PKX - POSCO: South Korean Steel Giant Undergoing Period Of Transformation

2023-04-05 02:23:31 ET

Summary

- Posco is South Korea's US $22B flagship steel producer borne from state fund economic revitalization plans in the late 60s.

- Since then, the company has undergone a period of transformation extending its reach into battery minerals and decarbonization.

- Under the present CEO, the conglomerate is likely to evolve with new technologies becoming a more meaningful part of the income statement.

Company Introduction

If ever there was a cultural, social, and economic transformation story, it would have to be one of POSCO ( PKX ). The rags-to-riches South Korean behemoth, borne out of a late 60s government investment program aimed at providing the steel required to build the economy, is rapidly transforming itself to a sprawling conglomerate with goals of righting society.

Once known as the Pohang Iron and Steel Company, the venture has been one of the driving forces behind South Korea's swift industrialization and economic ascendency.

At its heart, the $22B Korean steel maker manufactures and markets iron and steel rolled products, offering hot and cold rolled steel, plates, rods, stainless steel, and titanium. POSCO serves a wide range of customers in automotive, construction, shipbuilding, energy, consumer durables, and capital equipment.

{kind=link}

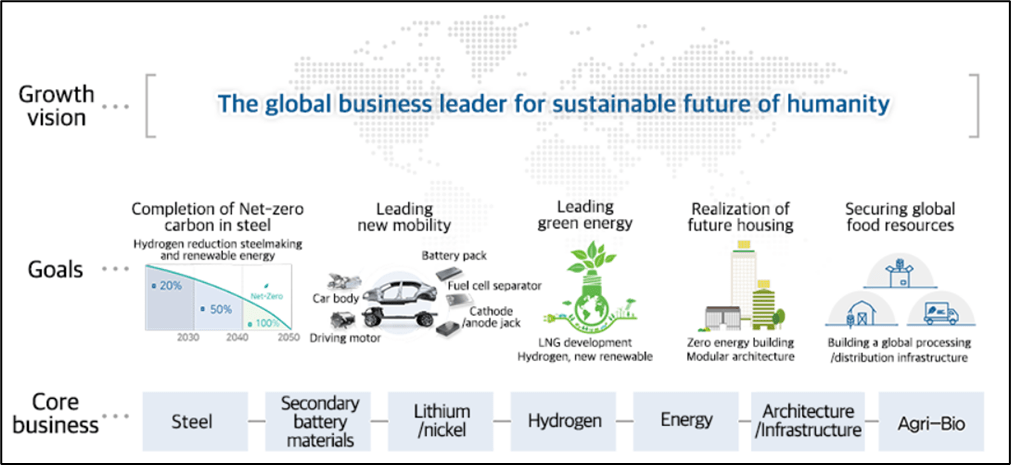

POSCO 's diversification drive is seeing the firm expand into sustainability and take a paternalistic approach to engagement with society.

Under Jeong-Woo Choi, recently nominated CEO of the year by S&P Global , the company registers annual sales of ~ US $67B, trades at 9x forward and generated almost $7B in EBITDA FY 2022. It is the 6th largest steel producer in the world, churning out almost 43 million tons in 2021.

At ZMK Capital, we remain bullish on POSCO's prospects despite a challenging macro environment in 2023. While the company trades at a premium (9x) compared to national peers such as Hyundai Steel Company (5x) and Daehan Steel Company (3.9x), we believe the expansion into newer business lines, particularly battery minerals and process chemistry, justify current valuation.

Let us find out more.

{kind=link}

Under Jeong-Woo Choi, the South Korean steel maker has expanded into new business lines with a focus on renewable energy, sustainability, and decarbonization.

Global Steel Market

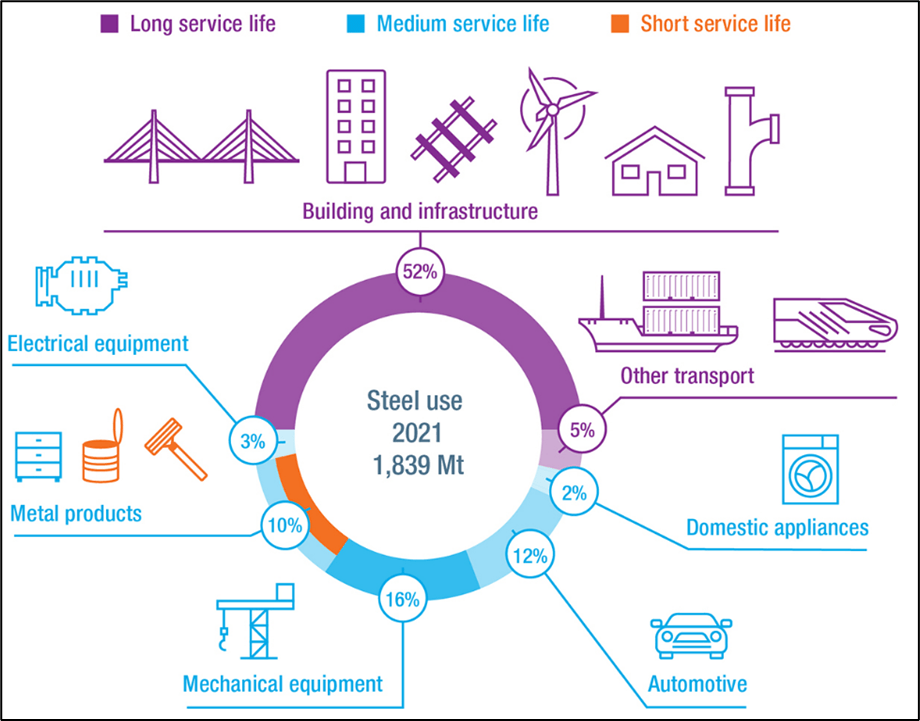

While POSCO was originally founded as a domestic steel producer, export markets and macro-economic forces increasingly factor into the firm's financial performance. With most steel being dedicated to building and infrastructure (52%) a measured cooling of this sector, impacted by monetary tightening, will make itself felt in 2023 forecasts.

The steel market in the United States is likely to remain resilient as government spending programs and initiatives help support industry. Fears around demand in China and economic growth in Europe may also hit prices, further pressuring margins.

Consumption outside of China is picking up pace, principally because of economic growth in India and Southeast Asia. China's targeted reduction in steel production coupled with government stimulus, infrastructure spending programs and protectionist trade measures in other geographies will probably provide some support to prices.

European supply and demand dynamics have swiftly adjusted as the European economy felt the impact of the war in Ukraine and gradually went into decline. Competition in unprotected markets is becoming increasingly intense with margins starting to normalize following a Covid induced price boom.

All in, expect global steel markets to be mixed in 2023 with economic jitters in China, a war in Europe, and US inflationary pressures all impacting supply and demand dynamics.

{kind=link}

Most of global steel use goes toward building and infrastructure. That is meaningful because highly dependent on interest rates, government stimulus and fiscal policy.

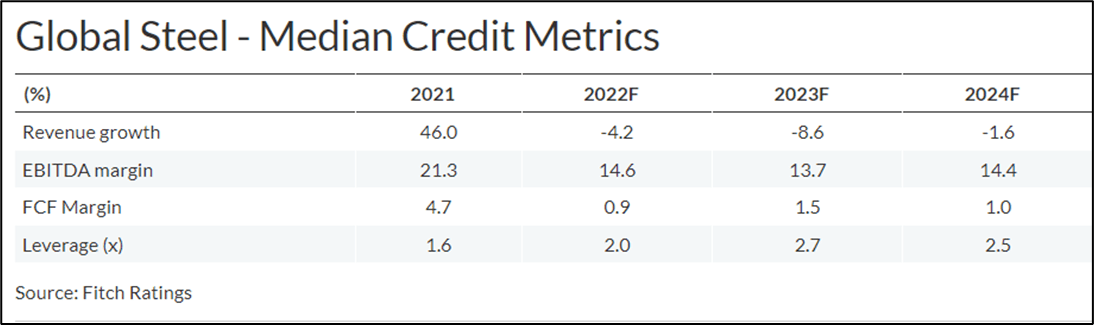

Macro-economic forces dragging on steel prices make POSCO's expansion into battery minerals, chemical process technology and sustainable energy even more important. Median credit metrics as per Fitch are forecast to see an ongoing normalization as the world recovers from the post Covid inflationary boom.

Median revenue growth is expected to decline in 2023, with margins not far behind. Expect 2024 to witness slight improvements in revenues and a progressive deleveraging industry-wide as key players look to decouple debt laden balance sheets in an environment of tight money.

{kind=link}

Financials

POSCO is a relatively mature business with high fixed costs, sizable leverage, and comparably low margins. The firm has had stable revenues for the past 10 years, hovering between US $50B-$70B annually. EBITDA margins have been stable too at around 10% with only a covid induced price boom (16% EBITDA FY2021) being an exception to the rule.

Net income margins are reflective of the nature of the industry (~3%) characterized by high volume, big operating leverage and somewhat fragmented nationalistic markets. The company is a cash machine, consistently producing between US $3B-$7B in cash flow from operations over the past decade.

Currently in a steady state, future returns for the Korean metals venture are likely to be premised on the success generated from newer, growthier business lines focused on sustainability and decarbonization. Inflationary pressures have seeped into POSCO's cost of revenues with the Korean giant posting roughly 9% gross profit margins, down from ~15% FY 2021.

The SARS-Cov2 pandemic accounted for a sizable chunk of the firm's good financial fortune so any analysis should look to discount a standout performance during this period.

Research and development spend increased by almost 40% (US $142M FY2022 v $103M FY2021) underpinning some of the firm's aspirations to develop green hydrogen for steel making and branch out into new energy. POSCO's substantial debt load comes with an annual interest bill of $482M, offset only marginally by $227M in interest and investment income.

The company has been impacted by tightening monetary policy but continues to manage rolling over its debt, accessing capital markets and managing liquidity. There is enough cash on tap ($6.3B in cash and $8.4B in marketable securities) for the company to navigate changes in credit markets. Notwithstanding, inventory remains a sizable chunk of current assets ($12B FY2022), up from $8.7B FY2020.

POSCO does have $351M in goodwill on the balance sheet but the company has made efforts to impair this over the last few years. The balance sheet holds common equity of $41.7B, most of which is made up in retained earnings. All in, the company is a mature state business running profitable operations while traversing a relatively volatile period in the economy.

Risk Profile

An investment in POSCO holds risk, specifically for near term investors looking to reap near term capital gains. With current macro-economic uncertainties clouding activity in 2023, particularly in the steel market, our outlook is premised on a holding period of several years.

2024 is likely to see a return to growth and improved market dynamics but near term, POSCO's cash cow - steel making - is likely to be hampered by dampened economic sentiment. The company is intrinsically linked to South Korea's economic output which presents challenges, particularly given the country's declining GDP growth rate, declining manufacturing PMIs, and dampened economic sentiment shared by regional trading partners.

South Korea is a net importer of raw materials required for production, so POSCO remains particularly exposed to commodity prices that are likely to increase on a weaker US dollar into the back end of the year.

Key Takeaways

POSCO is a steel maker undertaking a period of corporate transformation that will see the firm focus on technologies around sustainability and decarbonization.

The company is already making efforts to expand into battery minerals, target investments upstream in the value chain and de-risk by diversifying out of a single sector. That is great news for the long term as 2023 is likely to be somewhat shaky for global steel markets.

For further details see:

POSCO: South Korean Steel Giant Undergoing Period Of Transformation