PKX - POSCO: Favorable 2023 Outlook

2023-04-04 12:18:49 ET

Summary

- POSCO Holdings' steel business should witness a substantial increase in its 2023 operating earnings, thanks to price hikes, demand recovery, and the resumption of operations at its Pohang steel mill.

- PKX's key non-steel businesses such as POSCO Chemical, POSCO International, and its recycling business are also expected to perform well this year.

- I make no changes to my existing Buy rating for POSCO Holdings, as I don't think that the market has sufficiently rewarded PKX's shares for its 2023 growth prospects.

Elevator Pitch

I continue to rate POSCO Holdings Inc.'s ( PKX ) [005490:KS] stock as a Buy.

I previously raised my investment rating for POSCO Holdings to a Buy with my earlier January 19, 2023 update for the company in consideration of potential re-rating catalysts.

My current article focuses on PKX's 2023 business outlook and valuations. I estimate that POSCO Holdings' bottom line could potentially increase by +20% in the current year. Despite the favorable bottom line outlook, the market currently values PKX at a single-digit forward P/E ratio. I am of the view that POSCO Holdings' stock is undervalued and decide to retain my Buy rating for the stock.

Steel Business Is Expected To Deliver Robust Operating Earnings Growth This Year

At the company's most recent Q4 2022 earnings briefing (call transcript sourced from S&P Capital IQ ), POSCO Holdings guided for a +31% growth in operating income from KRW2,295 billion last year to KRW3 trillion for full year fiscal 2023. In my view, PKX's operating profit target for its steel business is realistic and achievable, taking into account multiple drivers.

Firstly, POSCO Holdings' key Pohang steel mill has already resumed operations since late February 2023 . In my prior January 19, 2023 write-up, I noted that "the suspension of production at its steel mill in Pohang resulting from typhoons" in 2H 2022 would have hurt the performance of the company's steel business. Specifically, PKX disclosed in its Q4 2022 results presentation slides that its steel business' operating income for FY 2022 took a KRW1.34 trillion hit from production disruptions at the Pohang steel mill. As such, the steel business is likely to see a strong operating earnings turnaround in 2023 with its Pohang steel mill back in operation.

Secondly, PKX's steel business will benefit from an increase in steel demand this year. The Organization For Economic Co-operation And Development or OECD had earlier forecasted in December 2022 that worldwide steel consumption will reverse from a decline last year to achieve positive growth in the current year. OECD's steel demand projections are consistent with POSCO Holdings' management comments at the fourth quarter results call. PKX had highlighted its expectations that "the steel market is expected to recover" in 2H 2023, with the "easing of COVID-19" restrictions and the introduction of "stimulus packages" in China being cited as a key demand driver.

Thirdly, price hikes will be supportive of an improvement in the profitability of POSCO Holdings' steel business for 2023. According to a March 15, 2023 commentary published by steel company Yieh Corp., PKX had increased the selling price of its hot-rolled coil or HRC sold in the Korean market by +KRW200,000 per metric ton in 2023 year-to-date. POSCO Holdings had stressed at the company's Q4 2022 results briefing that steelmakers, including its steel business, have the ability to "increase the prices" notwithstanding "the global downturn" which is indicative of pricing power.

Non-Steel Businesses' Prospects For 2023 Are Good

I have a positive view of the growth prospects for PKX's key non-steel businesses.

With regard to POSCO Chemical, 2022 was an inflection point for this business segment. POSCO Chemical saw the sales of new sub-segments, cathode materials and anode materials (59% of 2022 top line), surpass the revenue contributed by the legacy refractories and quicklime/chemical sub-segments for the first time last year. Looking forward, PKX emphasized at the most recent quarterly earnings call that it will "aggressively pursue investments in cathodes and other different battery-grade materials" in 2023. The expected increase in cathode and anode production capacity should help to drive significant operating profit growth for POSCO Chemical in the current year.

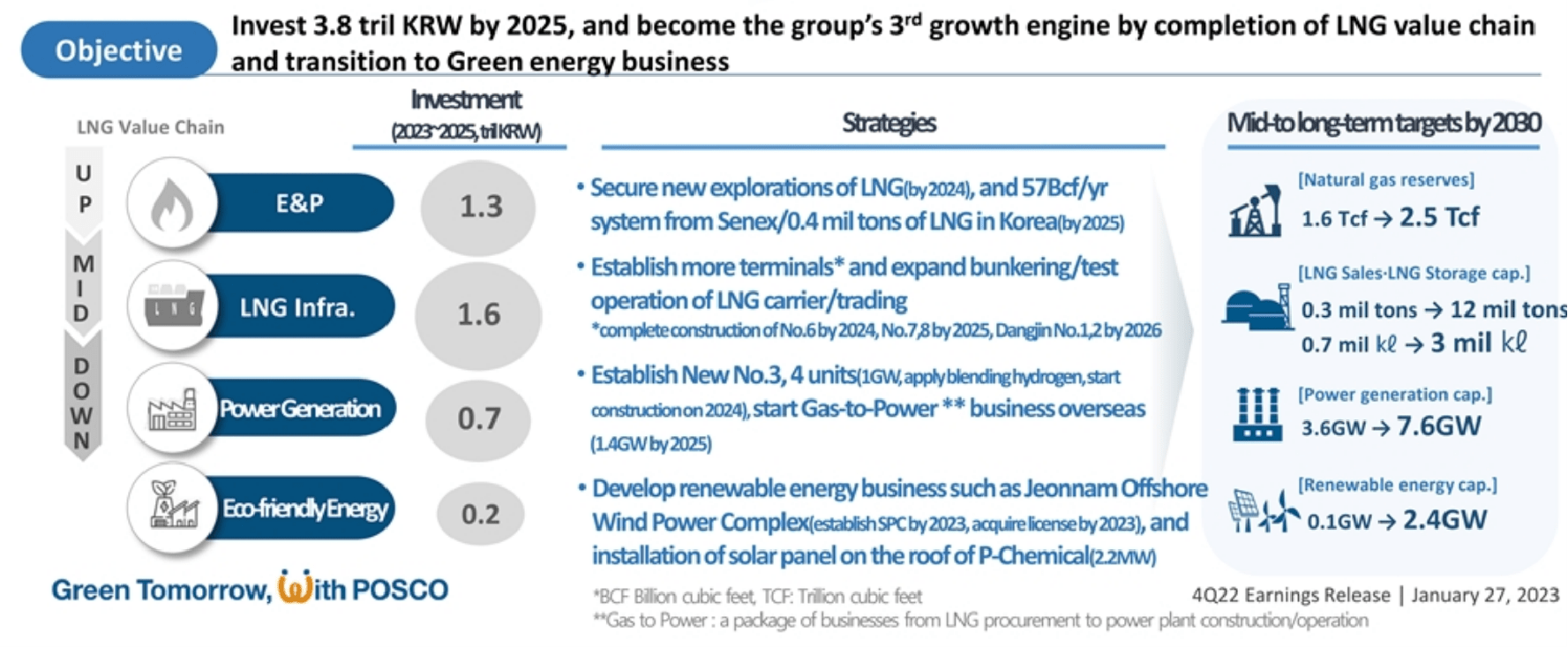

In relation to POSCO International and POSCO Energy, I touched on the conclusion of the merger between the two businesses in my January 19, 2023 article. PKX outlined its expectations of the new POSCO International (merged entity) achieving a double-digit percentage increase in 2023 operating income at its Q4 investor briefing. The company's specific plans for expanding the new POSCO International's business operations by becoming fully integrated across the Liquefied Natural Gas or LNG value chain are detailed in the chart below.

POSCO International's Investments And Growth Targets

PKX's Q4 2022 Earnings Presentation

{kind=link}

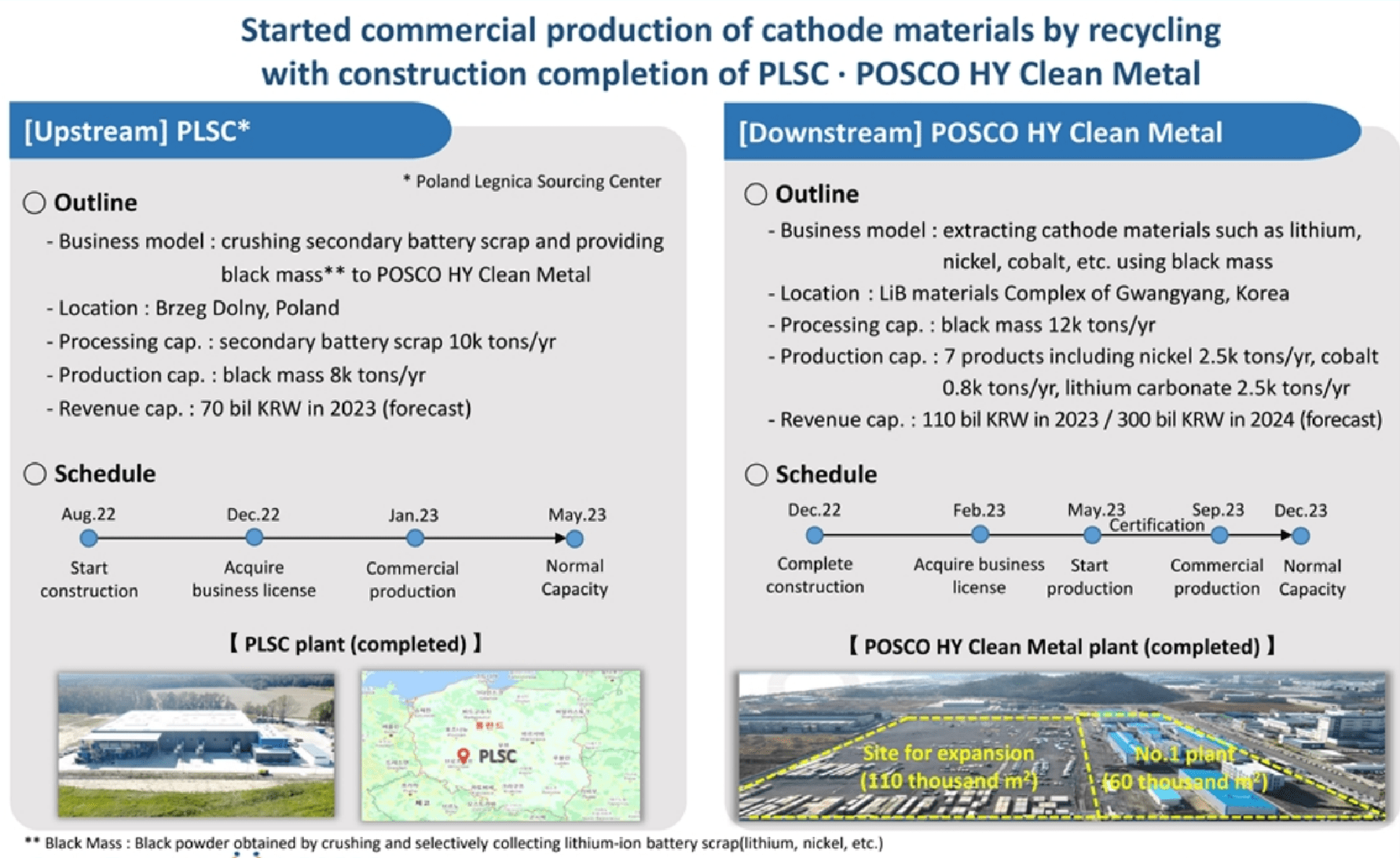

Separately, POSCO Holdings' recycling business will witness a meaningful increase in revenue contribution this year with two of its recycling plants commencing production. Specifically, PKX's HY Clean Metal and PLSC recycling plants are expected to generate sales of KRW110 billion and KRW70 billion, respectively in 2023. Going forward, the expansion of POSCO Holdings' recycling business will allow it to capitalize on the growth in demand for recycled materials as countries around the world become more focused on sustainability.

Expansion Of POSCO Holdings' Recycling Business In 2023

PKX's Q4 2022 Earnings Presentation

{kind=link}

Closing Thoughts

Based on the analysis of POSCO Holdings' steel and non-steel businesses presented above, I expect PKX's net profit to grow by around +20% from KRW3.6 trillion in FY 2022 to KRW4.2 trillion for FY 2023. The expected earnings recovery for POSCO Holdings isn't fully reflected in its stock price, with the company's shares trading at a normalized forward P/E multiple of around 6 times . Taking into account the misalignment between the stock's attractive valuations and the company's earnings growth outlook, I deem PKX's shares to be worthy of a Buy rating.

For further details see:

POSCO: Favorable 2023 Outlook