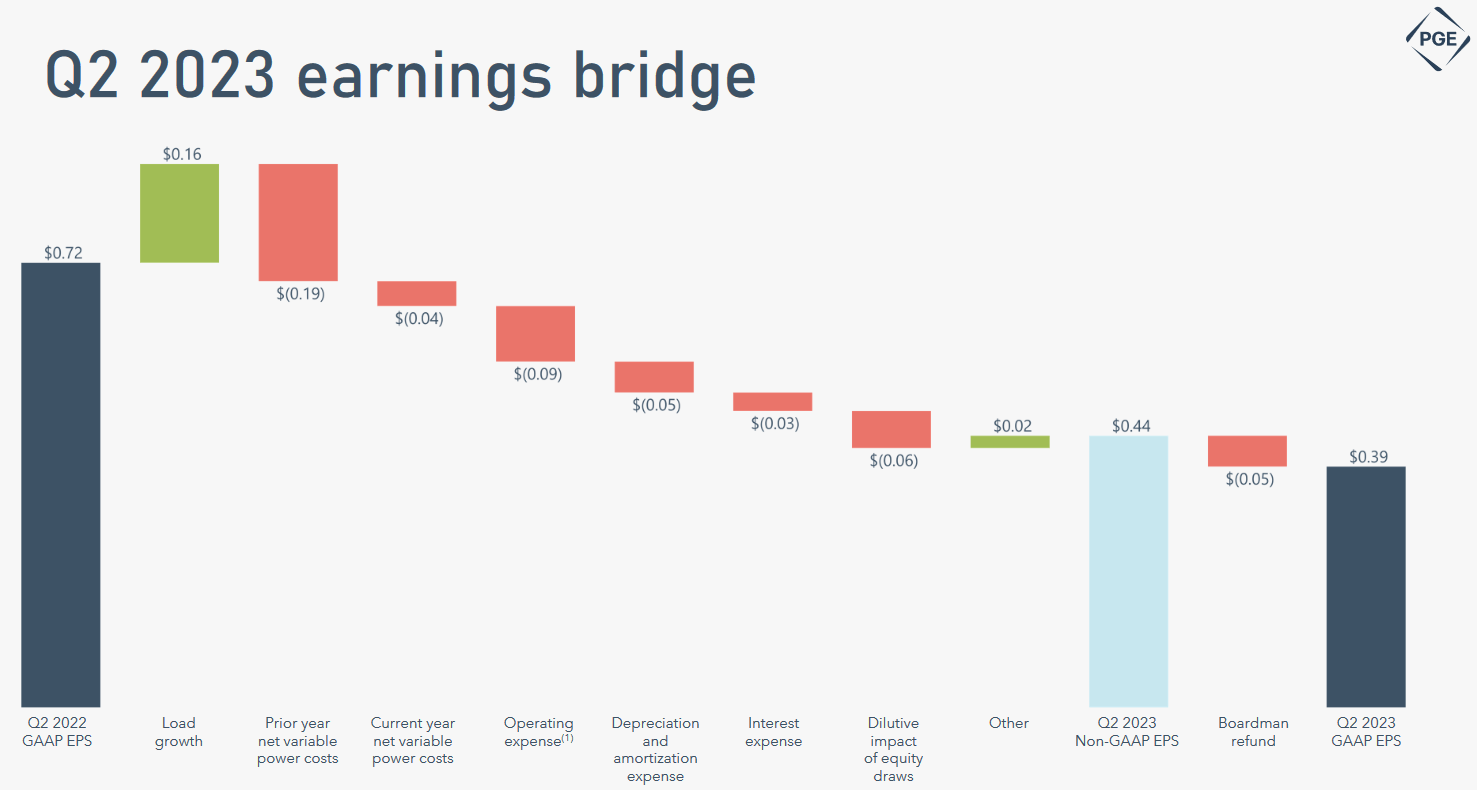

The one big thing that we immediately note here is that Portland General Electric had to purchase power from other utilities because its own hydroelectric dams were unable to meet the demands of its customers. This was, without a doubt, the single largest impactor on the company's year-over-year earnings:

{kind=link}

Basically, the incremental costs of this item totaled $0.19 per share, outstripping the positive impact of higher electric demand. This is a problem that we could begin to see more frequently across the utility sector as renewable energy generation accounts for a greater and greater proportion of the energy mix. This is because renewable power is unreliable, which can easily result in a utility being forced to buy electricity from other generation companies if its own generation plants are unable to supply the immediate demands of its customers.

In this case, though, Portland General Electric's problem came from its hydroelectric plants being unable to generate sufficient power to satisfy customer demands. Hydroelectric dams are generally among the most reliable sources of renewable energy generation, but as we saw this quarter, even they sometimes end up short. Hopefully, this proves to be a one-off occurrence, but as of right now, management has provided no information about how well its internal generation operations have performed relative to electricity demand in the third quarter.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. We like to see a company that we are invested in grow and prosper with the passage of time. Fortunately, Portland General Electric is well-positioned to accomplish exactly that.

As noted above, the company has been experiencing rising electric demand from semiconductor manufacturers and other technology firms that have come into the area. This may be a direct result of the corporate exodus out of California's Silicon Valley. As Forbes notes , numerous companies have moved their headquarters or other operations out of California over the past three years, including Tesla ( TSLA ), Apple ( AAPL ), and Oracle ( ORCL ). The Forbes article specifically states that Oregon has been one of the destination states for this exodus, and Portland is by far the largest city in Oregon. It is, therefore, quite possible that some of these companies have opted to relocate to an area served by Portland General Electric. The company's net income increased by $0.16 per share compared to last year due to rising demand for electricity, which would have resulted in year-over-year earnings per share growth were it not for the already discussed problems with the company's hydropower generation facilities.

Unfortunately, Oregon's population as a whole appears to be shrinking. Last year, the state's population declined by 0.38%, and it is down by roughly 100,000 people since peaking in 2021:

{kind=link}

As we can see above, it is currently projected that Oregon's population will continue to decline until at least 2029. Fortunately, the projected decline is not particularly rapid as the state is still projected to have a population of around 4.1 million by the end of the decade.

This population decline could prove to be a drag on Portland General Electric's growth going forward. After all, a declining population in the company's service territory means that it would have fewer customers paying their monthly electric bills as time goes on. However, the above population projections are for the entire state of Oregon and Portland General Electric's service territory does not cover the entire state. As such, the fact that the state's population is declining does not mean that the company's customer count is declining. Portland General Electric unfortunately did not provide its customer count in its earnings report, so it is uncertain at this time exactly what the demographic trends of the company's service territory look like.

Fortunately for our purposes, Portland General Electric Company has another method that it can use to grow its earnings per share regardless of changes in its customer levels. This is by growing its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the prices that it charges its customers in order to earn that specified rate of return.

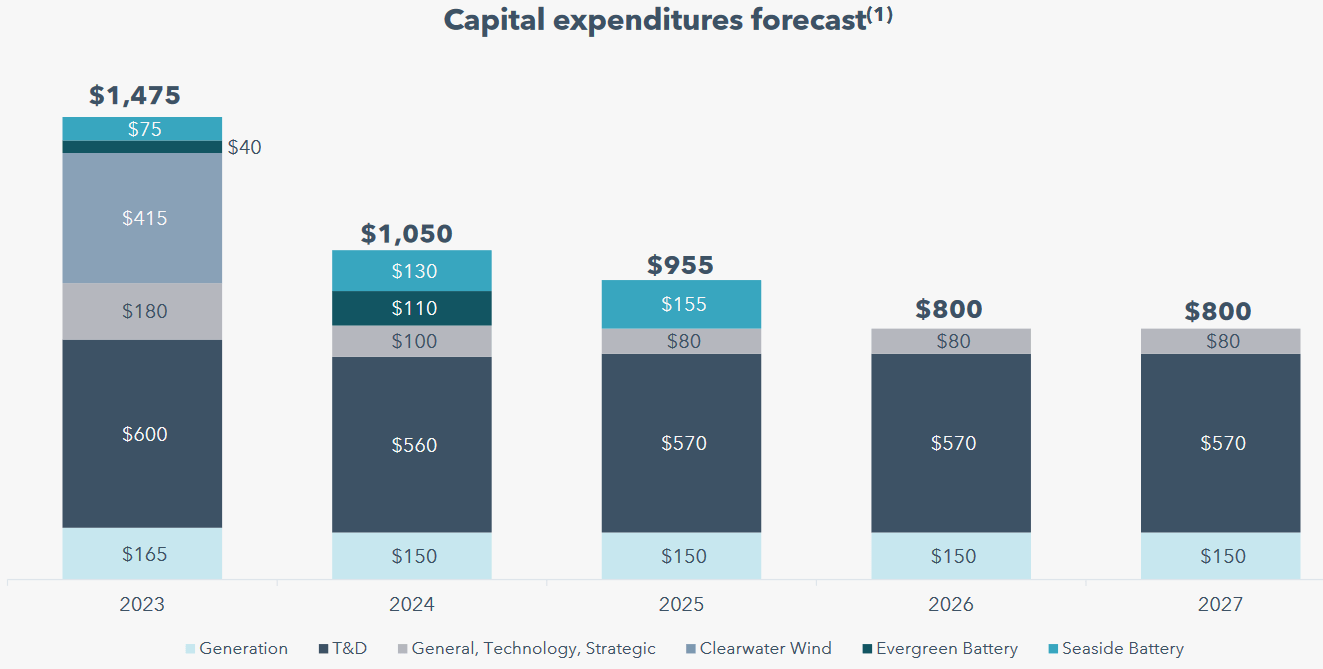

The usual way for a utility company to grow its rate base is by investing money into upgrading, modernizing, and possibly even expanding its utility-grade infrastructure. Portland General Electric Company is planning to do exactly this as the company presented a $5.080 billion capital spending plan for the 2023 to 2027 period during its earnings conference call:

{kind=link}

The purpose of this is to, of course, increase its rate base. Portland General Electric Company unfortunately did not provide any estimates as to the effect that this program will have on its rate base. The one curious thing that I notice here, though, is that the company's capital expenditures are very heavily front-loaded, whereas most utility companies increase their spending over time.

This one is doing the opposite, which could mean that it either boosts its 2026 and 2027 spending well beyond the current $800 million estimate or its growth slows severely as time passes. Management's guidance is for this plan to grow its earnings per share at a 5% to 7% compound annual growth rate over the period. When we combine this with the current 4.06% dividend yield, we get an estimated total average annual return of 9% to 11% over the projection period, which is very reasonable for a conservative utility company.

The company has already begun using its rate base growth to push for rate hikes, as the company filed a rate case back in February that would result in an approximate 14% price increase for its customers. I would almost laugh and say that this shows that the inflationary trend in the economy has certainly not abated yet, but that is more appropriate for other articles. This rate hike, if approved by Oregon regulators, should naturally boost the company's revenues and net income next year.

Financial Considerations

It is always important to investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. After all, very few companies have sufficient cash to completely pay off their debts as they mature. This can cause a company's interest expenses to increase following the rollover, which is almost a certainty today considering that interest rates are at the highest levels that we have seen since 2007. In addition to interest-rate risk, a company must make regular payments on its debts if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push it into financial distress if it has too much debt. Although electric utilities like Portland General Electric Company usually have very stable cash flows, bankruptcies have occurred in the sector so this is certainly a risk that we should not ignore.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity can cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of June 30, 2023, Portland General Electric Company had a net debt of $3.925 billion compared to $3.200 billion in shareholders' equity. This gives the company a net debt-to-equity ratio of 1.23 today. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity |

| Portland General Electric Company |

| 1.23 |

| DTE Energy ( DTE ) |

| 1.89 |

| FirstEnergy Corporation ( FE ) |

| 2.17 |

| CMS Energy ( CMS ) |

| 1.91 |

| Public Service Enterprise Group ( PEG ) |

| 1.28 |

As we can very clearly see, Portland General Electric Company appears to be quite conservatively financed relative to most of its peers. This is a good situation to be in as it should represent a relatively low risk for investors in terms of the company's debt load. After all, this low ratio tells us that the company is not overly dependent on debt to finance its operations. As such, there does not appear to be anything for us to worry about here.

Dividend Analysis

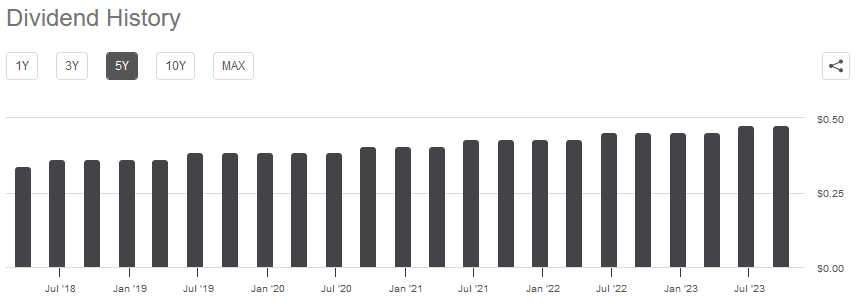

One of the biggest reasons why investors purchase utility stocks is because they usually have higher yields than many other things in the market. This is due to the fact that utilities in general are very low-growth companies so the market will not reward them with the capital gains that we see in long-duration sectors, such as technology. As such, utilities will pay out a large proportion of their cash flows to their investors in order to provide an investment return. In addition, since these are low-growth companies, the market does not usually assign high earnings multiples so the dividend ends up being a significant percentage of the stock price. Portland General Electric Company is no exception to this as the stock yields 4.06% at the current price. In addition to its fairly high yield, the company has a long history of increasing its dividend on an annual basis:

{kind=link}

The fact that Portland General Electric Company increases its dividend on an annual basis is something that is very nice to see during inflationary periods, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can buy with the dividend that the company pays out. This can make it feel as though an investor is getting poorer and poorer with the passage of time, which is particularly problematic for retirees and other individuals that are dependent on their portfolios to pay their bills and finance their lifestyles. The fact that Portland General Electric Company raises its dividend every year helps to offset this effect and ensures that the dividend maintains its purchasing power over time.

As is always the case though, it is important that we make sure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we judge a company's ability to pay its dividends is by looking at its free cash flow. The free cash flow is the money that was generated by a company's ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is, therefore, the money that is available to do tasks that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend. During the second quarter of 2023, Portland General Electric reported a negative levered free cash flow of $132.6 million. That is obviously nowhere near enough money to pay any dividends, let alone the $44.0 million that the company actually paid out to its shareholders during the quarter. At first glance, this is likely to be concerning as the company did not earn sufficient free cash flow to cover its dividends.

However, it is not uncommon for a utility to finance its capital expenditures through the issuance of equity and debt. It will then pay its dividends out of its operating cash flow. This is done because of the incredibly high costs involved of constructing and maintaining utility-grade infrastructure over a wide geographic area. If the company were to attempt to finance all of these things internally, it would have to charge prices that are unaffordable by customers in order to provide any sort of investment return.

During the second quarter of 2023, Portland General Electric Company reported an operating cash flow of $182.0 million, which was easily enough to cover the $44.0 million that was paid out in dividends with a substantial amount of money left over for other purposes. Thus, the company's dividend is probably sustainable and we should not need to worry too much about a cut in the near future.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like Portland General Electric, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa.

However, there are very few companies that trade for such low multiples in today's very expensive market. As such, the best way to use this ratio today is to compare Portland General Electric's valuation to its peers in order to determine which company offers the most attractive relative valuation.

According to Zacks Investment Research , Portland General Electric Company will grow its earnings per share at a 6.02% rate over the next three to five years. This is in line with the growth rate that we calculated earlier based on the company's rate base growth so it seems pretty solid. This gives the company a price-to-earnings growth ratio of 2.85 at the current price. Here is how that compares to the company's peers:

| Company |

| PEG Ratio |

| Portland General Electric Company |

| 2.85 |

| DTE Energy |

| 2.95 |

| FirstEnergy Corporation |

| 2.28 |

| CMS Energy |

| 2.41 |

| Public Service Enterprise Group |

| 3.66 |

This is disappointing, to say the least. As we can clearly see, Portland General Electric Company has a higher relative valuation that some of its peers. It is not considerably overvalued though, as it is the median stock in our comparison here. As such, we can conclude that the stock is fairly valued compared to its peers but it does not appear to be a value play.

Conclusion

In conclusion, Portland General Electric Company's latest results showed the stability that we have come to expect from a company like this, but the firm was clearly adversely impacted by the weather not cooperating with its generation facilities. This is something that will probably become a more common problem across the sector as the use of renewables becomes commonplace and utilities become more dependent on unreliable sources of power. The company is positioned to deliver reasonably steady growth and total return though, and its 4.06% dividend yield appears secure. The stock is also not too expensive today.

For further details see:

Portland General Electric: Q2 Results Show Stability And Risks From Renewables